Sample Category Title

Canadian Dollar Slightly Higher in Light Holiday Trade

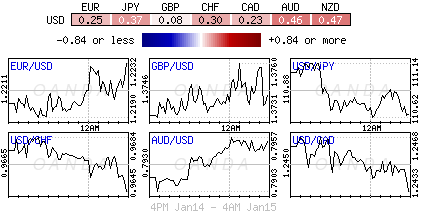

USD/CAD is subdued in the Friday session. Currently, the pair is trading at 1.2433, down 0.22% on the day. On the release front, there are no Canadian or US events on the schedule. US markets are closed in observance of Martin Luther King Day. On Tuesday, the sole indicator is the US Empire State Manufacturing Index.

The Canadian dollar improved on Friday, as investors were not impressed with lukewarm numbers in the US. CPI slowed to 0.1%, down from 0.4% a month earlier. Core CPI was stronger, improving to 0.3%. Both indicators were within expectations, but pointed to weak inflation levels. On the bright side, consumer spending remained strong. December retail sales, boosted by Christmas shopping, were up 5.4% compared to a year ago. Although investors were not impressed with the December data, as the euro rally continued, the spending numbers point to a strong finish for the economy in 2017.

After strong gains in December, the Canadian dollar has held its own against the greenback in January. There are two important factors for this positive trend. First, Canada has recorded outstanding employment numbers in the past two months. In December, the economy added 78.6 thousand jobs, defying experts who predicted a minuscule gain of 1.8 thousand. This release comes on the heels of a superb November release, when the economy added 79.5 thousand news jobs. The unemployment rate dropped to 5.7% in December, down from 5.9% a month earlier. Second, the recent rise in oil prices, which are up 6.8% since mid-December, has boosted the commodity-based Canadian currency. The Bank of Canada is expected to raise rates later this week, which could boost the Canadian dollar. One dark cloud on the horizon, however, is NAFTA. The free-trade agreement, crucial to the Canadian economy, is in trouble, as US President Trump has threatened to cancel the pact, which could have serious ramifications and send the Canadian dollar sharply lower.

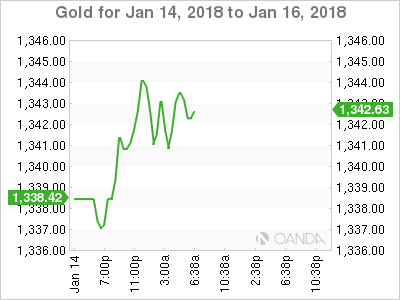

Spot Gold at New Highs; Focuses Target at $1357

Spot Gold started week in firm bullish tone and extended strong rally of past three days to new four-month high at $1344. The metal benefited from fresh weakness of the dollar and extended the second leg of steep rally from $1236 (12 Dec low). Bulls took out the last obstacle at $1340, on the way towards key med-term barrier at $1357 (08 Se high). Gold price maintains firm bullish sentiment as the greenback continues to fall, with bullish studies ignoring so far strongly overbought conditions on daily chart. However, corrective action should be anticipated in the coming session, with shallow pullback (ideally to be contained by rising 10SMA at $1322), before final push towards $1357 target.

Res: 1344; 1350; 1352; 1357;

Sup: 1340; 1335; 1327; 1322

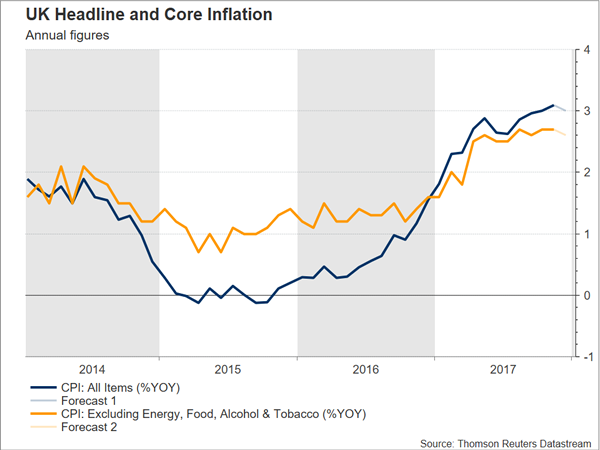

UK Inflation Forecast To Ease A Bit Though Remain Comfortably Above BoE Target

UK inflation figures for the month of December will be made public on Tuesday at 0930 GMT. Annual inflation is expected to grow by 3.0%, easing a bit from the near six-year high of 3.1% recorded in November, which given that it was by more than 1% above the Bank of England’s target for inflation of 2% meant that Governor Carney had to write a letter to the Chancellor of the Exchequer Philip Hammond to explain the overshoot.

Month-on-month, December CPI is forecast to expand by 0.4%, above November’s respective figure of 0.3%. Core inflation, which excludes energy, food, alcohol and tobacco items, is anticipated to grow by 2.6% y/y in December, this being a slightly softer pace relative to the 2.7% in the preceding two months which constituted the highest rate of growth for the measure since late 2011.

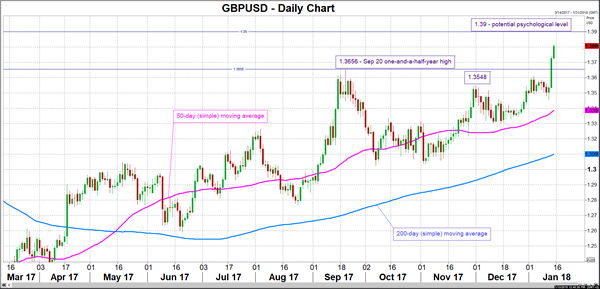

Should inflation figures come in excess of analysts’ projections, then forex market participants could propel pound/dollar higher in expectation for another interest rate increase by the BoE – after the one in early November – to be delivered sooner rather than later. In this case, the area around the 1.39 handle could act as a psychological barrier to the upside. The pair is currently trading at its highest since June 2016’s Brexit referendum and could be meeting some resistance around 1.38 – 1.38 itself being broken – which is roughly where the 61.8% Fibonacci retracement of the decline that followed the referendum is situated. For the record, markets currently expect another quarter percentage point interest rate increase by the BoE – for the bank’s target rate to reach 0.75% – by year-end.

If, on the other hand, inflation numbers come in below expectations, then sterling might weaken, as it could be perceived by market participants that the UK’s central bank would face less pressure to soon deliver additional rate hikes. A falling sterling versus the dollar could meet support around 1.3656, a top recorded in late September.

How fierce the market reaction would be, will also depend on the extent of the deviation from analysts’ forecasts. But another caveat should be mentioned: in the case of the UK, the analysis is not as “binary” as it might be in the US, the eurozone and Japan for example, where inflation is running short of the respective central banks targets and where a higher reading would definitely be welcome. In the UK, higher-than-anticipated inflation might raise hopes for interest rate hikes to be delivered earlier in time, but is also weakening the outlook for growth as inflation outpaces wage increases, setting a negative backdrop for consumer spending as UK households are seeing their purchasing power getting shrunk. In fact, last month’s inflation overshoot beyond market expectations led to gains in sterling that were short-lived.

BoE policymakers would likely be reluctant to deliver additional rate hikes when faced with a possibly grimmer economic environment. Add into the equation Brexit and other political uncertainty – with PM Theresa May seen as gradually getting weaker – and the attempt to predict the monetary policy outlook becomes an even more complicated endeavor.

Data on producer prices and retail price inflation – a measure used to calculate payments on instruments such as index-linked government bonds and other contracts such as indexed-pensions – for December will also be released alongside CPI figures, while numbers on UK retail sales for the month of December will be made public on Friday at 0930 GMT.

Technical Outlook: COPPER – Strong Rally Signals An End Of Correction

Copper rallied strongly on Monday and broke above four-day congestion, signaling that corrective phase from new high at $3.3200 may be over.

The metal received fresh support from weakening dollar which came under increased pressure on Monday and spiked to $3.2900 so far, near Fibo 76.4% of $3.3200/$3.2065 pullback. Today's close above cracked $3.2766 barrier (Fibo 61.8%) is needed to confirm reversal.

Bullish daily techs returned to full bullish setup and started gaining fresh bullish momentum, signaling further recovery for full retracement of corrective leg from $3.3200 peak. Broken thick 4-hr cloud ($3.2695/$3.2481) marks strong support zone, reinforced by 10SMA at $3.2425, which is expected to contain dips.

Res: 3.2900, 3.2932, 3.2970, 3.3085

Sup: 3.2695, 3.2525, 3.2481, 3.2425

Dollar Deflates On Federal Holiday

Monday January 15: Five things the markets are talking about

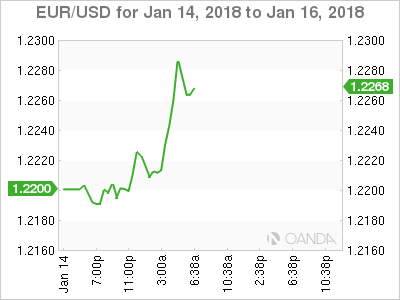

The U.S dollar is in trouble and is heading for a fourth day of losses against G10 currency pairs on rate differentials, while Euro equities are under pressure as the region's ‘single' currency (€1.2260) rallies to its strongest position in more than three-years outright.

Last Friday's December U.S CPI report should go some ways to provide some reassurance to the Fed that domestic inflation is likely to rise towards their target over time, however, both U.S policy makers and the market will most likely require more convincing that firmer inflation can be sustained and reason why the U.S currency starts this week on the back foot.

On the agenda for this week, the Bank of Canada's (BoC) interest-rate decision comes Wednesday (10 am EDT), while monetary policy announcements are also due in South Korea, South Africa and Turkey.

Stateside, industrial production (IP) probably increased last month, a report may show Wednesday, completing a solid year for manufacturing, while U.S housing starts Thursday is expected to have slipped in December for the first time in three-months as cold weather impeded work.

Elsewhere, China releases Q4 GDP, December industrial production and retail sales on Thursday.

Note: U.S. markets are closed Monday for the Martin Luther King Jr. holiday.

1. Stocks mixed results

In Japan, the Nikkei share average tracked a rise in global equities and advanced overnight, although the dollar's (¥110.62) weakening against the yen capped gains. The Nikkei ended +0.26% higher, while the broader Topix added +0.4%.

Down-under, the ‘big' miners helped keep Australia's equity market in the green overnight. By day's end, the S&P/ASX 200 inched up +0.1% for a second consecutive session, as energy, tech and telecom shares weighed.

In Hong Kong, stocks snapped a 14-day winning streak, dragged down by a retreat in property shares and index heavyweight Tencent Holdings. At the close, the Hang Seng index was down -0.23%, while the Hang Seng China Enterprises index rose +0.01%.

In China, equities snapped an 11-session winning streak, with gains in banking and real estate firms offset by resources and industrial shares. The Shanghai Composite index was down -0.55%, while the blue-chip CSI300 index was flat.

In Europe, regional indices trade mostly lower in quieter trade, as U.S cash markets remain closed in observance of Martin Luther King. News flows have been relatively quiet ahead of a busier corporate schedule for the week ahead.

Indices: Stoxx600 -0.2% at 397.80, FTSE flat at 7776, DAX -0.3% at 13208, CAC-40 -0.2% at 5504, IBEX-35 flat at 10466, FTSE MIB -0.2% at 23397, SMI -0.1 at 9542, S&P 500 Futures +0.2%

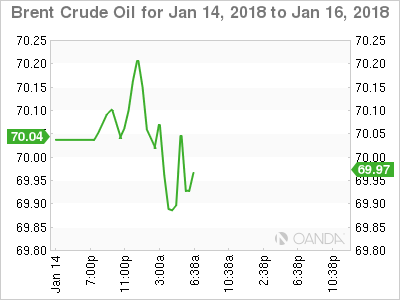

2. Oil hovers near highs, clouded by rise in U.S. output, gold rallies

Oil hovered below a three-year high near $70 a barrel on Monday on signs that production cuts by OPEC and Russia are tightening supplies, but analysts warned of 'red flags' due to surging U.S. production.

Brent crude futures are trading -18c lower at +$69.69, after having risen above +$70 earlier in the session. U.S West Texas Intermediate (WTI) crude futures are at +$64.22, down -8 cents from Friday's close.

A production-cutting pact between the OPEC, Russia and other producers has given a strong tailwind to oil prices, with both benchmarks last week hitting levels not seen in three-years.

Growing signs of a tightening market has boosted confidence among traders and analysts that prices can be sustained near current levels. Other factors, including political risk, have also supported crude.

Gold prices hit a four-month high as the dollar index slumped to a three-year low. Spot gold is up +0.1% at +$1,339.46 an ounce, after earlier touching its strongest since September at +$1,339.97.

Note: Spot gold rose for a fifth consecutive straight week last week, gaining +1.4%.

3. Sovereign yields try to back up

Friday's U.S inflation data showing that the underlying pace of U.S. inflation accelerated last month finally drove the U.S two-year benchmark yield above +2%, as traders priced in a growing likelihood that the Fed would follow through on its projection of three-rate increases this year.

Note: Along the U.S curve, Treasuries fell broadly, led by shorter maturities, with the difference between yields on five- and 30-year maturities approaching the tightest spread in 10-years.

Elsewhere, the rise in bond yields over the past fortnight has pushed the yield of Germany's 30-year benchmark bund to around +1.30%, which should help demand at Wednesday's German long Bund auction.

Note: On the negative side, the volume of Germany's 30-year debt issuance will be higher this year than in 2017, with planned volume at +€16B vs. +€11B last year.

Elsewhere, in the U.K, the 10-year yield declined -1 bps to +1.339%, the first retreat in a week and the largest decrease in more than a week.

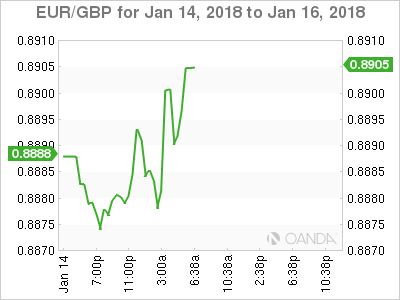

4. Sterling highest vs. dollar since Brexit

Even though Carillion PLC (U.K's second biggest construction company) goes into liquidation this morning, currently there is no other bad news capable of pushing the pound down and with the USD falling across the board, GBP/USD has reached its highest since the Brexit vote, rising +0.5% to £1.3809.

Note: Tomorrow's U.K inflation data could see the market firm up expectations for a May hike (CPI and PPI at 04:30 am EDT).

The EUR (€1.2286) continues to shine as the dollar loses more ground, lifting the ‘single' currency to another three-year high. Despite the dollar's weakness, there are a number of reasons supporting the ‘single' currency – positive political developments in Germany, a 'more-hawkish-than-expected' ECB, an exceptionally strong eurozone economic data and ongoing ‘undervaluation' have led investors to favor the EUR outright.

5. Euro area international trade

Data this morning showed that the first estimate for Euro region (EA19) exports of goods to the rest of the world in November 2017 was +€197.5B, an increase of +7.7% compared with November 2016 (+€183.5B).

Imports from the rest of the world stood at +€171.2B a rise of +7.3% compared with November 2016 (+€159.6B).

As a result, the Euro area recorded a +€26.3B 'surplus' in trade in goods with the rest of the world in November 2017, compared with +€23.8B in November 2016.

Intra-euro area trade rose to +€165.5B in November 2017, up by +6.9% compared with November 2016.

Euro Rally Continues, US Markets Closed For MLK Day

The euro has started off the trading week with considerable gains. Currently, EUR/USD is trading at 1.2280, up 0.66% on the day. In economic news, it’s a quiet start to the week. In the eurozone, the trade surplus climbed to EUR 22.5 billion, edging above the estimate of EUR 22.4 billion. In the US, banks and stock markets are closed for Martin Luther King Day, and there are no economic indicators on the schedule.

The euro continues to rally, as EUR/USD has climbed to its highest level since December 2014. On Friday, pair gained 1.4%, following reports from Germany that Angela Merkel’s conservative bloc and the Social Democrats have agreed on a coalition blueprint. This ends months of political uncertainty,which has eroded Merkel’s standing and also sidelined Germany on issues such as Brexit and political reform in the eurozone. Still, the talks are only in the preliminary stage, and further negotiations will be continuing in the coming weeks. Any coalition deal must be approved by all members of the Social Democrats camp, and this could present a challenge for party head Martin Shulz. The draft which Shulz and Merkel hammered out calls for an annual limit of 220,000 immigrants, and many Social Democrats oppose any cap on immigration.

The dollar lost ground on Friday, as US consumer data for December was lukewarm. CPI slowed to 0.1%, down from 0.4% a month earlier. Core CPI was stronger, improving to 0.3%. Both indicators were within expectations, but pointed to weak inflation levels. On the bright side, consumer spending remained strong. December retail sales buoyed by Christmas shopping, were up 5.4% compared to a year ago. Although investors were not impressed with the December data, as the euro rally continued, the spending numbers point to a strong finish for the economy in 2017.

CRUDE OIL Bullish Breakout

Crude oil is has broken resistance given at 62.21 (04/01/2018 high). Strong support is given at 55.82 (07/12/2017 low). Expected to keep increasing as demand seems very strong.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. For the time being the pair lies in an upside momentum. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

SILVER Renewed Bullish Pressures

Silver has been bouncing on hourly support at 16.99 (04/01/2018 low). Hourly resistance is given at 17.46 (16/10/2017 high). Expected to show continued bullish pressures.

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

GOLD Heading Higher

Gold is pushing higher after the strong collapse even though traders are taking some profit. Hourly support is given at 1306 (04/01/2018 low). Resistance located at 1326 (04/01/2018 has been broken and the commodity is now targeting strong resistance at 1357 (08/09/2017 high).

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

BITCOIN Holding Below 14k

Bitcoin is suffering these past few days. The technical structure has shown a tremendous positive short-term momentum so far. Hourly support area located around 10775 (22/12/2017 low). In the short-term, the technical structure suggests a continued bearish momentum. Expected to show further decline.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will reach $40'000 in 2018.