Sample Category Title

US Tax Reform Dominates Attention, Appetite For Risk Pushes Equities Higher

Here are the latest developments in global markets:

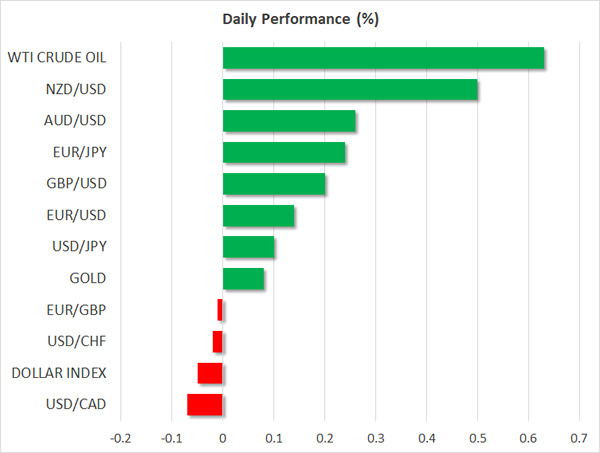

FOREX: The dollar was slightly down against a basket of currencies after posting gains on Friday following the announcement that House and Senate Republicans have found common ground on the front of tax legislation. The antipodeans were again gaining ground versus the greenback.

STOCKS: The Nikkei 225 added 1.55% and the Hang Seng was higher by 1.0% on a day when Asian equities were mostly on the rise on the back of positive sentiment following US tax reform momentum. Euro Stoxx 50 futures were up by 0.7% at 0725 GMT, while Dow, S&P 500 and Nasdaq 100 contracts traded higher by 0.45%, 0.3% and 0.4% respectively.

COMMODITIES: WTI and Brent crude were both up by 0.6%, at $57.66 and $63.63 per barrel respectively. Gold was slightly higher at $1,256.20 an ounce.

Major movers: Dollar not much changed as markets await tax vote; antipodeans on the rise

The dollar index was down, though not by much, trading at 93.87. Following the latest developments on tax reform, it looks increasingly likely that Congress will pass the relevant bill this week. The bill will subsequently be send to President Trump for it to be signed.

Dollar/yen was 0.1% higher at 112.68, though the US currency was losing some ground relative to the euro and the pound. Euro/dollar and pound/dollar traded up by 0.1% and 0.2%, at 1.1770 and 1.3345 respectively. Still, both pairs were at a distance to recently tracked highs.

Long-term Treasury yields not edging higher, at least not to a significant extent, also didn't allow the dollar to post stronger gains.

Towards the end of last week, Germany's Social Democrats agreed to get into talks with Merkel's Christian Democrats on forming a government. In the absence of anything concrete and given that talks are expected to begin with the start of the new year, eurozone's common currency didn't get much of a boost on the back of the news.

The antipodean currencies maintained last week's positive momentum, a week during which the aussie added 1.9% and the kiwi 2.2% versus the greenback. Aussie/dollar and kiwi/dollar were up by 0.3% and 0.5% on the day, at 0.7024 and 0.7667 respectively. The aussie was trading around one-month high levels and the kiwi around two-month high levels.

In emerging markets, dollar/rand retreated sharply on Friday – and was last trading close to Friday's low at 13.1268 – on relief that South African Deputy President Cyril Ramaphosa was likely to be nominated as the next chief of the African National Congress, South Africa's ruling party. Investors feared that Nkosazana Dlamini-Zuma, the ex-wife of South African President Jacob Zuma who was involved in numerous scandals, could be ANC's next leader and likely the country's next president after elections take place in 2019. Earlier in the day, dollar/rand fell below the 13 handle to record its lowest in three months.

Day ahead: May to propose plans on transition period; EU final inflation numbers ahead

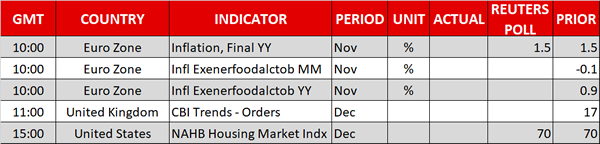

Eurozone's final inflation figures for the month of November due at 1000 GMT will be gathering attention, with analysts expecting consumer prices to keep growing below the ECB's target of 2.0%. Annually, headline CPI is anticipated to inch up by 0.1 percentage points to 1.5% y/y and remain flat on a monthly basis at 0.1% m/m.

December's industrial trends measured by the British CBI business organization will follow at 1100 GMT. Recall that in November, the index which tracks economic expectations of the manufacturing executives in the UK, surprisingly bounced by 19 points to +17, reaching its highest since 1988.

In other news out of the UK, the Prime Minister, Theresa May, who managed to break the deadlock in Brexit negotiations at the two-day EU summit in Brussels last week, will head to the British parliament on Monday to inform lawmakers about her latest talks with the EU and present her plans on the transition period which aim to limit a cliff-edge scenario for individuals and businesses after the country departs from the EU block.

In the US, eyes will be on the tax legislation as markets remain confident that the proposed-by- Republicans tax cuts will pass the Congress as soon as this Tuesday after the Senate and the House lawmakers added the final touches on tax overhaul on Friday. Furthermore, Republicans hope for the bill to be signed by the US President, Donald Trump, by the end of this week.

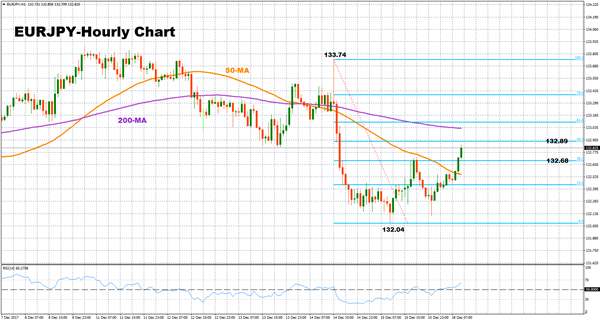

Technical Analysis: EURJPY bullish in the very short-term

EURJPY stretched to the upside on Monday, deviating from Friday's low of 132.10 and consequently painting a bullish picture in the very short-term. The RSI supports this view as the indicator is heading higher.

Better than expected inflation figures out of the eurozone could push prices towards 132.89 which is the 50% Fibonacci of the aforementioned downelg. From here steeper increases could also find strong resistance at the 133 key-level where the 200-day moving average and the 61.8% Fibonacci also lay.

On the downside, immediate support could emerge at the 38.2% Fibonacci at 132.68 before the current level of the 50-day MA at 132.54 and the 132 key-point come into view.

PBOC’s Rate Hike Is Consistent With The Deleveraging Theme That Would Be Reiterated At CEWC

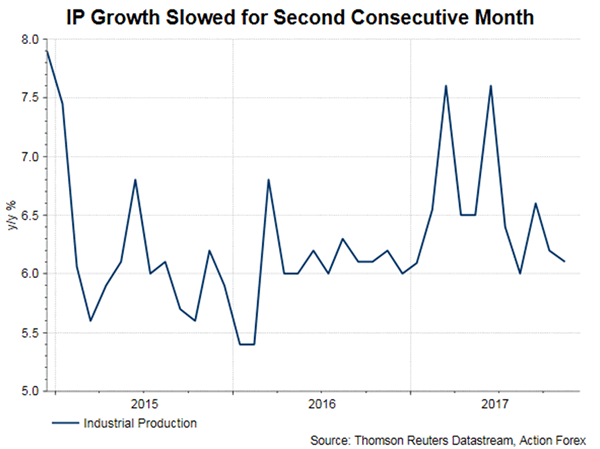

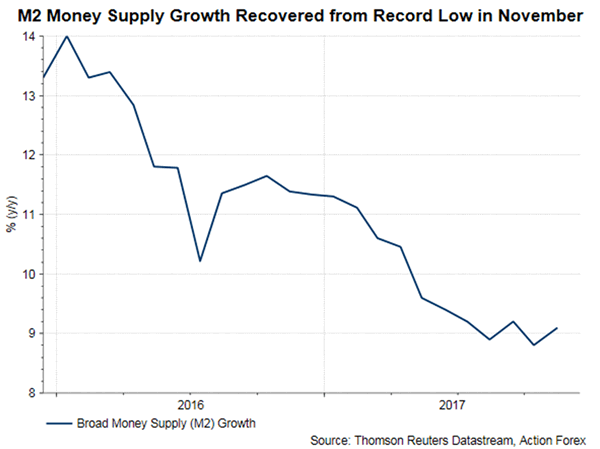

Overshadowed by a series of central bank meetings last week, China's macroeconomic data were mildly disappointing. Yet, this should not affect the country's growth to reach its full-year growth target of +6.5%. Indeed, the PBOC's monetary tightening on December 14, closely following the Fed's rate hike, is a manifestation that the government remains confident over the economic outlook. The three-day Central Economic Work Conference (CEWC) beginning today (December 18) would reveal China's economic policy and the closely-watched GDP growth target for 2018. We expect the politburo might revise lower the target from this year's +6.5%, and/ or adopt more flexibility in it language.

November Activity Data

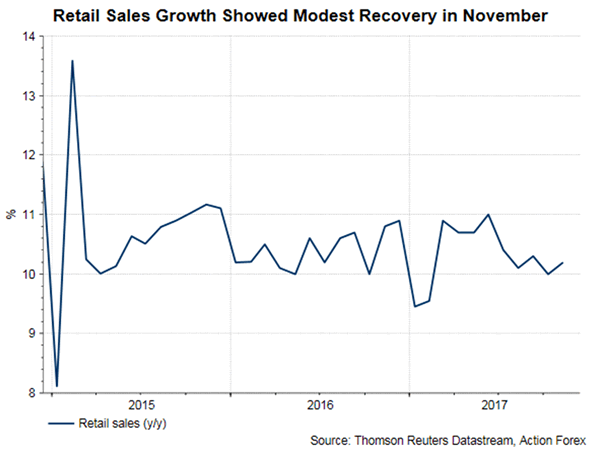

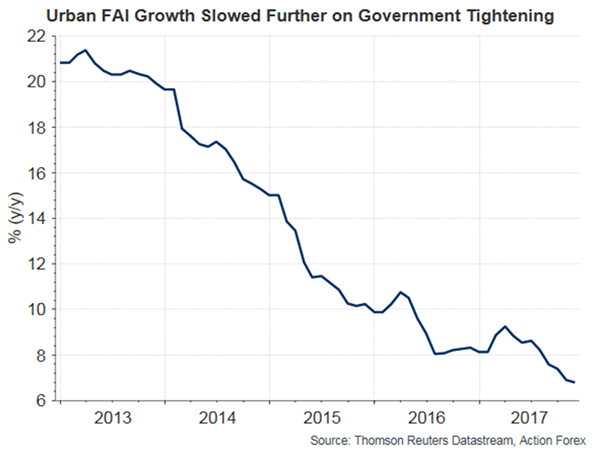

Industrial production (IP) expanded +6.1% y/y in November, weaker than consensus of, and October's, +6.2%. IP growth was weighed down by the anti-pollution campaign as northern China during the winter heating season. Retail sales rose +10.2% y/y in November, improving from +10% in October. However, this also missed expectation of +10.3%. Improvement in retail sales growth was undoubtedly helped the “double-11” festival, of which the effect was exemplified in the rebound in November PMIs (https://www.actionforex.com/action-insight/china-watch/60756-china-s-november-pmis-helped-by-double-11). Urban fixed asset investment (FAI) growth eased further to +7.2% y/y in the first 11 months of the year, compared with consensus of +6.2%. Growth was +7.3% in the first 10 months of the year. Deceleration in FAI growth has been the theme this year as the government cracks down property investment with the aim of deleverage. The moderation was further facilitated by the suspension of construction activities in northern China.

PBOC Rate Hike

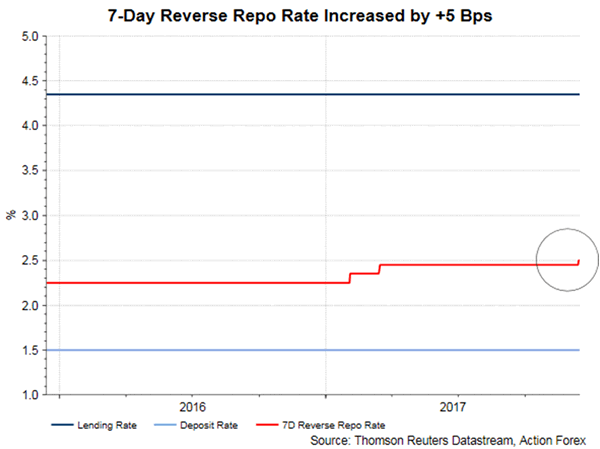

The PBOC lifted the 7-day and 28-day OMO reverse repo rates by 5 bps to 2.5% and 2.8% respectively. It also raised the 1-year MLF rates by 5 bps to 3.25%. These were in response to the Fed's 25-bps rate hike in the prior day. Note that the PBOC has raised the policy rates for three times this year. The previous two times were the 10-bps hikes in the OMO and MLF rates in February and March. As suggested in the accompanying statement, the rate hikes last week was partly driven by the Fed's rate hike. The PBOC stressed that it does not follow closely the monetary policy of the Fed, citing the inaction after Fed's June rate hike. More importantly, the rate hike was in response to the market rates which have been markedly higher than those guided by the central bank. Despite the fact that the rate hikes came in lower than consensus, PBOC believed that it would help discourage leveraging and excessive credit expansion (http://www.pbc.gov.cn/goutongjiaoliu/113456/113469/3440258/index.html).

Central Economic Work Conference (CEWC)

The annual Central Economic Work Conference would set the agenda for the economy of China and its financial and banking sector. Indeed, the theme of the agenda should echo what was announced in the 19th Party Congress in October and the 25-member politburo meeting last week. We believe the key policies should aim at reducing risks and deleveraging, eradicating poverty and preventing pollution.

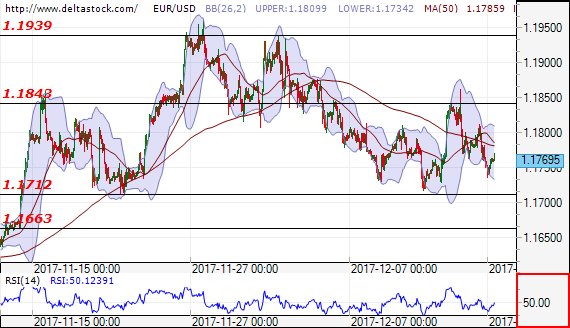

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.1769

The outlook is positive for test at 1.1843 and after that for another test of the next resistance level at 1.1939. In negative direction a breakthrough of the support level at 1.1712, may lead to test of the next support at 1.1663.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.1843 | 1.1939 | 1.1712 | 1.1663 |

| 1.1939 | 1.2090 | 1.1712 | 1.1550 |

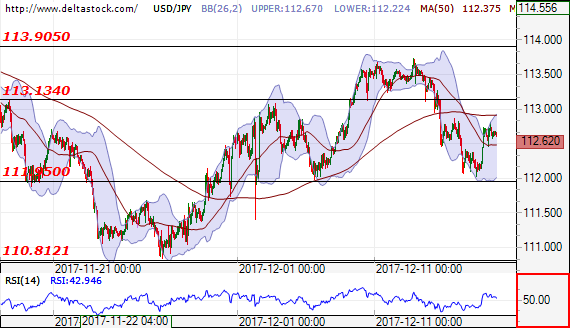

USD/JPY

Current level - 112.62

Although the unsuccessful breakthrough of the support level at 111.95, the outlook is negative for a test and breakthrough of the next support at 110.81.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 113.13 | 113.90 | 111.90 | 109.50 |

| 113.90 | 114.50 | 110.80 | 107.30 |

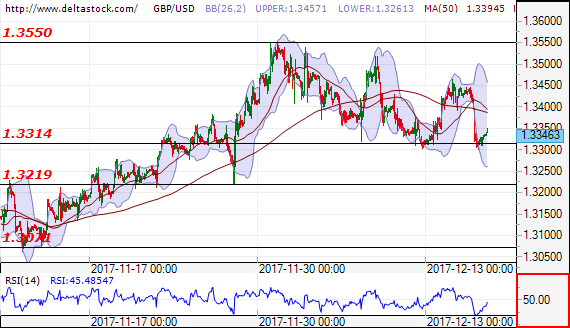

GBP/USD

Current level - 1.3346

After the unsuccessful breakthrough of the support level at 1.3314, the outlook is positive for test of the resistance level at 1.3550. In negative direction a breakthrough at 1.3314, may lead to the next support at 1.3219.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.3550 | 1.3660 | 1.3310 | 1.3220 |

| 1.3550 | 1.3660 | 1.3220 | 1.3070 |

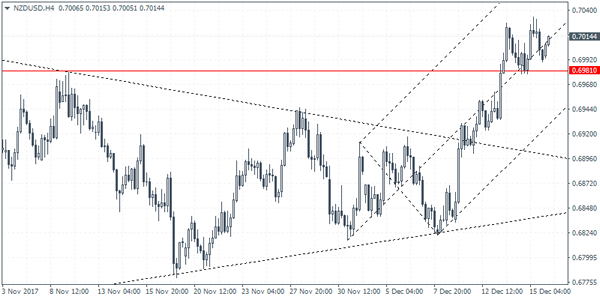

NZDUSD Intraday Analysis

NZDUSD (0.7014): The New Zealand dollar slipped last week but with price action supported above the 0.6981 level of support and minor higher low formed near the top, the bias remains to the upside. However, the double top pattern formed near the top could signal a downside breakout if the support level gives way. NZDUSD could be seen extending gains towards 0.7062 in the near term on a successful close above the double top pattern.

USDJPY Intraday Analysis

USDJPY (112.63): The USDJPY managed to close on a bullish note on Friday. Price action is currently looking a bit weaker with the lower high being formed. Further downside could be expected if the reversal fails to break past the previous high formed. On the 4-hour chart, the sideways range is established within 113.00 level of resistance and 112.04 level of support. We expect this range to be maintained with a breakout from this level expected to establish further direction in the near term.

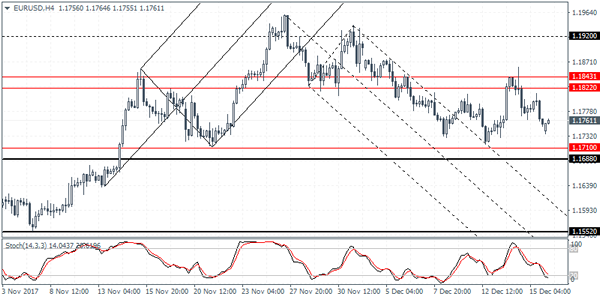

EURUSD Intraday Analysis

EURUSD (1.1761): The EURUSD gapped lower this morning, but price action was seen reversing the losses, filling up Friday's closing gap. Price action remains supported above the 1.1730 level of support. This suggests a potential near term upside in prices. However, with the resistance level established near 1.1843 - 1.1822, the gains might be limited to this level. Only a break out above this resistance will signal any further gains that could see EURUSD rally towards 1.1920 level of resistance. To the downside, the next support is seen at 1.1710 - 1.1688 level where the declines could be halted.

Dollar Maintains Gains, Vote On Tax Cuts Due On Tuesday

The U.S. dollar closed on Friday with some gains although there were no major economic releases scheduled. The U.S. House is expected to vote on the tax bill on Tuesday which will potentially bring out the much anticipated tax cut proposals. The deal is expected to lift the sentiment in the U.S. dollar as the markets head into the holiday season.

Looking ahead, the economic calendar for today is light. The Eurozone final inflation figures will be coming out. Eurozone inflation is expected to remain steady at 1.5% while core inflation is expected to rise 0.9% as per the initial estimates.

The U.S. trading session is quiet with only the NAHB housing market data on the agenda.

Hopes Of Early Christmas Gift Keeps Markets Elevated

Asian equities were mostly higher on Monday after Wall Street closed on record highs last Friday as the U.S. Congress seemed very close to passing a final bill that will reduce corporate taxes from 35% to 21%. The House and Senate are expected to vote on the bill by mid-week, before it goes to the White House for President Trump's signature. Trump tweeted "I promised we would pass a massive TAX CUT for the everyday working American families who are the backbone and the heartbeat of our country, now, we are just days away." If the bill is signed, it will be the first major legislative victory since he took office.

After details were released on Friday, U.S. companies labeled "Made in USA" will be the biggest beneficiaries of the new tax cuts - mainly oil refiners, airlines, and banks. Many corporates in this sector will see earnings boosted significantly, with some adding 30% to 2018. This is not only good news for these corporates but it also makes current overstretched valuations look more realistic. What will be interesting to see is whether asset managers will rotate heavily from multinational firms to more U.S.- based revenue companies, for the few remaining days of 2017.

The impact on the overall economy remains unknown. Many CEO's may choose to reward shareholders by increasing dividends and share repurchases, instead of expanding their businesses. That's probably why the dollar isn't responding very positively to the news.

Another explanation for the limited appreciation in the USD is the Treasury bond performance. US 10- year yields have been stuck in a range of 2.3% - 2.43% for two months, and if optimism isn't reflected in the fixed income space, I don't expect to see much appreciation in the currency, even after Mr. Trump signs the bill.

Sterling will remain in focus this week after the E.U. warned that the U.K. would be unable to renegotiate a new Brexit deal, if the Parliament votes to reject the one struck by Theresa May. May will meet her Brexit Cabinet today in an attempt to convince MPs to sign trade deals during the transition period. A positive outcome will likely lead to a relief rally in the pound, but given the loss in the Commons last week a soft Brexit seems to be at high risk.

Euro traders will keep a close eye on inflation data today. Consumer prices are expected to have risen by 0.1% in November. Given that the ECB has updated growth projections and latest PMI data pointed towards a stronger economy, inflation remains the missing ingredient. Any surprise, on the upside or downside will likely have a strong impact on EURUSD moves today.

EURUSD Daily Bearish Below 1.1787 Level

The euro currency continues to hold to the downside against the U.S dollar, with price-action still trading below major support as the new trading week begins. The EURUSD pair fell towards the 1.1737 level on Friday, as the U.S dollar index moved higher, following optimism that the Trump administrations new tax reform bill would be passed as early as this Tuesday. Investors now look to key November CPI inflation figures from the eurozone later today, and news updates coming from U.S politics.

The EURUSD pair remains intraday bearish while price-action trades below the 1.1787 level, price-action may find support from the 1.1750 and 1.1713 technical levels. Extended weekly support is found at the 1.1660 level.

Should the EURUSD pair start to move above the 1.1787 level, buyers may again start to target the 1.1813 and 1.1860 resistance levels.

GBPUSD Bears In Control Below 1.3360 Level

The British pound remains under selling pressure against the U.S dollar, after dropping sharply on Friday towards the 1.3300 support level. Pound sentiment faded quickly, following confirmation that the UK and EU Brexit negotiations will move to the next stage, in March 2018. Price-action has now recovered towards the 1.3330 area, with the GBPUSD pair holding 1.3300 support. Going forward, U.S Politics and global CPI figures are likely to be the main market movers for the pair this, as we head into the Christmas holiday period.

GBPUSD sellers retain control of the pair while price-action holds below the 1.3360 technical level. Downside targets for sellers remain the 1.3300 and 1.3267 levels.

Should price-action move above the 1.3360 technical level for a sustained period, further buying towards the 1.3400 level remains likely for the GBPUSD pair.