Sample Category Title

USDJPY Retains Short-Term Neutral Stance Around 50-Day MA

USDJPY retains a short-term neutral stance on the daily chart, confirmed by the flat technical indicators. The RSI is neutral, while the 50 and 200-day moving averages are moving sideways. In the bigger picture, the pair has been trading in a range between 108 and 114 since March and is currently located in the upper end of this range.

Additional gains are possible since the market is above the two moving averages and RSI is above 50. A pick up in upside momentum would help push prices to the top of the range at 114 and re-test the prior high at 114.73. These two levels are creating a strong resistance zone, which if broken would shift the overall bias to bullish and likely propel USDJPY towards the 115 handle.

Failure to rise above 114 in the short-term could see prices slip down towards 113 and 112.97, which is an area of support around the 50-day MA. A decline from here would shift focus to the 200-day MA and the bottom of the long-term range at 111.

The near-term bias is expected to remain neutral around the 50-day MA. USDJPY is likely going to continue to trade sideways between 112 and 114 for now. There is no change to the medium-term neutral outlook.

Bitcoin Recovers As Markets Enter Sleep Mode

With most financial markets in vacation mode, Bitcoin is the only currency making big moves in a holiday-thinned trading week.

After crashing by more than $8,000 from an all-time high, Bitcoin is up 3.5% at the time of writing. Although the recent plunge frightened many bitcoin fans, when looking at the relatively short history of bitcoin trading, the price action seems just normal. During 2017 the cryptocurrency crashed by 30% or more six times. Every fall was followed by huge price appreciation until it peaked on 17 December.

Whether the Bitcoin bull market is close to an end or just pausing for a short break, remains to be a wild question for 2018. I still believe that Bitcoin is in a bubble formation. However, there’s no effective test to measure at which stage we are currently standing. For example, equity prices may be said in a bubble territory if investors are willing to pay much more for a stock than the intrinsic value which is justified by the discounted divided stream. Similarly, econometric tests may be run on bonds, commodities, currencies or any other asset to come up with a justified value. For Bitcoin, there isn’t any fundamental basis to justify the price.

Traders should look at multiple factors to anticipate the next move, such as government regulations, hedge funds interest, the stability of the network, and broader mainstream adoption.

However, latest signs are not encouraging. Here are a few:

- Israel became the most recent country to propose banning companies based on digital currencies to trade on its stock exchange.

- A South Korean bitcoin exchange has been hacked, leading it into bankruptcy.

- Cryptocurrency exchanges are disabling transaction temporarily due to high traffic.

- Professional traders on CBOE seems to be going short on Bitcoin.

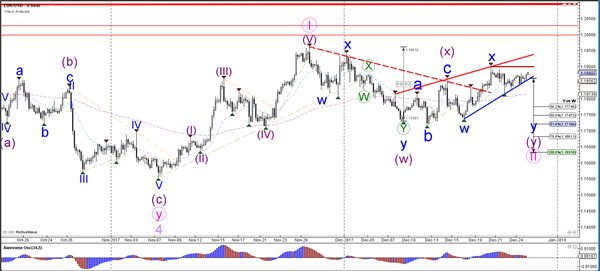

Daily Wave Analysis: EUR/USD Challenges 1.19 Resistance And Rising Wedge Pattern

Currency pair EUR/USD

The EUR/USD is building a rising wedge chart pattern (red/blue lines). A bullish breakout could indicate a continuation of the uptrend whereas a bearish reversal could send the EUR/USD lower to test the wave 2 vs 1 (pink) and the Fib levels of wave Y (purple).

The EUR/USD is testing the Fibonacci levels of wave X (green). A break below the support trend line (blue) could be a larger bearish correction.

Currency pair GBP/USD

The GBP/USD is in a bull flag and triangle chart pattern, which is indicated by the support (blue) and resistance (red) trend lines. A bullish breakout could confirm a wave 5 of wave C. A break below the lowest support line makes a wave 4 less likely.

The GBP/USD seems to be building a potential ABC (blue) within a wave 3 (green).

Currency pair USD/JPY

The USD/JPY needs to break below support before a bearish reversal becomes more likely whereas a break above resistance could indicate and uptrend continuation.

The USD/JPY is facing important and critical support (blue) and resistance (red) trend lines.

Market Update – Asian Session: Equity Volume Remains Light

General Themes: Asia indices trade mixed, in line with the NY session

Energy companies outperform

Chipmakers in South Korea rebound

World's Largest Shipbuilder Hyundai Heavy share price declines by record on capital raise

PBoC skips OMO for 4th straight session amid signs of ‘high bank liquidity’ into year-end

China Nov Industrial Profits grow at slowest pace since April

Australia

ASX 200 opened flat: closed flat

ASX 200 Resources Index +0.7%, Energy +0.7%; Financials -0.1%

ORL.AU Enters binding deed with Mr J Will Vicars for proposed whole business outcome and continuation of operations

RFG.AU Extended 3-year debt facility which was due to mature in Dec 2018 to 2020; reduces 5-year credit facility amount by A$25M; +9%

China/Hong Kong

Shanghai Composite opened -0.1%, Hang Seng +0.2%

Hang Seng Information Energy Index +1.8%, Property/Construction +1.8%; Technology -1%

Herbal products firm Bawang International -30% (bankruptcy concerns)

(CN) China Nov Industrial Profits Y/Y: 14.9% v 25.1% prior (slowest rise since April); China Stats Bureau cited prices for the slowdown in the data

(CN) China Beige Book: industrial firms continued to ramp up output in Q4, wages and hiring dipped with the retail sector lagging other industries an acute hit on weak rev; see slower growth in 2018

(CN) China State Researcher: China's economy hasn't bottomed out - China Daily

(CN) China PBoC sets yuan reference rate at 6.5421 v 6.5416 prior

(CN) PBoC OMO: Skips OMO v skips prior; Net drain CNY40B v CNY50B drain prior (4th consecutive skip)

(CN) China Party Central Committee Meeting to hold plenary in January - Xinhua

(CN) China 2018 registered unemployment rate may be 4%; surveyed unemployment 5% - China Securities Journal

(CN) China NDRC on alert over surge in chip prices - China Daily

(CN) China Tangshan City issues pollution alert for Tuesday – financial press (**note: Tangshan, home to dozens of steelmakers, is located in heavily-polluted Hebei province, China's biggest steelmaking region. Hebei produced 192.6 million tonnes of steel last year, nearly a quarter of the national total)

(CN) China Information Daily: China will fight against online finance violations

HNA Group: Bohai Capital unit received China CSRC approval to sell up to CNY4.0B in bonds

(CN) China risk reduction efforts to focus on three main areas: state-owned enterprise leverage, local debt risk, and the asset management industry - Economic Information Daily

(CN) Some China interbank deposit rates hit record high in December - China Securities Journal

In China 734 bond issues have either failed or been canceled during the first 11 months of 2017, amounting to CNY586.6B v last year’s total canceled or failed issues worth CNY577.5B

China Securities Journal discusses recent appreciation in yuan, driven largely by sharp drop in the US dollar index

(CN) PBoC Adviser: forecasts yuan consolidation after recent gains - China press

Japan

Nikkei 225 opened -0.2%; closed +0.1%

TOPIX Securities Index +1.3%, Iron/Steel +0.7%

J Front Retailing +7% (9-month profits +24%); Fast Retailing +1%

Kawasaki Heavy Industries +7% (broker commentary)

Japan govt reportedly could boost penalties for manufacturers who falsify product quality data - Nikkei

Japan Center for Economic Research Survey shows expect avg CPI of 0.9% in FY18, higher than actual 0.6% rate achieved in the April-November period and the highest since FY08

The number of IPOs in Japan in 2017 made it the second busiest year on record – Nikkei

(JP) JAPAN NOV HOUSING STARTS Y/Y: -4.2% V -2.5%E; ANNUALIZED HOUSING STARTS: 951K V 934KE; Construction Orders y/y: 20.5% v +6.7% prior

Looking Ahead: Japan prelim Nov Industrial Production data due on Thursday

Korea

Kospi opened -0.3%

Hyundai Heavy -28% (announced KRW1.29T capital raise)

Broad weakness in financial sector: Woori -3%, KB Financial -2.4%

Chipmakers rebound from Tuesday’s declines: Samsung Electronics +1.2%, Hynix +1.9%

LG Electronics +6.5%; Announces autonomous car partnership with Here Technologies

Korean (KRW) trades at 2 ½ year high

South Korea Dec Consumer Confidence: 110.9 v 112.3 prior

China delays 3-way summit with Japan and South Korea – Yomiuri

(KR) US Treasury announces sanctions targeting two North Korea officials

(KR) According to Korea Economic Research Institute South Korean economy will likely take a hit from a reversal of top corporate tax rates in Asia's fourth-largest economy and the United States

010620.KR Guides FY18 orders $3.0B, affirms FY17 orders $2.31B; -21%

Looking Ahead: South Korea Nov Industrial Production, Retail Sales and Service Sector Output data due on Thursday

Other Asia

USD/TWD (TW) Taiwan Central Bank Deputy Gov Yang Chin-long: Taiwan Dollar (TWD) appreciation reflects US dollar weakness and the appreciation this year is not big

(TW) Taiwan Premier: Affirms sees 2018 GDP growth of 2.3%; to implement policy loosening and increase investment in 2018; Calls for higher salaries at listed companies.

North America

US equities ended mixed: Dow flat, S&P500 -0.1%, Nasdaq -0.3%, Russell 2000 +0.1%

S&P500 Energy sector +0.9%; Technology -0.7%

(RU) Russia said to limit US open skies access, starting Jan 1st; in response to planned US curbs

(US) Pres Trump tweets: "All signs are that business is looking really good for next year, only to be helped further by our Tax Cut Bill. Will be a great year for Companies and JOBS! Stock Market is poised for another year of SUCCESS!"

(LY) Explosion reported at Waha Oil pipeline feeding Es Sider terminal inLibya (production approx 260K bpd); Waha output reportedly down about 70K bpd after the incident - financial press

Levels as of 01:00ET

Nikkei225 +0.1%, Hang Seng +0.1%; Shanghai Composite -0.3%; ASX200 flat, Kospi +0.3%

Equity Futures: S&P500 +0.1%; Nasdaq100 +0.1%, Dax +0.2%; FTSE100 +0.3%

EUR 1.1880-1.1855; JPY 113.36-113.17; AUD 0.7747-0.7724;NZD 0.7053-0.7029

Feb Gold -0.0% at $1,287/oz; Feb Crude Oil -0.4% at $59.76/brl; Mar Copper -0.5% at $3.26/lb

Aussie Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the AUD rose 0.06% against the USD and closed at 0.7726.

LME Copper prices rose 0.6% or $42.0/MT to $7019.0/MT. Aluminium prices rose 1.4% or $28.5/MT to $2137.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7739, with the AUD trading 0.17% higher against the USD from yesterday’s close.

The pair is expected to find support at 0.7721, and a fall through could take it to the next support level of 0.7702. The pair is expected to find its first resistance at 0.775, and a rise through could take it to the next resistance level of 0.7760.

With no macroeconomic releases in Australia today, investor sentiment would be governed by global macroeconomic factors.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

German GfK Consumer Sentiment Surprisingly Advanced In January

For the 24 hours to 23:00 GMT, the EUR declined 0.11% against the USD and closed at 1.1857.

On Friday, data indicated that Germany’s GfK consumer confidence index recorded an unexpected rise to a level of 10.8 in January, highlighting that consumers grew optimistic over the country’s growth prospects in the new year. Market participants had expected the index to remain steady at a level of 10.7.

Macroeconomic data released in the US showed that the Dallas Fed manufacturing business index climbed to a more than eleven-year high level of 29.7 in December, beating market expectations for a rise to a level of 20.0. In the prior month, the index had registered a level of 19.4. On the other hand, the nation’s Richmond Fed manufacturing index declined more-than-anticipated to a level of 20.0 in December, compared to market consensus for a drop to a level of 21.0 and after recording a reading of 30.0 in the prior month.

On Friday, data revealed that the preliminary durable goods orders in US rebounded 1.3% in November, amid a jump in orders for civilian and defence aircraft. Durable goods orders had registered a drop of 0.8% in the previous month, while investors had envisaged for a rise of 2.0%. Moreover, the nation’s new home sales surged to a ten-year high level in November, after it advanced more-than-estimated by 17.5% on monthly basis to a level of 733.0K, compared to a revised level of 624.0K in the previous month. On the contrary, the nation’s final Reuters/Michigan consumer sentiment index dropped to a three-month low level of 95.9 in December, while the preliminary figures had recorded a fall to a level of 96.8. The index had posted a reading of 98.5 in the prior month.

Other data indicated that the nation’s personal spending jumped more-than-expected by 0.6% on a monthly basis in November, following a revised gain of 0.2% in the previous month, while markets were expecting for an increase of 0.5%. Meanwhile, the nation’s personal income climbed 0.3% in November, falling short of market expectations for an advance of 0.4%. In the previous month, personal income had registered a rise of 0.4%.

In the Asian session, at GMT0400, the pair is trading at 1.1863, with the EUR trading marginally higher against the USD from yesterday’s close.

The pair is expected to find support at 1.1847, and a fall through could take it to the next support level of 1.1831. The pair is expected to find its first resistance at 1.1879, and a rise through could take it to the next resistance level of 1.1895.

Amid no macroeconomic releases in the Euro-zone today, traders would keep a close watch on the US consumer confidence index for December, followed by pending home sales data for November, both scheduled to release later in the day.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

UK’s Economy Expanded As Initially Estimated In 3Q 2017

For the 24 hours to 23:00 GMT, the GBP slightly declined against the USD and closed at 1.3373.

Data released on Friday showed that Britain's final gross domestic product (GDP) rose 0.4% on a quarterly basis in the third quarter of 2017, confirming the flash estimate. The nation's GDP had registered an advance of 0.3% in the previous quarter.

In the Asian session, at GMT0400, the pair is trading at 1.3378, with the GBP trading marginally higher against the USD from yesterday's close.

The pair is expected to find support at 1.3354, and a fall through could take it to the next support level of 1.3331. The pair is expected to find its first resistance at 1.3395, and a rise through could take it to the next resistance level of 1.3413.

Moving ahead, investors would focus on the release of UK's BBA mortgage approvals data for November, due in a few hours.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Japan’s Jobless Rate Surprisingly Declined To A 24-Year Low Level In November

For the 24 hours to 23:00 GMT, the USD declined 0.11% against the JPY and closed at 113.21.

In economic news, Japan’s unemployment rate recorded an unexpected drop to 2.7% in November, hitting its lowest level since November 1993, suggesting that robust economic recovery in the world’s third largest economy is strengthening the nation’s labour market. Market participants had expected the unemployment rate to remain steady at 2.8%. Moreover, the nation’s national consumer price index (CPI) rose more-than-expected by 0.6% on an annual basis in November, but remained far from the Bank of Japan’s (BoJ) 2.0% inflation target. In the previous month, the CPI had recorded a rise of 0.2%, compared to market consensus for a rise of 0.5%.

Separately, according to minutes of the Bank of Japan’s (BoJ) October meeting, officials stressed the need to stick to the central bank’s ultra-loose monetary policy until it reaches the inflation target.

On Monday, data showed that the nation’s final coincident index rose less than initially estimated to a level of 116.4 in October, compared to a level of 116.2 in the previous month, while the preliminary figures had indicated an advance to 116.5. Meanwhile, the nation’s final leading economic index surprisingly climbed to a level of 106.5 in October, while the preliminary print had indicated a drop to a level of 106.1. In the prior month, the index had registered a reading of 106.4.

In the Asian session, at GMT0400, the pair is trading at 113.26, with the USD trading slightly higher against the JPY from yesterday’s close.

The pair is expected to find support at 113.13, and a fall through could take it to the next support level of 113.01. The pair is expected to find its first resistance at 113.37, and a rise through could take it to the next resistance level of 113.49.

Moving ahead, investors would focus on the BoJ’s summary of opinions report of its December meeting along with Japan’s flash industrial production, retail trade and large retailers’ sales, all for November, due to release overnight.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages

Swiss Franc Trading A Tad Higher In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.1% against the CHF and closed at 0.9897.

On Friday, data indicated that Switzerland’s KOF leading indicator climbed to a level of 111.3 in December, compared to a revised reading of 110.4 in the previous month, while markets had expected for a rise to a level of 110.5.

In the Asian session, at GMT0400, the pair is trading at 0.9896, with the USD trading slightly lower against the CHF from yesterday’s close.

The pair is expected to find support at 0.9883, and a fall through could take it to the next support level of 0.9871. The pair is expected to find its first resistance at 0.9912, and a rise through could take it to the next resistance level of 0.9929.

Ahead in the day, market participants would closely monitor Switzerland’s ZEW expectations index for December and UBS consumption indicator November.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Canada’s Economic Growth Unexpectedly Stalled In October

For the 24 hours to 23:00 GMT, the USD declined 0.28% against the CAD and closed at 1.2689.

On Friday, data revealed that Canada's gross domestic product (GDP) surprisingly remained flat on a monthly basis in October, defying market expectations for an advance of 0.2%, thus diminishing the odds of an interest rate hike by the Bank of Canada (BoC) in the near-term. In the previous month, the GDP had risen 0.2%.

In the Asian session, at GMT0400, the pair is trading at 1.2686, with the USD trading slightly lower against the CAD from yesterday's close.

The pair is expected to find support at 1.2671, and a fall through could take it to the next support level of 1.2655. The pair is expected to find its first resistance at 1.2715, and a rise through could take it to the next resistance level of 1.2743.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.