Sample Category Title

Market Update – Asian Session: Bitcoin Weaker On Crackdowns In South Korea And China

Headlines/Economic Data

General Trend:

Japanese officials comment after recent gains in the Yen

PBoC raises rate on 63-day open market operation (OMO) by 5bps to 2.95% (in line with prior 5bps increases on 7, 14 and 28-day reverse repos)

Japan

Nikkei 225 opened flat; closed +1%

TOPIX Iron & Steel Index -1.5%

Softbank +1.9% (gained 3.2% prior session on speculation related to listing of mobile phone unit)

Fast Retailing +2.5% (reported better than expected Q1 results on Jan 11th)

(JP) JAPAN DEC PPI (CGPI) M/M: 0.2% V 0.4%E; Y/Y: 3.1% V 3.2%E

(JP) Japan Fin Min Aso: No comment on FX levels, do not see a big deal with dollar at ~¥110.80

(JP) Japan Econ Min Motegi: Want to closely monitor impact that FX, financial market moves have on economy

(JP) Japan Nov Tertiary Industry Index m/m: 1.1% v 0.3%e

Japan MoF sells ¥1.79T v ¥2.2T indicated in 0.10% (prior 0.1%) 5-yr bonds; avg yield -0.084% v -0.107% prior; bid to cover 5.24x v 4.19x prior

Korea

Kospi opened flat

Chipmakers gain: Samsung Electronics +1%, Hynix +1%

General weakness in financial sector: Industrial Bank of Korea -2.4%, Hana Financial -1.7%, Woori Bank -2.2%, KB Financial -1.2%

(KR) South Korea Fin Min Kim: Irrational speculation in cryptocurrency; tax and regulation needed on crypto - Korean press

(KR) South Korea has 147K people that have been jobless for six months or longer last year, the highest since record keeping began in 2000 - Korean press

China/Hong Kong

Hang Seng opened +0.3%, Shanghai Composite -0.2%

Info Technology +2%, Services +1.1% (supported by strength in gaming sector), Energy +1.4%, Materials +1.5%, Financials +1.3%, Property/Construction +1%

(CN) China is unlikely to loosen property controls – CSJ

(CN) Ratio of treasuries in China FX reserves is not likely to fall - Chinese press

(CN) China debt yield may stay high and continue to rise – CSJ

(CN) China PBOC Official Ruan Jianhong: To keep prudent and neutral monetary policy; Low M2 growth may become new normal - China Daily

(CN) China President Xi: China and US should properly settle trade issue - Xinhua

(CN) China PBoC OMO: Injects CNY320B in 7, 14 and 63-day reverse repos v CNY150B injected in 7 and 14-day prior: Net injects CNY270B v CNY50B drained prior; Raises 63-day reverse repo rate to 2.95% from 2.90% prior

USD/CNY (CN) PBoC sets yuan reference rate at 6.4372 v 6.4574 prior (Strongest setting since Dec 11th 2015)

Australia/New Zealand

ASX 200 opened +0.1%; closed -0.5%

Rio Tinto: Opened higher but has since pared gains after Q4 production update and guidance

Energy -1%, Telecom -1%, Utilities -1%, Resources -0.5%, Financials -0.3%

(AU) Australia ANZ Roy Morgan Weekly Consumer Confidence Index: 123.5 v 122.0 prior

(AU) Australia AOFM announces new benchmark 2.75% 2029 bond

(AU) Australia Dec Motor Vehicle Sales m/m: 4.5% v 0.1% prior; y/y: 6.7% v 2.1% prior

(NZ) New Zealand Dec Non-Resident Bond Holdings: 61.1% v 60.4% prior

(NZ) ANZ’s NZ Market Focus report: productivity will need to rise if recent GDP growth is to be maintained

Baby formula firm Bellamy's (BAL.AU) Announces Conditional Acquisition of Camperdown; Raises FY18 Rev +30-35% y/y (prior 15-20% y/y); EBITDA Margin 20-23% (prior 17-20%); +22%

Fonterra (FCG.NZ) Reports Dec collections Total New Zealand 176.1M v 186.3M y/y; Fonterra Australia 16.1M v 12.6M y/y

Rio Tinto (RIO.AU) Reports Q4 Pilbara iron ore shipments 90.0Mt v 89.7Mte v 87.7Mt y/y; Pilbara iron ore production 87.9Mt, +3% y/y

Other Asia

(IN) India 10-year bond yield has risen by over 9bps on session: Reserve Bank of India (RBI) Acharya said banks shouldn't be repeatedly surprised with higher yields, Interest rate risks of banks can't be managed by regulator.

(PH) Philippines Central Bank (BSP) Chief Espenilla: CPI could trend higher than anticipated; faces primary challenges managing risks to CPI view

(TW) Taiwan said to consider allowing foreign banks to issue Taiwan Dollar (TWD) denominated bonds – local media

North America

(US) GOP leaders said to be weighing spending deal to Feb 16th

Looking Ahead: Corporate earnings are expected from companies including Citi, CSX and UnitedHealth

Europe

(UK) EU draft documents shows revised directives for EU chief negotiator Michel Barnier with more stringent conditions for a post-Brexit transition deal – FT

(UK) Chancellor of Exchequer Hammond (Fin Min): Britons want to keep European economic model - UK press

(UK) PM May planning speech to outline Brexit policy in February - UK press

(UK) PM May's EU Withdrawal Bill expected to move to the House of Lords this week and pass - financial press

(UK) BOE’s Tenreyro: UK productivity growth could beat expectations; faster UK wage growth alone would not necessarily point to rate hike, productivity is important too; Expected to vote for "a couple more" quarter-point rises in the next three years if the economy performs in line with the BOE's expectations. - speaking at Queen Mary University of London

(DE) Germany SPD Schulz: SPD leadership is united behind exploratory result; optimistic majority will vote for talks with Merkel; Notes ‘successful’ exploratory talks with Germany Chancellor Merkel.

(FR) Bank of France said it already held some of currency reserves in yuan (CNY); vast majority of reserves remain invested in US dollar denominated assets

(GR) Greece parliament approves austerity measures

(EE) ECB’s Hansson (Estonia): Appropriate to end asset purchases after September if growth and inflation continue to evolve in-line with the central bank’s expectations - German press

(EU) Moody's: Forecast policy rates to approach 1% for the ECB and 2% for the BoE and 3% for the US Fed by 2021.

Fiat: CEO Marchionne: Have no intention of breaking up the company or selling individual brands to China or other parties

BMW: Expects slight global sales growth in 2018 on new models - US financial press; Cites CFO at Detroit Auto Show.

Continental: Said to hire JPMorgan as adviser regarding possible break-up - financial press

Schaeffer: CEO: Guided Q4 Rev ~€3.5B, +8.5% y/y; 2017 Rev €14.0B, +5.9% y/y

Looking Ahead: UK Dec CPI due for release

Levels as of 01:00ET

Nikkei225 +1%, Hang Seng +1.0%; Shanghai Composite +0.2%; ASX200 -0.5%, Kospi +0.8%

Equity Futures: S&P500 +0.3%; Nasdaq100 +0.2%, Dax +0.2%; FTSE100 +0.1%

EUR 1.2279-1.2248; JPY 110.98-110.48; AUD 0.7975-0.7949;NZD 0.7307-0.7281

Feb Gold +0.4% at $1,340/oz; Feb Crude Oil +0.4% at $64.53/brl; Mar Copper -0.4% at $3.25/lb

Yen Appreciation Abated Somewhat With USD/JPY Rising Close To 111

Market movers today

In the UK, CPI inflation for December is released, which we estimate fell back to 2.9%, from 3.1% in November, due mainly to a lower contribution from food prices. We estimate core inflation fell from 2.7% to 2.6% due to a decrease in service price inflation. Despite the higher oil prices, we expect overall inflation pressure in the UK to fade t his year, as food prices seem to have peaked and GBP has stabilised in recent months. Underlying inflation pressure is still muted, as wage growth remains subdued.

Later in the day we also get the US Empire Manufacturing PMI for January. Consensus is for a small increase, although severe winter weather in the region might have impaired economic activity to some degree at the start of 2018.

No scheduled Scandi events for today.

Selected market news

Despite (more) hawkish ECB comments Monday afternoon, it has been a relatively quiet session overnight with focus across markets remaining on the continued dollar rout/euro rebound. In equities, it has been an overall positive session in Asia with most indices seeing small gains and notably the Hang Seng hitting new record highs (US was out yesterday for Martin Luther King Day). Yen appreciation abated somewhat with USD/JPY rising close to 111 again this morning as focus on the risk of Bank of Japan policy possibly becoming less accommodative faded somewhat . Also, oil prices edged higher yet again with Brent crude hovering around the USD70/bbl mark after Iraq called for continued OPEC production curbs over the weekend.

Hawkish comments from the ECB's Hansson yesterday in a German newspaper interview added fuel to the fire under already-aggressive ECB pricing (a first hike priced in for early 2019) and sent EUR/USD close to 1.23. While a perceived hawk, Hansson notably said that QE purchases could be taken to zero in one go, suggesting new purchases could end as early as Q4 this year, provided the economy is on t rack. He added that policy guidance should be adjusted ahead of the summer and, further, that recent euro appreciation provides little threat to the eurozone inflation out look. This line of reasoning adds to the tone of December ECB minutes and paints the picture of a central bank, where – at least some – members look increasingly keen t o get going on policy ‘normalisat ion'. A few ECB speakers coming up later this week but otherwise market focus will turn to Mario Draghi's stance at next week's ECB meeting. While we look for a softening tone at the January meeting, it is noteworthy that only hawks have been speaking publicly since the aggressive market reaction fol lowing the minutes last week.

Dollar Woes Continue

DOLLAR STRUGGLES

And despite uncertainty over Brexit, the pound is also sitting around levels against the dollar last touched in June 2016, when Britain voted to leave the European Union.

Stephen Innes, head of Asia-Pacific trading at Oanda, warned the greenback could face further selling.

“With the dollar trading ‘three sheets to the wind’ and ‘wobbling like a drunken sailor’, there is a stronger chance that panic dollar selling will ensue and hammer the dollar lower,” he said.

The yuan extended Monday’s advance that followed news Germany’s central bank would include the Chinese currency in its own reserves, the latest step towards its internationalisation.

The currency is at a two-year high after Bundesbank board member Andreas Dombret’s comments. The announcement follows the International Monetary Fund’s decision in 2016 to include the yuan in its elite basket of currencies.

Aussie Trading Slightly Lower This Morning

For the 24 hours to 23:00 GMT, the AUD rose 0.47% against the USD and closed at 0.7966.

LME Copper prices rose 1.6% or $109.5/MT to $7180.0/MT. Aluminium prices rose 0.6% or $12.5/MT to $2227.5/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7963, with the AUD trading a tad lower against the USD from yesterday’s close.

The pair is expected to find support at 0.7934, and a fall through could take it to the next support level of 0.7904. The pair is expected to find its first resistance at 0.7986, and a rise through could take it to the next resistance level of 0.8008.

Looking ahead, traders would await Australia’s Westpac consumer confidence index for January, slated to release overnight.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Euro-Zone’s Trade Surplus Widened In November

For the 24 hours to 23:00 GMT, the EUR rose 0.57% against the USD and closed at 1.2264, after the Euro-zone's seasonally adjusted trade surplus widened more-than-expected to €22.5 billion in November, amid an increase in exports, thus countering concerns about the impact of a stronger Euro on exporters. The region had recorded a surplus of €19.0 billion in the previous month, while markets were anticipating for a surplus of €22.3 billion.

In the Asian session, at GMT0400, the pair is trading at 1.2258, with the EUR trading marginally lower against the USD from yesterday's close.

The pair is expected to find support at 1.2202, and a fall through could take it to the next support level of 1.2145. The pair is expected to find its first resistance at 1.2306, and a rise through could take it to the next resistance level of 1.2353.

Going ahead, traders would look forward to Germany's final inflation numbers for December, scheduled to release in a few hours. Moreover, the New York Empire State manufacturing index for January, scheduled to release later in the day, would be on investors' radar.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Pound Trading On A Weaker Footing, Ahead Of UK’s Inflation Data

For the 24 hours to 23:00 GMT, the GBP rose 0.44% against the USD and closed at 1.3796.

In the Asian session, at GMT0400, the pair is trading at 1.3786, with the GBP trading 0.07% lower against the USD from yesterday's close.

The pair is expected to find support at 1.3739, and a fall through could take it to the next support level of 1.3691. The pair is expected to find its first resistance at 1.3827, and a rise through could take it to the next resistance level of 1.3867.

Moving ahead, UK's crucial consumer price inflation for December, slated to release in a few hours, would pique significant amount of investor attention.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Japanese Yen Reverses Its Gains In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.16% against the JPY and closed at 110.58.

In the Asian session, at GMT0400, the pair is trading at 110.94, with the USD trading 0.33% higher against the JPY from yesterday's close.

Early morning data indicated that Japan's tertiary industry index registered a rise of 1.1% on a monthly basis in November, higher than market expectations for an advance of 0.3%. The index had registered a revised rise of 0.2% in the prior month.

The pair is expected to find support at 110.52, and a fall through could take it to the next support level of 110.10. The pair is expected to find its first resistance at 111.17, and a rise through could take it to the next resistance level of 111.40.

Going ahead, market participants would eye the release of Japan's machine orders for November, due to release overnight.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.

Swiss Franc Trading On A Weaker Footing In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.41% against the CHF and closed at 0.9632.

On the data front, Switzerland’s total sight deposits increased to CHF573.8 billion in the week ended 12 January, after recording a level of CHF572.8 billion in the preceding month.

In the Asian session, at GMT0400, the pair is trading at 0.9638, with the USD trading 0.06% higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9602, and a fall through could take it to the next support level of 0.9567. The pair is expected to find its first resistance at 0.9674, and a rise through could take it to the next resistance level of 0.9711.

Later in the day, all eyes would be on a speech by the Swiss National Bank (SNB) President, Thomas Jordan.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Canada’s Existing Home Sales Grew For Fifth Consecutive Month In December

For the 24 hours to 23:00 GMT, the USD declined 0.26% against the CAD and closed at 1.2426.

Macroeconomic data revealed that Canada's existing home sales climbed 4.5% MoM in December, rising for the fifth straight month. In the previous month, existing home sales had advanced 3.9%.

In the Asian session, at GMT0400, the pair is trading at 1.2433, with the USD trading 0.06% higher against the CAD from yesterday's close.

The pair is expected to find support at 1.2404, and a fall through could take it to the next support level of 1.2374. The pair is expected to find its first resistance at 1.2462, and a rise through could take it to the next resistance level of 1.2490.

With no macroeconomic releases in Canada today, investors would focus on global macroeconomic news for further direction.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

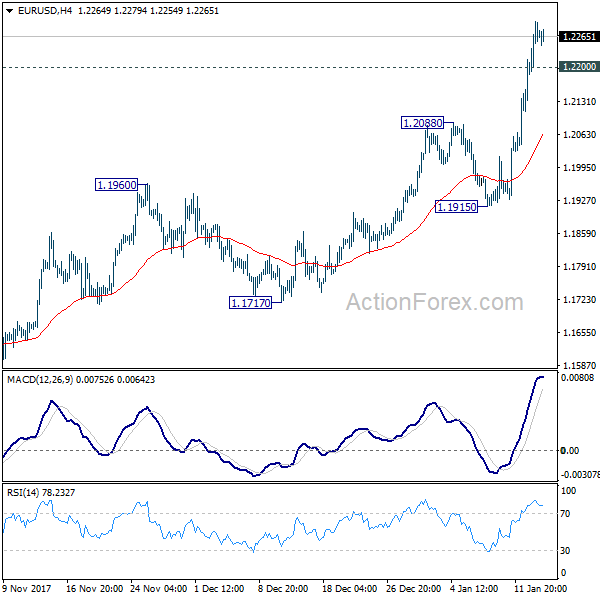

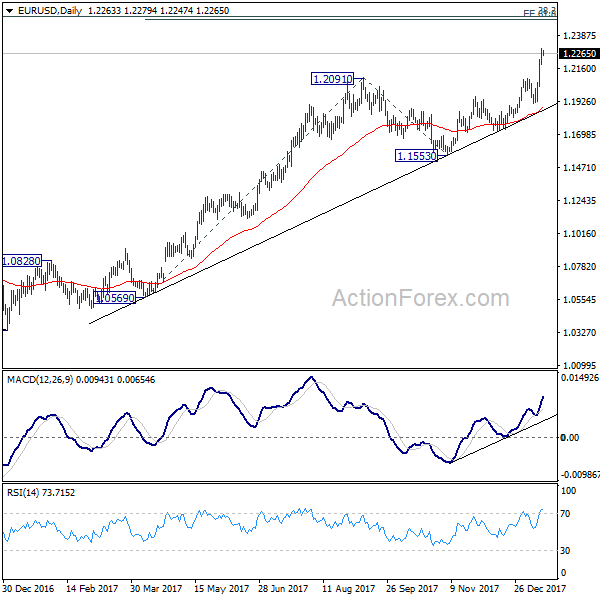

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.2202; (P) 1.2249 (R1) 1.2311; More....

Intraday bias in EUR/USD remains on the upside at this point. Current rally is targeting 1.2494/2516 key resistance zone next. At this point, we'd continue to expect strong resistance from there to limit upside and bring reversal. On the downside, below 1.2200 minor support will turn intraday bias neutral first. But near term outlook will stay bullish as long as 1.1915 support holds.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494. Break of 1.1553 support will confirm completion of the rise. However, sustained break of 1.2516 will carry larger bullish implication and target 38.2% retracement of 1.6039 to 1.0339 at 1.3862.