Sample Category Title

Gold To Silver Ratio Showing Next Move for Silver

Hello fellow traders, in this article I want to discuss with you the Gold to Silver Ratio.

Before we get into that let me explain it shortly. Well, the gold to silver says how many silver ounces it takes to buy one ounce of gold. Which basically tells us how many ounces of silver we need to purchase for one ounce of gold.

Currently, the Gold to Silver ratio is approx. at 78. Which tells us that we need 78 ounces of silver to purchase 1 ounce of gold.

But why do we need this information now, you may ask? The easiest answer for that is it could signal us potential big moves in silver or gold. When the gold to silver ratio rallies, mostly gold and silver will fall. Obviously, we need to understand that the gold to silver ratio is highly volatile and fluctuates widely which means it is not a tick by tick correlation. You can't just buy or sell accordingly to the ratio. But what you can do is you can potentially forecast weekly moves.

Let's have a look at the technical view. In the image below you can see clearly that the gold to silver ratio chart ended cycle from 03/2016 peak in blue wave (W) and blue (X) connector consequently at 07/10/17 peak (data spike is not that deep). From that high, the market ended cycle from 07/06/17 in black wave ((w)). From that low, it is already extreme. It can be the case that the black ((x)) connector is already in place at the recent high (but I also wouldn't discount another marginal new high, doesn't really matter at this stage). Which means that market should correct in 3 waves at least from that blue box lower.

Gold to Silver Ratio Daily Chart

When that happens, Silver will also pullback in at least 3 waves to the upside. (As they are negatively correlated) Have a look at the Silver chart below.

Silver Daily Chart

Whether silver can really start its next big to the upside (shown in blue line) remains to be seen, it is not confirmed yet and can still make another margin new low. However, silver should be supported overall. I wish you all the best and don't forget our special offer below.

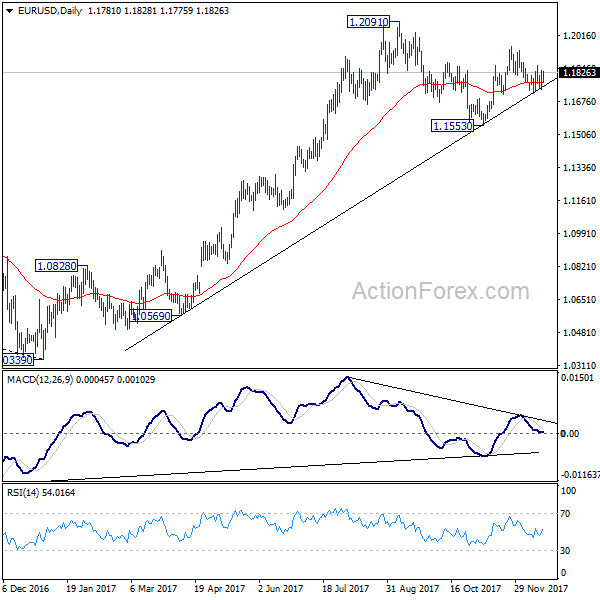

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1733; (P) 1.1784 (R1) 1.1831; More....

Intraday bias in EUR/USD remains neutral for the moment. On the downside, decisive break of 1.1712 cluster support (61.8% retracement of 1.1553 to 1.1960 at 1.1708) should confirm completion of rebound from 1.1553 at 1.1960. This would also be supported by a head and shoulder pattern (ls: 1.1860; h: 1.1960; rs: 1.1862). And in that case, deeper fall should be seen through 1.1553 to extend the medium term decline from 1.2091. Meanwhile, above 1.1862 will revive near term bullishness and target 1.1960 and above.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1435) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

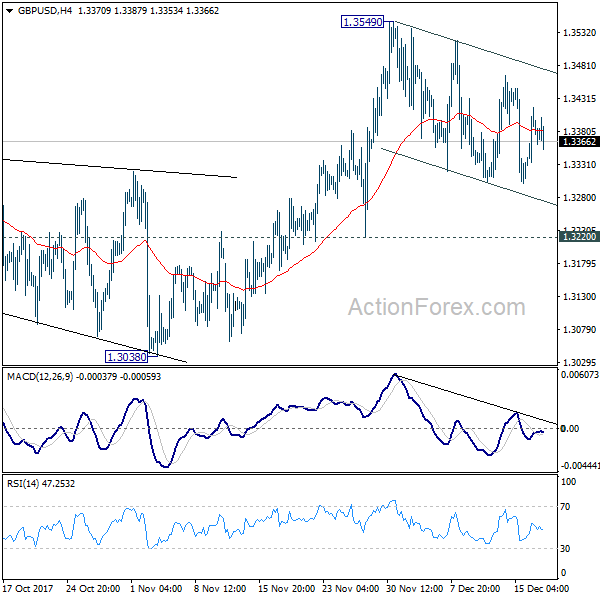

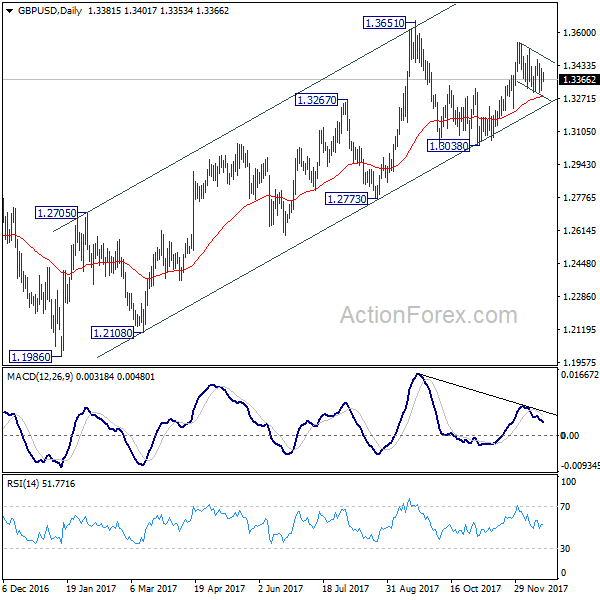

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3263; (P) 1.3354; (R1) 1.3410; More.....

GBP/USD is staying in the correction from 1.3549 and intraday bias stays neutral for the moment. As long as 1.3220 support holds, we'd favor another rise. Break of 1.3549 will target 1.3651 high next. Break there will resume medium term rally from 1.1946. However, firm break of 1.3220 will turn near term outlook bearish for 1.3038 key support level.

In the bigger picture, while the medium term rebound from 1.1946 low was strong, it's limited below 1.3835 key support turned resistance. As long as 1.3835 holds, we'd view such rebound as a correction. That is, we'd expect another leg in the long term down trend through 1.1946 low. However, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

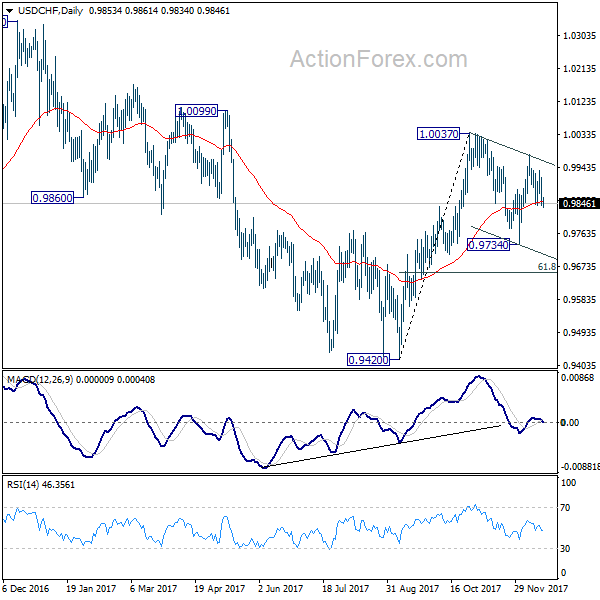

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9825; (P) 0.9870; (R1) 0.9902; More....

Break of 0.9839 indicates fall from 0.9977 is resuming. Intraday bias in USD/CHF is back on the downside for 0.9734 and possibly below. But we'd expect strong support from 61.8% retracement of 0.9420 to 0.1.0037 at 0.9656 to complete the correction from 1.0037 and bring rebound. On the upside, break of 0.9977 will resume the rebound from 0.9734 for 1.0037 resistance.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

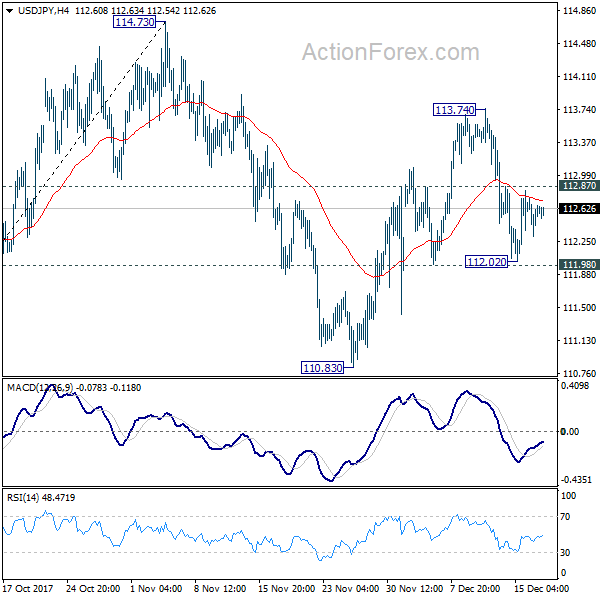

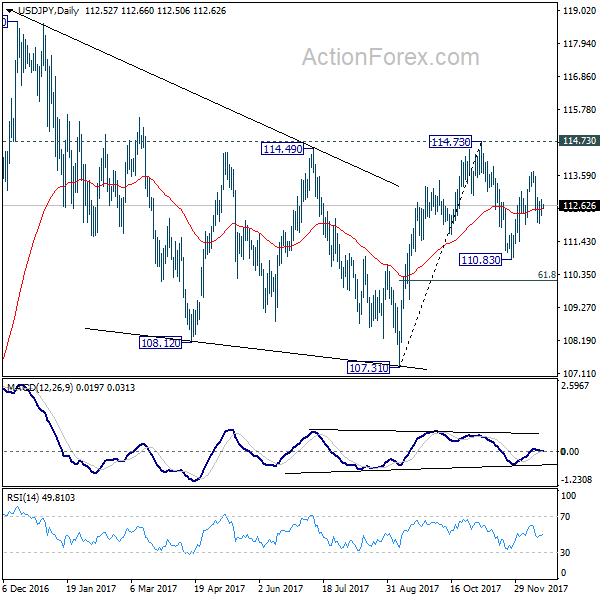

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.16; (P) 112.45; (R1) 112.87; More....

Intraday bias in USD/JPY remains neutral as it's still bounded in range of 111.98/112.87. With 111.98 intact, we'd favor another rise in the pair. Above 112.87 minor resistance will turn bias to the upside for 113.74. Break will target 114.73 key resistance. However, firm break of 111.98 support will extend the decline from 114.73 with another fall, possibly to 61.8% retracement of 107.31 to 114.73 at 110.14 before completion.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

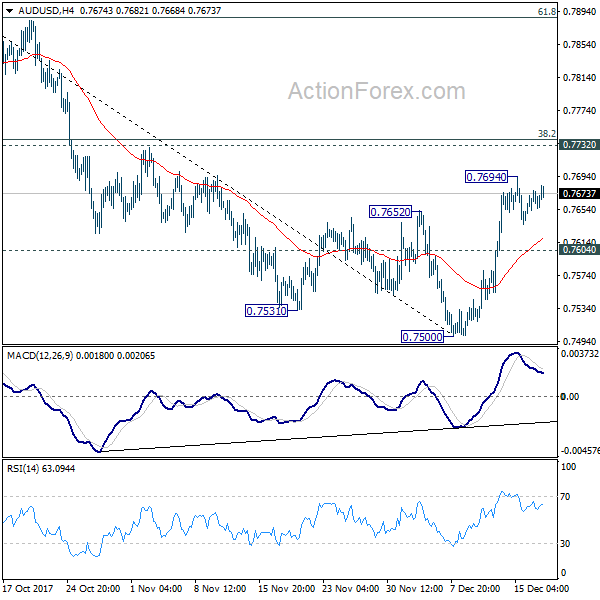

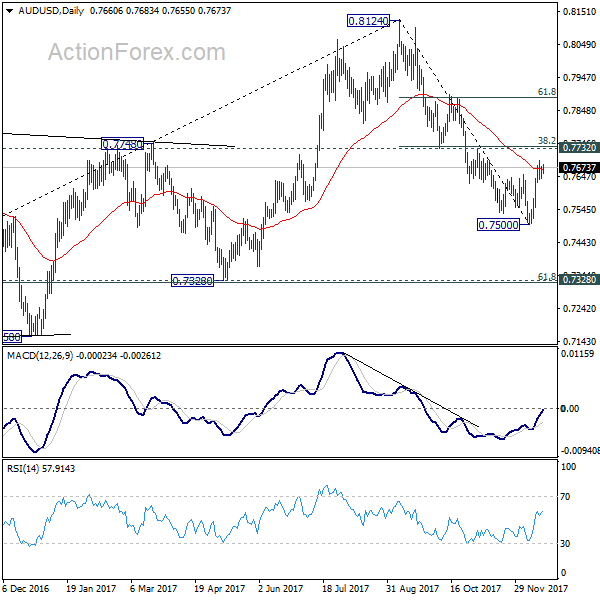

AUD/USD Mid-Day Outlook

Daily Pivots: (S1) 0.7619; (P) 0.7657; (R1) 0.7676; More...

Intraday bias in AUD/USD remains neutral at this point. Price actions from 0.7500 are viewed as a corrective pattern. Upside should be limited by 0.7732 cluster resistance (38.2% retracement of 0.8124 to 0.7500 at 0.7738). On the downside, below 0.7604 minor support will bring rest of 0.7500. Break will resume whole fall from 0.8124. However, sustained break of 0.7732 should invalidate our bearish view and bring stronger rise through 61.8% retracement at 0.7886.

In the bigger picture, corrective rise from 0.6826 medium term bottom is likely completed at 0.8124, after hitting 55 month EMA (now at 0.8034). Decisive break of 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) will confirm. And in that case, long term down trend from 1.1079 (2011 high) will likely be resuming. Break of 0.6826 will target 61.8% projection of 1.1079 to 0.6826 from 0.8124 at 0.5496. This will now be the favored case as long as 0.7732 near term resistance holds.

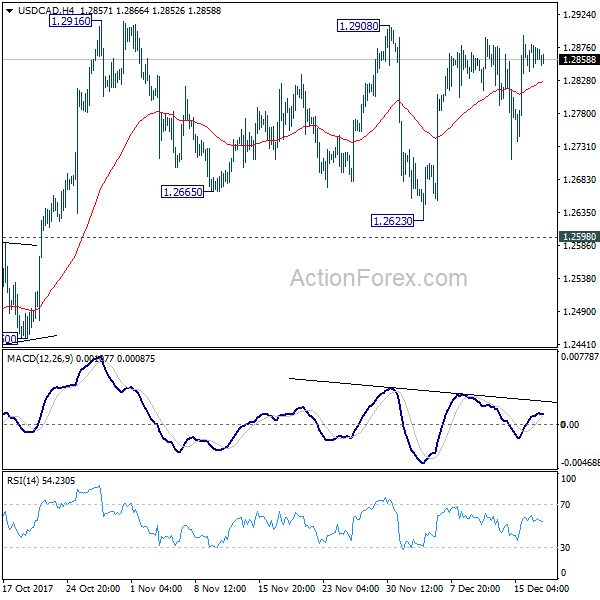

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2843; (P) 1.2862; (R1) 1.2882; More....

USD/CAD continues to stay in range of 1.2623/2916 and intraday bias remains neutral. Consolidation from 1.2916 might still extend. But, as long as 1.2598 resistance turned support holds, near term outlook remains bullish. On the upside, break of 1.2916 will resume the rise from 1.2061 and target 1.3065 medium term fibonacci level next. However, sustained break of 1.2598 will argue that rebound from 1.2061 has completed after hitting 55 week EMA (now at 1.2885). Near term outlook will be turned bearish in this case.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

CAC Steady, Investors Await US Tax Reform Votes

The CAC index has posted small losses in the Tuesday session. Currently, the index is at 5413.50, down 0.13% on the day. There are no French or eurozone events on the schedule. On Wednesday, the eurozone releases Current Balance, with the surplus expected to drop to EUR 33.4 billion.

It could be a banner week for global stock markets, as investors anxiously await the outcome of President Trump's tax reform initiative. After frantic efforts by Republican lawmakers in recent weeks, the tax reform bill appears to have enough votes to become law. The House and Senate reconciled their versions of the tax bill on Friday, and the uniform legislation is expected to be voted on in the House on Tuesday and the Senate on Wednesday. With Democrats in both branches opposing the bill, the Republicans will need every vote in the Senate, where they have a razor thin 59-41 majority. Several Republican senators who were undecided have said they will vote in favor, so the bill is likely to pass through Congress and will then be signed into law by President Trump. This marks the first major overhaul of the US tax code in 30 years, and would represent a huge victory for Trump, ahead of Congressional elections in 2018.

There are few French indicators ahead of the Christmas holiday, but investors should keep a close eye on French consumer spending, which will be released on Friday. Consumer spending was dismal in October, with a sharp decline of 1.9%, compared to the forecast of 0.0%. However, the markets are expecting a strong rebound for November, with an estimate of a 1.4% gain. Christmas shopping will likely translate into strong consumer spending numbers for December, which could boost fourth quarter economic growth and send the CAC to higher levels.

US-China Relations on a Concerning Path

- Following a much-celebrated visit to China by US President Donald Trump in early November, the US-China relationship has gone steeply downhill.

- Several US trade actions and yesterday a very confrontational tone towards China in the US National Security Strategy have rapidly worsened the relationship.

- The risk of a tit-for-tat trade conflict over the coming year has unfortunately increased again. Keep an eye on potential US action in areas such as intellectual property rights, aluminium and steel. This could trigger retaliation by China.

Optimism high following Trump's visit to China…

Our optimism that China and the US would solve their differences through constructive co-operation was fairly high following President Trump's visit to China.

First, during the visit Trump and China's President Xi Jinping signed deals worth around USD250bn. Second, Trump had barely left China before China announced that it would allow foreign financial institutions to own 51% of Chinese security firms, fund managers and futures companies – the first time foreign institutions could hold a majority stake (see New York Times, 10 November). Two weeks later, China stated it was cutting tariffs on a wide range of consumer goods, reducing average import tax from 17.3% to 7.7% on products such as food, medicine, medicine, clothing and other goods (see Xinhua, 24 November).

Similarly, while being criticised for some time of dumping steel on world markets due to overcapacity, China has acknowledged the problem of overcapacity and taken steps to cut capacity with a target of a reduction of 10% over five years from 2015 (see China Daily, 14 November). A move that was alluded to in the IMF's People's Republic of China: Staff Report for the 2017 Article IV Consultation, 8 August, in which directors 'welcomed the authorities' efforts to reduce overcapacity'.

After Trump's visit, China praised the relationship with the US. In a China Daily editorial on 9 November, with the headline 'Sino-US relations stand at historic new starting point', the editor wrote 'although the differences that had been pestering bilateral ties have not instantly disappeared, the most important takeaway from their talks in Beijing has been the constructive approach to these issues the two leaders demonstrated'. China Daily is one of the Communist Party's papers and editorials are seen as closely aligned with the views of the Communist Party.

…but relations have gone downhill since then

However, it did not take long for it to become evident that our expectations of a constructive relationship solving differences in bilateral negotiations were probably too high.

- On 28 November, the Trump administration began a probe into Chinese aluminium imports, which could lead to tariffs. The Commerce Department took the unusual step of initiating the case itself, rather than going through the regular route of starting an investigation based on requests by US companies.

- China objected to the investigation and warned of retaliation. For example, an editorial in China Daily on 30 November said that the move 'goes against fair trade' and specifically mentioned that the move comes 'less than a month after US President Donald Trump wound up his maiden trip to Beijing with the signing of business deals worth USD250bn'. It added that 'it seems Washington wants Beijing to make all the concessions and it is unwilling to try and meet it halfway. Instead the US has gone in the opposite direction…This only hurts mutual trust and may trigger retaliation'.

- On 12 December, the US, European Union and Japan announced a partnership to tackle overcapacity issues and forced technology transfers – a move clearly targeted at China, although the statement does not specifically mention China (see Bloomberg, 9 November). The US is also cracking down on steel coming from China via third countries. In December, the US Commerce Department imposed duties on steel products from Vietnam that originated in China.

- On the issue of sanctions on North Korea, China complained in late November about what it calls 'US long-arm jurisdiction'. Sanctions on specific Chinese companies is causing frustration. China Daily (23 November) reports China as saying it aims to strictly implement UN Security Council resolutions and that the 'US should share any intelligence it might have of Chinese individuals or companies violating them so that China can investigate for itself any contravention of its international obligations'.

The above comes on top of the investigation launched by US Trade Representative Robert Lighthizer on alleged theft by China of US intellectual property and forced technology transfer (launched in August).

To top it up, Donald Trump yesterday used very harsh words on China when presenting the National Security Strategy. Among other things, Trump stated that China (and Russia) is attempting to erode American security and prosperity and that it is developing weapons that could threaten US critical infrastructure (see Appendix for more statements).

China hit back at Trump in a, for China, very blunt statement by the Chinese Embassy in Washington on 19 December. It stated that 'Preaching rivalry and confrontation goes against the global trend and will lead to failure', adding that 'For the US, it also needs to get used to and get along with a developing China. We call on the United States to abandon its outdated zero-sum thinking and work together with China to seek common ground and engage in win-win co-operation'.

In our view, there is a clear risk that China feels a bit betrayed by Trump following the concessions given under and after Trump's visit, which China saw as part of meeting Trump's demands, believing that differences would be solved through negotiations rather than unilateral action. If Trump acts unilaterally, we believe the risk is high that China will retaliate.

Concerning rise in tensions – US mid-term elections won't help

The relationship between China and the US has quickly moved to a low point, taking a sharp turn from improved sentiment and apparent co-operation between the two nations in 2017. We have some concerns that Trump will take action over the next year that could trigger a tit-for-tat trade tension and worsen the co-operation on the important North Korean issue.

Adding to fears is that Trump seems to have wide backing at home for his confrontational course with China (see South China Morning Post article, 15 December) and that he may use the trade weapon in the run-up to next year's mid-term election to gain Republican support. In addition, should Trump lose the Republican majority in both the Senate and the House, it would leave him with power only in the areas of foreign policy and trade.

Appendix: National Security Strategy statements on China

'China and Russia challenge American power, influence and interests, attempting to erode American security and prosperity. They are determined to make economies less free and less fair, to grow their militaries and to control information and data to repress their societies and expand their influence.'

'China and Russia are developing advanced weapons and capabilities that could threaten our critical infrastructure and our command and control architecture.'

'Every year, competitors such as China steal US intellectual property valued at hundreds of billions of dollars.'

'China is using economic inducements and penalties, influence operations and implied military threats to persuade other states to heed its political and security agenda…Its efforts to build and militarise outposts in the South China Sea endanger the free flow of trade, threaten the sovereignty of other nations and undermine regional stability.'

Housing Heats Up

The early boom and bust of the US housing market left it on the sidelines of the global home-price ramp but that may soon change. All currencies are up against the US dollar with the exception of GBP and JPY. NZD and EUR are the top perfomers since the start of Tuesday Asia trade. In the Premium Insights, the short FTSE trade was stopped out as the index joined the rest of indices higher. There are 8 trades in progress.

The effect of year-end flows was evident on Monday with the euro climbing 40 pips into the London fix only to give it all back in the hours afterwards. Expect to see more whippy trading until New Year's Day. Ashraf has a piece on cross currency swaps and how these happen to temporarily support USD.

On the US data front, the NAHB home builders sentiment survey ramped up to 74 from 70, breaking above the 2005 high to reach its best level since 1999. That's curiously high given that housing construction is half of what it was in the halcyon daysm, but an indication that the bubble could begin to reflate.

The commentary about the economy, stocks and housing is all begin to change. That's probably a sign that we're getting into the latter stages of the expansion but it will also mean that consumers are more likely to spend and that should keep housing as a tailwind for at least a year or two.

Trump, meanwhile, touched on what could be another theme of 2018: Trade. He will assuredly finish out 2017 by signing a tax bill, before moving to other priorities. He singled out China as a strategic competitor in a national security speech Monday. We're also nearing make-or-break time on NAFTA.

For the day ahead, the IFO report, US housing starts and Eurozone labour costs are on the agenda but first the minutes of the December RBA meeting are due at 0030 GMT. The market isn't expecting much in terms of a signal so we will be looking for clearer signs of a bias or for signals about what metrics Lowe is measuring.