Sample Category Title

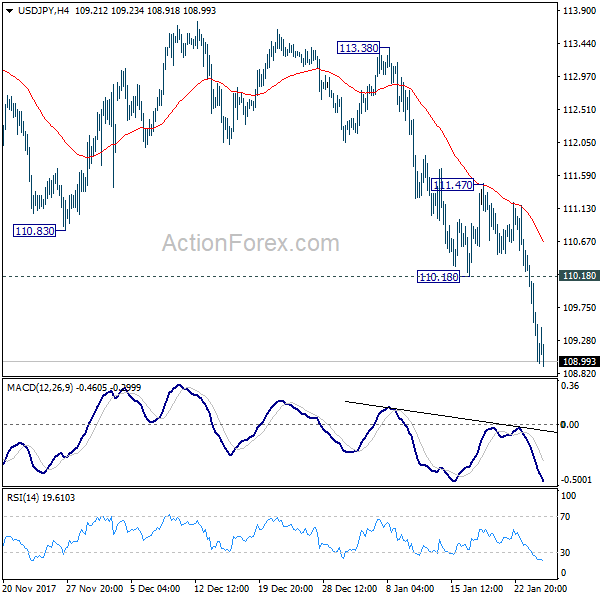

USD/JPY Daily Outlook

Daily Pivots: (S1) 108.67; (P) 109.50; (R1) 110.04; More...

USD/JPY drops to as low as 108.91 so far. Intraday bias remains on the downside for 107.31 low. Break will will target next fibonacci support at 106.48. On the upside, break of 110.18 support turned resistance will be the first sign of near term reversal and will turn bias back to the upside for 111.47 resistance.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD?JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9393; (P) 0.9486; (R1) 0.9547; More...

Intraday bias in USD/CHF remains on the downside for further fall. At this point, we're still expecting strong support around 0.9420 to bring rebound. Above 0.9535 minor résistance will turn bias back to the upside for rebound. However, sustained break of 0.9420 will carry larger bearish implication and pave the way to next key fibonacci level at 0.9115.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore,we don't expect a firm break of this level. However, firm break of 0.9420 will confirm that fall from 1.0342 is developing into a long term down trend. And in that case, next downside target will be 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115.

NZD/USD Bullish Above 0.7320, EUR/USD And GBP/USD Surges Higher

Key Highlights

- The New Zealand Dollar made good ground recently and traded above 0.7400 against the US Dollar.

- There is a crucial bullish trend line forming with support at 0.7330 on the 4-hours chart of NZD/USD.

- The current price action is positive despite the recent drop from the 0.7437 high.

- New Zealand CPI in Q4 2017 increased 1.6%, less than the forecast of 1.9%.

NZDUSD Technical Analysis

The New Zealand Dollar is enjoying a solid uptrend from the 0.6950 swing low against the US Dollar. The NZD/USD pair has moved up by more than 400 pips so far this month.

Looking at the 4-hours chart of NZD/USD, there is a strong uptrend in place above the 0.7320 pivot level. The pair recently traded above the 0.7400 level and it looks set for further gains.

The pair formed a high at 0.7437 and corrected below the 50% Fib retracement level of the last wave from the 0.7305 low to 0.7437 high. There is a major support forming near 0.7320 and a crucial bullish trend line at 0.7330 on the 4-hours chart.

An intermediate support is around the 76.4% Fib retracement level of the last wave from the 0.7305 low to 0.7437 high. The overall price action is positive as long as the pair is above 0.7320.

If the current trend remains intact, the pair could continue to move higher and it may even test the 0.7400 resistance. The 4-hours RSI retreated from the overbought levels, but it is currently above the 50 level, which is a positive sign.

The market sentiment is very bearish on the US Dollar since other pairs such as EUR/USD and GBP/USD gained a lot of strength recently. EUR/USD was able to move above 1.2350 level and GBP/USD surpassed the 1.4200 level.

Moreover, there was a lot of bearish pressure noted on USD/JPY and the pair broke a major support at 110.00, which is a key negative sign.

To sum up, the greenback is under pressure and pairs like EUR/USD, GBP/USD and NZD/USD may continue to rise.

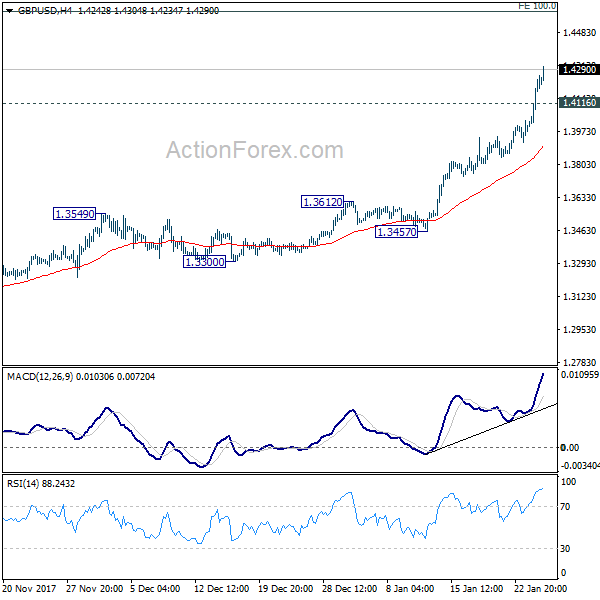

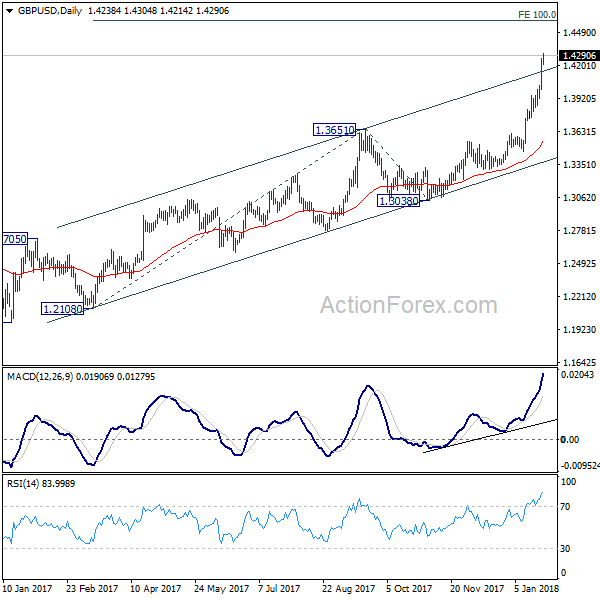

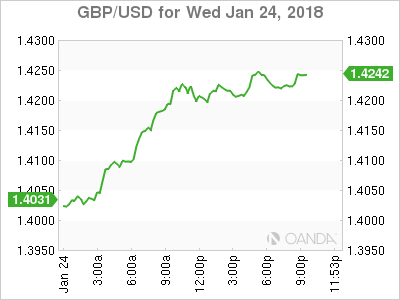

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.4067; (P) 1.4164; (R1) 1.4333; More.....

GBP/USD's rally extends to as high as 1.4304 so far today. Intraday bias remains on the upside for 100% projection of 1.2108 to 1.3651 from 1.3038 at 1.4581 next. On the downside, below 1.4116 minor support will turn intraday bias neutral first. But retreat should be contained well above 1.3612 resistance turned support to bring another rise.

In the bigger picture, sustained break of 1.3835 key resistance level indicates that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. Further rise should now be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Medium term outlook will stay bullish as long as 1.3038 support holds, in case of pull back.

Market Morning Briefing: Euro-Yen Continues Its Movement In A Very Narrow Range Of 135.3-135.7

STOCKS

Dow (26252.12, +0.16%) was stable yesterday No major movement expected just now. Trade within 26000-26500 is possible in the near term.

Dax (13414.74, -1.07%) came off from 13600 to re-test 13400 again in a single session. While above 13400, there could be chances of a rise towards 13600 or higher again in the coming sessions; else a fall back to levels near 13300 or lower would be expected.

Nikkei (23721.28, -0.92%) has come off a bit as weakness in dollar brings down USDJPY to levels below 110. A fall back towards 23600-23500 is possible in the coming sessions while the Dollar Yen trades lower.

Shanghai (3545.36, -0.40%) is slightly down today but is likely to hold below immediate resistance near 3570 as seen in the 3-day candles. 3510-3570 could be the region of trade for a few sessions. Only on a breaka above 3570, we may look at higher levels of 3600.

Nifty (11086.00, +0.02%) and Sensex (36161.64, +0.06%) were unable to sustain at intra-day highs yesterday. It would be important to see where the indices close today. Another leg of rise, if seen today could take the indices to new highs else some consolidation can be expected for a few sessions. Note that a maximum upside of 11400 on Nifty and 36750 is what we may consider on the upside. While below these levels, we still look for a sharp correction that could begin soon; else a break above 11400 and 36750 respectively will force us to review our targets.

COMMODITIES

Brent (70.90) and WTI (66.16) have both risen sharply and is currently trading above our earlier mentioned resistance levels at 70 and 65 respectively. Both are looking strongly bullish just now as the US stock inventory declined. Also supply restrictions from a group of producers of OPEC and Russia are expected to last throughout 2018 and that could be supportive of crude bullishness. Also the weakness in the US Dollar combines to aid a rise in the Crude prices.

Gold (1359.70) did not stop near 1345-1350 and has moved up beyond the interim resistance contrary to our expectations. While above 1350, a rise towards earlier high of 1374 looks possible in the next few sessions. Gold looks bullish.

Copper (3.2275) tested almost levels of 3.10 yesterday but has now recovered to levels above 3.20. While the rise continues, we may see the price heading back towards 3.25-3.30 in the near term.

FOREX

Dollar Index (89.069) has dropped even further after the US Treasury Secretary indicated from Davos that the US likes a weak dollar since it helps in trade. Although there was an attempt by the White House to undo the damage, the Dollar is now trading weaker against all major currencies. On the daily and weekly line charts, we see some support near 88.5. This should hold in the near term. The ECB meeting today would also be important in determining how the Dollar Index behaves in the near term.

Euro (1.2423) against our expectations has broken resistance near 1.2320-1.2330 on the daily candles. The crucial resistance near 1.25 on the weekly line charts might not be tested in the near term, as a dip from current levels can be expected. The ECB meeting could well be an important factor which brings about some consolidation in the Euro.

Contrary to what we expected, Dollar-Yen (109.13) is trading below support on daily candles (near 109.5). The next few sessions will give some clarity on whether it goes back above this support and respects it, or, drops further to test support near 108.75 on the weekly line charts.

Euro-Yen (135.57) continues its movement in a very narrow range of 135.3-135.7, just below 136. As mentioned yesterday, we might have to wait for a couple of sessions to get more directional clarity on whether it will first drop to test support near 134 on daily candles or, resume its rise towards resistance at 137.

Pound (1.4273) has also strengthened against the Dollar and has now broken resistance on weekly candles near 1.41-1.42.We will have to wait and watch if some near term strengthening of the Dollar can pull Pound back below this resistance level near 1.42.

Dollar Rupee (63.5025) has also dropped marginally in morning trade, reflecting Dollar weakness. It could now see a drop towards 63.40 today.

INTEREST RATES

US 10 Yr (2.6428%), 30 Yr (2.9259%), 5 Yr (2.4267%) & 2 Yr (2.0721%) are again all up as the recent volatility in US yields continues. US 10 Yr might just have found a support near 2.61%-2.62% and could now attempt to rise higher while it stays above this level. The 30 Yr might look to respect resistance near 2.92% in the near term.

Japanese 10 Yr (0.088%) has gone back up again after yesterday’s drop in response to the Bank of Japan’s apparent dovish stance. It is broadly continuing its ranging between 0.07% and 0.089%, which might continue for some more sessions. The ECB meeting today could again bring about some shift in the bond market sentiments and hence it should be watched closely.

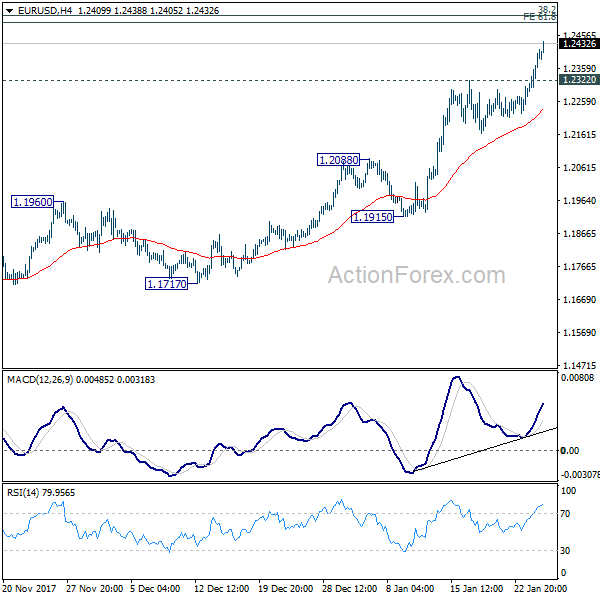

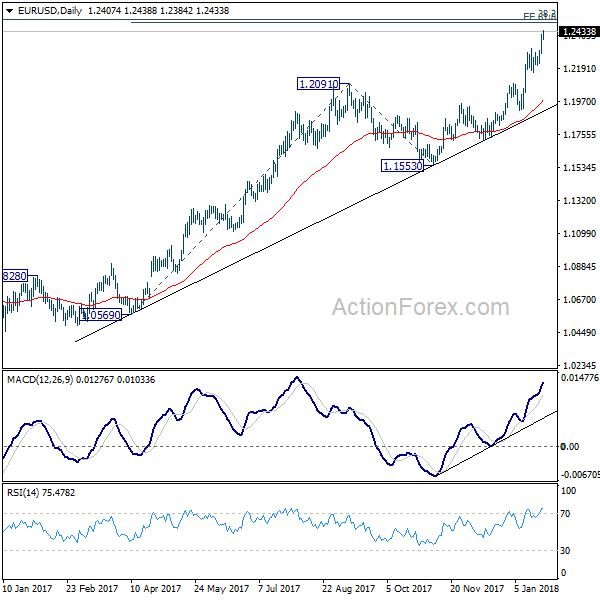

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2326; (P) 1.2370 (R1) 1.2452; More....

EUR/USD's rally is still in progress and reaches as high as 1.2438 so far today. Intraday bias remains on the upside for target next key fibonacci cluster level at 1.2494/2516. At this point, we'd still expect strong resistance from there to limit upside and bring reversal. On the downside, below 1.2322 minor support will turn intraday bias neutral first.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Therefore, in case of further rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494. Break of 1.1553 support will confirm completion of the rise. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Dollar Stays Weak after Broad Based Selloff, ECB Draghi Watched

Dollar stays weak in Asian session as the broad based selloff is extending. Dollar index broke 90 handle for the first time in more than three years after US Treasury Secretary Steven Mnuchin's comment that a weak dollar is good for trade. One explanation for recent weakness of the greenback is that global central banks would be starting to follow Fed's path of tightening. And that kept Dollar soft ahead of this week's BoJ and ECB meeting. However, the downside acceleration since Mnuchin's comments could now be taking the selloff to another level. In particular, markets would be looking forward to comments from ECB president Mario Draghi in the post meeting press conference. Any hawkish flavor in Draghi's message could prompt another round of sell-off in Dollar.

Weak Dollar might not be good

Mnuchin's, and likely President Donald Trump's too, preference for a weak dollar is relatively rare. Traditionally, the White House usually prefer a strong currency. While Mnuchin believe it's good for trade, there are counter arguments that a weak Dollar is bad for the economy as a whole. In particular, Dollar's status as the world's reserve currency could be threatened. It's already reported that China is considering to diversify away from Dollar assets and dollar's depreciation could accelerate the process. Also, further downside acceleration in dollar could prompt capital outflows that could push up interest rates and drag down stocks.

Dollar index on track to 87.23

Technically, we're maintaining the view that Dollar's down trend from 103.82 is a corrective move. After taking out 91 key level, it's now heading to 61.8% projection of 103.82 to 91.01 from 95.15 at 87.23. At this point, we're expecting strong support from 84.58/85 cluster support to complete the correction. This cluster zone represents 84.75 (2013 high) and 61.8% retracement of 72.69 to 103.82 at 84.58.

Focus on ECB forward guidance

ECB is widely expected to keep monetary policies unchanged today. The main refinancing rate will be held at 0.00%. Also, the EUR 30b asset purchase program will be kept unchanged and will run through September. However, since the release of the December meeting accounts, there are speculations that ECB could start to tweak its forward guidance. And, it might drop the pledge to extend the asset purchase program if necessary. Indeed, some ECB officials have openly given the nod to putting and end date to the program. It would be a dilemma for President Mario Draghi today considering the surge in EUR/USD this week. Any hawkish change in the forward guidance will definitely shoot of EUR/USD, which ECB would not like to see.

On the data front

New Zealand CPI rose 0.1% qoq, 1.6% yoy in Q4, much weaker than expectation of 0.4% qoq, 1.9% yoy. Germany will release Gfk consumer sentiment and Ifo Business climate. UK will release BBA mortgage approvals and CBI reported sales. Canada retails sales will be feature later in the day. US will release trade balance, jobless claims, wholesale inventories, new home sales and leading index.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2326; (P) 1.2370 (R1) 1.2452; More....

EUR/USD's rally is still in progress and reaches as high as 1.2438 so far today. Intraday bias remains on the upside for target next key fibonacci cluster level at 1.2494/2516. At this point, we'd still expect strong resistance from there to limit upside and bring reversal. On the downside, below 1.2322 minor support will turn intraday bias neutral first.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Therefore, in case of further rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494. Break of 1.1553 support will confirm completion of the rise. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | CPI Q/Q Q4 | 0.10% | 0.40% | 0.50% | |

| 21:45 | NZD | CPI Y/Y Q4 | 1.60% | 1.90% | 1.90% | |

| 07:00 | EUR | German GfK Consumer Confidence Feb | 10.8 | 10.8 | ||

| 09:00 | EUR | German IFO Business Climate Jan | 117 | 117.2 | ||

| 09:00 | EUR | German IFO Expectations Jan | 109.2 | 109.5 | ||

| 09:00 | EUR | German IFO Current Assessment Jan | 125.3 | 125.4 | ||

| 09:30 | GBP | BBA Loans for House Purchase Dec | 39.7K | 39.5K | ||

| 11:00 | GBP | CBI Reported Sales Jan | 13 | 20 | ||

| 12:45 | EUR | ECB Rate Decision | 0.00% | 0.00% | ||

| 13:30 | EUR | ECB Press Conference | ||||

| 13:30 | USD | Advance Goods Trade Balance Dec | -68.6B | -70.0B | ||

| 13:30 | USD | Wholesale Inventories M/M Dec P | 0.30% | 0.80% | ||

| 13:30 | USD | Initial Jobless Claims (JAN 20) | 236K | 220K | ||

| 13:30 | CAD | Retail Sales M/M Nov | 0.80% | 1.50% | ||

| 13:30 | CAD | Retail Sales Ex Auto M/M Nov | 0.90% | 0.80% | ||

| 15:00 | USD | New Home Sales Dec | 676K | 733K | ||

| 15:00 | USD | Leading Index Dec | 0.50% | 0.40% | ||

| 15:30 | USD | Natural Gas Storage | -183B |

When It Rains It Pours , Mnuchin Mania

When it rains it pours, Mnuchin Mania

The US dollar bids were far and few between thanks to Treasury Secretary Mnuchin's outward endorsement for weak USD policy.While we already knew the administration previously favoured a weaker dollar. His comments caught the dollar prone and defenceless opening floodgates to a massive wave of dollar selling

His comments have turned into a bit of fiasco and will end up going down in market folklore for marking the first time since the early 90's a US Treasury Secretary endorsed a weaker US dollar. Bond market took an immediate and predictable defensive posture as US 10y yields soared topping at 2.66 % as memories of savage bear market resonated after then-Treasury Secretary James A. Baker III threw down the gauntlet and endorsed a weaker dollar in the early 90's. But we are far from the fractures and turbulent world economy of the late 80's or early 90′, so the Munchin fallout is unlikely to trigger the tsunami of global risk aversion that occurred in yesteryear. But none the less the aftershocks are still reverberating in the early APAC session.

Oil Markets

Oil markets too were at the epicentre of volatility with WTI breaking the $ 65.00 per barrel market and marking the highest close since Dec 2014. Oil prices pivoted higher after the U.S. Energy Information Administration ( EIA) reported a 10th straight drop in US crude inventories. The report solidifies the view that OPEC production caps are working.

But let's not lose sight of the US dollar follies, which are underpropping oil markets and providing the bounce to all commodity markets. Since we may only be in the early stages of the US dollars demise, and when aggregated with the oil markets OPEC induced positive developments, the market could press significantly higher from increasing sensitivity and stronger correlations to the US dollar alone.

Structurally, the dollar can push much lower as sings are developing that we may be in the early stages of a multi-year secular bear market.

Gold Markets

Gold hit an 18 month high as investors were more than willing to pay hefty insurance premia as a hedge against the inflationary impacts from a hapless dollar. US Treasury Secretary Steven Mnuchin opened the floodgates to dollar sales, but with traders base case scenario to sell the dollar at all costs, gold prices should remain well supported on dips and could be poised to move even higher on the next US dollar wobble.

G-10

The EUR

Decision day for the ECB and the traders are jointly overseeing price action which usually sends a convincing signal to reduce risk as its typical to reduce longs ahead of the ordinarily dovish Draghi

Given the extended EUR position; we should expect the EUR to give way some points on dovish Draghi. But with the primary macro theme in FX markets being USD weakness, it's unlikely those EURO offers will hang around too long, especially after dollar red flags raised when BoJ Kuroda erred as dovish as could be and the market still bought JPY

The Japanese Yen

They Yen has been tracking the general dollar weakness overnight, but traders are waiting for the BoJ next move. USDJPY is too high to sound the intervention alarm bells, leading me to believe a swift shift in policy may be in the offing,

The Australian Dollar

AUD has recovered all of Iron Ore inspired losses, as the freefalling greenback has supported the commodity block of currencies en masse.

But the next catalyst may come from a build-up of RBA ” rate hike fever' that seems to be making the rounds these days. While the market base case ifs for the RBA to remain neutral, any bullish shift higher in a measly priced in May hike probability could push the Aussie to 82 level.

Traders are starting to take notice of the recent string of economic data which has been particularly boisterous led by strong employment print supported by an uptick in consumer sentiment.

However, with the Aussie dollar soaring these days there a higher likelihood, the RBA will remain faithful to current expectations as opposed to moving in front of them.

The Chinese Yuan

The market has come a long way in a few days primarily driven on the heels of the broader USD malaise as fast money speculators have pilled into both sides of the ledger. However, there is chatter circulating of some sizable stops are cluttering the landsca[e near the 6.34 level that could prove an attractive target and test the Pboc resolve.But either way, recent price discovery is telling us heaps about the Pboc's current currency policy which appears much more investor-friendly than ever before.

The Malaysian Ringgit

Overnight price action was more a reflection of a struggling US dollar rather than pre MPC market positioning

But none the less the Ringgit was supported by surging crude prices and the sagging dollar. But today is the day of reckoning for Riggit Bulls, and .the BNM could make or break many of our top line views.

Pre BNM banter

Straw polls suggest that 65 % of the market has long Malaysian exposure in either short USDMYR or long short dated Malays Bonds.

But the massive lifting will be left to Bank Negara to express a strong currency bias by raisings interest rates at today's meeting

Our base case scenario is for slightly more aggressive action from Bank Negara Malaysia ( BNM) than the market's consensus of one hike and done. So if the BNM signal one additional rate hike in for 2018 this would trigger an immediate downside test of 3.70whereas if the BNM signals only one single rate hike for 2018, the market will test 3.80

And for the most unlikely scenario, if the BNM take a dovish tack, suggesting no imminent rate hike the USDMYR could gap above 4.00 USDMYR in a heartbeat.

As far as yesterday CPI data. While coming in at 3.5 % for Dec 3.7 % for the full year 2017 and within the central banks 3-4 % inflation target. The BNM is still expected to hike interest rates later today since firmer oil prices will translate into high headline inflation in 2018.

Dollar Collapses After Mnuchin Weak Currency Comments

USD Softer Ahead of ECB Monetary Policy Meeting

Trump Administration Endorses Dollar Weakness and gets tough on trade

The USD tumbled against all majors on Wednesday. The US Secretary of the Treasury issued comments in support of a weaker dollar. The combination of a lower currency and a tough stance on trade has sparked concerns that a global trade war could ignite. The US dollar has lacked traction in 2018 as domestic political uncertainty and economic recovery abroad continue to put downward pressure on the greenback. The highlight for the market on Thursday will be the press conference from European Central Bank (ECB) President Mario Draghi.

- The ECB minutes from December diverged form what Draghi said.

- The World Economic Forum in Davos continues in Switzerland

- US Commerce Secretary talked up hardline approach to trade

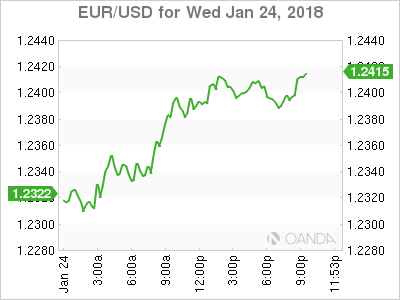

The EUR/USD gained 0.82 percent on Wednesday. The single currency is trading at 1.24 after some comments from US officials showed the current administration has diverged from the past in seeking a strong dollar policy and in fact could be ramping up for a trade war. US Secretary of the Treasury Steven Mnuchin said he welcomed the weakness in the US given the positive impact on trade. The words from the Secretary were shocking given his predecessors comments on a strong currency. Trade has been at the forefront after the US has imposed tariffs on certain products with President Donald Trump scheduled to talk at Davos on Friday. The US leader is anticipated to continue to paradox of highlighting stronger growth, which should value the currency higher, while at the same time seeking trade advantages in his America first strategy.

The European Central Bank (ECB) will publish its minimum bid rate on Thursday, January 25 at 7:45 am EST. There is no change expected with the attention of the market focused on the words of ECB President Mario Draghi who will host a press conference at 8:30 am EST.

The EUR touched a three year high versus the USD and given the minutes showed a more hawkish ECB, Draghi could go even deeper into neutral territory and talk down both the currency by highlighting the still low European inflation. Given that most of this EUR move was sparked by US dollar weakness Mr Draghi is facing an uphill battle.

The GBP/USD gained 1.53 percent in the last 24 hours. The currency pair is trading at 1.4210 and reached levels not seen since the aftermath of the Brexit referendum. The higher chances of a softer exit and the weakness of the US dollar left the pound in current levels with the assumption that the ECB is close to announcing an end of QE this year with a small possibility of higher rates before the end of 2018. Mario Draghi has tried to shied away from saying that in so many words, with his actual statements remaining neutral despite evidence that there is a strong economic recovery underway, particularly by looking at Germany. That the engine of the European recovery is Germany will not be a surprise but this time it seems the there are multiple signs of optimism in the EU.

The GBP was the strongest performer on Thursday against the dollar, but similar to the EUR move it was based more on USD weakness than any particular British indicator. The political uncertainty which ended in a 1 day shutdown of the Federal Government was not the perfect start for for Washington taking into consideration the primaries in the fall.

Market events to watch this week:

Thursday, January 25

7:45am EUR Minimum Bid Rate

8:30 am CAD Core Retail Sales m/m

8:30 am EUR ECB Press Conference

Friday, January 26

4:30 am GBP Prelim GDP q/q

8:30 am CAD CPI m/m

8:30 am USD Advance GDP q/q

8:30 am USD Core Durable Goods Orders m/m

Gold Climbs Against Battered US Dollar, Hits 16-Week High

Gold has posted strong gains in the Wednesday session. In North American trade, the spot price for an ounce of gold is $13523.90, up 0.94% on the day. On the release front, Existing Home Sales disappointed, slowing to 5.57 million. This missed the forecast of 5.72 million. On Thursday, the US releases unemployment claims and New Home Sales.

The broad selloff of the US dollar continues, as major rivals such as the euro, pound and yen have posted strong gains on Wednesday. Gold has also jumped on the bandwagon, and has climbed 3.7% in the month of January. Gold has benefited from weaker appetite for risk, as global equity markets are lower. We could see more movement from gold later during the week, with the release on Friday of Advance GDP for the fourth quarter of 2016, as well as durable goods reports.

The US government shutdown lasted just three days, and only affected one working day. Still, the positive news didn’t boost the struggling US dollar. The funding agreement that Congress approved is little more than a band-aid solution, as it extends funding only until February 8. The Democrats held up a funding bill last week, in order to force the Republicans to the table over illegal immigration. The Republicans have promised to hold a vote on this issue, but many Democratic lawmakers remain skeptical that President Trump and the Republicans will deal in good faith over immigration. If the bipartisan efforts to reform immigration implodes, the government will again find itself without funds come next month. With many members of Congress up for re-election in November, lawmakers will be trying to avoid angering voters with a second shutdown next month.