Sample Category Title

Daily Wave Analysis: USD/JPY Contracting Triangle In Bearish ABC Zigzag

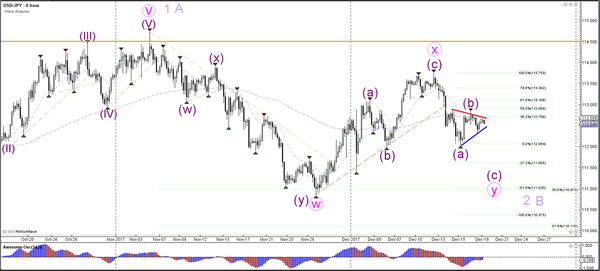

Currency pair USD/JPY

The USD/JPY is building a triangle correction (red/blue lines) which is probably part of a wave B (purple). A break below support could see price extend its bearish momentum towards the Fib targets at 111 and 110.

The USD/JPY respected the 38.2% Fib but could see a deeper Fib bounce if price were to break above resistance. A break above the 100% Fib level at 113.75 invalidates the ABC zigzag whereas a break below the support could confirm it

Currency pair EUR/USD

The EUR/USD needs to break the support or resistance trend line before the short-term direction becomes clear. A break below the 100% Fib level of wave 2 vs 1 invalidates the wave 2 (pink) and indicates an expansion of wave 4 (light purple).

The EUR/USD completed a bearish ABC (green) but the bullish rally is probably an extension of the larger correction and has been labelled as a wave X (blue). The wave X is invalidated if price breaks above the 138.2% Fib and becomes less likely when price breaks above the 100% Fib.

Currency pair GBP/USD

The GBP/USD is in between a larger support and resistance trend line. The correction could be a large bull flag chart pattern. A bullish breakout could confirm the pattern and a wave 5 of wave C

The GBP/USD break below the 61.8% makes a wave 4 less likely.

US Rates And The DXY Index Are Little Changed

Market movers today

It is a fairly thin data calendar today with most focus on the US Republican tax bill amid the House and the Senate being on the verge of passing the bill.

In the euro area, the wage growth figures for Q3 are due for release today. Wages have been increasing steadily since Q3 16, reaching 1.8% y/y in Q2 17. Although wage growth has increased, it is still well below the pre-crisis average (from 1996 to 2008) of around 2.4% y/y. We do not expect wage growth to catch up to the pre-crisis average in the near future, as inflation expectations and negotiated wages (especially in Germany) do not show an upward trend. We expect wage growth to remain around 1.8% y/y in H2 17.

The German Ifo expectations are also released today. Ifo expectations have been on the rise since we entered 2016 and this measure of German business sentiment might not have reached its peak yet , although ZEW expectat ions dropped to 17.4 in December.

Other: In Sweden, the National Institute of Economic Reasearch will release macro forecasts. In South Africa, markets will watch closely any signals from the newly-elected ANC leader, Cyril Ramaphosa. Finally, the central bank (MNB) meeting in Hungary will reveal more details on its new exceptional quantitative easing programme.

Selected market news

The global equity rally has continued amid rising expectations that the Republicans will get through a bill to overhaul the US federal tax code before year-end. In the US, the major indices have reached new highs and this morning most indices in Asia are trading in ‘green' territory. In comparison, US rates and the DXY index are little changed since Friday, which might underline a market belief that the total growth impact of the proposed tax bill should prove limited. We have made the last scheduled revision this year to our FX projections. In short, we have made few changes and still pencil in a weaker USD next year despite the US tax reform.

In South Africa, Cyril Ramaphosa has won the ruling African National Congress' leadership contest . The election of Ramaphosa, the current deputy president of South Africa and a former successful businessman, is clearly market positive as he has run on a pro-business and anticorruption campaign, trying to dist inguish himself from President Jacob Zuma.

In terms of China, yesterday we published our leading indicator update. In short , our favourite indicators in the likes of home sales, credit impulse and commodity price inflation still point to a moderate slowdown but the downturn is cushioned by solid export indicators. The financial implications of this are less tailwind to equities (all else being equal), lower global inflationary pressures and support to global fixed income markets at the beginning of 2018.

In a blogpost, the Fed's Neel Kashkari explained why he dissented against last week's US interest rate hike. In short, he based the decision on the same arguments for his previous dissents – e.g. that labour market slack is underestimated, that low inflation expectations are becoming self-fulfilling – but this time he added that the US yield curve flat tening was worrying to him. Importantly, Kashkari and the other dissenter Charles Evans will not be voting members in 2018.

RBA More Confident About The Economic Outlook, But Remained Worried About Consumer Spending: RBA Minutes

For the 24 hours to 23:00 GMT, the AUD rose 0.12% against the USD and closed at 0.7668.

LME Copper prices rose 1.6% or $108.5/MT to $6844.0/MT. Aluminium prices gained 0.6% or $11.5/MT to $2047.5/MT.

The Reserve Bank of Australia (RBA), in its minutes of the December meeting, stated that recent data had increased confidence that there would be further progress on fronts such as unemployment, inflation and household debt in 2018. The central bank expects employment growth to continue over the coming quarters but remained concerned over household consumption and the outlook for higher wages. The RBA warned that weakness in consumer spending remains a major risk for the economy amid slow wage growth and high debt levels.

In the Asian session, at GMT0400, the pair is trading at 0.7661, with the AUD trading 0.09% lower from yesterday's close.

The pair is expected to find support at 0.7650, and a fall through could take it to the next support level of 0.7639. The pair is expected to find its first resistance at 0.7675, and a rise through could take it to the next resistance level of 0.7689.

Going forward, investors would now turn their attention to Australia's Westpac leading index for November, due to release overnight.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages

Eurozone Inflation Advanced As Expected In November

For the 24 hours to 23:00 GMT, the EUR rose 0.20% against the USD and closed at 1.1783, after data showed that the Eurozone's consumer price index (CPI) rose at an annual rate of 1.5% in November, in line with the previous estimate. The increase in the region's inflation was mainly driven by higher energy prices.

Meanwhile, the US NAHB housing market index climbed to an 18-year high in December, as it rose to 74 from a revised level of 69 in November. Market had expected the index to report a level of 70.

In the Asian session, at GMT0400, the pair is trading at 1.1788, with the EUR trading a tad higher from yesterday's close.

The pair is expected to find support at 1.1752, and a fall through could take it to the next support level of 1.1716. The pair is expected to find its first resistance at 1.1829, and a rise through could take it to the next resistance level of 1.1870.

Moving ahead, Germany's Ifo survey on business climate, expectations and current assessment, all for December, due in a few hours would be closely monitored by investors. Also, the Eurozone's construction output data for October would be eyed by market participants. Moreover, the US housing starts and building permits, both for November, scheduled later today, would garner significant amount of market attention.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

UK CBI Manufacturing Order Growth Stayed At A 30-Year High

For the 24 hours to 23:00 GMT, the GBP rose 0.38% against the USD and closed at 1.3383.

Data indicated that the UK CBI industrial trends orders remained unchanged at 17 in December from the last month. Market had expected CBI industrial trends orders to dip slightly to 15.

In the Asian session, at GMT0400, the pair is trading at 1.3380, with the GBP trading a tad lower from yesterday’s close.

The pair is expected to find support at 1.3335, and a fall through could take it to the next support level of 1.3289. The pair is expected to find its first resistance at 1.3422, and a rise through could take it to the next resistance level of 1.3463.

With no economic data scheduled in the UK today, trading in the currency pair would be governed by global macroeconomic events.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Japanese Yen Trading Lower In The Asian Session

For the 24 hours to 23:00 GMT, the USD declined 0.06% against the JPY and closed at 112.57.

In the Asian session, at GMT0400, the pair is trading at 112.63, with the USD trading 0.05% higher from yesterday’s close.

The pair is expected to find support at 112.38, and a fall through could take it to the next support level of 112.13. The pair is expected to find its first resistance at 112.81, and a rise through could take it to the next resistance level of 112.99.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Swiss Franc Trading Marginally Higher In The Morning Session

For the 24 hours to 23:00 GMT, the USD declined 0.44% against the CHF and closed at 0.9862.

Data showed that Switzerland’s total sight deposits declined to CHF575.4 billion in the week ended 15 December from a level of CHF575.9 billion in the previous week.

In the Asian session, at GMT0400, the pair is trading at 0.9858, with the USD trading slightly lower from yesterday’s close.

The pair is expected to find support at 0.9830, and a fall through could take it to the next support level of 0.9801. The pair is expected to find its first resistance at 0.9897, and a rise through could take it to the next resistance level of 0.9935.

Ahead in the day, the SECO economic forecast for December would be monitored by traders.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Loonie Trading Slightly Higher This Morning

For the 24 hours to 23:00 GMT, the USD rose 0.08% against the CAD and closed at 1.2869.

In the Asian session, at GMT0400, the pair is trading at 1.2867, with the USD trading marginally lower from yesterday’s close.

The pair is expected to find support at 1.2846, and a fall through could take it to the next support level of 1.2826. The pair is expected to find its first resistance at 1.2884, and a rise through could take it to the next resistance level of 1.2902.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

RBA Added Some Hawkish References In December Minutes

The RBA minutes for the December meeting revealed that policymakers were more upbeat on the global and domestic economic outlook. While maintaining a natural monetary policy stance, the minutes contained some hawkish ingredients, suggesting that recent data on employment and inflation have made the members more confident. The key concerns remained subdued wage growth and household consumption.

The last paragraph evidenced the central bank's more upbeat outlook. As noted in the minutes, 'the unemployment rate had fallen and inflation had moved closer to target'. It added that 'recent data had increased confidence that there would be further progress on these fronts over the following year'. The minutes also acknowledged that 'risks in household balance sheets had lessened'.

Yet, Australian economy is not without risks. Indeed, policymakers noted that the outlook for household consumption remains 'a significant risk' as wage growth remained low and debt levels were high. Yet, they added that its liaison program was 'suggesting that moderate growth in consumption had continued into the December quarter', citing the stronger-than-expected retail sales growth of +0.5% m/m in October. On the property market, RBA forecast that dwelling investment should 'remain at a high level for the following year or so'.

On the monetary policy stance, the RBA retained the view that 'holding the stance of monetary policy unchanged at this meeting would be consistent with sustainable growth in the economy and achieving the inflation target over time'. It added that 'how far and when stronger conditions in the economy and labour market might feed through into higher wage growth and inflation remained important considerations shaping the outlook.

Market Morning Briefing: The Euro-Yen Is Absolutely Ranged Between 132-134 For Now

STOCKS

Expectations that the republicans would come out with their tax plans this week and some news stating lower tax rates for bankers and retailers is giving a boost to the equities. Dow (24792.20, +0.57%) is headed to make a high of 25000 and it could happen faster than our expectations. As mentioned yesterday near term looks bullish.

Optimism and heightened expectations of US tax cut has aided the Dax (13312.30, +1.59%) too to move higher. A break above 13150 has been seen finally and while that sustains, it would trigger a sharper rise towards 13400 or even higher in the near term. After breaking on the upside from the medium term sideways phase, the index could possibly gather some momentum now. Bullishness likely to prevail for the coming sessions.

Resistance near 23000 seems to be holding well on the Nikkei (22910.79, +0.04%) just now and while below 23000, the index could come off towards 22700-22500 levels in the coming sessions. Sideways trade within 23000/200-22500 levels is possible in the near term.

Shanghai (3286.65, +0.57%) has managed to bounce back yesterday from 3250 but while below 3325, the index may have some chances of testing lower levels of 3225. Some sideways movement is possible for now.

Nifty (10388.75, +0.54%) saw high fluctuation in the 10050-10450 region yesterday but after the BJP win in the Gujarat elections, the index could try to move up towards 10500-10550 in the next few sessions. There could also be a slight possibility of a re-test of 10100 before the index starts to rise towards 10500 or higher.

Sensex (33601.68, +0.41%) could trade within 33000-34000 for a couple of sessions before trying to attempt higher levels.

COMMODITIES

Gold and Copper looks bullish just now while the crude prices could remain stuck in some narrow and small movements in the next few sessions.

Gold (1261.60) has moved up a bit and looks bullish towards 1270-1280 in the near to medium term. Immediate resistance is visible near 1280.

Brent (63.52) and WTI (57.39) are almost stable. Earlier mentioned targets of 58.0-58.5 (for WTI) and 65-66 (for Brent) remain on the upside and while that holds, a small corrective dip could be seen followed by a sharp rise later on.

Copper (3.1275) is likely to come off from 3.15 to test lower levels of 3.05-3.00 again. Failure to come off from there just now would take it higher towards 3.20, but that looks less likely just now.

FOREX

Most currencies may go quiet over the next couple of days, headed into the holidays. While the Euro and Pound look potentially weak, the Yen and Aussie look potentially strong.

Although the Euro (1.1786) continues to trade above the mentioned Support at 1.1750, its failure to build on its rise to 1.1834 last night is a sign of potential weakness. Alternatively, the market is just hunkering down for the X'mas/ New Year week and may trade sideways between 1.1750-1825 for the next couple of days. The trend-deciders to be watched for the medium term are 1.1700 and 1.1900.

Dollar-Yen (112.60) too is likely to be quietly ranged between 112-113.50 for a few days now. In the bigger picture we shall see whether it is able to break below 112 or not.

The Euro-Yen (132.73) is absolutely ranged between 132-134 for now, but has long-term Resistance in the 134.05-45 region and could be vulnerable to the downside on a break below 132.00-131.75. This will be an interesting pair to watch in early 2018.

Look for near-term range trade between 1.33-35 in the Pound as well. Longer term could be bearish while below the Resistance at 1.35.

Unlike the Euro and Pound, which seem to have long-term Resistances overhead, the Aussie (0.7658) has bounced well from 0.75 last week and appears potentially bullish in the long-term.

Dollar-Rupee (64.24) may range between 64.15-30 today. A break below 64.05 or above 64.40 is needed to start a trend for the coming weeks.

INTEREST RATES

The German-US 10Yr Spread (-2.09%) continues to move down as German 10Yr has Resistances overhead at 0.40% while the US 10Yr has Support at 2.35%.

The German-Japan 10Yr Spread (0.27%) is also moving down and has broken below earlier support in the 0.30-28% region recently. Further decline below 0.25% could pull the Euro-Yen lower.

The 10Yr GOI (7.18%) remains in an uptrend as of now, but may face Resistance near 7.25% in the coming days which could produce a corrective fall towards 7.00% in the medium term.