Sample Category Title

EURGBP Still Holds in a Bearish Sideways Channel; Remains Vulnerable

EURGBP has been creating a bearish sloping channel since October after the peak at the 0.9030 resistance level. However, the pair is on track to post its second bullish week after the rebound from the five-month low at 0.8690.

Looking at the 4-hour chart, in the short-term timeframe, the price is holding below the 0.8890 strong obstacle, while it is above the three simple moving averages (50, 100 and 200). Additionally, the pair hit the 23.6% Fibonacci retracement level with the high at 0.9305 and the low at 0.8690 on Wednesday and the next immediate resistance barrier to have in mind is 0.8890.

On the reverse side, a slip below the aforementioned Fibonacci obstacle and a drop below 0.8827, which coincides with the 50-SMA in the short-term chart, could push the price towards the 0.8790 support level.

Short-term momentum is weak and the MACD oscillator is endorsing the scenario for further bearish movement as it lies below its trigger line. Although, the RSI indicator is pointing to the upside and is standing near the 50 level.

Traders may be in confusion as the tendency is not clear yet in EURGBP as it is trading in the middle of the sideways channel

Sharp Canadian Retail Sales Sends Loonie to 2-Week High

The Canadian dollar continues to improve, and has posted slight gains in Friday trade. Currently, USD/CAD is trading at 1.2720, down 0.14% on the day. On the release front, it's a busy day on both sides of the border. Canada releases its monthly GDP report, which is expected to remain unchanged at 0.2%. In the US, there are three key events – Durable goods reports are expected to improve, but the markets are braced for softer readings from New Home Sales and UoM Consumer Sentiment.

The Canadian currency is on track for its strongest weekly gains since September, after jumping 0.75% against the US dollar on Thursday. Canadian consumer numbers boosted the loonie, and pushed it to its highest level since December 12. Retail Sales sparkled with a gain of 0.8% in October, well above the forecast of 0.4%. This was the indicator's highest gain since April. As well, CPI improved to 0.3%, a five-month high. This edged above the estimate of 0.2%. If GDP follows suit and also beats the forecast, the Canadian dollar rally could continue.

Christmas has come early for President Trump, as he celebrated with Republican lawmakers the new tax reform bill. Earlier in the week, both branches of Congress passed the legislation, although the votes were tight, as all Democrats voted against the bill. It's a major victory for Trump, as one of his key campaign pledges was tax reform, and the new legislation marks the first overhaul of the tax code since the Reagan administration.

The US economy received an excellent report card on Thursday, as Final GDP posted a strong gain of 3.2%, just shy of the Preliminary GDP reading of 3.3%. With the US economy posting growth above 3% for another quarter, the Federal Reserve remains on track for another rate hike in January. The CME Group has pegged the odds of a January hike at 98%, and if the economy continues its current pace, the Fed could raise rates up to four times in 2018. Inflation remains a sore point, as the Fed target of 2.0% remains well out of reach. Fed Chair Janet Yellen and other FOMC members have said they expect that the strong labor market will lead to higher inflation, but the Fed has demonstrated that it is willing to press ahead with rate hikes despite low inflation.

US Data Eyed as Congress Delays Shutdown

- US Futures Higher as Congress Kicks the Can Down the Road;

- Catalans Give Independence Parties Slight Majority;

- Bitcoin Tumbles Again But Buyers Putting Up a Fight.

US Futures Higher as Congress Kicks the Can Down the Road

US equity markets are on course to open marginally higher on the final trading day before the Christmas break, with investors seemingly buoyed by not only the passage of tax reform through Congress but also efforts to delay a government shutdown until 19 January.

There's been some speculation that Donald Trump may sign that tax reform bill today, which will complete the formalities, although I think it's clear that any near term benefit for markets is now priced in. Friday is likely to be a little thin from a trading perspective, despite the fact that we will get income, spending and inflation data from the US, as well as new home sales, durable goods orders and consumer sentiment.

Catalans Give Independence Parties Slight Majority

The Spanish IBEX is underperforming its peers this morning while Spanish yields have ticked higher after the Catalan election failed to ease the problems in the region, as separatist parties sealed a small majority. To compound the issue further, Mariano Rajoy's People's Party was decimated at the polls, dropping eight seats to leave it with only three in the 135-seat Catalan assembly. Rajoy's next steps will be crucial, with the Spanish leader potentially now being forced into talks with the separatist groups in order to find a solution that appeases all concerned.

Bitcoin Tumbles Again But Buyers Putting Up a Fight

Bitcoin is trading in the red again on Friday and is headed for a sixth day of losses on the Bitstamp exchange, something we haven't seen in a very long time. What we're seeing in Bitcoin in recent days is what many people have been anticipating for a while which is speculators getting burned by a sharp and aggressive correction. The rally over the last couple of months has left Bitcoin vulnerable to this kind of move and it seems the run up to Christmas has triggered some profit taking on the rally and even a shift into some alternative coins.

We're now seeing a bounce from the earlier lows after a near 20% drop on the day but losses are still substantial. This period is going to be a big test of speculators appetite for these kinds of swings when we're seeing two-way price action, something we haven't seen too much of recently.

CAC Slips As Catalan Voters Rebuke Rajoy

.

The CAC index has lost ground in the Friday session. Currently, the index is at 5360.50, down 0.35% on the day. On the release front, there was only one event. French Consumer Spending climbed 2.2%, crushing the forecast of 1.4%.

The French economy continues to rebound, as indicators in the second largest economy in the eurozone continue to point upwards. The economy has been expanding, exports are up and unemployment has dropped. Consumer spending, a key driver of economic growth, looked sharp in November, jumping 2.2%. The impressive reading comes after a decline of 1.9% in October and marked the highest gain since February 2012. This is the final French event of 2017, and the stock markets are likely to be subdued during the Christmas holidays.

European stock markets are digesting the results of Thursday’s Catalan election. With no party winning an outright majority, the uncertainty could spook investors and hurt the stock markets. Although a nationalist party scooped up the most seats, three pro-independence parties have won 70 seats out of 135, good enough for a slim majority. The vote is a stinging rebuke for Spanish Prime Minister Mariano Rajoy, who has imposed direct rule on the region, called the snap election with the hope that the independence movement would lose momentum. However, this tactic clearly failed and Spain could be headed for more political turmoil in the coming months.

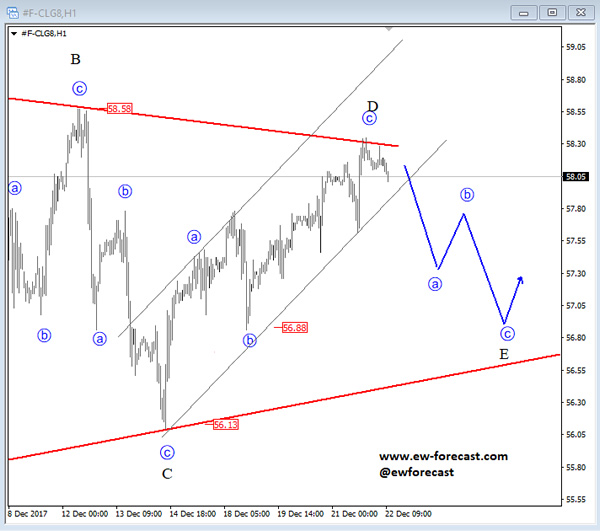

Elliott Wave Analysis: Crude Oil Points Higher, 60.0 Per Barrel Is In View

Crude oil is still trading choppy, slow and overlapping which suggests a bigger Elliott wave triangle correction to be in progress. Specifically we see price trading at the end of corrective leg D of a bigger triangle, that can see limited upside around the 58.30 level. A breach below the lower channel line would suggest a three-wave reversal within final leg E to be in progress. Support for corrective leg E can later be found at the 56.88 level, of a former swing low.

Crude oil, 1h

Below we have the 4h chart and its full development.

Crude oil, 4h

Another Turmoil In Spain Shakes European Markets

Pro-independence party in Catalonia won an absolute majority in regional elections

Catalonia will be radical enough to push for independence?

The trauma in Spain is leading the Spanish markets lower

Another blow for the Spanish Prime Minister, as the pro-independence party in Catalonia, won an absolute majority in regional elections. The three separatist parties won 70 seats collectively and this would help them to form a government as the threshold was 68. This would only escalate the tensions between Madrid and Barcelona whilst creating a major headache for investors as they will start to rekindle their thoughts in order to tackle this threat. Madrid without Barcelona only spells disaster, and nothing less. This is not something which you would like to digest as the first event in 2018, the hopes around making any reasonable compromises are completely shattered.

Heading in to 2018, investors are going to look at only aspect which is the threat of independence. The focus will be if the new government in Catalonia will be radical enough to push for independence. The recent failed attempt of independence in October clearly shows an example for the new upcoming government in what to avoid. It also provides them with a guidance where they have to make any changes in order to achieve a more favourable outcome.

The trauma in Spain is leading the Spanish markets lower this morning and it is also pushing other European markets lower too. The Euro is feeling some pain but nothing too dramatic because investors debate over the possibility of a fresh turmoil in Spain. The snap election in Spain hasn’t triggered the kind of outcome which Mr Rajoy was not hoping for. Perhaps, he would have to adopt a different approach given that he has suffered two failures. Spanish banking sector is where we are seeing the most blood and investors are hitting hard on the likes of Banco de Sabadell and CaixaBank SA.

DAX Under Pressure After Catalan Election

The DAX index has ticked lower in the Friday session. Currently, the index is at 13,079.50, down 0.23% on the day. In economic news, German indicators were solid. German GfK Consumer Climate inched up to 10.8, above the estimate of 10.7 points. As well, Import Prices gained 0.8%, up 0.6% from the previous release.

European stock markets are digesting the results of Thursday’s Catalan election. With no party winning an outright majority, the uncertainty could spook investors and hurt the stock markets. Although a nationalist party scooped up the most seats, three pro-independence parties have won 70 seats out of 135, good enough for a slim majority. The vote is a stinging rebuke for Spanish Prime Minister Mariano Rajoy, who has imposed direct rule on the region and was hoping that the election would hurt the independence movement. Rajoy’s heavy-handed approach has clearly not extinguished the pro-independence movement, and Spain could be headed for more political turmoil in the coming months.

Republicans lawmakers presented Donald Trump with an early Christmas present, as both branches of Congress passed Trump’s landmark tax reform bill. One of Trump’s key campaign pledges was tax reform, and the new legislation marks the first overhaul of the tax code since the Reagan administration. There was more good news, as US Final GDP posted a strong gain of 3.2%, just shy of the Preliminary GDP reading of 3.3%. With the US economy posting growth above 3% for another quarter, the Federal Reserve remains on track for another rate hike in January. The CME Group has pegged the odds of a January hike at 98%, and if the economy continues its current pace, the Fed could raise rates up to four times in 2018. Inflation remains a sore point, as the Fed target of 2.0% remains well out of reach. Fed Chair Janet Yellen and other FOMC members have said they expect that the strong labor market will lead to higher inflation, but the Fed has demonstrated that it is willing to press ahead with rate hikes despite low inflation.

Euro Edges Lower As Markets Digest Catalonia Vote

The euro has ticked higher in the Friday session. Currently, EUR/USD is trading at 1.1853, down 0.17% since Thursday's close. On the release front, German GfK Consumer Climate inched up to 10.8, above the estimate of 10.7 points. French Consumer Spending soared 2.2%, well above the forecast of 1.4%. It's a busy day in the US, with a host of key events. Durable goods reports are expected to improve, but the markets are braced for softer readings from New Home Sales and UoM Consumer Sentiment.

Catalans flocked to the polls in a highly-anticipated election, but the results have shown that little has changed since the region declared independence in October. Although a nationalist party scooped up the most seats, the three pro-independence parties have won 70 seats out of 135, good enough for a slim majority. The vote is a stinging rebuke of Spanish Prime Minister Mariano Rajoy, who has imposed direct rule on the region and was hoping that the election would hurt the independence movement. Spain endured a deep political crisis when Catalonia declared independence, and it appears that more political uncertainty and instability lie ahead for the fourth largest economy in the eurozone.

It has been a great week for President Trump. Republicans lawmakers presented him with an early Christmas present, as both branches of Congress passed Trump's landmark tax reform bill. One of Trump's key campaign pledges was tax reform, and the new legislation marks the first overhaul of the tax code since the Reagan administration. There was more good news, as US Final GDP posted a strong gain of 3.2%, just shy of the Preliminary GDP reading of 3.3%. With the US economy posting growth above 3% for another quarter, the Federal Reserve remains on track for another rate hike in January. The CME Group has pegged the odds of a January hike at 98%, and if the economy continues its current pace, the Fed could raise rates up to four times in 2018. Inflation remains a sore point, as the Fed target of 2.0% remains well out of reach. Fed Chair Janet Yellen and other FOMC members have said they expect that the strong labor market will lead to higher inflation, but the Fed has demonstrated that it is willing to press ahead with rate hikes despite low inflation.

.

CRUDE OIL Ready To Test Strong Resistance Area

Crude oil is has failed to break resistance given at 59.05 (24/12/2017 high). Support is given at 55.82 (07/12/2017 low). As volatility declines, expected to show further bearish breakout.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. For the time being the pair lies in an upside momentum. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

SILVER Bullish Momentum

Silver has been bouncing on hourly support at 15.61 (14/07/2017 low). Hourly resistance given at 16.15 (13/12/2017 high) has been broken. Expected to show continued bullish pressures.

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).