Sample Category Title

Daily Wave Analysis: What Is Next After Bullish EUR/USD Reaches 1.25?

Currency pair EUR/USD

The EUR/USD bullish breakout has reached the main target at 1.25 as mentioned in our analysis throughout the week. Price bounced at the round 1.25 level and trend line (orange) but the bearish price action could be just a pullback within a larger wave 3 (pink)

The EUR/USD already bounced at the 23.6% Fibonacci level of wave 4 (green) but the bearish price action lead to a potential bearish ABC (blue) zigzag or flat.

Currency pair GBP/USD

The GBP/USD managed to reach 1.43 before making a strong bearish retracement. The bullish price action has been labelled as a wave 3 (green) due to its significant momentum. The current pullback could therefore find support at the Fibonacci levels of wave 4 vs 3.

The GBP/USD already bounced at the 23.6% Fibonacci level of wave 4 (green) but the bearish price action lead to a potential bearish ABC (blue) zigzag or flat.

Currency pair USD/JPY

The USD/JPY has reached and bounced at the -61.8% Fibonacci target. The bullish bounce could indicate a reversal and completion of wave B or 2 (light purple).

If the USD/JPY is building areversal, then price could be in a wave 1-2 (blue) and it would not break the bottom of wave 1 which is the 100% Fibonacci level of wave 2 vs 1.

Market Update – Asian Session: Cautious Trading Ahead Of Advance Q4 GDP Data Out Of The UK And US

Headlines/Economic Data

General Trend:

Japan Finance Min Aso declines to address US officials comments related to currencies

Japan Core CPI holds steady in Dec

US dollar (USD) trades with a generally weaker tone in Asia: PBoC continues to fix yuan at multi-year high

PBoC skipped open market operation (OMO) for second straight session; cited relatively high liquidity level in banking system

Australia/New Zealand

ASX 200 closed for holiday

China/Hong Kong

Hang Seng opened +0.6%, Shanghai Composite -0.4%

Hang Seng Information Technology Index +1.8%, Property/Construction +1.5%, Financials +1.2%; Energy -1.8%

Leshi Internet [300104.CN]: Trades limit down (-10%) for 3rd straight session

(CN) China Dec Industrial Profits Y/Y: 10.8% v 14.9% prior: 2017 industrial profits CNY7.52T, +21% y/y (fastest growth since 2012)

(CN) PBOC SETS YUAN REFERENCE RATE AT 6.3436 V 6.3724 PRIOR (strongest CNY fix since Nov 5th, 2015)

(CN) PBoC: Skips OMO (2nd straight session) vs skipped prior; Net drain CNY270B v CNY120B drain prior; Weekly Net drain CNY320B v CNY590B injection w/w

(CN) Previously announced PBoC targeted RRR cut* has limited impact on liquidity; PBoC to withdraw liquidity in open market operations (OMOs); PBoC may adjust OMO for deleveraging. – Xinhua (**Reminder: The targeted RRR cut that was announced last September, became effective on Jan 25th)

(CN) 'Window' not open yet for PBoC benchmark rate hike (in line with prior comments) - China Securities Journal

(CN) China NDRC: To crack down on irregularities in oil refining sector: Will focus on violations such as illegal crude oil purchases and processing.

(CN) China Finance Ministry (MOF): To swap CNY1.73T in existing local government debt by Aug

(CN) China NDRC: To allow banks to create private-equity funds to conduct market-based debt for equity swaps

(CN) China Finance Ministry Researcher Liu Shangxi: Sees next major source of China government debt is pension deficit.

South Korea

Kospi opened -0.1%

Hyundai Mobis [012330.KR]: Down over 8% (reported unexpected Q4 net loss)

Hyundai Motor [005380.KR] Has declined by over 4% (reported Q4 earnings on Thursday)

E-Mart [139480.KR]: +12.5% (Affinity and BRV to invest over KRW1T in E-Mart Online)

South Korea Unification Ministry: North Korea may stage 'threatening' military parade on Thursday, Feb 8th anniversary - South Korean Press

South Korea and the US are planning to hold second meeting on Free Trade Agreement (FTA) revision Jan 31-Feb 1st, expected to continue to focus on modifications and amendments

South Korea Trade Ministry comments on recently announced US tariffs on washing machines: To prepare steps to increase local demand for washers

Japan

Nikkei 225 opened +0.4%; closed -0.2%

Rakuten [4755.JP] Gained over 3% (announced online grocery delivery service with Wal-Mart)

Komatsu [6301.JP] Gained over 1.5% on session (Caterpillar reported earnings on Thursday)

Fujitsu [6702.JP]: +1.3% (confirmed talks regarding mobile phone business)

Isetan [3099.JP]: +1% (May report results later today)

Fanuc [6954.JP]: Flat (May report earnings today)

Shin-Etsu Chemical [4063.JP]: Flat (May report earnings later today)

Koito Mfg Co [7276.JP]: +1.7%, May report earnings today

JAPAN DEC NATIONAL CPI Y/Y: 1.0% V 1.1%E; EX-FRESH FOOD (CORE) Y/Y: 0.9% V 0.9%E

Japan Jan Tokyo CPI Y/Y: 1.3% v 1.1%e; Ex-Fresh Food (Core) Y/Y: 0.7% v 0.8%e

BoJ released Minutes of Dec 20-21 Policy Meeting: Most Members (Price momentum is being maintained; Appropriate to continue 'powerful' monetary easing); Some Members (Said must continue to look at both positive and negative effects of current policy, including effects on financial system) ; One Member (Said functioning of financial intermediation had not been impaired yet, but bank profits show effects of low rates on strength of financial institutions had been accumulating; Said BoJ should keep policy steady now, but might need to consider adjusting level of interest rates when economy, prices were expected to continue improving)

Japan Fin Min Aso: Reiterates G7 agreement is to avoid targeting FX for the sake of competitiveness; won't comment on other countries' remarks on FX

Former Japan FX Official Sakakibara ('Mr Yen'): Expects USD/JPY to trade toward ¥100 by end of 2018; USD/JPY at ¥100 or ¥105 not a major problem; BoJ Gov Kuroda may start talking about an exit in 2-3 years

Other Asia

(SG) Singapore Dec Industrial Production M/M: -2.0% v +2.4%e; Y/Y: -3.9% v +0.8%e

(TH) Thailand Central Bank Gov Veerathai: To be more 'stringent' in monitoring Baht (THB); prepared to add more measures if Baht moves are 'unusual'

North America

US equity markets ended mostly higher: Dow +0.5%, S&P500 +0.1%, Nasdaq -0.1%, Russell 2000 +0.1%

S&P500 Utilities +1.5%, Health Care +0.8%; Energy -0.8%

Intel [INTC]: Gained over 3% afterhours: Reports Q4 $1.08 v $0.86e, Rev $17.1B v $16.3Be; Raises FY18 capex plan materially; raises quarterly dividend by 10% to $0.30 from $0.2725 (2.65% yield); Guides Q1 EPS ~$0.65-0.75 v $0.73e, Rev $14.5-15.5B v $15.1Be

Starbucks [SBUX]: Down over 4% afterhours: Reports Q1 $0.65 v $0.57e, Rev $6.07B v $6.14Be; Affirms FY18 global comp sales growth +3-5% (prior +3-5%); to open 2,300 new stores (prior 2,300)

(US) Pres Trump: the Dollar will strengthen as the economy does; ultimately I want to see a strong dollar; Mnuchin comments this week were out of context - CNBC interview excerpts

(US) President Trump said to have 'ordered' special investigator Mueller fired in June 2017 – NY Times

Looking Ahead: US Dec Durable Goods and Q4 US Advance GDP due for release; Canada Dec CPI

Corporate earnings are expected out of companies including AbbVie, Air Products, Colgate, Honeywell, Lear, Moog, PolyOne, Rockwell Collins

Europe

(EU) ECB sources: ECB council divided about next move as the rise of the Euro complicates the forecasts; Some want to remove the easing bias in March; others prefer June for next policy adjustment; Others are more hesitant and want to fully reassess at the next meeting – press

(ES) Spain govt reportedly intends to move forward with plan to block separatist Puigdemont candidacy for regional Catalan president - press

(IE) Ireland Central Bank: Raises 2018 GDP growth forecast to 4.4% v 3.9% prior; raises 2017 GDP growth forecast to 7.0% v 4.9% prior; economy is not overheating at present; Brexit risks may have moved slightly in a benign way.

Looking Ahead: Euro Zone Dec M3 Money Supply and Private Sector Loans, along with UK Q4 Advance GDP due for release

Levels as of 01:00ET

Hang Seng +1.4%; Shanghai Composite +0.3%; Kospi +0.3%

Equity Futures: S&P500 +0.2%; Nasdaq100 +0.3%, Dax +0.2%; FTSE100 +0.1%

EUR 1.2370-1.2434 ; JPY 109.34-109.77; AUD 0.8005-0.8058 ;NZD 0.7292-0.7345

Feb Gold +0.3% at $1,351/oz; Feb Crude Oil -0.2% at $65.36/brl; Mar Copper +0.3% at $3.212/lb

The First Estimate Of GDP Growth In Q4 Is Due Out

Market movers today

On the political front , market focus will be on the meetings at the World Economic Forum at Davos, where President Trump will make a special address at 14:00 CET. The address is particularly interesting in the wake of this week's statement from the US administ ration on the USD and trade protectionism. Furthermore, in the wake of yest erday's ECB meeting, the market will assess the latest ECB stance, when board member Benoît Coeuré speaks.

In the US, we are due to get the first release of GDP growth in Q4. According to the At lanta Fed GDPNow indicator, growth was 3.2% q/q annualised while the NY Fed GDP Nowcast indicator suggests growth was 3.9%. If the annualised growth rate exceeds 3.2% q/q AR, it will be the strongest pace since 2014. Consensus is 3.0% right now. In addition, the number for the US preliminary core capex in December is being released, which we expect to show that business investment is still recovering.

In the UK, the first estimate of GDP growth in Q4 is due out . PMIs suggest GDP growth was 0.4-0.5% but the NIESR GDP estimate says it could have been as high as 0.6%. We estimate GDP growth was 0.4% but given the indicators there are upside risks to this forecast . We estimate annual growth in GDP has slowed to 1.4% y/y, the slowest since Q2 12.

In Sweden, December prints on retail sales, household lending and trade balance are due.

Selected market news

The ECB left its policy measures and forward guidance unchanged yesterday and reiterated that policy rates would remain at current levels for an extended period and well past the horizon of asset purchases. The press conference confirmed our view that a change to the asymmetric communication on the purchase programme will come at the 8 March meeting. See ECB review - Language to be revisited in March, 25 January, for details.

The ECB/MarioDraghi sent a positive signal on growth for the eurozone economy, and the impact on the fixed income markets from the press conference was quite negative with a solid rise in the 5Y and 10Y segment and flat tening between 5Y and 30Y.

The exchange rate was mentioned twice in the introductory statement as a source of uncertainty that requires monitoring, a sentence that has not been used since September 2017. Draghi also sent a very clear critique towards the US regarding its weak US dollar (USD) policy. However, the euro still rose sharply and EUR/USD broke above 1.25 during the press conference. Later last night , US president Trump dismissed Steven Mnuchin's dollar comment saying that he ultimately wants to see a stronger dollar. The USD gained on Mr Trump's comments on the greenback and reversed earlier loses in the DXY index and EUR/USD fell back below 1.24%.

The long continuous upward trend in Japanese inflation stopped in December as CPI inflation excluding fresh food stood unchanged at 0.9% y/y. Stripping out energy (and fresh food), prices climbed 0.3% y/y. Hence, underlying inflation pressure remains weak and with inflation still not even halfway to the Bank of Japan's target , it supports our view that the BoJ will keep its current monetary policy programme unchanged in the coming 12 months.

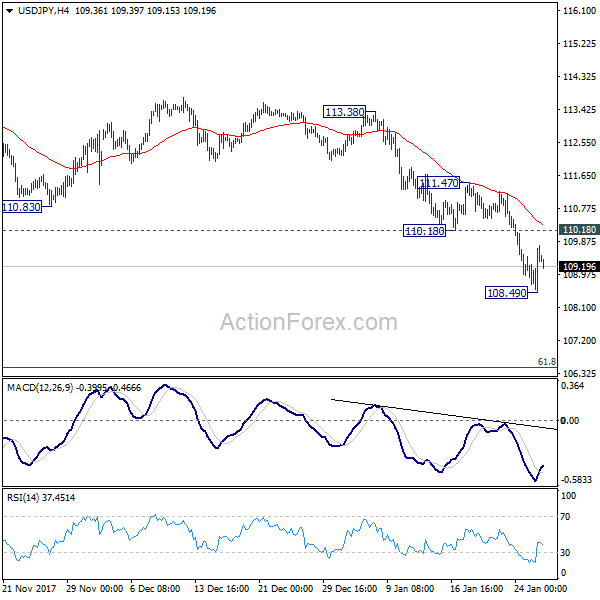

USD/JPY Daily Outlook

Daily Pivots: (S1) 108.70; (P) 109.19; (R1) 109.90; More...

USD/JPY recovers after forming a temporary low at 108.49 and intraday bias is turned neutral first. At this point, deeper fall is still expected as long as 110.18 support turned resistance holds. Below 108.49 will target next fibonacci support at 106.48. Nonetheless, break of 110.18 will be the first sign of near term reversal and will turn bias back to the upside for 111.47 resistance.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD?JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).

Dollar Stabilizing as Trump Said He Wants a Strong Currency

After being pressured for most of the week, Dollar is trying to stabilize after US President Donald Trump said he wants a strong Dollar. But so far, there is little sign of sustainable rebound yet. The greenback is still vulnerable to another selloff. The key to whether Dollar could reverse recent fortune might lie in Q4 GDP. Sterling remains one of the strongest one this week and will also look into UK GDP for more strengthen. Euro jumped overnight after ECB President Mario Draghi's comment but there was no follow through buying.

Trump said he "wants" a strong Dollar

Trump said in a CNBC interview in Davos, Switzerland, that he wants to "see a strong dollar". He said that Treasury Secretary Steven Mnuchin's comments earlier this week were "taken out of context". Trump added that "no. 1 I don't like talking about it because frankly nobody should be talking about it. It should be what it is, it should also be based on the strength of the country - we are doing so well. Our country is becoming so economically strong again and strong in other ways too, by the way that the dollar is going to get stronger and stronger and ultimately I want to see a strong dollar." Dollar gained some footing after Trump but there is no sign of a reversal yet.

SNB Jordan: Forex usually focuses on fundamentals

SNB Chairman Thomas Jordan said in Davos that he didn't believe trade war is imminent. He noted that "every time monetary policy changes somewhere, the spillovers are bigger than in the past, because the interest rate instrument is not available as it used to be." And, therefore, "maybe we should not focus on daily volatility". He added that "usually the foreign exchange market will refocus on fundamentals again and also correct again." Regarding the Swiss Franc, he said that "what we don't look at is specific exchange rates" Ad, "we look at all the exchanges together and see what is the impact on the Swiss economy and then, if necessary, decide whether to intervene or not."

ECB maintained policy and forward guidance unchanged

Yesterday, ECB left the policy rates unchanged, with the main refinancing rate, the marginal lending rate and the deposit rate staying at 0%, 0.25% and -0.40% respectively. The pace of asset purchases also stayed unchanged at 30B euro per month until September, or beyond, if necessary. President Mario Draghi attempted to downplay speculations that the central bank would soon adjust the forward guidance, as interpreted by many following the December meeting minutes. Meanwhile, he stressed that any rate hike would be 'well past' the end of asset purchases. Draghi also warned of the impacts of the strong euro on growth and complained about the US for talking down the greenback at the World Economic Forum. More in Euro Rallied Further Despite Draught's Attempt To Downplay Forward Guidance Adjustment

On the data front

Japan national CPI core was unchanged at 0.9% yoy in December. Tokyo CPI core slowed to 0.7% yoy in January. Corporate services price rose 0.8% yoy in December. Eurozone M3 will be released in European session. But main focus will be on UK Q4 GDP. Later in the day, Canada will release CPI. US will release Q4 GDP and durable orders.

USD/JPY Daily Outlook

Daily Pivots: (S1) 108.70; (P) 109.19; (R1) 109.90; More...

USD/JPY recovers after forming a temporary low at 108.49 and intraday bias is turned neutral first. At this point, deeper fall is still expected as long as 110.18 support turned resistance holds. Below 108.49 will target next fibonacci support at 106.48. Nonetheless, break of 110.18 will be the first sign of near term reversal and will turn bias back to the upside for 111.47 resistance.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD?JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Dec | 0.90% | 0.90% | 0.90% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Jan | 0.70% | 0.80% | 0.80% | |

| 23:50 | JPY | Corporate Service Price Y/Y Dec | 0.80% | 0.80% | 0.80% | |

| 23:50 | JPY | BOJ Minutes | ||||

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Dec | 4.90% | 4.90% | ||

| 09:30 | GBP | Index of Services 3M/3M Nov | 0.40% | 0.30% | ||

| 09:30 | GBP | GDP Q/Q Q4 A | 0.40% | 0.40% | ||

| 13:30 | CAD | CPI Y/Y Dec | 1.90% | 2.10% | ||

| 13:30 | CAD | CPI Core - Trimmed Y/Y Dec | 1.80% | |||

| 13:30 | CAD | CPI Core - Common Y/Y Dec | 1.50% | |||

| 13:30 | CAD | CPI Core - Median Y/Y Dec | 1.90% | |||

| 13:30 | USD | GDP Annualized Q/Q Q4 A | 3.00% | 3.20% | ||

| 13:30 | USD | GDP Price Index Q4 A | 2.30% | 2.10% | ||

| 13:30 | USD | Durable Goods Orders Dec P | 0.90% | 1.30% | ||

| 13:30 | USD | Durables Ex Transportation Dec P | 0.60% | -0.10% |

Aussie Reverses Its Losses In The Asian Session

For the 24 hours to 23:00 GMT, the AUD declined 0.55% against the USD and closed at 0.8011.

LME Copper prices rose 2.4% or $169.0/MT to $7112.0/MT. Aluminium prices rose 1.0% or $21.5/MT to $2237.5/MT.

In the Asian session, at GMT0400, the pair is trading at 0.8056, with the AUD trading 0.56% higher against the USD from yesterday’s close.

Earlier today, in China, Australia’s largest trading partner, industrial profits rose 10.8% on an annual basis in December, after recording a rise of 14.9% in the previous month.

The pair is expected to find support at 0.8001, and a fall through could take it to the next support level of 0.7946. The pair is expected to find its first resistance at 0.8115, and a rise through could take it to the next resistance level of 0.8174.

Next week, investors would eye Australia’s consumer price index, AiG performance of manufacturing index, the NAB business confidence index and building approvals data.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

ECB Kept Its Monetary Policy Unchanged, Warned Over Surging Euro

For the 24 hours to 23:00 GMT, the EUR declined 0.14% against the USD and closed at 1.2383, after the European Central Bank (ECB) President, Mario Draghi expressed worries over volatility in the Euro.

The ECB, in a widely expected decision, opted to leave the benchmark interest rate unchanged at 0.00% and reiterated its commitment to keep its ultra-easy monetary policy steady for an extended period and well past the end of its bond buying programme, until a self-sustaining rise in inflation is achieved. In a post-meeting statement, the ECB Chief, Mario Draghi, stated that recent economic data confirmed a “robust pace” of economic expansion, adding that inflation will likely rise in the medium term. However, he characterised the recent surge in the Euro as a source of uncertainty for the inflation outlook.

On the economic front, Germany's Ifo business climate index surprised to the upside, after it advanced to a fresh record high level of 117.6 in January, vindicating that firms remain highly optimistic about their growth prospects despite the lack of a new government four months after a general election. Market participants had envisaged the index to drop to a level of 117.0, after recording a level of 117.2 in the previous month. Moreover, the nation's Ifo current assessment index unexpectedly advanced to a level of 127.7 in January, defying market anticipation for a drop to a level of 125.3. The index had registered a level of 125.4 in the previous month.

On the other hand, the nation's Ifo business expectations index declined more-than-estimated to a level of 108.4 in January, after recording a reading of 109.5 in the prior month. Other data indicated that the nation's GfK consumer confidence index unexpectedly advanced to a level of 11.0 in February, confounding market expectations for the index to remain steady at a level of 10.8.

The greenback gained ground against a basket of major currencies, sparked by comments from the US President, Donald Trump that he favoured a stronger US Dollar and stated that the currency would strengthen along with the US economy.

Macroeconomic data showed that first time claims for the US unemployment benefits climbed less-than-anticipated to a level of 233.0K in the week ended 20 January, compared to a revised reading of 216.0K in the previous week. Investors had expected initial jobless claims to rise to a level of 235.0K. Further, the nation's new home sales eased 9.3% on monthly basis to a level of 625.0K in December, hitting its lowest level in more than a year. Markets had expected for a drop to a level of 675.0K, compared to a revised reading of 689.0K in the previous month.

On the other hand, the nation's leading indicator registered a more-than-expected rise of 0.6% in December, compared to a revised gain of 0.5% in the previous month.

In the Asian session, at GMT0400, the pair is trading at 1.2428, with the EUR trading 0.36% higher against the USD from yesterday's close.

The pair is expected to find support at 1.2349, and a fall through could take it to the next support level of 1.2270. The pair is expected to find its first resistance at 1.2522, and a rise through could take it to the next resistance level of 1.2616.

With no crucial macroeconomic releases in the Euro-zone today, investors would focus on the US flash 4Q GDP numbers as well as advance goods trade balance and durable goods orders, both for December, scheduled to release later in the day.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

UK’s BBA Mortgage Approvals Hit A Nearly 5-Year Low In December

For the 24 hours to 23:00 GMT, the GBP declined 0.78% against the USD and closed at 1.4125, after UK's mortgage approvals registered an unexpected drop in December.

Data showed that Britain's BBA mortgage approvals declined to its lowest level since April 2013, after it fell to a level of 36.12K in December, intensifying concerns about the health of the nation's housing market. In the prior month, mortgage approvals had registered a revised level of 39.01K, while markets were expecting for a rise to a level of 39.80K.

In the Asian session, at GMT0400, the pair is trading at 1.4190, with the GBP trading 0.46% higher against the USD from yesterday's close.

The pair is expected to find support at 1.4067, and a fall through could take it to the next support level of 1.3944. The pair is expected to find its first resistance at 1.4329, and a rise through could take it to the next resistance level of 1.4468.

Trading trend in the Pound today is expected to be determined by UK's crucial 4Q GDP data and BoE Governor Mark Carney's speech, set to release in a few hours.

The currency pair is trading below its 20 Hr moving average and showing convergence with its 50 Hr moving average.

Few Officials Saw Future Need To Raise Rates, Slow Asset Buying: BoJ Minutes

For the 24 hours to 23:00 GMT, the USD rose 0.37% against the JPY and closed at 109.60.

In the Asian session, at GMT0400, the pair is trading at 109.38, with the USD trading 0.2% lower against the JPY from yesterday's close.

Minutes of the Bank of Japan's (BoJ) December monetary policy meeting showed that majority of board members believed that it was appropriate to stick to the central bank's current monetary policy stance as inflation remains far from its 2.0% target. However, some officials expressed a need to consider raising interest rates or reducing purchases of risky assets if the economic recovery continued.

Data released overnight showed that Japan's national consumer price index (CPI) advanced less-than-anticipated by 1.0% on an annual basis in December, adding to the complication for the central bank as it struggles to boost inflation in the nation. The CPI had registered a gain of 0.6% in the prior month, while markets were expecting for a rise of 1.1%.

The pair is expected to find support at 108.66, and a fall through could take it to the next support level of 107.95. The pair is expected to find its first resistance at 109.93, and a rise through could take it to the next resistance level of 110.49.

Going ahead, traders would await the release of Japan's jobless rate, flash industrial production and retail trade data, all due to release next week.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.

Swiss Franc Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.36% against the CHF and closed at 0.9423.

In the Asian session, at GMT0400, the pair is trading at 0.9391, with the USD trading 0.34% lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9304, and a fall through could take it to the next support level of 0.9218. The pair is expected to find its first resistance at 0.9463, and a rise through could take it to the next resistance level of 0.9536.

Moving ahead, traders would focus on Switzerland’s ZEW expectations survey, real retail sales, the manufacturing PMI and SECO consumer confidence data, all scheduled to be released next week.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.