Sample Category Title

Market Morning Briefing: Euro Bounced Yesterday After Testing Support Near 1.175

STOCKS

Dow (24754.75, -0.15%) came off a bit after almost testing 24800 levels yesterday. It could possibly remain stable for another session or two before heading towards 25000 in the coming sessions. Near to medium term looks bullish.

Dax (13215.79, -0.72%) lost all gains seen yesterday, coming back to levels near 13200. Immediate support is visible near 13150-13100 levels and while that holds, the index could probably attempt another rise targeting 13400 in the next few sessions.

Nikkei (22853.23, -0.06%) is stuck in the narrow 22600-23000 region with the upper level being an important near term resistance. Unless a break above 23000 is seen and sustained, the index could be trading sideways near current levels for some more time. Note that 23000 has not been able to produce a sharp rejection and could be an indication of bears losing out some strength just now.

Shanghai (3296.42, 0%) could be stuck in a sideways phase within 3320-3260 region and while that holds, there is lack of clarity on further direction the index could take. Near term likely to remain stable.

Nifty (10463.20, +0.72%) and Sensex (33836.74, +0.70%) have risen sharply yesterday. Nifty could test resistance near 10500-10550 levels today while Sensex could also head towards 34500. Thereafter a small dip or at least some sideways consolidation would be expected before deciding on further direction.

COMMODITIES

Gold (1263.81) has moved up a bit as Dollar seems to be turning a little weak. While the Dollar Index (93.43) is below 93.75, Gold is likely to sustain above 1260. As mentioned earlier, immediate upside could be limited to 1280 for Gold.

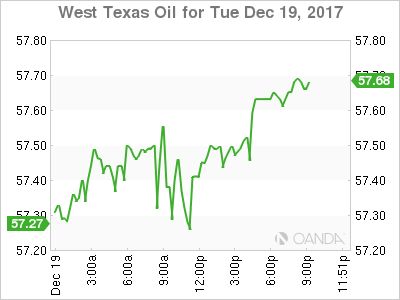

Brent (63.91) and WTI (57.75) are attempting to move up eventually. There is room on the upside for Brent towards 68 while WTI may face resistance near 59 itself. Either of the two is likely to impact the other. In case, Brent rises sharply towards 65 and higher, WTI could possibly attempt to break above 59; else a fall from 59 on WTI could slow down the rise in Brent. Need to watch the crude prices carefully.

Copper (3.1470) has come up to test 3.15 as expected and could target medium term resistance near 3.20. While 3.20 holds, another down-leg in Copper looks likely towards 3.00-2.95 levels.

FOREX

Dollar-Index (93.43) dipped yesterday after testing resistance near 94 on the 3 day candles and is currently trading below support near 93.5 on the daily candles. With the holiday week approaching, we might see minimal movement in the index, but it could still tend towards 93 which acts as support on 3 day candles; and in case of a break of the same, move towards support near 92.5 on the weekly line charts. A break below 92.5 could set off a downtrend for the index in January.

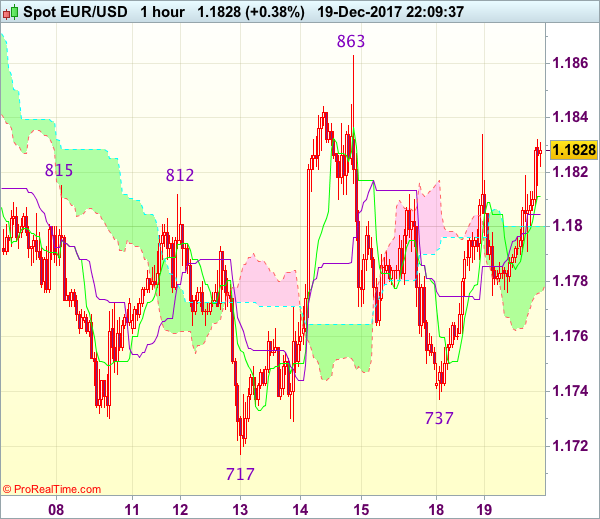

Euro (1.1843) bounced yesterday after testing support near 1.175 and is currently trading around 1.184-1.185. Along with the Dollar Index, Euro is likely to move in a narrow range (1.175-1.185) over the next few days. If Dollar Index tests support near 93 or the one near 92.5, we might see Euro move up and test resistance at 1.19. As mentioned yesterday, trend-deciders in the medium term continue to be 1.17 & 1.19.

Dollar-Yen (112.94) is maintaining strength inspite of the Dollar Index dipping, which might be due to US-Japan 10 yr yield spread breaking short term resistance and rising up to 2.4%. However, over the holiday period we might not see any significant movement in the Dollar Yen, with likelihood of it being ranged between 112 and 113.5. A break below 112 in the medium term is likely in case of Dollar Index breaking below 92.5.

Pound (1.3395) might again see range wise oscillation between 1.325-1.345 in the next few days and is currently moving up towards immediate resistance near 1.343-1.345.

Rupee (64.03) might go down towards 63.90 on the downside with Nifty looking bullish for a test of resistance near 10600 and the Euro rising up towards 1.19 gradually. There is less likelihood of a rise past 64.20 currently.

INTEREST RATES

Very sharp rise seen in the US yields yesterday. Some economists state that as the Congress moved closer to turn the tax bill into law, this would add to the deficit and signal more growth, leading to a rise in the interest rates. The 5YR (2.21%), 10Yr (2.45%) and the 30Yr (2.81%) are all up from previous levels of 2.18%, 2.40% and 2.74% respectively. If the rise sustains, the yields could rise towards 2.90% (30Yr), 2.52% (10Yr ) and 2.30% (5Yr).

Sharp break in the US-Japan 10Yr yield spread (2.40%) seen today as the US yields rose sharply. This break on the upside is very crucial and could pull up Dollar Yen and Nikkei to higher levels in the coming sessions. The yield spread is likely to rise towards 2.49% in the next few sessions.

The Indian 10Yr GOI (7.1780%) is headed towards resistance near 7.25% as mentioned yesterday and is likely to trade in the 7.25-7.155 region in the near term.

Tax Reform $ Bounce

Tax Reform Bounce

Foreign Exchange Traders were getting very edgy in Asia yesterday amid holiday-thinned markets with little impetus one way or the other, but thankfully there was some news to sink their teeth into overnight.

The dollar was firmer against most currencies in NY helped along by robust U.S. housing data, and a steeper US Treasury curve with 10-year yields rising to 2.47%.The move came after Fed's Robert Kaplan told Bloomberg TV that a flattening yield curve was limiting the Fed's “operating flexibility.” Having interest lower for longer certainly curbs the Feds ability to use the traditional monetary policy tools when or if the economy takes another downturn, and this has been a long-held view by dollar bulls.

But after all was said and done, doubts about the overall economic impact from the US tax bill capped the dollar gains as the dollar sold off versus the yen and held losses against the euro after the House approved the bill.

Currency traders continue to think the economic bump will be small while there's increasing chatter that the markets have likely overemphasised the impact of tax repatriation flows in the overall dollar narrative.

Equity Markets

Equity investors came up for air as stock markets were flat to indifferently lower through most of the session. No doubt a bit of year-end profit taking is setting in while typical dip buyers were absent likely wary of taking new positions ahead of the holiday break. But without question, the vibe around tax reform remains overwhelmingly positive for equity markets

Energy Markets

The American Petroleum Institute reported a 5.22 million barrel decline in US crude inventories at the end of the day. WTI was lifted to $57.75 from $57.58. The significant draw was a huge turn around for last weeks report, but more significantly it comes amidst reports of increased US Shale Production this week.

The Euro

EURUSD tested 1.1850 level spurred on by reports that Germany will flood the markets with Ultra Long Debt next year

But the EU hawks took flight overnight also with Bundesbank President Jens Weidmann, who told reporters that “a faster conclusion of net asset purchases and a communicated end date (to asset purchases) would have been reasonable”. And Governing Council member Jozef Makuch told his audience that “discussions are increasingly moving from asset purchases to the eventual future use of interest rates to regulate the economy”.

With Draghi continuing to lean dovish it's clear the ECB internal squabbles will come more to the fore in 2018 and should lend support to the hawkish ECB narrative and the EURO.

This shifting narrative explains the disconnect between the USDJPY and EURUSD moves overnight.

IN the background remains the debate if the ECB was as dovish as the market assumed. Eurozone money markets are steepening and given the outstanding economic prints coming out of the EU; it's easy to rationalise that the EU economy is leaps and bounds ahead of where the US economy was sitting when the Fed began to normalise.Structurally the Euro should move higher.

The Japanese Yen

USDJPY rallied from the open, rising from 112.55 to 113.06 before late afternoon profit-taking took prices back to 112.89. Rising US Treasury yields underpinned the currency pair. The price action played out as planned with dollar bears fading the tax bill uptick but perhaps less aggressively as scheduled after 10 Year UST's move closer to the fundamental 2.5 % level. But overall, the Fed's easy money policy and with little economic growth from tax reform expected the dollar Bears remain camped in the 113.25-50 region looking to fade any rallies

The market will now pivot to the BoJ meeting tomorrow. The USD will be the primary driver in USDJPY momentum, even with bearish dollar bets on the rise it's hard to rationalise a home run trade in the pair. Japans economy continues to struggle with inflation and despite all the noise around YCC of late, its unlikely the BoJ will change tack anytime soon meaning the weaker JPY storyline remains intact.

The Australian Dollar

Price action says it all. The RBA meeting passed without any fireworks. There was nothing to suggest a shift from neutral bias until at least mid-2018 despite their perceived marked improvement in the overall economy.

The market may be overplaying the diminishing differential narrative as broader USD dollar weakness alone is positive for the Aussie given the high beta. But the optimistic side of global growth narrative, resilient commodity prices and robust regional economies could provide the draft for the A dollar

The Malaysian Ringgit

The MYR was driven overnight by the broader USD momentum on the back of fast short-term money. Given that the dollar is trading with some positive energy from both Tax Reform and higher US Yields, investors will be reluctant buy the MYR until all the dust settles. But the Ringgit remains very comfortable at current ranges and the stability alone is a real positive in my view.

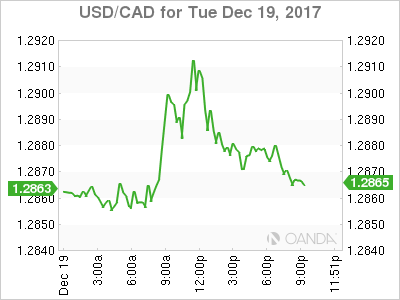

USD/CAD Canadian Dollar Lower Ahead Of US Senate Tax Overhaul Vote

The Canadian dollar depreciated on Wednesday as oil prices were volatile and the US dollar advanced spurned by the approval of the tax bill by the US House of representatives. The US Senate vote could happen later in the afternoon paving the way for US President Donald Trump to signs the bill and score his first major policy victory of the year. The US dollar started the year strong on the back of tax reform expectations and infrastructure spending promises. The Trump Administration decided to focus instead on immigration and health care which proved to be unpopular and were non-starters. The White House corrected the course and in the fall got back on track with its intention to overhaul the tax code. The road to tax reform has not been easy as it has proved unpopular in polls, but not with markets as it has given the greenback a boost before the end of the year.

Canadian economic indicators will be few and far between until next year. Inflation and retail sales on Thursday, December 21 and the monthly GDP release on Friday will close out the year. The Bank of Canada (BoC) stood pat in December keeping the benchmark rate at 1.00 percent. The central bank hiked twice in 2017 but is now sounding more dovish as the economy is slowing down in the second half of the year. BoC governor Poloz confused markets after a speech in Toronto was a hawkish take on the economy while later in the day the same topics got a dovish outlook. The rising risks of unknown factors such as the fate of NAFTA was present in both and could be a major blow to the economy in 2018 after the negotiations are almost at a standstill.

The USD/CAD gained 0.13 percent on Tuesday. The currency pair is trading at 1.2877 although at one point during the session the pair was trading above 1.29. The loonie has depreciated as the tax reform push is closer to the outcome Republicans wanted. The unified tax bill has passed the US House of Representatives and awaits the vote from the Senate later tonight before heading to the White House for President Trump’s signature. The vote will happen tonight and if successful to be presented on Wednesday Morning at the Oval office to be signed into law. As trading desks around the world look forward to the holidays the US tax overhaul is the last big event in the agenda.

Despite dovish comments from the Minnesota Fed Chief Neil Kashkari on how low inflation should be reason enough to pause monetary tightening in 2018, economic indicators were US dollar positive on Tuesday. Building permits rose to 1.30 million beating expectations, the current account showed a lower deficit at 101 billion (down form 124 billion last quarter) and housing starts also were above the forecast with 1.30 million beginning construction last month.

The price of oil rose in the last 24 hours. The price of West Texas Intermediate is trading at $57.50 as the outage in the North Sea pipeline continues. The issues at the Forties pipeline forced the operator to shut it down to perform repairs with no a two to four week window. Oil prices had been more stable after the Organization of the Petroleum Exporting Countries (OPEC) and other major producers announced an extension to their production cut deal now expected to end in December of 2018. US production is expected to ramp up to take advantage of the rise in prices.

US weekly inventories will be released on Wednesday, December 20 at 10:30 am EST. The string of drawdowns that started on November 22 is expected to continue with a forecasted 3.6 million barrels less of crude stocks. Gasoline stocks have had a bigger impact in the latest reports with surprise buildups that hint at a slowdown in demand. The OPEC led initiative has been offset with the promise of higher production in Brazil, Canada and the US with demand expected to remain stagnant oil prices could remain caught in a tight range unless there is a disruption in supply like the North Sea outage, geopolitical risk event or weather based.

Market events to watch this week:

Wednesday, December 20

10:30 am USD Crude Oil Inventories

4:45 pm NZD GDP q/q

Midnight JPY Monetary Policy Statement

Thursday, December 21

1:30 am JPY BOJ Press Conference

8:30 am CAD CPI m/m

8:30 am CAD Core Retail Sales m/m

8:30 am USD Final GDP q/q

8:30 am USD Unemployment Claims

Friday, December 22

4:30 am GBP Current Account

8:30 am CAD GDP m/m

8:30 am USD Core Durable Goods Orders m/m

Gold Ticks Lower As US Housing Numbers Impress

Gold has inched lower in the Tuesday session. In North American trade, the spot price for an ounce of gold is $1260.51, down 0.14% on the day. On the release front, Building Permits and Housing Starts both beat expectations. There was more good news as the US current account deficit in Q3 dropped to $101 billion, easily beating the estimate of $116 billion. This was the lowest monthly deficit since 2014. On Wednesday, the US releases Existing Home Sales.

Thanks to monumental efforts by Republican lawmakers in recent weeks, the US tax reform bill appears to have enough votes to pass through Congress and become law. The House and Senate reconciled their versions of the tax bill on Friday, and the uniform legislation is expected to be voted on in the House and the Senate later on Tuesday. With Democrats in both branches opposing the bill, the Republicans will need every vote in the Senate, where they have a razor thin 59-41 majority. Several Republican senators who were undecided have said they will vote in favor, so the bill is likely to pass through Congress and will then be signed into law by President Trump. This marks the first major overhaul of the US tax code in 30 years, and would represent a huge victory for Trump, ahead of Congressional elections in 2018.

Despite a persistent lack of inflation, a second rate hike in two months appears likely in January. The US economy has been firing on all cylinders, but analysts remain stumped as to why strong growth and a red-hot labor market have not led to higher inflation. The labor market continues to operate at full capacity and various sectors in the economy are reporting a lack of workers. Still, this has not translated into stronger wage growth, despite predictions from Janet Yellen and other Fed policymakers that a lack of workers is bound to push up wages. The Fed appears ready to continue to jack up rates, despite the lack of inflation. The markets are preparing for another quarter-point increase next month, with the odds of a rate hike standing at 98%, according to the CME Group.

Pound Ticks Lower, US Construction Reports Beats Expectations

The British pound is showing limited movement in the Tuesday session. In North American trade, GBP/USD is trading at 1.3367, down 0.12% on the day. There are no British indicators on the schedule. In the US, Building Permits and Housing Starts both beat expectations. There was more good news as the US current account deficit in Q3 dropped to $101 billion, easily beating the estimate of $116 billion. This marked the lowest deficit since 2014. On Wednesday, BoE Governor Mark Carney testifies before the Treasury Select Committee in London, and the US releases Existing Home Sales.

Mark Carney will be discussing the November Financial Stability Report before a parliamentary committee on Thursday, but lawmakers are likely to press him on inflation, which is currently at 3.1%, its highest level since March 2012. Carney is obligated to write an open letter to the British finance minister, explaining how the BoE plans to lower inflation closer to the Bank's target of 2.0%. The BoE has not made much headway in taming inflation, and his testimony and open letter may not provide any satisfactory answers. If inflation continues to run above 3%, Carney will be under strong pressure to raise rates, even though the economy could be facing difficulties ahead, especially with Britain departing the European Union in March 2019.

After frantic efforts by Republican lawmakers in recent weeks, the US tax reform bill appears to have enough votes to become law. The House and Senate reconciled their versions of the tax bill on Friday, and the uniform legislation is expected to be voted on in the House and the Senate later on Tuesday. With Democrats in both branches opposing the bill, the Republicans will need every vote in the Senate, where they have a razor thin 59-41 majority. Several Republican senators who were undecided have said they will vote in favor, so the bill is likely to pass through Congress and will then be signed into law by President Trump. This marks the first major overhaul of the US tax code in 30 years, and would represent a huge victory for Trump, ahead of Congressional elections in 2018.

Yen Edges Higher, BoJ Policy Meeting Looms

The Japanese yen has recorded slight gains in the Tuesday session. In North American trade, USD/JPY is trading at 112.77, up 0.20% on the day. In the US, construction numbers were sharp, as Building Permits and Housing Starts both beat expectations. There was more good news as the US current account deficit in Q3 dropped to $101 billion, easily beating the estimate of $116 billion. This marked the lowest deficit since 2014. Later in the day, Japan releases All Industries Activity, with an estimate of 0.4%.

The Federal Reserve and the ECB set interest rates last week, and it's the turn of the Bank of Japan, which holds a policy meeting on Wednesday and Thursday. The BoJ is expected to hold the course and maintain interest rate levels and its stimulus package. Japan's economy has rebounded in 2017, as a stronger global economy has boosted the country's export and manufacturing sectors. Still, ultra-low interest rates have resulted in a weak yen, much to the angst of Japan's trading partners, which has accused Tokyo of manipulating the exchange rate in order to boost exports. Although BoJ Governor Haruhiko Kuroda has dropped some hints about reducing stimulus, absent a surge in inflation, such a move is unlikely in the near future.

President Trump's proposal to replace Obamacare was a disaster, but things are looking much brighter for his tax reform initiative. Barring any unexpected surprises, tax reform will become law this week. On Friday, the legislation passed a major milestone, as the House and Senate hammered out the differences in their tax proposals and drafted a uniform bill. The legislation is expected to be voted on in the House later on Tuesday and the Senate on Wednesday. With Democrats in both branches opposing tax reform, the Republicans will need every vote in the Senate, where they have a thin 59-41 majority. Several Republican senators who were undecided have said they will vote in favor, so the bill is likely to pass through Congress and will then be signed into law by President Trump. This marks the first major overhaul of the US tax code in 30 years, and would represent a huge victory for Trump, ahead of Congressional elections in 2018.

Will the Greenback Stage a Comeback in 2018?

The US dollar plummeted in 2017, but that may not necessarily continue in 2018. The Fed seems set to undergo a hawkish shift in voting rights, while the Republicans are on the verge of implementing the highly-anticipated tax package. Although these factors could provide some support for the greenback overall, the currency's fortunes may also depend to a large degree on the performance of its major counterparts, such as the euro and the yen.

It is not hyperbole to say that 2017 has been a harsh year for the US dollar. Even though the greenback started the year at very high levels – buoyed by expectations that massive fiscal stimulus would stoke inflation – it quickly gave back its gains to finish the year notably lower against a basket of currencies. Will 2018 be any different?

Broadly speaking, the dollar's direction will likely hinge on two deciding factors: the pace at which the Fed continues to normalize policy, and on whether the Republican tax overhaul will finally be enacted. Kicking off with the Fed, the composition of voting rights within the FOMC will change drastically in 2018. The Committee appears set to become slightly more hawkish, as ultra-doves like Kashkari and Evans are set to lose their voting rights, while notorious hawks such as Mester are due to become voters. The "wild card" here is who Trump will nominate as Fed Board Governors. There are currently three vacant Governor seats, which will increase to four once Yellen leaves in February. His choices could be a major driver for the USD next year, as Board Governors are permanent FOMC voting members.

With regards to rate hikes, the December "dot plot" suggests the Committee is set to deliver 3 quarter-point increases in 2018, while the market has priced in slightly less than 2, according to the Fed fund futures. Thus, the point of interest for the dollar is whether the market will gradually move closer to the Fed's forecasts and price in another hike, or whether the Fed will revise down its own rate path and come closer to market pricing. Although a lot will depend on incoming economic data, the hawkish shift in FOMC voting rights supports the case for investors to gradually price in an additional hike.

Turning to tax cuts, the "heavy lifting" seems to be over, after both the House and the Senate passed their own versions of the tax bill. Having worked out the differences between their two plans in recent days, all that remains now is for the two chambers of Congress to vote on the final version. The critical question for the USD is to what extent such a bill would push US yields higher, and how much of that is priced in already. The fact that the Republicans can only afford to lose 2 votes in the Senate suggests that this is not a done-deal yet, especially so because some Republican Senators still appear to be undecided (Susan Collins, Jeff Flake, Mike Lee). Therefore, most of the "good news" may be factored in already, but one still can't rule out a surge in the USD should Congress vote the tax bill into law, as uncertainty over the US fiscal outlook fades. On the other hand, in the unlikely event that Congress rejects the bill, that would likely come as a major surprise given the heightened expectations for a tax overhaul, and could thereby lead to a significant drop in the dollar.

Overall, the greenback could recover somewhat in 2018, though it might not be ready for a major healthy uptrend. Instead, the currency's performance may depend to a significant degree on the performance of its counterparts as well. For instance, euro/dollar may head a little lower in early 2018 on the back of the tax package in the US and resurfacing political risks in Europe. However, the cross could in the end finish 2018 higher, as any USD strength due to Fed hikes is likely to be overshadowed by euro gains – should the ECB proceed with an end to QE in late 2018 and a signal for higher rates in 2019. A much better proxy for potential USD gains in 2018 may be dollar/yen. The BoJ is expected to continue to keep the yields on longer-dated JGBs fixed near 0%, while the Fed could even deliver more rate hikes in 2018 than the market currently anticipates. The widening spread between US and Japanese yields would argue in favor of a higher dollar/yen over time, conditional upon the BoJ keeping its policy framework untouched.

Euro Outlook 2018: Short-Term Pain, Long-Term Gain?

Whether or not the euro will continue its bull run into 2018 is likely to depend on a variety of political and economic factors. How will the upcoming election in Italy play out, and will markets begin to price in concerns regarding the stability of the euro area ahead of the event? Moreover, will the ECB be optimistic enough to signal an end to its QE program, thereby increasing the appeal of the common currency? A reasonable scenario for the euro's path is one where it corrects lower on political woes early in the year, only to recover its losses and perhaps trade higher by year-end, supported by Eurozone's strengthening recovery and the ECB decreasing its stimulus dose even further.

The euro enjoyed a remarkable year in 2017, defying all skeptics to stage a spectacular bull-run that drew support from both politics and economics. The outcome of the French presidential election provided the initial spark for the rally as political risks diminished, while the bloc's economic upturn and the subsequent optimistic rhetoric from the European Central Bank (ECB) sparked speculation for an eventual end to the QE-era. Whether or not 2018 will prove equally beneficial for the common currency is likely to depend, once again, on politics initially and on economics thereafter.

Kicking off with politics, even though the victory of Macron in the French election calmed the nerves of investors regarding more countries leaving the EU, political uncertainty could well stage a comeback in the first half of 2018, ahead of the looming general election in Italy. According to the latest opinion polls, the incumbent Democratic Party is neck and neck with the Five Star Movement, a Eurosceptic party that has previously advocated for holding a referendum on the euro. As such, heading into the election, we could see a risk premium being factored into the euro, as investors price in the possibility of a euro-exit in case of a government that includes (or is led by) the Five Star Movement.

The outcome of the election could determine the euro's short-term prospects, with a Five Star victory likely to keep the currency under downward pressure. On the flipside, a victory by other major parties could signal a continuation of the status-quo in the Eurozone and thereby, trigger a relief rally in the euro. Such an outcome would also keep the door open for much-needed structural reforms in the EU, such as the completion of the Banking Union, the creation of a shared budget among member countries, and the introduction of some form of public risk sharing. This may be another major theme for the euro in 2018, with any signs that such reforms will be implemented likely to increase the currency's appeal to investors, since they could be viewed as better preparing the region to handle future crises.

Turning to monetary policy, the ECB will probably take center stage in the second half of 2018, as it will be called to decide on the future of its asset purchase program. Market focus may fall on whether the Bank will opt to extend QE again, or whether it will set a roadmap towards ending the program completely. It is important to note that after the latest QE extension, key policymakers like Jens Weidmann and Benoit Coeure hinted at a clear exit from the program next year, which may be a preliminary sign of how the "heavyweights" in the ECB will vote. That said, the actual decision may depend primarily on the evolution of the bloc's economic data and particularly, on any potential pick-up in wage growth, inflation, and economic activity.

All things considered, the euro could drift lower early next year, as market attention shifts back to politics and the possible scenario of a euro-referendum by Italy. A correction lower may be particularly visible in euro/dollar, if the expected tax package in the US was to tilt the bias in favor of the dollar in early 2018. Overall though, the currency's broader direction will probably be decided by ECB policy. One could argue the ECB is more likely than not to signal an end to its QE program in 2018, amid an improving growth outlook for the Eurozone, financial stability concerns, and technical limitations on the eligible bonds it can buy. In such case, the common currency could well recover any potential losses it posts on political worries and perhaps manage to end the year higher, with euro/dollar potentially aiming for a test of the 1.2570 territory, marked by the highs of December 2014.

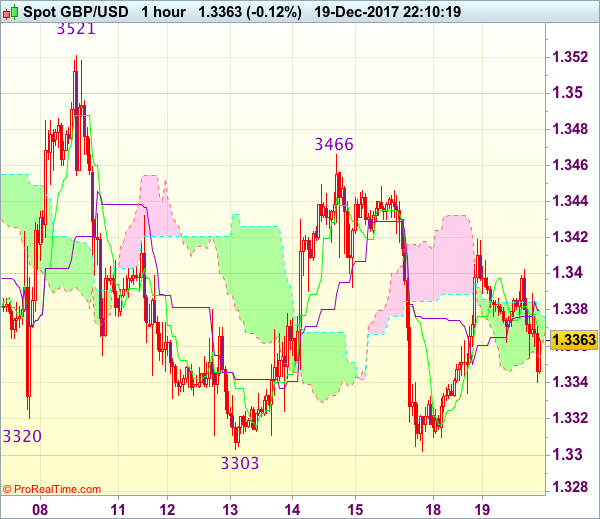

Trade Idea Wrap-up: GBP/USD – Hold short entered at 1.3390

GBP/USD - 1.3354

Most recent candlesticks pattern : N/A

Trend : Sideways

Tenkan-Sen level : 1.3371

Kijun-Sen level : 1.3380

Ichimoku cloud top : 1.3379

Ichimoku cloud bottom : 1.3352

Original strategy :

Sold at 1.3390, Target: 1.3290, Stop: 1.3420

Position : - Short at 1.3390

Target : - 1.3290

Stop : - 1.3420

New strategy :

Hold short entered at 1.3390, Target: 1.3290, Stop: 1.3405

Position : - Short at 1.3390

Target : - 1.3290

Stop : - 1.3405

Although the British pound found good support at 1.3302 and staged a strong rebound yesterday, reckon upside would be limited and mild downside bias remains for another decline, below 1.3330-35 is needed to signal the rebound from 1.3302 has ended, bring retest of this level, break there would extend recent decline from 1.3550 top to 1.3280, then towards 1.3250, however, still reckon previous support at 1.3221 would remain intact.

In view of this, we are holding on to our short position entered at 1.3390. Above 1.3420-25 would defer and risk rebound to 1.3445-50 but said resistance at 1.3466 should remain intact and bring another decline later.

Trade Idea Wrap-up: EUR/USD – Stand aside

EUR/USD - 1.1816

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.1811

Kijun-Sen level : 1.1805

Ichimoku cloud top : 1.1800

Ichimoku cloud bottom : 1.1776

New strategy :

Stand aside

Position : -

Target : -

Stop : -

As the single currency found support at 1.1775 yesterday and has rebounded again, suggesting another test of indicated resistance at 1.1834 cannot be ruled out, above there would extend the rebound from 1.1737 to 1.1850-55, however, as broad outlook remains consolidative, reckon last week’s high at 1.1863 would hold from here, bring further choppy trading later. Only a break above this level would signal the rebound from 1.1717 is still in progress for further subsequent gain to 1.1880, then 1.1900 but price should falter well below resistance at 1.1940

On the downside, expect pullback to be limited to 1.1775-80 and bring another rebound. Below indicated support at 1.1737 would bring retest of last week’s low at 1.1717 but break there is needed to confirm recent decline from 1.1961 top has resumed for weakness to 1.1695-00, then 1.1670-75. As near term outlook is mixed, would be prudent to stand aside for now.