Sample Category Title

EURUSD Intraday Analysis

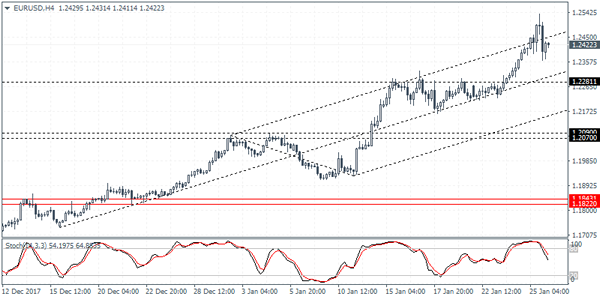

EURUSD (1.2422): The EURUSD touched a fresh 4-year high as the intraday rally saw prices reaching for 1.2537. However, the euro gave back the gains rather quickly with the daily session closing with a doji candlestick pattern. Currently, we see some retracement taking place but the gains could be short lived. Initial support is seen at 1.2281 which could be tested if the downside momentum increases. A break down below this level could see the EURUSD extend the declines down to 1.2090 - 1.2070 levels. To the upside, unless price action closes strongly above the 1.2400 handle on the daily basis, we expect the EURUSD to turn flat near the current highs.

USD Whipsaws On Trump’s Comments, Q4 GDP Coming Up

The U.S. dollar was met with another volatile day as late in the day the U.S. President sought to clarify the Treasury Secretary Mnuchin's comments on preferring a weaker dollar. The greenback was seen extending declines earlier in the day as the ECB left the monetary policy unchanged. With Mario Draghi not addressing the exchange rate of the euro, the common currency briefly rallied to a fresh 4-year high only to reverse the gains by the close of business.

The economic calendar was sparse besides the ECB meeting. Canada's core retail sales continued to accelerate, rising 1.6% on the month and beating estimates of a 0.8% increase. Headline retail sales however rose just 0.2% and missed estimates of a 0.7% increase.

Looking ahead, GDP data across the UK, Canada and the U.S. will keep the markets busy. The UK's preliminary GDP is expected to show that the economy advanced 0.4% on the fourth quarter. Canada will be releasing the inflation data which is expected to show a 0.3% decline erasing the increase from the previous month. The U.S. advance GDP report is expected to show a modest increase of 3.0% in the GDP. Later in the day, BoE and the BoJ governors will be speaking at the World Economic Forum in Davos.

Currencies: Dollar Receives Lifeline From President Trump

Sunrise Market Commentary

- Rates: Test of key yield levels in US and Europe continues

Yesterday, US and German 10-year yields again tested key resistances levels as ECB’ Draghi sounded optimistic on (EMU) growth. However, a sustained break didn’t occur as positive comments from President Trump on the dollar eased pressure on US Treasuries. Even so, a break might still occur. Today’s US GDP data and a speech from President Trump in Davos are the next potential triggers. - Currencies: Dollar receives lifeline from President Trump

Yesterday, EUR/USD jumped north of 1.25 during the ECB press conference even as ECB’s Draghi mentione the strong euro as a source of uncertainty. Surprisingly, president Trump finally blocked the rise of EUR/USD as he said to favour a strong US dollar. Are the comments from President Trump a harbinger of some calm to turn to USD trading?

The Sunrise Headlines

- US equities ended the session little changed with the Dow outperforming as investors assessed the potential implications from recent gyrations in the interest rate and FX markets. Asian equity markets are trading mixed with China and Korea outperforming.

- U.S. President Trump said he ultimately wants the dollar to be strong, lifting the greenback and contradicting comments made by Treasury Secretary Steven Mnuchin earlier this week .

- Britain's finance minister Hammond called for a modest Brexit that would keep the UK as closely aligned as possible with the EU after its 2019 exit. However sources in May's office rebuked Hammond, saying the changes that Britain will undergo cannot be described as "very modest".

- Japan's inflation in December continued to lag a strong economic revival. Core inflation rose 0.9% Y/Y, unchanged from November - well off the Bank of Japan's 2 percent price goal.

- Profits for China's industrial firms rose at the slowest pace in a year in December as anti-smog curbs hit activity, but profits clocked the fastest annual rise in six years as cost cutting and a construction boom helped businesses in 2017.

- Ireland's central bank hiked its 2018 growth forecasts, predicting a faster rate of expansion for next year than the government has pencilled in. The CB expects gross domestic product to grow by 4.4 percent this year and by 3.9 percent in 2019.

- The calendar is well filled today. In EMU, the M3 money supply data and the ECB Survey of professional forecasters will be published. The UK will provide a first estimate of Q4 GDP growth. The US calendar contains the Q4 GDP, durable orders, the goods trade balance and inventory data. Markets will also keep a close eye on speeches from Davos, including from US President Trump.

Currencies: Dollar Receives Lifeline From President Trump

Dollar receives lifeline from President Trump

The dollar and the euro had a roller-coaster ride yesterday. EUR/USD spiked again sharply higher during the ECB press conference. ECB’s Draghi mentioned FX volatility as a source of uncertainty. He also said that some recent communication on FX was not in line with what was agreed at the level of the IMF. It didn’t to prevent a resumption of the rise of the euro. EUR/USD jumped above 1.25, supported by a positive economic assessment of the ECB. Euro strength was the dominant trend, but some underlying USD weakness was also at work. Later, the dollar received unexpected support from US president Trump. He wants to see a strong dollar, mirroring the strength of the US economy. EUR/USD tumbled from 1.25+ to below 1.24 and closed the session at 1.2396. USD/JPY finished the day at109.41, after testing 108.50 intraday.

Overnight, Asian equities are trading mixed, mirroring an indecisive close in the US. Some clam also returned to the FX market. EUR/USD hovers in the low 1.24 area. USD/JPY is trading in the mid 109. The yen weakened slightly on soft Japanese inflation data, but rebounded later.

The eco calendar is well filled today, especially in the US, with the first estimate of US Q4 GDP, durable orders and the goods trade balance. The GDP report and the trade balance data are interesting from an FX point of view. Markets will look out whether US growth surpasses 3.0%. The price deflators will also be closely watched (core PCE expected to rise from 1.3% to 1.9%). With the focus on international trade relations, the US trade deficit might get more attention than is usually the case. Evidently, most attention from (FX) markets will go to Davos. President Trump is expected the ‘defend’ its ‘America first’ agenda. Yesterday’s comments suggest that, if needed, he is more inclined to use specific trade measures, rather than aiming for a weaker dollar. Key question for EUR/USD trading is whether yesterday’s spike was some kind of an exhaustion move. Global USD strength might be mitigated after President Trump’s comments. On the other hand, the positive ECB assessment on the economy keeps the debate on a less easy ECB policy on the radar. If EUR/USD today can stay away from the 1.2537/1.2596 area, some consolidation on the euro rally/USD decline might be on the cards. For now, the jury is still out.

Yesterday, EUR/GBP extensively tested the 0.8690 support area, but the test was rejected. Euro strength during the ECB press conference was one factor. However, indications of ongoing discord within the UK government on Brexit maybe also dampened recent hope on a soft Brexit, causing some profit

taking on sterling longs. EUR/GBP closed the session at 0.8764. Today, the focus is on the first estimate of the UK Q4 GDP. A modest 0.4% Q/Q and 1.4% Y/Y is expected. If confirmed, these data suggest that the BoE should be in no hurry to raise rates anytime soon. Yesterday’s price action suggest that 0.8690 is indeed a strong support area. We don’t see a trigger for a break anytime soon.

EUR/USD: Was yesterday’s intraday reversal a sign of an exhaustion move

USDJPY Intraday Direction Defined By 108.98 Level

The U.S dollar has encountered extreme volatility against the Japanese yen currency overnight, with price-action spiking towards the 109.76 level, following U.S President Donald Trump’s comments on the U.S dollar. Speaking in the World Economic Forum, President Trump said the value of the U.S dollar will get much stronger, causing the USDJPY pair to rally over one-hundred pips from the 108.50 support level. Price-action is currently trading around the 109.20 level, with the greenback now giving back gains.

The USDJPY pair is likely to move higher while price-action trades above the 108.98 level. Upside targets for buyers remain 109.76 and 110.00.

Should price-action on the USDJPY pair decline below the 108.98 level, further losses towards 108.60 and 108.20 seem possible.

EURUSD Buyers Look To The 1.2432 Level

The euro has fallen sharply lower from the 1.2500 level against the greenback, after U.S President Donald Trump endorsed having a stronger U.S dollar. After hitting a new three-year trading high, at 1.2537 on Thursday, the EURUSD pair crashed towards the 1.2564 level on the back of President Trump’s comments. Price-action is now gaining bullish momentum above the 1.2400 handle and trading around the 1.2440 region, as financial markets stay focused on the next directional move in the U.S dollar index.

The EURUSD pair retains its intraday bullish bias while price-action trades above the 1.2432 level, further upside towards 1.2500 and 1.2537 seems likely.

Should the EURUSD pair decline below the 1.2432 level, we may see further selling towards the 1.2400 and 1.2364 support levels.

Concerns About Ripple Mounts

In the past few days, Ripple's price against the dollar has remained unchanged. Partly, this is because of new concerns about the currency and its valuation.

Some financial experts have continued to question Ripple's listing alongside bitcoin and ethereum. Their argument is that its technology is not decentralized unlike that of other cryptocurrencies. As such, having a centralized platform makes no sense for its claim to be a blockchain platform. For miners, there is no method of mining the ripple 'coins'.

Multiple people like Jens Bader, a successful cryptocurrencies trader and founder of a company called MuchBetter have raised these concerns. Recently, he said:

'It might be a good complimentary currency to bitcoin and ethereum, but since it is a centralised system, it does not live up to the brief of what a cryptocurrency is meant to do, and the USPs of blockchain technology.'

Remember, Ripple has a different role than bitcoin. Its main role is to ease cross-border settlement among financial institutions. On its part, bitcoin is positioned as a digital currency, which people can use to make transactions.

Therefore, given its centralized system, some have argued against its valuation. According to Coinmarketcap, Ripple is the third largest 'cryptocurrency' with a valuation of more than $51 billion.

In the just released ratings by Weiss, Ripple received a C-rating which is similar to that of bitcoin.

As shown below, Ripple is currently trading at 1.3040 level. At this level, it is at the apex of a symmetrical trading pattern, which means that a breakout can happen in either direction. It is also trading at the same 50 and 14-day moving average. All this is an indication that the pair could go in either direction.

High Profile US Data Headlines Friday Session

A steady stream of economic data will make the rounds on Friday, rounding out a highly active week in the markets that saw the US dollar plunge to three-year lows.

Action on Friday begins at 07:45 GMT with reports on French consumer confidence and the business climate. Both indicators will be used to gauge the strength of the Eurozone's second-largest economy.

The market will quickly shift its focus to the United Kingdom, whose government will unveil revised fourth quarter GDP figures. The revised estimate is forecast to show 0.4% quarter-on-quarter growth. That translates into year-over-year growth of 1.4%.

In the United States, the Department of Commerce will release the final estimate of fourth quarter GDP at 13:30 GMT. The world's largest economy is projected to grow 3% annually in the fourth quarter.

In a separate release Friday, Commerce will report on durable goods orders for the month of December. Orders for manufactured goods meant to last three years or more are expected to climb 0.8% after rising 1.3% the month before.

Government economists will also report on the goods trade balance for December. The monthly report is expected to show a narrowing of the trade deficit to $68.6 billion from $70 billion in November.

North of the border, the Canadian government will report on the December consumer price index, a key measure of inflation.

In monetary policy, European Central Bank (ECB) governor Benoit Coeure will deliver a speech at 10:00 GMT. Three hours later, the Federal Reserve's James Bullard will also deliver a speech.

In currencies, the US dollar index continued its long descent in Friday's Asian session, where it fell to more than three-year lows. The dollar index (DXY) touched a session low of 89.12 before recovering near 89.20. The world's most actively traded currency is down more than 3% since the new year. More declines are expected as the Trump administration wrestles Canada and Mexico for a new trade agreement to replace NAFTA.

EUR/USD

The euro extended its winning streak on Friday, climbing 0.4% to 1.2427 US. The common currency is enjoying strong upside thanks to a weak US dollar and favorable economic developments throughout the euro area.

GBP/USD

Cable resumed its uptrend on Friday, climbing 0.5% to 1.4185. The GBP/USD continues to break multi-year highs, although the bulk of the gains have been driven by renewed dollar weakness. This trend is expected to continue for the foreseeable future.

USD/JPY

The dollar also lost ground against the Japanese yen, with the USD/JPY falling 0.2% to 109.39. The pair briefly traded below 109.00 on Thursday before staging a late recovery. However, the outlook remains firmly tilted to the downside as the two currencies continue to diverge.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 154.04; (P) 155.06; (R1) 155.70; More...

With 153.66 support intact, further rally is expected in GBP/JPY. Next target is 100% projection of 139.29 to 152.82 from 146.96 at 160.49. However, break of 1.5366 will indicate short term topping and turn bias back to the downside for 150.18 support.

In the bigger picture, as long as 146.96 key support holds, medium term outlook remains bullish. Rise from 122.36 is in favor to extend to 61.8% retracement of 195.86 to 122.36 at 167.78. However, break of 146.96 support will indicate trend reversal. And there would be prospect of retesting 122.36 in that case.

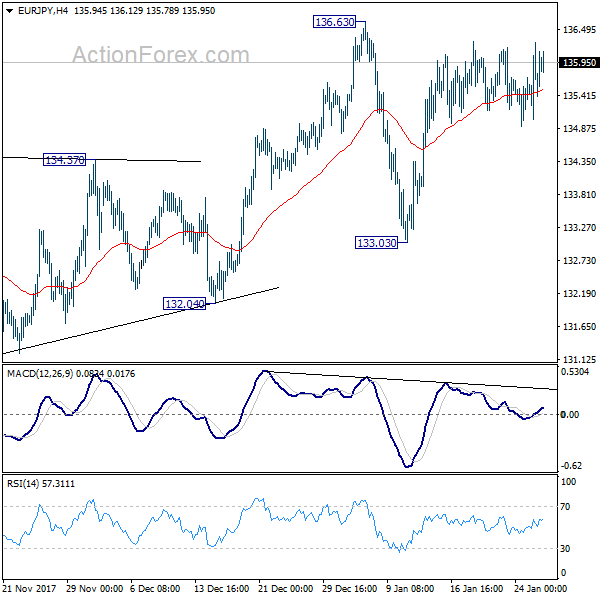

EUR/JPY Daily Outlook

Daily Pivots: (S1) 135.01; (P) 135.64; (R1) 136.26; More....

Intraday bias in EUR/JPY remains neutral and more consolidation would be seen in range of 133.03/136.63. But after all, outlook stays bullish with 133.03 support intact. Break of 136.63 will resume medium term up trend. However, on the downside, break of 133.03 will have 55 day EMA and medium term channel support firmly taken out. Also, considering bearish divergence condition in daily MACD too, that will suggest medium term reversal. Deeper fall should then be seen to 132.04 support for confirmation.

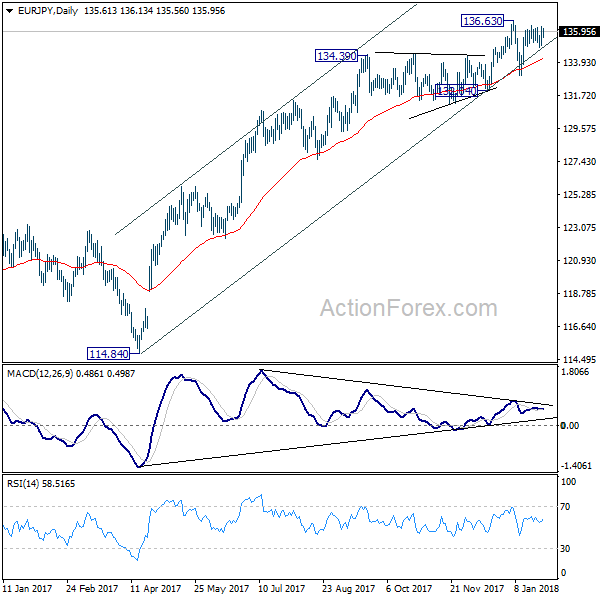

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). It should be targeting 141.04/149.76 resistance zone. On the downside, break of 132.04 support is needed to indicate medium term reversal. Otherwise, outlook will stay bullish in case of deep pull back.

4Ds: Donald Trump, Davos, Dollar Index, Economic Data | Gold Set For Weekly Gain

Equity and forex relationship matter

Dollar index facing major turbulance

Trump to speak in Davos

Today is not the 3D day but 4D. The letter 'D' matters for traders; Donald Trump, Davos, Dollar and Economic Data. The World Economic Forum in Davos comes to an end, Donald Trump will speak in Davos, Dollar index would be under the spotlight after a massive rollercoaster ride yesterday and the UK's Prelim GDP Data will be released which would impact sterling and the FTSE index.

The relationship which is prominent in the markets is that when a currency picks up some steam, the equity index of that country loses esteem among investors. The strength in the Sterling is matched by the weakness in the FTSE index which touched the lowest level YTD yesterday. The Euro erupted to the upside and this capped the gains for the European stocks.

The dollar index experienced massive turbulence yesterday. Perhaps, the US Treasury Secretary wasn't on the same page as President Donald Trump. One was saying that the lower dollar is good for the economy and other was trying to sway the markets that the dollar is going to become stronger and stronger. The dilemma created by both brought enormous volatility for the dollar index and currencies such as the Euro and Sterling experienced mammoth moves. The dollar index is on track for its worst monthly performance since March 2016.

The Euro by any measure is highly undervalued in our view and the weakness in the dollar index isn't the only reason that we have seen it surpassing the 1.25 mark yesterday. The European Central Bank policy members failed to show united front and investors saw that there aren't many reasons going to stop the ECB from increasing the interest rate next year. We think one interest rate hike is surely on the cards before mid-2019. We think that the Euro would continue to move higher and the next major resistance is sitting at 1.27 against the dollar.

Sterling is in a better position in hopes that Theresa May has survived the most difficult part and the European partners are striking a more favourable tone in relation to develop a new deal.

Mr Trump's speech in Davos is going to be the highlight of the day, he wants to talk about tax, America first and what he thinks a fair deal. However other leaders are less enthusiastic towards his speech. Investors would like to know if the Cold War has already started which triggered by Mr Trump who inflated the import duties and tariffs.There could be some significant headlines on the relationship between the two countries (UK and US) which preferred antiglobalisation. His views on Pacific trade deal could also generate some flashing newswires. Overall, we think the event would create more volatility and it would be across the equity and forex markets.

As for the precious metal, the dollar strength is fading again and the precious metal is set for another weekly gain. The dollar may remain under pressure due to the policies which Mr Trump has adopted and this plague could drag the dollar index lower. Improving fundamental over in Europe and the Chinese Lunar year should keep the gold price rising. It is more than likely that we may see a test of the $1400 mark next week. Gold having its best month since February 2017.