Sample Category Title

Week Ahead – Bank of Canada Ponders Raising Rates Again; Aussie Eyes Jobs Data and China GDP

The Canadian and Australian dollars will be in focus next week as the Bank of Canada holds its first monetary policy meeting of the year, while Australian employment and Chinese growth figures will test the aussie's recent bull run. Other highlights will include inflation data out of the UK and the Eurozone. But the US will see a quieter week in terms of economic releases.

China's economy likely slowed in Q4

China will be the first major economy to report fourth quarter growth data when it publishes its GDP numbers on Thursday. After growing by 6.9% year-on-year in the first half of 2017 and 6.8% in the third quarter, China's growth rate is expected to moderate slightly to 6.7% in the final three months of the year, giving a full year figure of 6.8%. China's Premier, Li Keqiang, said this week it expects growth of 6.9%. But a weaker growth is possible too given that authorities have been intensifying their efforts to cut excess capacity and pollution. Also to watch out of China next week are December figures for industrial output, retail sales and fixed asset investment.

Positive numbers from China could spur the Australian dollar higher to back above $0.79, after testing the level on Friday for the first time since September 2017. However, data out of Australia should also attract bets in the aussie/dollar pair as December employment figures are released on Thursday. Recent data out of Australia have been on the strong side, helping the aussie rebound sharply from its December 6-month low. Another strong jobs report next week could strengthen the currency's upside momentum, putting the $0.80 handle within reach.

Japan reports producer prices and machinery orders

The yen soared against its major peers this week after a small reduction in long-dated government bond purchases by the Bank of Japan in a regular market operation on Tuesday prompted speculation that the BoJ may soon announce a scaling back of its stimulus program. Data out of Japan next week are unlikely to trigger similar moves but will nevertheless be watched to gauge the strength of the Japanese economy. Starting with corporate goods prices on Tuesday, Japan's equivalent of producer prices is forecast to rise a solid 0.4% month-on-month in December, though the year-on-year rate is expected to ease from 3.5% to 3.2%. Machinery orders will follow on Wednesday. Core machinery orders - a good indication of business expenditure - is forecast to decline by 1.4% m/m in November after a 5% jump in October.

Is UK inflation peaking?

Inflation (Tuesday) and retail sales (Friday) numbers will be the focus for pound traders next week as they could give clues as to whether the Bank of England is likely to raise interest rates this year. The 12-month CPI rate hit a near 6-year high of 3.1% in November. It is expected to edge down to 3.0% in December - perhaps a sign that the upside price pressures generated by sterling's sharp devaluation following the Brexit referendum are starting to subside. Core inflation is also forecast to ease slightly, from 2.7% to 2.6% y/y. Retail sales meanwhile will likely take the shine away from the optimistic picture painted by the November industrial output figures which surged on the back of the weaker pound and rising global demand. Retail sales are forecast to drop 0.6% m/m in December after an unexpectedly strong November.

The Eurozone will also publish inflation figures. The final readings for December are expected to show CPI unrevised at 1.4%, but core CPI being revised lower from 1.1% to 0.9% y/y. A downward revision in the core rate could provide investors with an excuse to take profit on the euro's impressive gains this week when it broke above the key $1.21 level for the first time since January 2015.

Few attractions out of the US

US releases will be scarce next week with Wednesday's industrial production figures for the month of December, Thursday's data on housing starts for the same month and Friday's preliminary survey on January consumer sentiment by the University of Michigan expected to draw the most attention.

Industrial output is expected to exhibit positive growth for the fourth straight month, expanding by 0.5% m/m, a faster pace relative to November's 0.2%. Manufacturing output figures - a subset of industrial output ones - will also be watched. Moving to housing starts, it would be interesting to see if they continue coming in solidly after reaching a more than a decade high in November. Lastly, the University of Michigan's survey is expected to reflect an improvement in consumer sentiment, following the previous month's decline. Other notable releases in the coming seven days are the Empire State Manufacturing index (Tuesday) and the Philly Fed Business index (Thursday).

Bank of Canada headed for third rate hike in six months

Canada's economy continues to confound expectations with recent data on employment and retail sales suggesting the output gap is fast closing. This fuelled expectations that the Bank of Canada will raise rates for a third time since July when it meets on Wednesday. Futures markets are currently implying a more than 90% probability that the overnight rate target will rise from 1.0% to 1.25%. However, some analysts are warning that the BoC may decide to wait a little longer before hiking rates again so soon. Concerns about the possible termination of NAFTA and flat growth in monthly GDP in October may dissuade the BoC from taking early action.

A surprise no change in policy would be negative for the Canadian dollar, which rallied to a 3-month high of C$1.2354 to the US dollar in early January on the expectations of a rate rise this month, before retreating to around C$1.25 on renewed NAFTA worries.

Weekly Focus: Strong Start to 2018 Amid Increasing US-China Tensions

Market movers ahead

- Overall, it looks like a fairly quiet week on the news front. In the US, industrial production and more Fed speeches should not give a big change to the outlook.

- China GDP for Q4 is set to show growth of 6.7% y/y. This would leave overall growth for 2017 at 6.8% or 6.9%.

- In the euro area, we are set to get more details on December inflation with the final release. We estimate UK inflation fell back below 3% in December.

- In Scandinavia, we expect the most interesting data to be Swedish house prices (HOX), where we look for a further decline in Stockholm flats of 2.6% m/m, taking the cumulated decline to 12% since August 2017.

Global macro and market themes

- We are still positive on equities, as global growth remains solid, although the acceleration phase is likely to be over soon.

- Inflation remains one of the most important topics this year. Despite higher oil prices, we expect core inflation to remain subdued.

- In our view, markets have priced the ECB too aggressively, as we see the first ECB hike in Q2 19.

- Increasing tension between the US and China is a cause for concern.

GBPJPY Rallies; Corrective Move or Shift in Trend?

GBPJPY shifted out of its neutral phase and has turned more bullish in the short term to regain the 151 handle. Looking at the 4-hour chart, the pair appears to have put in a base after falling to its lowest level in around 3 weeks.

The pair is strengthening after making an aggressive move higher to breach what was a firm resistance level at 151 and the rally may have legs to move higher towards the next key level at 152. RSI is rising and has reached the 50 level, although it hasn't broken it yet.

Minor support is expected at 150.50 and below this, the focus turns to 150 ahead of a re-test of the mid-December low of 149.40, with additional weakness seen from here.

Unless GBPJPY reaches into the 152 handle soon, then upside momentum may fade fast and the recent recovery would be seen as merely a corrective move of the downtrend from January 8 and not a shift in trend. A breach of 153 resistance is needed to bring GBPJPY back to a bullish market structure.

Still Not Much Heat in US Inflation – But is that a Barrier to Further Rate Hikes?

Highlights:

- All items CPI met market expectations with a 0.1% month-over-month increase in December. Lower energy prices limited the gain, unlike November when they contributed to a 0.4% headline increase.

- All items inflation edged down to 2.1% year-over-year from 2.2% in November.

- Excluding food and energy, prices were up 0.3% in December—the largest monthly increase since last January. December's gain was helped by a 0.4% increase in the sizeable shelter component.

- Core inflation edged up to 1.8% year-over-year in December but has been stuck in a tight 1.7-1.8% range over the last eight months.

The December CPI report caps off a year that saw little evidence of tight economic conditions fueling higher consumer prices. The headline rate of 2.1% is exactly where it was a year earlier, while core inflation remains stuck below the Fed's 2% objective after having been on the opposite side throughout 2016. That is despite the unemployment rate falling to 4.1%—below most estimates of what the economy can sustain without driving inflation higher. It remains the case that without the impact of one-off factors like a sizeable dip in wireless telephone service prices, core inflation would be right around the 2% mark. But still there is limited evidence that underlying inflation is actually heating up. That continues to be a sticking point for some members of the FOMC who are reluctant to raise interest rates further in the absence of greater inflationary pressure.

However, those on the other side who are concerned about upside risks to the inflation outlook now have a bit more ammunition thanks to the tax cuts passed in December. With the economy already running near full capacity, this fiscal boost arguably will need to be offset by tighter monetary policy. A pickup in inflation would certainly help make the case, but even if current price trends hold we think policymakers have to be concerned about falling behind the curve. So while core inflation is likely to remain stuck below 2% early this year, we continue to expect the Fed will raise rates again in March.

U.S Core CPI Posts Largest Increase in 11-Months

U.S headline inflation was muted as expected last month (+0.1% vs. +0.1%e m/m), but there was movement in the closely watched underlying measure.

Core-CPI prices, ex-food and energy, increased a seasonally adjusted +0.3% in December from a month earlier, the largest increase since January 2017.

Digging deeper, the gain in core-prices can be attributed largely to shelter inflation, which had been slowing over the past year but rose +0.4% in December. Besides shelter, the indexes for medical care, used cars and trucks, and new vehicles all contributed to the rise in core prices. The index for prescription drugs, which had weakened earlier this year, rose 1% in December on the back of a 0.6% increase in November.

Note: Shelter accounts for about a third of the overall consumer price index.

U.S Retail sales ends last year on solid footing

U.S retail stores, restaurants and online-shopping platforms closed out December on a strong note.

Data this morning showed that U.S retail and food services sales rose a seasonally adjusted +0.4% in December from the prior month, the fourth straight increase. Ex-autos and gas, sales also rose +0.4% in November.

Total sales in Q4 were up +5.5% from the same period a year earlier. For 2017 as a whole, overall sales rose +4.2% from the prior year, the strongest annual growth in three years.

USD/CAD – Subdued as US Inflation, Retail Sales Within Expectations

USD/CAD is subdued in the Friday session. Currently, the pair is trading at 1.2535, up 0.08% on the day. On the release front, there are no Canadian events. In the US, Retail Sales and CPI reports were within expectations.

There was unexpected news out of China on Wednesday. A report that China was considering slowing the purchase of US government bonds shook up the currency markets and sent the Canadian dollar lower. China boasts the largest currency reserves, estimated at $3 trillion. It is also the biggest holder of US government bonds, in the amount of $1.19 trillion. China is unlikely to halt all purchases, but its vast holdings of US bonds could serve as leverage in a trade war with the US. President Trump has railed against the US trade imbalance with trade with China, and by serving notice that it might reduce its US Treasury purchases, China appears to be flexing some muscle. If China does indeed make any moves regarding these bond purchases, traders can expect sharp market movement.

After strong gains in December, the Canadian dollar has held its own against the greenback in January. There are two important factors for this positive trend. First, Canada has recorded outstanding employment numbers in the past two months. In December, the economy added 78.6 thousand jobs, defying experts who predicted a minuscule gain of 1.8 thousand. This release comes on the heels of a superb November release, when the economy added 79.5 thousand news jobs. The unemployment rate dropped to 5.7% in December, down from 5.9% a month earlier. Second, the recent rise in oil prices, which are up 6.8% since mid-December, has boosted the commodity-based Canadian currency. The BoC is expected to raise rates later this month, which could boost the Canadian dollar.

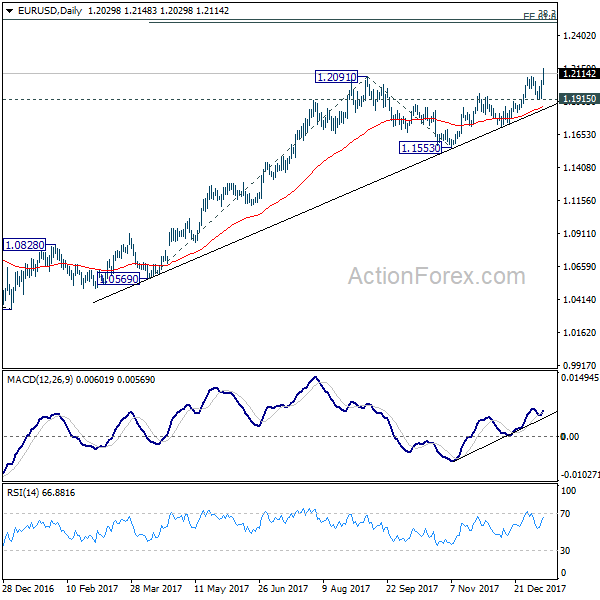

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1953; (P) 1.2006 (R1) 1.2084; More....

EUR/USD's firm break of 1.2091 resistance today indicates resumption of medium term rise from 1.0339. Intraday bias is back on the upside. Current rise should target 1.2494/2516 key resistance zone next. On the downside, break of 1.1915 support is needed to confirm short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494.

Euro Extends Rally on Breakthrough in German Coalition Talks, Dollar Gets No Support from CPI

EUR/USD powers through 1.21 handle today on new that German Chancellor Angela Merkel has achieved some breakthrough in forming the new coalition government. It's reported that Merkel has struck a deal with the Social Democrat to formally open talks for reforming the grand coalition. The marathon talks were closed with a 28-page blue print between the CDU/CSU and SPD. Close cooperation with France to strengthen the Eurozone is one of the key point of the blue print.

Merkel said after the talks that "we have felt since the elections that the world will not wait for us, and in particular regarding Europe we are convinced we need a new call for Europe". She also noted that "there will be difficult tasks to come" and, "the coalition negotiations probably won't be easier than the exploratory talks."

SPD leader Martin Schulz said in the joint press conference that there were "turbulent moments" during the talks but negotiators "never faced the risk of failure".He pledged that 'we want to ensure economic and political power for Germany is put towards creating a stronger Europe."

Released from US, headline CPI rose 0.1% mom, 2.1% yoy in December, slowed from 2.2% yoy but met expectations. Core CPI, on the other hand, beat expectation of rose 0.3% mom, 1.8% yoy. Headline retail sales rose 0.4% mom in December, while ex-auto sales also rose 0.4%. But the data provides little support to the greenback.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1953; (P) 1.2006 (R1) 1.2084; More....

EUR/USD's firm break of 1.2091 resistance today indicates resumption of medium term rise from 1.0339. Intraday bias is back on the upside. Current rise should target 1.2494/2516 key resistance zone next. On the downside, break of 1.1915 support is needed to confirm short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494.

Will December’s US Inflation Report Rescue the Dollar?

The Dollar sharply depreciated against a basket of major currencies on Friday after weaker-than-expected U.S. factory inflation data doused market optimism over inflation accelerating in 2018.

U.S. producer prices dished out a downside surprise by falling 0.1 in December which was the first decline in nearly 18 months. With yesterday's soft factory inflation figures leaving a bitter aftertaste on rate hike expectations, today's pending CPI data is a big deal and potential market shaker. The headline CPI is expected to decelerate to 2.1% y/y in December, while core inflation is predicted to remain steady at 1.7% y/y. A disappointing U.S. inflation report that prints below market expectations has the ability to fuel growing dissent within the Fed on when to raise U.S. rates. Naturally, the renewed concerns over low inflation in the States are likely to cloud prospects of higher U.S. interest rates, ultimately punishing the Dollar.

Alternatively, the Greenback could be granted a lifeline today if inflation figures offer an upside surprise and defy market expectations.

Focus will also be directed towards the U.S. retail sales figures which are expected to be +0.4% for the month of December. A retail sales figure that meets or exceeds market expectations could boost sentiment towards the U.S. economy and provide some support to the vulnerable Dollar.

Taking a look at the technical picture, the Dollar Index is unquestionably bearish on the daily charts as there have been consistently lower lows and lower highs. The decisive break down below the 91.80 support level has opened a path lower towards 91.20 and 91.00, respectively.

Euro Thrives on Political Relief; US CPI & Retail Sales Awaited

Here are the latest developments in global markets:

FOREX: Hopes that the ECB will step back from its monetary stimulus and bets that Germany will form a grand coalition government soon added further gains to the euro during early European trading hours. Merkel's Conservatives and their former coalition partners Social Democrats agreed today on a blueprint to formally start coalition negotiations. Euro/dollar rallied to a three-year high of 1.2136 (+0.76%), euro/yen surged to 134.78 (+0.64%) and euro/pound remained flat at 0.8891. The dollar index took a knock in the face of a strengthening euro, diving to a four-month low of 91.30 (-0.52%), while dollar/yen tumbled to a six-week trough of 111.12. The pound was also benefiting from a rising euro and a weaker dollar, with pound/dollar peaking at 1.3640, a level last seen in September.

STOCKS: Decreasing political risks in Germany offered little comfort to European stocks as the focus was mainly on earnings releases. The pan-European STOXX 600 offset earlier losses, edging up by 0.11% on the day after the British engineer GKN rejected a takeover from the rival Melrose, deciding instead to break the automotive and the aerospace divisions into two companies. A new chief executive was also declared. GKN shares jumped by 26%. The blue-chip Euro STOXX 50 was slightly up by 0.10% at 1100 GMT. The German DAX 30 rose by 0.22% driven by consumer cyclicals, the French CAC 40 increased by 0.30% while the Italian FTIMB jumped by 0.52%. The British FTSE 100 was up by 0.24%. US Stock futures were in the green, pointing to a positive open.

COMMODITIES: Oil prices were on the backfoot on Friday, slipping below three-year highs but were also on track to post a weekly gain for a fourth consecutive time. Investors believe that the market is overheating. WTI crude oil fell by 0.63% to $63.38 per barrel and Brent declined by 0.27% to $69.07. Gold stretched its uptrend to a fresh four-month high of $1332.96 per ounce.

Day ahead: US CPI & retail sales pending; eyes on euro

The dollar will be exposed to several economic releases during the European afternoon on Friday, while political developments in Europe have also the potential to influence the currency in the upcoming days.

At 1330 GMT, the Bureau of Labor Statistics will release figures on US consumer prices, with the headline index expected to inch down in December. Particularly, analysts expect consumer prices to rise at a softer pace of 2.1% y/y compared to 2.2% growth seen in November. The monthly gauge is also projected to ease from 0.4% to 0.2% in the aforementioned month. On the other hand, the core equivalent which excludes food and energy items is said to remain flat at 1.7% y/y and the monthly growth to edge up by 0.1 percentage points to 0.2% m/m. However, even if the CPI is a common inflation measure, it tends to have a relatively softer impact on the dollar as the Fed states its inflation goals and therefore decides on monetary policy based on the PCE index due on January 29.

Meanwhile, the US Census Bureau will be publishing stats on retail sales for the month of December. Forecasts are for the measure to rise by 0.4% m/m after posting impressive growth of 0.8% in the prior month. Leaving automobile sales aside, core retail sales are anticipated to expand by 0.4% as well.

Business inventories will follow at 1500 GMT, with the monthly gauge estimated to turn to positive growth rates in November after retreating slightly in the preceding month.

In terms of public appearances, the FOMC member, and Boston's Fed President, Eric Rosengren will speak on the economic outlook at 2115 GMT.

Yet, the euro's performance during the day will play an important role on whether the dollar will succeed to strengthen even if the data comes in positive. Earlier, news out of Germany stating that Merkel's Conservatives achieved a political breakthrough drove the euro to a fresh 2 ½-year high and pushed the dollar to bearish territory.

In oil markets, traders will keep a close eye on the US Baker Hughes oil rig counts due at 1800 GMT.