Sample Category Title

Technical Outlook: WTI OIL Maintains Bullish Tone But Without Stronger Upside Action So Far

Oil price ticked higher on Tuesday after previous day's action showed strong indecision, ending in long-legged Doji candle.

Fresh bulls attempt through 20SMA ($57.52) which capped past two day's action, break of which would open next pivot at $57.79 (Fibo 61.8% of $59.02/$55.81 downleg) and spark stronger rally on break.

Bullishly aligned daily techs are supportive with oil price being boosted by North Sea pipeline outage and expectations for another draw in US oil inventories (API report is due late today and EIA will release its weekly report on Wednesday).

Solid supports lay at $57.13 ( broken 10SMA) and $57.04 (broken Fibo 38.2% of $59.02/$55.81) and only sustained break here would weaken near-term structure.

Res: 57.56, 58.26, 58.54, 58.86

Sup: 57.13, 57.04, 56.57, 56.08

DAX Pauses After Strong Gains

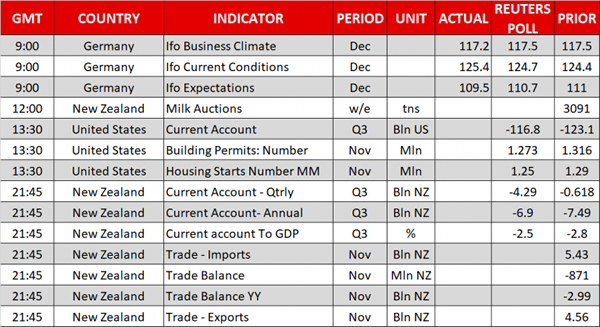

The DAX started the week with considerable gains, but has steadied in the Tuesday session. Currently, the index is at 13,298.50, down 0.08% on the day. On the release front, German Ifo Business Climate dipped to 117.2, short of the forecast of 117.6 points. On Wednesday, Germany releases PPI and the eurozone publishes Current Account.

German coalition talks have taken a shift, as President Angela Merkel's conservative bloc has entered into exploratory talks with its previous junior coalition party, the Social Democrats (SDP). The conservatives had a poor showing in the September election, and talks with smaller parties proved fruitless. The formation of new government promises to be a drawn-out process, with the sides not expected to discuss substantive issues until early 2018. Many SDP lawmakers want a more senior role for the SDP in any coalition, and the SDP will likely demand key portfolios in a new government. Despite the political uncertainty, the German economy continues to look very strong, as major indicators remain at high levels.

President Trump fared badly when he tried to replace Obamacare, but his tax reform proposal is poised to become law, barring any unexpected surprises. On Friday, the legislation passed a major milestone, as the House and Senate hammered out the differences in their tax proposals and drafted a uniform bill. The legislation is expected to be voted on in the House on Tuesday and the Senate on Wednesday. With Democrats in both branches opposing tax reform, the Republicans will need every vote in the Senate, where they have a thin 59-41 majority. Several Republican senators who were undecided have said they will vote in favor, so the bill is likely to pass through Congress and will then be signed into law by President Trump. This marks the first major overhaul of the US tax code in 30 years, and would represent a huge victory for Trump, ahead of Congressional elections in 2018.

US Tax Bill On Final Stage, European Stocks Hold Strong

Here are the latest developments in global markets:

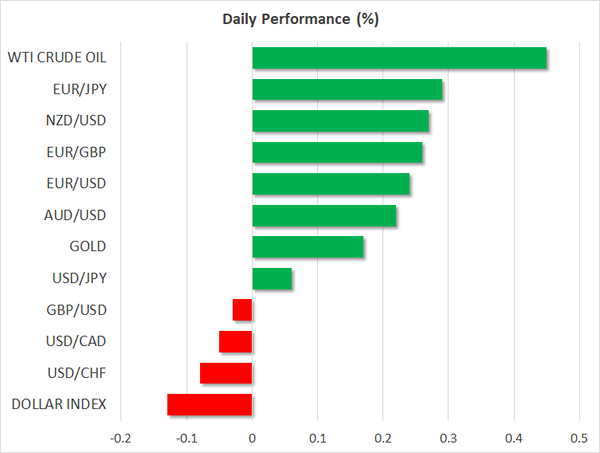

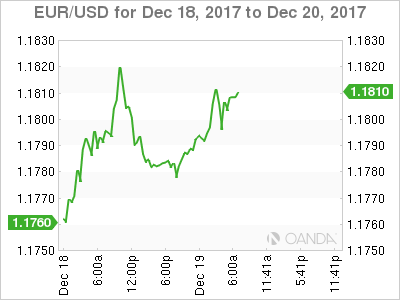

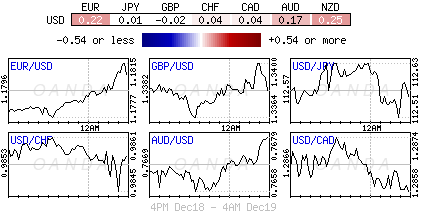

FOREX: The dollar was steady versus the yen at 112.62 as investors were waiting for the final tax vote to begin today, while trading was in general thin ahead of the holiday season. The euro, on the other hand, posted moderate gains versus the greenback, edging up to an intra-day high of 1.1817(+0.23%) and remained flat against the pound at 0.8832 as the German Ifo business climate index inched below expectations but remained at record high levels in December. The pound fell back to yesterday's lows, trading at $1.3370, while the aussie and the kiwi consolidated around today's highs.

STOCKS: The pan-European STOXX 600 rose to a fresh six-week high (+0.17%) as financials and consumer cyclicals continued to support the index. The blue-chip Euro STOXX 50 was flat at 1000 GMT with losses in utilities offsetting gains in telecommunications. The Spanish IBEX 35 and the British FTSE 100 jumped by 0.24%.

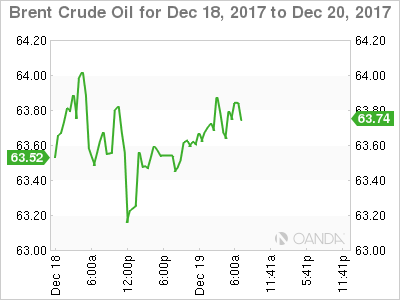

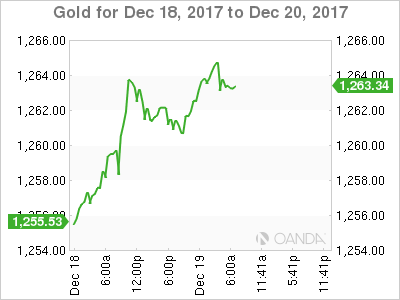

COMMODITIES: The shutdown of the British Forties pipeline in the North Sea continued to underpin Brent, sending it 0.35% higher to $63.63 per barrel. WTI crude also held onto gains, climbing by 0.45% to $57.42 as OPEC-led supply cuts supported the market despite concerns over a rising US oil production. Gold was last seen at $1,263.00 per ounce (+0.14%).

Day ahead: US Congress to make final decision on tax legislation

The long-awaited US tax vote will take place today around 1830 GMT at the House of Representatives before Senators also likely voting in favor of the final bill probably later today or on Wednesday. Projections are for the tax cuts to turn into law despite doubts over the post-growth effect remaining in the background. Positive sentiment on the tax code strengthened on Monday after two Senate Republicans agreed to back the legislation.

Meanwhile, the US Department of Commerce and the Bureau of Economic Analysis are scheduled to publish housing data and readings on the current account at 1330 GMT. Analysts expect the current account to improve from -$123.1 billion to -$116.8 billion in the third quarter, while they also forecast a slowdown in November's building permits and housing starts. The number of building permits and new constructions are said to decline by 0.04 million to 1.27 million (-3.1% m/m) and by 1.25 million respectively (-3.2% m/m).

At 2145 GMT, New Zealand will release figures on the current account as well as trade. Year-on-year, the current account is forecasted to rise by NZ$0.59 billion to -NZ$6.90 billion in the third quarter, whereas on a quarterly basis the deficit is anticipated to widen to -NZ$4.290 billion (six times larger than in the previous quarter).

Moreover, global dairy auction data are due today (the release, however, is tentative without a specific time of release), bringing some volatility to the kiwi.

In energy markets, investors will be waiting for the API weekly report at 2145 GMT to indicate the change in US crude oil stocks for the week ending December 15.

Stock Bulls Take The Lead, Dollar Keeps Calm

Tuesday December 19: Five things the markets are talking about

As is widely expected, markets remain stable and contained within tight ranges through the last few session of the pre-Christmas week.

Developed market volatility is at its lowest level in nearly three-years, but given the sensitivity currently being shown to political developments, investor caution is a necessity.

Today's main focus will be the progress of the U.S tax reform bill, with the House of Representatives expected to vote on it this afternoon, followed by the Senate either today or tomorrow.

In the U.K, a full cabinet discussion on the future trading relationship with the E.U is taking place, following yesterday's preliminary discussions. Sterling beware, the market is expecting that the second stage of Brexit negotiations to be more challenging than the recently concluded initial discussions.

1. Stocks look to U.S Tax Bill for support

In Japan, regional equities eased overnight in choppy trade as construction shares extended losses on bid-rigging scandal. The Nikkei ended -0.2% lower, while the broader Topix shed -0.3%.

Down-under, Aussie shares closed near their decade high overnight as optimism over the U.S tax bill boosted investor sentiment. The S&P/ASX 200 index rallied +0.5%, while in Korea's Kospi edged -0.1%

In China and Hong Kong, stocks followed Asian markets higher, inspired by a record-setting session on Wall Street. The Shanghai Composite index was up +0.53%, while the blue-chip CSI300 index was up +0.8%. In Hong Kong, the Hang Seng index was up +0.7%, while the Hang Seng China Enterprises index rallied +1.11%.

In Europe, regional indices trade higher across the board continuing the upward trend as year-end approaches, supported by positive investor sentiment on U.S tax reform, as well as a continued elevated German Ifo reading this morning (see below).

U.S stocks are set to open in the black (+0.1%).

Indices: Stoxx600 +1% at at 393.1, FTSE +0.2% at 7554, DAX flat at 13317, CAC-40 -0.1% at 5416, IBEX-35 +0.3% at 10275, FTSE MIB +0.1% at 22420, SMI +0.1% at 9460, S&P 500 Futures +0.1%

2. Oil rallies on U.K pipeline issues, gold stable

Oil prices remain better bid amid an ongoing North Sea pipeline outage and because a strike by Nigerian oil workers threatened its crude exports. Also, signs that booming U.S crude output growth may be slowing is also supporting the market.

Brent crude futures are at +$63.72 a barrel, up +49c or +0.8%, from yesterday's close. U.S West Texas Intermediate (WTI) crude futures are at +$57.70 a barrel, up +40c or +0.7%.

North Sea operator Ineos has declared 'force majeure' on all oil and gas shipments through its Forties pipeline system, while in Nigeria, the Petroleum and Natural Gas Senior Staff Association have started industrial action after talks with government agencies ended in deadlock.

With oil inventories falling globally, investors will take direction from this week's supply reports. Today's API data (4:30 pm EDT) is expected to show a further reduction in U.S crude inventories.

Gold prices remain range-bound as the 'big' dollar holds firm on U.S tax bill hopes. The 'yellow' metal has increased +0.2% to +$1,263.21 an ounce, the highest in more than a week.

3. Sovereign yield rise on U.S tax optimism

Global bond yields have edged up ahead of the U.S open as the market bets that U.S lawmakers will finally pass Trump's tax legislation this week that could boost growth and inflation.

Note: A view that interest rates will rise over the short-term, but inflation will remain subdued over the long term, has dominated the yield 'flattening' trade.

The spread between U.S shorter-dated and longer-dated Treasury yields widened yesterday from its narrowest in a decade on profit trading.

The yield on U.S 10-year Treasuries has backed up +1 bps to +2.39%. In Germany, the 10-year Bund yield has advanced +1 bps to +0.32%, while in the U.K, the 10-year Gilt yield has also climbed +1 bps to +1.158%.

Down-under overnight, the Reserve Bank of Australia's (RBA) Dec. minutes reiterated that the low level of interest rates was continuing to support the Australian economy with inflation to pick up gradually as the economy strengthens. Policy makers also noted that an appreciating FX rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecasted.

4. Dollar stays calm

On Monday, the 'mighty' U.S dollar was mostly weighed down by worries that the Fed may not raise interest rates at a faster pace in 2018 despite solid U.S growth.

Despite the Fed raising interest rates by +25 basis points last week, the central bank did not revise its long-term views on inflation, and stuck to its earlier projections of three rate increases next year. A percentage of the market had expected the Fed to change its viewpoint in light of more robust economic growth.

The overnight session saw a relatively subdue price action, but the USD remains a tad softer as the market continues to assess the potential impact of U.S tax bill. The EUR/USD (€1.1806) is a tad higher by +0.2%, while GBP/USD (£1.3370) trades further away from strong resistance at the £1.3400 handle. USD/JPY remains unchanged at ¥112.60.

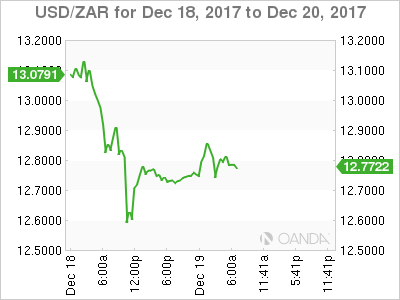

The ZAR ($12.7852) has seen some of yesterday's strong gains retrace in the aftermath of the ANC party leadership vote outcome. It's been a wild +7-8% swing for the currency over the past couple of sessions. The USD/ZAR tested $12.40 area after market-favored Ramaphosa was formally elected.

Bitcoin was last down -1.04% at $18,763, following an early-week fall amid the launch of CME futures trading.

5. German Ifo and E.U Labour costs

German data released this morning showed that Dec Ifo at 117.2 was a tad lower than the forecast of 117.5.

The small decline in the business sentiment from a record high suggests that the outlook for next year is bright despite the uncertain political backdrop and the prospect of ECB QE tapering. But with wage growth still very subdued in Q3, the ECB will be in no hurry to raise interest rates.

Elsewhere, the annual growth rate of euro-zone total hourly labour costs slowed from +1.8% in Q2 to +1.6% in Q3. Digging deeper, wage growth also fell (from +2.1% to +1.6%).

With productivity growth running at around +0.8%, this implies that unit labour costs are increasing at a very 'modest' pace which is somewhat inconsistent with the ECB's near +2% inflation target.

Euro Punches Above 1.18 Despite Soft German Ifo Business Climate

The euro has started the week with gains. Currently, EUR/USD is trading at 1.1805, up 0.20% on the day. On the release front, German Ifo Business Climate dipped to 117.2, short of the forecast of 117.6 points. In the US, today's key event is Building Permits, which is expected to slow to 1.25 million. We'll also get a look at Current Account and Housing Starts. On Wednesday, Germany releases PPI and the US publishes Existing Home Sales.

Germany's political landscape remains unclear, as coalition talks continue at a snail's pace. President Angela Merkel's conservative bloc suffered losses in the September election, and talks with smaller parties proved fruitless. Merkel has now shifted her efforts at her previous junior coalition party, the Social Democrats (SDP). On Friday, the SDP voted to begin exploratory talks with Merkel, with a view to discussing substantive issues in January. Many SDP lawmakers want a more senior role for the SDP in any coalition, and the SDP will likely demand key portfolios in a new government. Despite the political uncertainty, the German economy continues to look very strong.

President Trump's tax reform bill appears ready to sprint across the finish line, thanks to feverish efforts by Republican lawmakers in recent weeks. After the House and Senate reconciled their versions of the tax bills, the Republicans hammered out the sticking points and reconciled the bills. The uniform legislation is expected to be voted on in the House on Tuesday and the Senate on Wednesday. With Democrats in both branches opposing the bill, the Republicans will need every vote in the Senate, where they have a thin 59-41 majority. Several Republican senators who were undecided have said they will vote in favor, so the bill is likely to pass through Congress and will then be signed into law by President Trump. This marks the first major overhaul of the US tax code in 30 years, and would represent a huge victory for Trump, ahead of Congressional elections in 2018.

Equity Enthusiasm

Equity enthusiasm

Global markets are celebrating US tax reform. Asian stocks followed the record session on Wall Street. This bull market keeps running past forecasts, and profit-taking to lock in a solid year is not happening.

The World Bank increased its forecast for China’s economic growth in 2017 to 6.8% up from 6.7% in October. In 2018 China is likely to outpace consensus forecast. Our view of China and its RMB currency have brightened. The Bank of China’s 5-basis-point hike in front-end reverse repo and 1-year medium-term lending facility rates was less about managing immediate threats and more about signalling a tightening bias across monetary, regulatory and liquidity policies.

Dollar doves flap

With a warning from US Federal Reserve banker Neel Kashkari that increasing interest could trigger a recession, dollar doves are alive and vocal. We believe they will prevail enough to block some additional hikes. We are seller of USD in the mid-run against high yielding emerging market and G10 currencies.

Last week meeting the Fed voted for a 0.25% hike and increased its 2018 real GDP forecast, reflecting the boost of tax reform. Yet the policy projections were left broadly unchanged

USDZAR Bounces Off Lows After Strong Sell-Off

USDZAR has a bearish bias in the near term as the flow is back to the downside following the break below the upward sloping channel that was standing since March 27. The price plunged more than 5% in the previous couple of days and printed a fresh nine-month low at 12.51.

Today, the pair is making a timorous recovery but in case of further losses, the price could test the 12.31 support level.

As long as USDZAR remains below the rising channel the downward momentum holds. However, a run back above the lower boundary of the channel could push the price towards the 13.24 resistance barrier.

In the short to medium-term timeframe (daily chart), the picture is negative as the MACD and the RSI technical indicators are holding in the bearish area. The MACD oscillator is strengthening its bearish state and is moving beneath the zero and trigger lines, whilst the RSI indicator bounced off the 30 level and is slightly pointing north. The market is also below the 50, 100 and 200-period simple moving averages.

EURUSD Bullish SHS Pattern Close To D L3 Camarilla Pivot

As I showed yesterday on my Session Recap webinar, the EUR/USD made the retracement to 1.1770 zone and rejected as planned. We can see a Bullish SHS pattern (inverted Head and Shoulders) formed slightly above the D L3 Camarilla pivot. That implies a potential continuation of a bullish setup towards 1.1834 and 1.1878. However, a clear h1 or h4 close above 1.1825 is needed for the price to proceed further up. In case of retracement, pay attention to 1.1760-75 zone again ( right shoulder, 78.6, atr pivot, D L3) and a possible rejection again. As long as the price is held above the W L3 - 1.1714 the EUR/USD is bullish.

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

CRUDE OIL Volatility Declines

Crude oil is has failed to break resistance given at 59.05 (24/12/2017 high). Support is given at 55.82 (07/12/2017 low). As volatility declines, expected to show further bearish breakout.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. For the time being the pair lies in an upside momentum. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

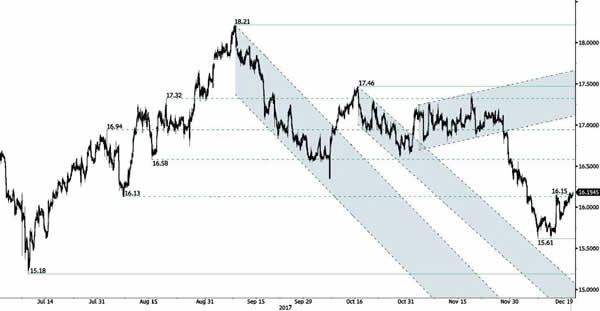

SILVER Continued Bounce

Silver has been bouncing on hourly support at 15.61 (14/07/2017 low). Hourly resistance given at 16.15 (13/12/2017 high) has been broken. Expected to show continued bullish pressures.

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).