Sample Category Title

Global Equities Surge on US Tax Plan, Dollar Shrugs it and Stays Soft

While the it looks like Dollar couldn't care less, global equities seem to be responding very well to the developments on the US tax plan. House and Senate Republicans are expected to pass the final bill mid-week. And the bill could then be on President Donald Trump's desk before Christmas. Nikkei closed up 1.55% at 22901.77 earlier today. European indices follow and gains broadly. In particular, DAX is up 1.6% at the time of writing while CAC 40 is up 1.2%. In the currency markets, major pairs and crosses are generally stuck in range with exception in weakness in Canadian Dollar. Euro is trading broadly higher with Nov Eurozone CPI finalized at 1.5% yoy.

DOW to extend record run on tax optimism

DOW futures point to triple digit gain at open, in response to tax bill optimism. With that strong momentum, DOW should finally take out 161.8% projection of 20379.55 to 22179.11 from 21731.12 at 24642.80. While the index is clearly overbought, as seen in daily MACD, more upside acceleration could follow to 200% projection at 25330.24. It's early to talk about topping yet.

BoJ to stand pat this week, Kataoka might dissent again

BoJ will start its two day monetary policy meeting on Wednesday and announce the decision on Thursday. With core CPI standing at 0.8%, there is little room for BoJ to talk about exiting stimulus. It's widely expected to keep policy unchanged. That is, short-term policy interest rate will be kept at -0.1%. And under the yield curve control framework, BoJ will continues with the annual pace of JPY 80T JGB purchases to keep 10 year yield at around zero. Goushi Kataoka will likely dissent the decision again and continues his push for more stimulus. Also, Kataoka will also maintain his put to target 15 year yield to less than 0.2% too.

Japan adjusted trade surplus widened to JPY 364b in November, above expectation of JPY 270b. Exports rose 14.7% yoy while import rose 17.2% yoy. Increase in exports were broad based. Exports to China rose 25% yoy, to US rose 13% yoy, to EU also rose 13% yoy. The data adds to the case that the export-led Japanese economy is on track for gradual recovery.

RBA minutes to watch in upcoming Asian session.

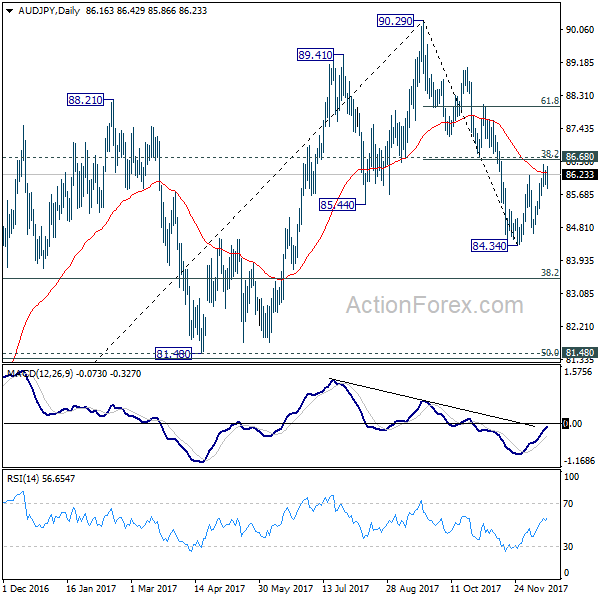

RBA minutes will be a focus in the upcoming Asian session. Aussie was strong last week as boosted by stellar job data. But after all the job growth, wage growth remained sluggish. And that's a key factor in keeping inflation low, and holding RBA's hand. Indeed, markets are expecting the central bank to stand pat throughout 2018. Hence, until a turnaround is seen incoming data, we'll view current rebound in the Aussie as a corrective move at most

This is also inline with the technical picture in AUD/JPY too. The rebound from 84.34 is held below 86.68 cluster resistance (38.2% retracement of 90.29 to 84.34 at 86.61). Such rebound is seen as a correction. Fall from from 90.29 is expected to resume later through 84.34 to 38.2% retracement of 72.39 to 83.45, and possibly to 81.48 cluster support (50% retracement at 81.34). However, sustained break of 86.61/8 will dampen our bearish view.

China's hike last week partly driven by Fed's move

Last week, China's PBOC lifted the 7-day and 28-day OMO reverse repo rates by 5 bps to 2.5% and 2.8% respectively. It also raised the 1-year MLF rates by 5 bps to 3.25%. These were in response to the Fed's 25-bps rate hike in the prior day. Note that the PBOC has raised the policy rates for three times this year. The previous two times were the 10-bps hikes in the OMO and MLF rates in February and March.

As suggested in the accompanying statement, the rate hikes last week was partly driven by the Fed's rate hike. The PBOC stressed that it does not follow closely the monetary policy of the Fed, citing the inaction after Fed's June rate hike. More importantly, the rate hike was in response to the market rates which have been markedly higher than those guided by the central bank. Despite the fact that the rate hikes came in lower than consensus, PBOC believed that it would help discourage leveraging and excessive credit expansion. More in PBOC's Rate Hike Is Consistent With The Deleveraging Theme That Would Be Reiterated At CEWC

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9870; (P) 0.9902; (R1) 0.9931; More....

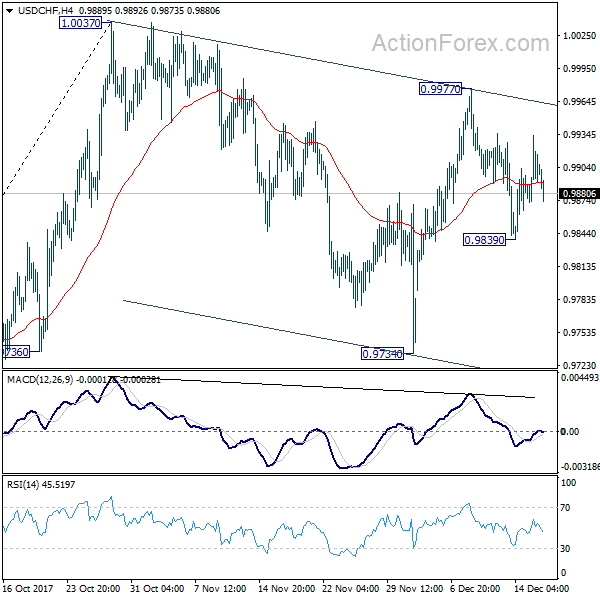

USD/CHF drops slightly today but intraday bias remains neutral at this point. On the upside, above 0.9977 will resume the rebound from 0.9734 for 1.0037 resistance. Break there will resume whole rally from 0.9420 and target 1..0342 key resistance next. On the downside, below 0.9839 will likely extend the correction from 1.0037 through 0.9734. But in that case, we'd expect strong support from 61.8% retracement of 0.9420 to 0.1.0037 at 0.9656 to contain downside and bring rebound.

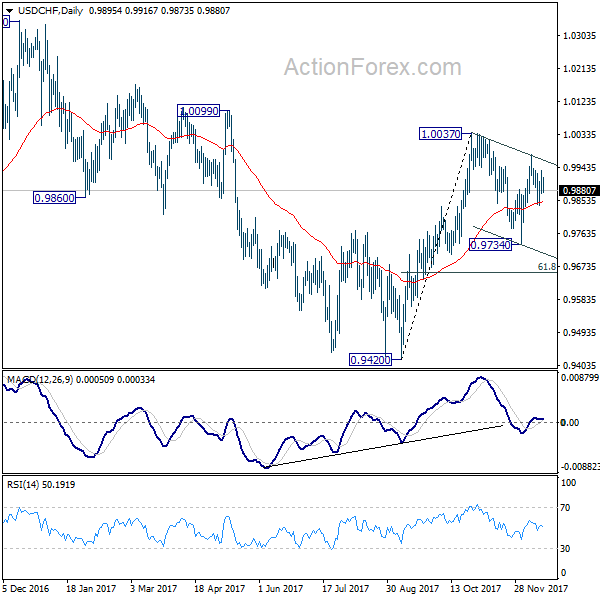

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Trade Balance Nov | 0.36T | 0.27T | 0.32T | 0.35T |

| 10:00 | EUR | Eurozone CPI M/M Nov | 0.10% | 0.10% | 0.10% | |

| 10:00 | EUR | Eurozone CPI Y/Y Nov F | 1.50% | 1.50% | 1.50% | |

| 10:00 | EUR | Eurozone CPI Core Y/Y Nov F | 0.90% | 0.90% | 0.90% | |

| 11:00 | GBP | CBI Trends Total Orders Dec | 17 | 15 | 17 | |

| 13:30 | CAD | International Securities Transactions (CAD) Oct | 16.81B | |||

| 15:00 | USD | NAHB Housing Market Index Dec | 70 | 70 |

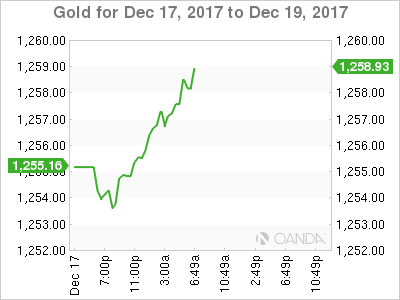

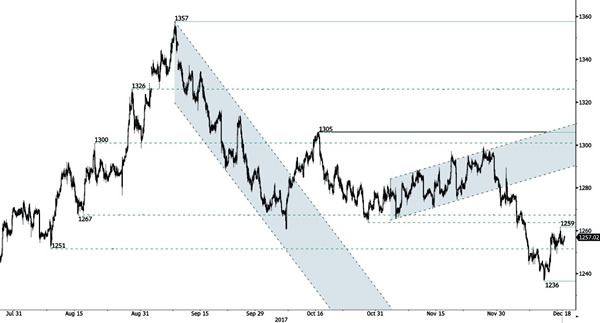

Gold Stuck In Range After Rebounding Off 5-Month Lows, Risk Is To Upside

Gold prices are firmer after rebounding off a 5-month low of 1236.49 last week but remain stuck in a range between 1250 and 1260 during the past few trading days. The flat RSI on the 4-hour chart is indicative of no clear direction in the market.

Risk though is tilted to the upside as prices are trading in the upper half of the Bollinger Band. Also, gold has crossed above the 50-period MA, strengthening the prospects for more upside in the near term.

But prices are nearing a resistance zone between 1259 and the 1261.82 high. A sustained move higher would open the way to target the key 1270 level, which would result in a shift to a bullish phase.

Caution is needed as the 50 and 200-period moving averages are bearishly aligned. Gold’s inability to break out of its current range and rally higher in the near-term may increase the risk of falling below 1250 with scope to re-test the 1236.49 low.

Trump Aims To Be No Mr. Scrooge

Monday December 18: Five things the markets are talking about

In the last full trading week of the year, global equities are kicking off on a positive note after Friday's Republican Senate caucus agreement on the shape of U.S tax cuts aimed at boosting growth in the world's largest economy.

The vote is expected to take place Tuesday – which will almost certainly pass – with passage onto a Senate vote later in the week and possibly allow President Trump to sign into law ahead of Christmas.

The Bank of Japan (BoJ) will meet mid-week (Dec. 20), and is expected to maintain its current policy.

Elsewhere, it is a relatively light week for economic data. November merchandise trade data will be released for Japan, while Q3 final GDP estimates will be released for the U.K, U.S, France and New Zealand.

Tomorrow, in Germany, the December Ifo survey will be posted, while Spain's Catalonia votes on Thursday in a regional election for the second time on independence.

Note: The Czech Republic, Hungary, Taiwan and Thailand also set interest rates this week.

In China, President Xi Jinping kicks off China's Central Economic Work Conference. The market will focus on whether officials will cut the growth target from this year's +6.5% or actually increase it. In the U.K, PM Theresa May addresses parliament today and meets with her cabinet tomorrow to begin work on a trade wish list. The E.U will unveil its position on Wednesday.

Finally, the market is also waiting for the outcome of South Africa ruling ANC party leadership elections – the two presidential candidates are Nkosazana Dlamini-Zuma and Cyril Ramaphosa.

1. Stocks get the green light

In Japan, equities scored their biggest rally in four-weeks overnight with financials and exporters in demand. The Nikkei share average finished +1.55% higher while the broader Topix was up +1.36%.

Down-under, Aussie shares finished higher overnight, with broad-based gains driven by stronger commodity prices, financials stocks and optimism around U.S tax reform. The S&P/ASX 200 index rose +0.7% at the close, ending a two-day losing streak. On the year, the index is up +7% this year, which would actually be its best performance since 2013.

In Hong Kong, equities closed firmer, with regional sentiment boosted by expectations that U.S lawmakers will pass the tax bill. *At close of trade, the Hang Seng index was up +0.7%, while the Hang Seng China Enterprises index rose +0.43%.

In China, Shanghai stocks slipped overnight, amid concerns over tight year-end liquidity after the People's Bank of China (PBoC) lifted interbank market rates. The Shanghai Composite index was down -0.13%, while the blue-chip CSI300 index was unchanged.

Note: The PBoC raised interest rates on reverse repos by +5 bps for the 14-day tenor.

In Europe, regional indices start the week on the front foot, trading atop of six-week highs as optimism over the U.S tax plan continuing to support markets.

U.S stocks are set to open in the black (+0.3%).

Indices: Stoxx600 +0.8% at 391.2, FTSE +0.3% at 7512, DAX +1.2% at 13258, CAC-40 +1.2% at 5413, IBEX-35 +0.7% at 10217, FTSE MIB +0.8% at 22274, SMI +0.3% at 9425, S&P 500 Futures +0.3%

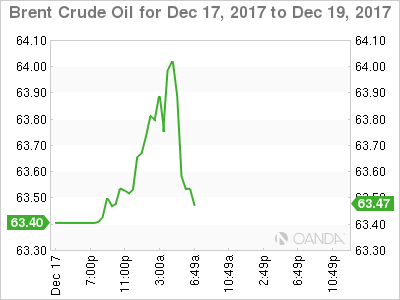

2. Oil prices rise on ongoing North Sea outage, Nigeria strike, and gold higher

Oil prices remain better bid amid an ongoing North Sea pipeline outage and because a strike by Nigerian oil workers threatened its crude exports. Also, signs that booming U.S crude output growth may be slowing is also supporting the market.

Brent crude futures are at +$63.72 a barrel, up +49c or +0.8%, from Friday's close. U.S West Texas Intermediate (WTI) crude futures are at +$57.70 a barrel, up +40c or +0.7%.

North Sea operator Ineos has declared “force majeure” on all oil and gas shipments through its Forties pipeline system, while in Nigeria, the Petroleum and Natural Gas Senior Staff Association have started industrial action after talks with government agencies ended in deadlock.

While in the U.S, data on Friday (Baker Hughes) indicated that energy companies have cut rigs drilling for new production for the first time in six weeks – 747 rigs in production in the week ended Dec. 15.

Gold prices remain range-bound as the ‘big' dollar holds firm on U.S tax bill hopes. The ‘yellow' metal has increased +0.1% to +$1,257.21 an ounce, the highest in more than a week.

3. Sovereign yields mixed results

Expectations that the Bank of Japan (BoJ) may tighten policy and steepen the yield curve sooner rather than later are lifting long-dated Japanese interest rates.

In recent weeks, some BoJ officials have dropped hints that it could tweak its policy, but this week is expected to come too soon. Many investors think officials could eventually lift its 10-year bond yield target, currently around zero, by +25 bps in H1, 2018. Japan's 10-year JGB yield has dipped less than -1 bps to +0.042%, the lowest in two-weeks.

Elsewhere, the yield on 10-year U.S Treasuries has climbed +2 bps to +2.37%, while Germany's 10-year Bund yield has gained less than +1 bps to +0.31%. In the U.K, the 10-year Gilt yield has fallen -1 bps to +1.146%, the lowest in almost 14 weeks.

Note: Portuguese bond yields have fallen sharply this morning after a two notch ratings upgrade from Fitch on Friday – the country now holds an investment grade from two of the three major rating agencies and could soon return to major bond indices.

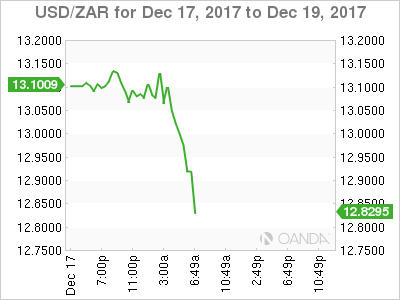

4. South Africa wait for ANC election results

The ZAR ($12.9504) remains better bid as South Africa's ruling ANC party votes for a successor to President Jacob Zuma today. The recent rally would suggest that the market is betting on a win for the pro-reform candidate Dlamini-Zumail Ramaphoosa. A win for Mr. Zuma's ex-wife Nkosazana Dlamini-Zuma would be negative for the rand.

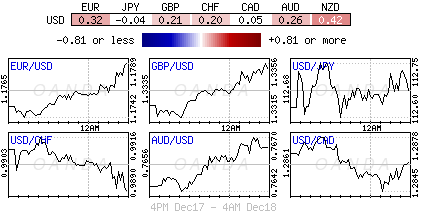

The USD trades mixed against the majors as the U.S tax reform bill moves closer to ratification. EUR is higher by +0.3% at €1.1791, but holding below the psychological €1.18 level. USD/JPY is little changed at ¥112.60 area.

Note: Republicans are confident Congress will now pass the tax bill this week, with a Senate vote as early as Tuesday and President Trump aiming to sign the bill by week's end.

5. Annual inflation up to +1.5% in the Euro area

Data this morning from Eurostat shows that Euro area annual inflation was +1.5% in November 2017, up from +1.4% m/m. In November 2016, the rate was +0.6%.

The E.U annual inflation was +1.8% in November 2017, up from +1.7% m/m. A year earlier the rate was +0.6%.

Digging deeper, the lowest annual rates were registered in Cyprus (+0.2%), Ireland (+0.5%) and Finland (+0.9%), while the highest annual rates were recorded in Estonia (+4.5%), Lithuania (+4.2%) and the U.K (+3.1%).

Note: Compared with the previous month, annual inflation fell in four Member States, remained stable in nine and rose in fifteen.

Euro Gains Ground As Eurozone CPI Edges Higher

The euro has started the week with gains. Currently, EUR/USD is trading at 1.1791, up 0.36% on the day. On the release front, Eurozone Final CPI improved to 1.5%, matching the forecast. There are no key indicators in the US. On Tuesday, Germany releases Ifo Business Climate and the US publishes Building Permits.

The Trump tax plan continues to wind its way through the corridors of Congress, but Republican lawmakers can see the light at the end of the tunnel. On Friday, the House and the Senate reconciled their tax bills. The uniform bill now goes to both branches, where it is expected pass by a slim margin, as all Democrats plan to vote against the bill. Crucially, two Republican senators who were opposed to the bill have now lent their support to the bill. The legislation is the first major overhaul of the US tax code in 30 years, and would represent a major victory for President Trump, who has campaigned vigorously for the legislation and wants to sign it into law before Christmas.

There were no surprises from the ECB on Thursday, as the Bank stayed on the sidelines and maintained interest rates at a flat 0.00%. ECB President Draghi sounded optimistic about economic conditions in the eurozone, noting that that ECB projections were “going in the right direction”. Draghi added a key caveat, stating that “an ample degree of monetary stimulus remains necessary”. The ECB raised its forecasts for growth and inflation, but this clearly wasn’t enough to coax the cautious Draghi to signal another taper of the Bank’s ultra-loose stimulus program. Some policy makers favored signaling a change in policy if inflation continues to move higher, but the majority favored staying the course, which means the ECB will continue buying bonds till September 2018 (or later) and will keep interest rates at record lows even longer.

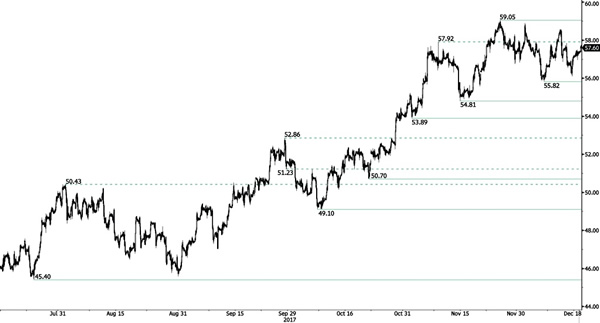

CRUDE OIL Ready For Another Leg Higher

Crude oil is has failed to break resistance given at 59.05 (24/12/2017 high). Support is given at 55.82 (07/12/2017 low). Expected to bounce back higher.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. For the time being the pair lies in an upside momentum. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

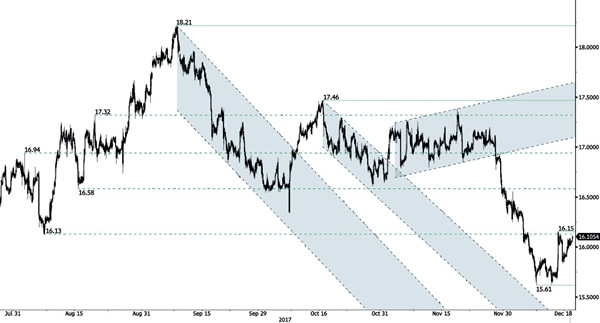

SILVER Short-Term Bullish

Silver has been bouncing on hourly support at 15.61 (14/07/2017 low). Hourly resistance is given at 16.15 (13/12/2017 high). Expected to show continued bullish pressures.

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

GOLD Starting A New Bullish Momentum

Gold is consolidating after the strong collapse even though traders are taking some profit. . Hourly support is given at 1236 (12/12/2017 low) . Resistance is located at 1259 (14/12/2017).

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

BITCOIN 20k On Target

Bitcoin's bullish momentum is far fom over. The technical structure has shown a tremendous positive short-term momentum. Hourly support is located below 14k (08/12/2017 low). Strong support stands very far at 2975 (22/08/2017 low). In the short-term, the digital currency should continue rising at levels unseen so far.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will reach $40'000 in 2018.

EUR/CHF Monitoring Uptrend Channel

EUR/CHF is testing support implied by the lower bound of the uptrend channel. Hourly resistance is given at 1.1737 (01/12/2017 high). Expected to show continued decline.

In the longer term, the technical structure has reversed. Strong resistance is given at 1.20 (level before the unpeg). Yet, the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

EUR/GBP Sideways Price Action

EUR/GBP is trading slightly lower. The pair is trading between support at 0.8689 (08/12/2017 low). Resistance is located at 0.8867 (05/12/2017 high). Expected to show further sideways trading.

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 (psychological level).