Sample Category Title

GBP/USD In Crucial Uptrend, UK CPI Release Next

Key Highlights

- The British Pound made a solid upside move recently and traded above 1.3750 against the US Dollar.

- A break above a major bearish trend line with resistance at 1.3550 on the 4-hours chart of GBP/USD initiated a crucial uptrend.

- The pair may correct a few pips during the coming sessions, but it remains supported above 1.3600.

- Today's UK Consumer Price Index for Dec 2017 could trigger swing moves in the short term (forecast 3.2% versus previous 3.1%, YoY).

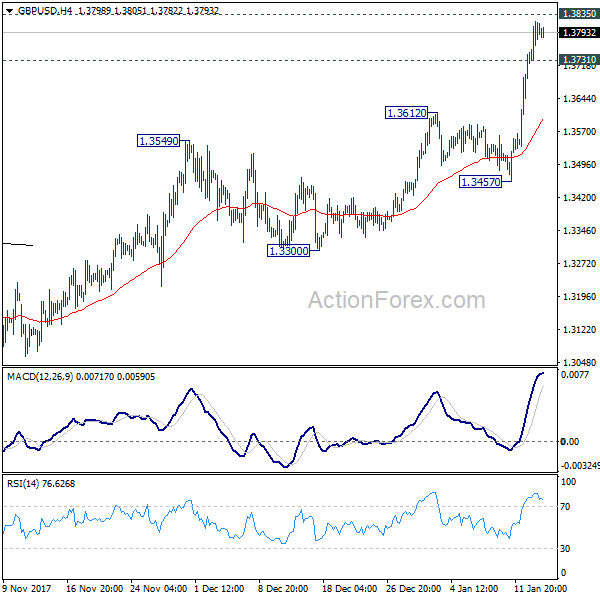

GBPUSD Technical Analysis

The British Pound rose sharply this week above 1.3600 against the US Dollar. The GBP/USD pair even broke the 1.3700 resistance to place itself in a major uptrend.

Looking at the 4-hours chart of GBP/USD, there was a break above a major bearish trend line with resistance at 1.3550. It opened the doors for more upsides and the pair broke the 1.3700 and 1.3750 resistance levels.

The upside move was strong and buyers were able to push the price above 1.3800. The recent high was 1.3819 from where a downside correction was initiated. An initial support on the downside is around the 23.6% Fib retracement level of the last wave from the 1.3457 low to 1.3819 high.

There are many supports on the downside such as 1.3680 and 1.3650. However, the most important is at 1.3600-1.3610. The stated 1.3600-1.3610 area is a significant pivot and it will most likely act as a strong buy zone if the pair corrects lower from the current levels.

On the upside, a daily close above 1.3800 could trigger a major upside reaction towards the next major barrier at 1.4000. The next move in GBP/USD may depend on today's Consumer Price Index results in the UK.

The market is looking for an increase of 3.2% in Dec 2017 (YoY). If the actual is 3.2% or above 3.2%, GBP/USD could accelerate its gains. On the other hand, any disappointing reading would ignite a short-term correction towards 1.3680 or 1.3610.

Looking at the other major pairs – EUR/USD settled above the 1.2200 level and it recently traded as high as 1.2296. USD/JPY extended declines and it seems like it is heading towards the 110.00 level.

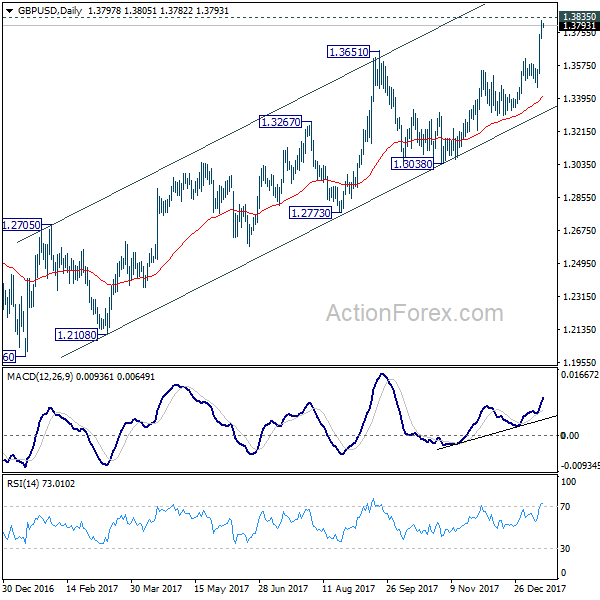

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3737; (P) 1.3777; (R1) 1.3833; More.....

Intraday bias in GBP/USD remains on the upside with focus on 1.3835 key resistance. At this point, we'd still expect strong resistance from 1.3835 to limit upside to complete the medium term rally from 1.1946. However, sustained break there will carry larger bullish implication and target long term fibonacci level at 1.5466. On the downside, below 1.3731 minor support will turn intraday bias neutral first. Further break of 1.3457 support should confirm reversal.

In the bigger picture, the break of long term trend line resistance from 1.7190 (2014 high) is seen as a sign of long term reversal. However, rise from 1.1946 (2016 low) is not impulsive looking. And the pair is limited below 1.3835 key resistance. Hence, we won't turn bullish yet and would continue to monitor the development. On the downside, break of 1.3038 support will now indicate that rebound from 1.1946 has completed and turn outlook bearish. Meanwhile, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

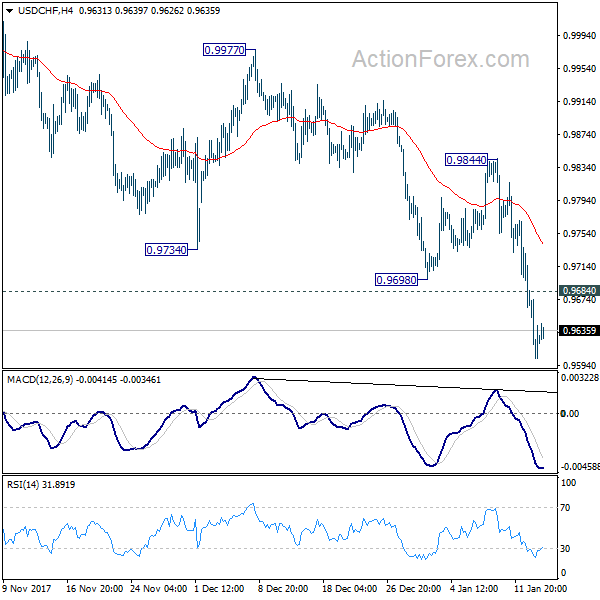

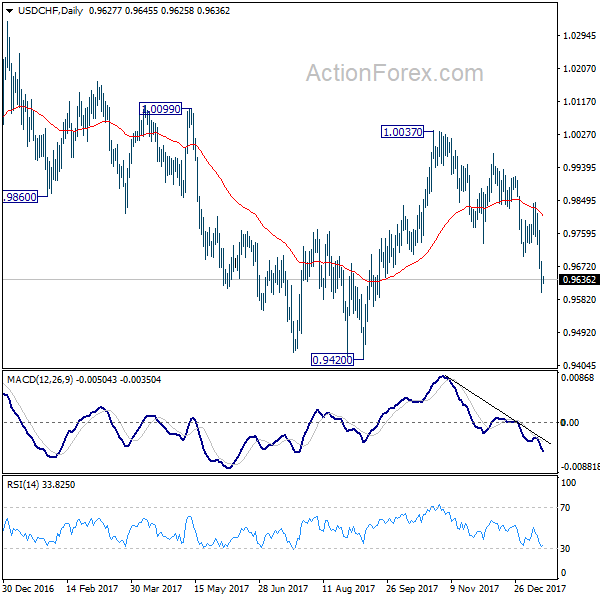

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9592; (P) 0.9638; (R1) 0.9674; More....

Intraday bias in USD/CHF remains on the downside as fall from 1.0037 is in progress for retesting 0.9420 low. On the upside, above 0.9684 minor resistance will turn intraday bias neutral first. But outlook will stay bearish as long as 0.9844 resistance holds.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

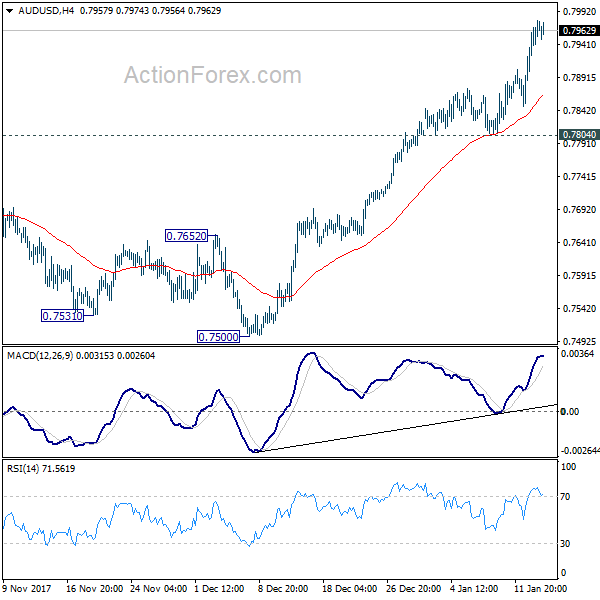

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7915; (P) 0.7947; (R1) 0.7994; More...

Intraday bias in AUD/USD remains on the upside as rise from 0.7500 is in progress for 0.8124 high. Break there will resume whole medium term rebound from 0.6826 and target key fibonacci level at 0.8451. On the downside, break of 0.7804 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, current development suggests that medium term rebound from 0.6826 is still in progress and could be resuming. Such rise could target 38.2% retracement of 1.1079 (2011 high) to 0.6826 (2016 low) at 0.8451. As such rise is seen as a corrective move, we'd expect strong resistance from 0.8451 to limit upside.

USD/JPY Daily Outlook

Daily Pivots: (S1) 110.17; (P) 110.68; (R1) 111.03; More...

A temporary low is in place at 110.32 in USD/JPY. Intraday bias is turned neutral for consolidations. But outlook will stays bearish as long as 113.38 resistance holds and deeper fall is expected. Break of 110.32 will extend the whole decline from 114.73 to 61.8% retracement of 107.31 to 114.73 at 110.14. We'd look for bottoming signal again below 110.14.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

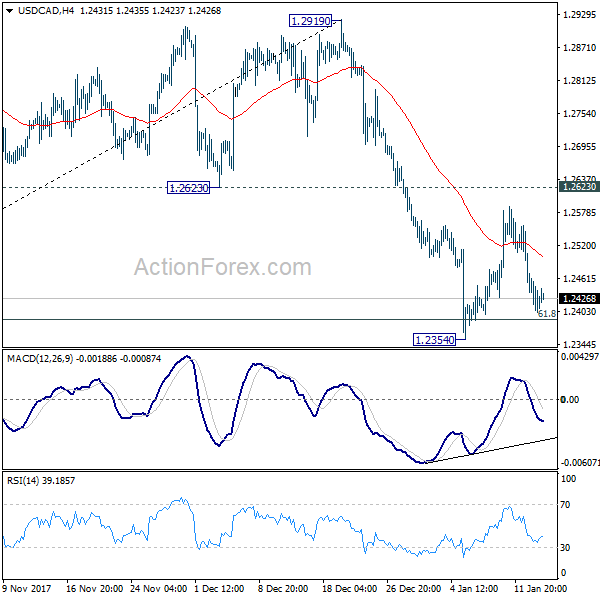

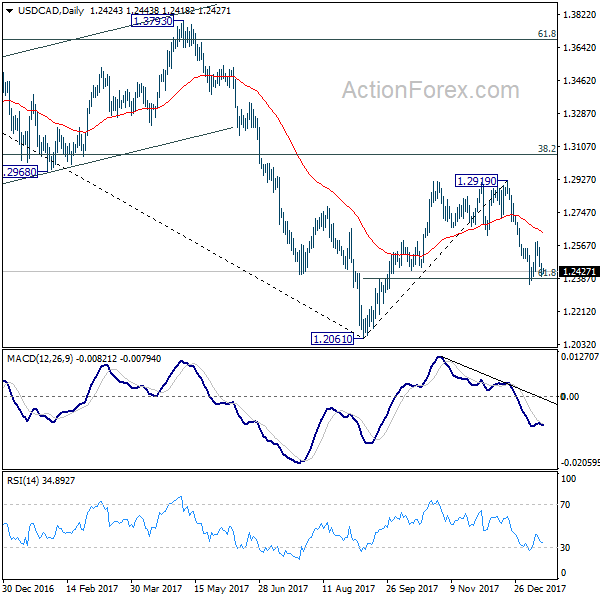

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2396; (P) 1.2434; (R1) 1.2465; More....

Intraday bias in USD/CAD remains neutral as consolidation from 1.2354 continues. As long as 1.2623 support turned resistance holds, deeper decline is expected. Break of 1.2354 will extend the fall from 1.2910 to retest 1.2061 low. However, sustained break of 1.2623 will argue that the fall has completed and turn bias back to the upside for 1.2919 resistance.

In the bigger picture, current development argues that rebound from 1.2061 has completed at 1.2919, rejected by 55 week EMA (now at 1.2850) and kept below 38.2% retracement of 1.4689 to 1.2061 at 1.3065. The development also suggests that long term fall from 1.4689 is not completed yet. Decisive break of 1.2061 low will target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. This will now be the favored case as long as 1.2919 resistance holds.

Euro Rally Continues With Hawkish ECB Comments, Aussie Strong on China

Dollar is mildly higher in Asian session, as it turns into consolidation after recent steep selloff. Among the mostly traded currencies, Australian Dollar is trading as the strongest one. That's partly supported by strength in China as the Shanghai SSE composite index, trading at 3420, is close to 2017 high at 3450. And break there will push the index into highest level since 2015. Meanwhile, Hong Kong HSI, as a proxy to China, is also close to the record high at 31958 made 10 years ago. Euro is trading as the second strongest as supported by hawkish comments from ECB officials. It seems now, after last week's December meeting minutes, ECB policymakers are starting to sing a chorus of ending asset purchases after September. As for today, UK inflation data will be a key event to watch.

ECB Hansson: Appropriate to end the purchases after September

ECB Governing Council Member Ardo Hansson said in an interview that there was "need for action in our communication." This echoed the views noted in December ECB minutes released last week. Hansson said that "there are certainly good reasons to reduce the importance of the net purchases in our communication soon -- also with a view to a potential end to these purchases." And should incoming data show that the economy evolve in line with ECB's own projections, it would "certainly be conceivable and also appropriate to end the purchases after September." Also, he said that the "last step to zero" asset purchase is "not a big deal anymore". And "we can go to zero in one step without any problems". He also talked down Euro's rising exchange rate and said it's "not a threat to the inflation outlook" and one "shouldn't overdramatize" it.

BoE Tenreyro: Productivity growth could beat forecasts

BoE MPC member Silvana Tenreyro said in speech yesterday that she "concurred" with the central bank's projections in the November inflation report. However, "in the medium-term, the risks to productivity may be skewed to the upside." She pointed to the drags on productivity from deleveraging in the financial sector and slowdown in manufacturing. However, the former is a process that would soon end. Meanwhile, global growth would help boost demand and manufactured goods from the UK. And productivity growth could beat BoE's forecasts once these two drags fade. She also noted that based on the November forecasts, BoE would need two more rate hikes over the next three years. But a better development in the economy could also change the rate outlook.

On the data front

Japan domestic CGPI rose 3.1% yoy in December versus expectation of 3.2% yoy. German CPI final will be released in European session. But main focus will be UK inflation data, including CPI, RPI and PPI. US will release Empire State manufacturing index later in the day.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7915; (P) 0.7947; (R1) 0.7994; More...

Intraday bias in AUD/USD remains on the upside as rise from 0.7500 is in progress for 0.8124 high. Break there will resume whole medium term rebound from 0.6826 and target key fibonacci level at 0.8451. On the downside, break of 0.7804 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, current development suggests that medium term rebound from 0.6826 is still in progress and could be resuming. Such rise could target 38.2% retracement of 1.1079 (2011 high) to 0.6826 (2016 low) at 0.8451. As such rise is seen as a corrective move, we'd expect strong resistance from 0.8451 to limit upside.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Domestic CGPI Y/Y Dec | 3.10% | 3.20% | 3.50% | 3.60% |

| 4:30 | JPY | Tertiary Industry Index M/M Nov | 0.30% | 0.30% | ||

| 7:00 | EUR | German WPI M/M Dec | 0.50% | |||

| 7:00 | EUR | German CPI M/M Dec F | 0.60% | 0.60% | ||

| 7:00 | EUR | German CPI Y/Y Dec F | 1.70% | 1.70% | ||

| 9:30 | GBP | CPI M/M Dec | 0.40% | 0.30% | ||

| 9:30 | GBP | CPI Y/Y Dec | 3.00% | 3.10% | ||

| 9:30 | GBP | Core CPI Y/Y Dec | 2.60% | 2.70% | ||

| 9:30 | GBP | RPI M/M Dec | 0.60% | 0.20% | ||

| 9:30 | GBP | RPI Y/Y Dec | 3.90% | 3.90% | ||

| 9:30 | GBP | PPI Input M/M Dec | 0.40% | 1.80% | ||

| 9:30 | GBP | PPI Input Y/Y Dec | 5.30% | 7.30% | ||

| 9:30 | GBP | PPI Output M/M Dec | 0.20% | 0.30% | ||

| 9:30 | GBP | PPI Output Y/Y Dec | 2.90% | 3.00% | ||

| 9:30 | GBP | PPI Output Core M/M Dec | 0.20% | 0.20% | ||

| 9:30 | GBP | PPI Output Core Y/Y Dec | 2.30% | 2.20% | ||

| 9:30 | GBP | House Price Index Y/Y Nov | 4.20% | 4.50% | ||

| 13:30 | USD | Empire State Manufacturing Index Jan | 19 | 18 |

USD/JPY Break Adds To USD Woes

A miserable 2017 has turned into a dismal 2018 for the US dollar and Monday's breakdown in USD/JPY is a fresh reason for worry. The New Zealand dollar was the top performer while USD lagged. Japanese PPI is due up next. The Premium long GBPUSD hit its final target of 1.3820 for 330 pip gain, closing automatically ahead of Tuesday's relase of UK CPI. The week's video for subscribers is posted below.

The US was on holiday Monday but that was no respite for the dollar as it crumbled for the second day. On Friday, the euro and pound broke out while Monday it was USD/JPY as the November low of 110.84 gave way.

Comments from Estonian ECB member Hansson accelerated EUR gains and underscored the dollar's challenges. He spoke about shifting to more-hawkish ECB language and ending bond purchases cold turkey in September. It's part of the increasingly aggressive rhetoric form global central bankers.

Contrast that with the US, where the Fed is basically paralyzed until Powell takes over at the end of this month.

Looking ahead, Japan is the focus of a light Asia-Pacific calendar with PPI due at 2350 GMT. The consensus is for a healthy 3.2% rise. Later, the November tertiary industry index is due at 0430 GMT but the real focus of the day comes later with German and UK CPI numbers due out. Both are risks to the high-flying EUR and GBP.

Market Morning Briefing: The Aussie Trades Higher

STOCKS

Stocks are overall mixed. Almost all indices have rallied enough in the past few months and is likely to come off, they lack bearish momentum and are unable to see follow through selling. A further rally from current levels in the coming weeks would be surprising.

Dow (25803.19, +0.89%) was closed today and with resumption of trade today, a test of 26000 or higher is possible in the coming sessions. Overall the index looks bullish.

Dax (13200.51, -0.34%) is falling eventually. A break below 13200 would take it further down towards 13000, else a bounce back to 13400 is possible.

Nikkei (23845.50, +0.55%) has moved up instead of coming down from levels near 23800. This raises doubts of whether the index would be bearish in the coming sessions. The bull strength doesn’t seem to have exhausted yet and a fight for another upmove looks eminent while the index stays above 23500. A sharp break below 23500 is needed to turn bearish over the medium term.

Shanghai (3425.34, +0.44%) also surprised a bit by bouncing from levels near 3400 instead of coming down further. While resistance near 3440-3450 levels hold, we may expect a fall towards 3380 or lower in the coming sessions.

Nifty (10741.55, +0.56%) and Sensex (34843.51, +0.73%) both moved up sharply breaking our immediate targets of 10750 and 34750 respectively. A break above 10800 on Nifty could take it higher towards 11000 in the medium term while Sensex may head towards 35250.

COMMODITIES

Brent (70.03) is trading at crucial resistance at 70 from where we expect a corrective fall towards 69-68 levels in the near term. Price action near current levels would be important to keep an eye on.

WTI (64.53) has moved up and is likely to come off a bit from 65 before again resuming its rise in the longer term.

Gold (1341.16) is almost stable near previous levels and could be soon headed to test previous high of 1357 seen in Sep’17 before again seeing a short corrective dip. Near term looks bullish.

Copper (3.2665) rose sharply from 3.20 and may move higher to re-test resistance near 3.35 in the coming sessions.

FOREX

Stronger than expected rise in the Euro (1.2266), past 1.2220 to a high of 1.2297. From these levels, it ought to see come correction/ consolidation down towards 1.2220 at least. However, IN CASE of a break above 1.2300, we have to look for 1.24-25 on the upside before exhaustion. The market will, most likely, go Long into the ECB meeting on 25th Jan (next Thursday). Plenty of time for it to move up to 1.24-25, if it wants to. But, the ECB is not going to like the Euro strength. Be careful there.

As expected, the Euro-Yen (135.83) is closing in on 136 and might try to rise further to 138, either in a straight line, or after a couple of days of consolidation.

Dollar-Yen (110.71) saw a low near 110.32. We take this as kind of meeting our target of 110, because there is Support near 110.30-20 on the 3-day and Weekly candles. Look for a bounce back towards 112 while this Support holds.

On the Pound (1.3797), we had pointed out a Resistance near 1.3820-50 on the Daily candles. It has seen a high near 1.3819 yesterday and there's a decent chance that the Resistance will hold on first testing, producing a small dip towards 1.3700. In case of a break above 1.38, we have to be ready for much higher levels, near 1.40.

The Aussie (0.7963) trades higher, as expected, but is yet to test its horizontal Resistance at 0.80 on the Weekly Line chart. Expect some profit-taking there.

Although Dollar-Rupee (63.49) dipped below target to a low near 63.33, it bounced back into Close. Now we need to see if it comes down from here because of Resistance at current levels on the Euro-Rupee (77.95) and Yen-Rupee (0.5735) or whether it rises past 63.55-60. We prefer a rise, given the near-term Oversold condition in Dollar-Rupee.

INTEREST RATES

The US 10Yr (2.5462%), 30 Yr (2.8443%) & 5 Yr (2.3499%) yields continue to maintain their levels seen in the last couple of days. If there is no significant upmove seen in bond yields for few more sessions, it would reflect further build up of confidence in the bond markets, which could lead to some correction in yields towards 2.5%, 2.8% and 2.3% respectively. However medium / long term outlook on bonds continues to be bearish with upside targets for the 10 Yr and 30 Yr at 2.62% and 2.9-3% respectively.

We remain bullish on the US 10 Yr- 5 Yr spread (0.1963%) & 30-10 Yr Spread (0.2981%), which could see a bounce soon from respective supports.

Japanese 10 Yr Yield (0.078%) could remain ranged between 0.07% and 0.088% in the next few days before any significant upmove is seen beyond resistance near 0.088%.

When It Rains, It Pours.

Currency Overview

The USD dollar rout took a bit of a breather in New York but has shown few signs of reversing. The lack of USD buying appetite after the stronger CPI reading Friday generated an all clear to sell the Greenback which quickly morphed into a full out retreat yesterday lead by both JPY and CNH in Asia. And then London extended the current EUR and GBP rally before virtually every currency jumped on the bandwagon.

Oil Markets

Oil prices are moving up again after Brent convincingly broke through the critical $70 level overnight, and WTI was zeroing in on the $65.00. With few meaning full headlines to digest overnight, the ongoing bullish sentiments, and recognition of geopolitical risks are supporting the commodity

But is to true that labour shortages are holding back Shale Oil producers from going full bore ” drill baby drill.”? Well, this discussion is hitting the rumour mill this morning and perhaps something to monitor.

Gold Markets

Overnight Gold prices touched the highest level since early September during the European trading session on Monda and primarily supported by the falling USD in the absence of any fundamental headline drivers. However, I suspect speculators are adding to bullish bets ahead of the potential adverse fallout from the possible U.S. government shutdown if the budget deal is not ratified. Also, seasonality factors remain in play, but so far physical demand has been light this week but could still pick up significantly ahead of the Chinese Lunar New Year.

The US Equity markets

Stronger economic signals from the US and Europe is giving investors the confidence to continue deploying capital into equities markets.

G-10

The Euro

Despite the thinner liquidity conditions in NY and few if any obstacles to prevent the dollar from wandering lower, Traders respected current lofty levels as the EURUSD, which has been leading the dollar selling charge, has now climbed to its highest level since December 2014. But tonights NY session will be interesting after traders return from the long weekend. With short-term traders, inter-day positioning a bit stretched there is some capacity for the USD to reverse.But with the dollar trading “three sheets to the wind” and “wobbling like a drunken sailor”, there is a stronger chance that panic dollar selling will ensue and hammer the dollar lower.

Hawkish ECB minutes and diminishing political risk should continue to drive sentiment.The Euro continues to be the highest conviction trade and will remain well supported on dips. Certainly, ECB’s Hansson hawkish comments overnight would help the view as indeed it doesn’t appear the ECB is pushing back against the rising Euro, well at least some elements aren’t

Notwithstanding, the general theme is developing for G-10 traders, especially for those that missed the bus, as they will be more inclined to fade USD strength vs a basket of currencies including AUD, CNH and EUR.

Japanese Yen

After breaking through the 111 level, USDJPY now looks poised to test 110 level. No, if and or buts, 110 USDJPY is historically significant pivot point sentiment, so things could get ugly quickly if this level gives way.

Cross asset market are all surging higher on the back of the accelerating global growth theme which is contributing to frothy equity markets and higher US yields. What is unusual is JPY was still rising higher suggesting traders are still concerned about a faster pace of BoJ taper after last weeks QE reduction despite BoJ Governor Kuroda once again indicating the bank, has no intention to adjust policy just yet.

This morning Japan PPI (CGPI) M/M: 0.2% V 0.4%E; Y/Y: 3.1% V 3.2%E came in on the weaker side, and at least for now USDJPY has shown some respect for fundamentals so far by jumping to 110.75 on short covering which could trigger a short-term squeeze above 111.

Chinese Yuan

The market reached new 2-year lows for USD/CNH and given that traders are embracing CNH as a broader proxy for dollar strength the move is quite significant. Not to mention and of equal importance, “the German central bank has decided to include CNY in its currency reserves” This is all part of Chinas grand scheme toward internationalising the Yuan. And while the purchase will comprise a tiny portion of the Bundesbank’s reserves, it’s symbolically meaningful making it highly unlikely mainland regulators are going to stand in front of the RMB party bus over the near term. Indeed the Yuan Bulls are running wild in the China shop this week and from a technical perspective, the close below last year’s low would suggest a move down to the 6.30 level.

Australian Dollar

The AUD Remains the catch-up mode, but with the convergence of the global growth narrative, the AUD looks to be the perfect place to park risk and enjoy the bubbly risk-on environment. The market, however, is not expecting too much play ahead of Thursday Jobs report an China data dump

Asia FX

Regional bourses continue their ascent and In Asia FX the continuation of the USD weakness theme, with DXY meandering southbound. Most EM Asian currencies have marked gains vs the greenback though we could see some moves paired back ahead of China’s data dump on Thursday.

The Malaysian Ringgit

Monitoring the 6.95 area closely as the market is treading a touch cautiously, but this has more to do with the pause in the overall USD selling momentum in a holiday-thinned NY session. The market could pair risk and book some profits ahead of 6.95 but will look to re-engage the strong Bullish momentum signal on a break of 6.95.

Given that the bullish fundamentals are fairly well entrenched, I suspect moves will be driven more by technical signals as we approach the crucial BNM rate decision later this month.