Sample Category Title

US Dollar Firm On Tax Plan Optimism

The US dollar received a boost thanks to increased optimism on Congress getting closer to passing the planned tax cuts. The US house of representatives are expected to vote on tax reforms on Tuesday and the Senate later in the week. If approved, Donald Trump should make it law by Christmas and that will make a nice present for US dollar bulls.

Later today, important Eurozone economic data are due out. Around 10:00 GMT the Eurozone final annualised consumer price index will be released. The inflation figure is expected to maintain the same growth as the previous figure of 1.5%. The final year on year Core CPI, which strips out the more volatile prices like food and energy, is also expected to come in at 0.9% which is in line with the previously announced figure of 0.9%.

What is otherwise a relatively quiet economic news day, we have at 11:00 GMT, the UK's industrial orders due for release with a forecast of 14 - previously it came out at 17. At 13:00 GMT Canada's international securities purchases report is due is which was previously 16.81 Billion. This may spell some volatility for the CAD which is closely linked to this indicator of foreign investor sentiment for both the Canadian economy and its dollar.

EUR/USD

The EUR/USD is under pressure and expected to continue its downside movement. The pair is capped by the descending 20-period moving average, which has crossed the 50-day moving average. The relative strength index is also moving below the neutrality level. 1.1812 (yesterday's high) is playing a major resistance role. As far as the price remains below the resistance level, expect a downward movement at 1.1717 (last week’s low) and 1.1670.

USD/CAD

The USD/CAD is expected to continue its upside movement. The pair accelerated on the upside and broke above its key resistance at 1.2815, which is a key support now. The 20- period moving average crossed above the 50- period moving average. The relative strength index is also bullish. To sum up, above 1.2815 look for new targets at 1.2893 (Friday's high) and 1.2909 (last month's high).

GBP/USD

The GBP/USD is under pressure and expected to continue the downside movement. The downside move is further accelerated by the declining 20 day and 50 day moving averages. The relative strength index is bearish and calls for a further decline. As long as 1.3350 is the resistance look for further drops towards 1.33016 (Friday's low) and 1.3265.

EURUSD Maintains Neutral Bias, Capped Below 50-Day Moving Average

EURUSD is neutral in a broad range between 1.1600 and 1.1900 since late September. The pair has been pivoting the 50-day moving average which is horizontal and indicative of a lack of clear direction in the market. The RSI is neutral around 50.

Near-term support appears to be holding at 1.1730 and limiting downside moves. Below this level dips are expected to find strong support at 1.1600.

The EURUS's outlook remains positive in the longer term as the uptrend from April to September (1.0820 to 1.2091) has not shown any signs of reversal yet, while the 50 and 200-day moving averages are bullishly aligned.

The consolidation phase that followed the peak at 1.2091 is expected to continue in the near term until the market retraces more than half of the April-September uptrend. EURUSD has only retraced 23.6% of this upleg and is trading just below this Fibonacci at 1.1792.

EURUSD has scope to extend higher towards 1.1900 and to re-test the November 27 high of 1.1960. But near-term momentum is weak. Consequently, the neutral bias is expected to remain intact in the short-term unless prices break above the 50-day MA.

Forex: US Tax Bill Moves Closer To Being Made Law

USD strengthened on reports that the US Tax Bill is moving closer to being ratified. Many top Republicans are confident that Congress will pass the Tax Bill this week. Once the Senate ratifies the bill, which could happen as early Tuesday, President Trump could sign and bring the Bill into law by the end of the week. However, as with most things in politics, there is a degree of concern in the markets that things may not go as smoothly as hoped. With a slim 52-48 Senate Republican majority there are some Republicans that still need to be 'swayed' to ensure the bill does indeed get approved. With the bill reducing corporation tax from 35% to 21%, there will be a windfall to US companies. With the possibility of share buy-backs and/or higher dividends by US Corporations, this will, in turn, increase the pace of interest rate hikes and see a stronger USD as a result.

UK Prime Minister Theresa May is scheduled to meet her 'Brexit Cabinet' to discuss what the UK's future relationship with the European Union should be. Recently EU leaders agreed that discussions can continue to phase 2 of Brexit. Phase 2, however, that will involve discussions on long-term future economic co-operation, is not likely to begin until March, although 'internal preparatory discussions' on future relations can take place prior to March. Phase 2 will pose the question of a future trading relationship that will involve forging agreement among 27 countries whose economic and political interests will diverge, depending upon the depth and character of their commercial and diplomatic ties to Britain. With the UK PM facing internal opposition and so many questions that remain unanswered GBP has faltered, with GBPUSD dropping nearly 1% on Friday before stabilizing just above 1.33.

President Trump is scheduled to deliver a national security speech on Monday that may 'point a finger' at certain countries attempts of economic aggression towards the US. Such comments tend to 'stoke the fire' and result in further rhetoric that can cause market volatility.

EURUSD is 0.15% higher in early Monday trading at around 1.1762.

USDJPY is little changed from Friday trading at around 112.65.

GBPUSD is 0.2% higher in early session trading at around 1.3340.

Gold is unchanged in early trading at around $1,255.50.

WTI is little changed, trading around $57.43.

Major data releases for today:

At 10:00 GMT: Eurostat will release Eurozone CPI and CPI Core month-on-month and annualized for November. Annualized: Core is forecast to see an increase to 1.0% from October's reading of 0.9% and CPI is forecast to remain unchanged at 1.5%. Month-on-Month: Core is forecast higher at 0.2% from the previous reading of -0.1% and CPI is forecast to be unchanged at 0.1%. Any significant deviation from forecast will see EUR volatility.

Russia’s Central Bank (CBR) Delivered Surprise Cut Of 50Bps To 7.75% On Friday

Market movers today

The main events this week will be the Riksbank meeting this Wednesday and the Bank of Japan meeting on Thursday.

On the data front , we start the week with a very light day.

In the euro area, note that the revised inflation figures for November are also due to be released today.

Furthermore, in South Africa, the election of the new leader of the ANC may take place, which is already having a great bearing on the South African financial assets and the ZAR.

Selected market news

The final details of the US tax overhaul were revealed on Friday. The Republican tax plan cuts the corporate tax rate to 21% on a permanent basis, while offering temporary cuts to individuals. The tax plan is expected to be voted through Senate by Tuesday and signed by President Donald Trump by the end of the week, before entering into force by February. According to the Joint Committee on Taxation (JCT), the reform will raise economic growth of about 0.8% over the next ten years. However, according to the JCT's estimate (link), this will only cover about a third of the cost , which means that the reform will add at least USD1trn to the USD20trn national debt over next decade. The plan could also boost US corporate earnings by some 10% on average, with oil refiners, airlines and banks among the main beneficiaries, according to Financial Times.

Expected passage of tax plan lifts equity markets. On Thursday, concerns about the tax plan passing this year weighed on stocks as not all Republican senators had committed to supporting it . However, on Friday there seemed to be full backing for the deal with all 52 Senate Republicans in support. This lifted US stocks, with S&P rising 0.9% and the gains have carried over to Asian trading this morning.

Fitch upgrades Ireland and Portugal on Friday. Ireland was upgraded by one notch to ‘A+', while Portugal's sovereign rating was raised two not ches to ‘BBB'. Please see the Fixed Income section for details.

Russia's central bank (CBR) delivered surprise cut of 50bps to 7.75% on Friday. Together with the market and Bloomberg consensus, we unanimously expected a 25bp cut . Yet , prior to the decision we pointed out that a 50bp cut would likely mean increasing hidden pressure on the CBR ahead of the presidential election as the central bank has stayed conventionally overcautious and hawkish despite falling inflation. We expect the CBR to cut its key rate gradually to 6.75% by end-2018 (previously 7.00%). As an init ial react ion the USD/RUB spot jumped slight ly higher and rates dropped a bit . After a while, RUB was stronger against the USD and rates were almost at the same level as they were before the surprise cut . We expect high real rates to prevail in Russia in 2018, being one of the supporting factors for the RUB.

Market Update – Asian Session: China Home Prices Stable In Nov, Australia Updates Outlook

Headlines/Economic Data

General Trend: Asian equities opened higher following Friday’s gains in the US, amid optimism related to tax reform

CME Bitcoin Futures opened at $20,650 and traded ~80 contracts in the first 15 minutes of trading

Japan

Nikkei 225 opened +1%; closed +1.6%

Financials track Friday’s gains in the US: Mitsubishi UFJ +2.7%, Sumitomo Mitsui +1.6%, Mizuho +1.6%

Japan pension fund GPIF said to consider absorbing the costs of negative interest rates – Japanese Press

Toyota +2.7% (seeking to sell more than 5.5M e-vehicles)

Tokyo Steel: -2.6% (follow-through selling; announced plans to raise steel prices for Jan)

JAPAN NOV TRADE BALANCE: ¥113.4B V -¥40.0BE; ADJ ¥364.1B V ¥265BE; Exports y/y: 16.2% (12th straight rise) v 14.7%e; Imports y/y: 17.2% v 18.0%e

Japan BOJ Tankan Dec survey of all firms inflation expectations: Raises 1-yr 0.8% y/y (prior 0.7%); Affirms 3-yr 1.1% y/y; Affirms 5-yr 1.1% y/y

Japan govt reportedly planning FY2018/19 annual general account budget spending at ¥97.7T, a record level - press

Japan Fin Min confirms FY18 budget assumes record low interest rate of 1.1% - Japanese Press (in line with press speculation from Dec 12th)

Japan is expected to approve its budget draft on Friday, Dec 22nd

Looking ahead: 10-year JGB auction due to be held on Tuesday; The BoJ is due to hold its two-day policy meeting on Dec 20-21st (Wed and Thursday)

Korea

Kospi opened +0.3%, has since pared gains

Steelmakers decline: Posco -1.9%, Hyundai Steel -3.7%

Financials trade generally lower: Woori Bank -0.8%, KB Financial -1.3% Shinhan Financial -0.2%

Kakao Corp -3% (to list shares in Singapore)

South Korea sells 20-yr Govt bond at 2.405%

Bank of Korea (BOK) sells KRW400B in 6-month monetary stabilization bonds at 1.66%

South Korea is monitoring North Korea in relation to its cryptocurrency moves; **Note: On Dec 15th, South Korea's Yonhap reported that North Korea was linked to cryptocurrency hacking that occurred in Sept.

(KR) South Korea President Moon’s Economic Advisor to meet with 8 largest companies in the country

China/Hong Kong

Shanghai Composite opened +0.1%, Hang Seng +0.3%

Hang Seng Materials Index +0.9%

(CN) China Ministry of Finance: To lower import taxes on products including cathode materials for power batteries, raw materials for advanced medicine, dobby or jacquard looms and coconut fibre; Export duties on steel and chlorite to be scrapped, effective Jan 1st

(CN) China Former PBoC Economist Ma proposed removing GDP target – Chinese Press

(CN) China NDRC issues guidelines on overseas investments by private companies; Asks companies to increase risk control, set up contingency plans, improve safety measures

(CN) China to offer tax cuts to state-owned enterprises (SOEs) related to environmental protection and public infrastructure

(CN) President Trump national security strategy said to accuse China of “economic aggression”, labeling it as a competitor and a threat - financial press; This would be the most aggressive economic response to China since 2001.

(CN) Wind data shows in 2017 China completed 4,018 M&A deals worth CNY1.51T v 2,998 deals with value of CNY1.7T y/y - Xinhua

PBoC raised the yield on 28-day reverse repo by 5bps; (**Note: Following last Wednesday’s Fed rate hike, the PBoC raised interest rates on its 7-day and 28-day reverse repo operations by 5bps. It also raised the rate on its 1-year medium-term lending facility by 5bps)

PBoC OMO: CNY300B in 7,14 and 28-day reverse repos v CNY150B injected in 7 and 28 day reverse repos prior; Net injected CNY260B v CNY150B prior

(CN) CHINA NOV PROPERTY PRICES M/M: RISES IN 50 OUT OF 70 CITIES V 50 PRIOR; Overall new home prices m/m: +0.3% v 0.3% prior; y/y: 5.1% v 5.4% prior

(CN) PBoC does not need to follow US to raise interest rates – China Daily

(CN) PBoC sets yuan reference rate at 6.6162 v 6.6113 prior

(CN) Reminder today is the first day of Central Economic Conference held from 18th to 20th

(CN) PBoC does not need to follow US to raise interest rates – China Daily

Australia/New Zealand

ASX 200 opened -0.2%; closed: Resources index +0.8%, Financials +0.6%, banks recovered amid a favorable move in yields

(AU) Australia Govt 2017/18 Mid-Year Economic & Fiscal Outlook Australian government 2017/18 Mid-Year Economic & Fiscal Outlook: Cuts 2017/18 GDP at 2.5% from 2.75% in May; Affirms 2017/18 CPI 2.0%; Cut wage growth forecasts for 2017/18 and 2018/19

(AU) Australia Treasurer Morrison: Commitment to corporate tax cuts remains unchanged; do not see upside risks to GDP growth forecasts

(AU) Moody’s: Affirms Australia AAA sovereign rating; Outlook Stable

(AU) RBA releases paper: Monetary Policy and Financial Stability in a World of Low Interest Rates

(NZ) New Zealand Nov Performance of Services Index: 56.4 v 55.6 prior

(NZ) New Zealand Dec ANZ Consumer Confidence Index: 121.8 v 123.7 prior; m/m: -1.5% v -2.1% prior

ACX.AU To be acquired by Oracle for A$7.80/shr in cash; +44%

RAP.AU Announces further positive results from Australian adult clinical studies; +30%

Looking ahead: Reserve Bank of Australia (RBA) Dec meeting minutes due on Tuesday, along with New Zealand Q4 Westpac Consumer Sentiment and ANZ Dec Business Confidence

Other Asia

(IN) Indian assets opened sharply lower amid close elections in the Gujarat State; Equities later pared losses amid indications that PM Modi’s BJP Party is expected to win

(SG) SINGAPORE NOV NON-OIL DOMESTIC EXPORTS M/M: 8.7% V 0.6%E; Y/Y: 9.1% V 6.4%E; ELECTRONIC EXPORTS Y/Y: 5.2% V 5.2%E

North America

Tax Reform: (US) Senator Rubio (R-FL): Confirmed he would now support the tax bill (comments from Dec 15th)

(US) Sen Corker (R-TN): will support GOP tax reform bill (comments from Dec 15th)

(US) Spokesperson for US Senator McCain (R): Senator to return to D.C in Jan (to miss Senate vote on tax bill)

(US) The White House and Senate Majority Leader McConnell are said to have been planning for the possibility that McCain might miss the tax vote, making Republic Senator Corker's announcement on Friday that he would support the plan as 'critical', said a CNN article.

(US) House Majority Leader McCarthy (R): House to vote on tax bill on Tuesday (Dec 19th)

(US) US Senate Majority Leader McConnell (R): Senate will get tax bill ‘done’ next week (comments from Friday)

Politics: (US) President Trump's private lawyers to meet with special counsel Robert Mueller as soon as next week – CNN; The President's lawyers consider this an opportunity to get a clearer understanding of the next steps in Russia probe

M&A: Snyders Lance: Campbell Soup reportedly in late stage talks to buy Snyder's-Lance; deal could be announced as soon as next week - CNBC

Equinix: To acquire Australia data center business Metronode for A$1.035B in cash

VIPS Tencent, JD.com invest $863M Equity Investment and Business Cooperation in VipShop

Europe

(UK) Chancellor of Exchequer Hammond (Fin Min): UK and China have agreed to accelerate preparations for London/Shanghai stock connect initiative

(AT) Austria People's Party Leader Kurz and Freedom Party said to have agreed to form a govt - Austria press

(UK) Canadian ratings agency DBRS affirms UK sovereign debt rating at AAA, stable

(PT) Fitch raises Portugal sovereign rating to investment grade from junk; raises two notches to BBB from BB+; outlook Stable from Positive (from Dec 15th)

(IE) Fitch raises Ireland sovereign rating one notch to A+ from A; outlook Stable (from Dec 15th)

M&A: Gemalto: Thales agrees to pay €51/share in cash or ~€4.8B to acquire the company

Levels as of 01:00ET

Nikkei225 +1.6%, Hang Seng +0.7%; Shanghai Composite -0.1%; ASX200 +0.7%, Kospi -0.0%

Equity Futures: S&P500 +0.2%; Nasdaq100 +0.3%, Dax +0.3%; FTSE100 +0.1%

EUR 1.1765-1.1738; JPY 112.83-112.48; AUD 0.7661-0.7641;NZD 0.7017-0.6989

Feb Gold +0.1% at $1,258/oz; Feb Crude Oil +0.2% at $57.44/brl; Mar Copper -0.6% at $3.12/lb

Daily Wave Analysis: EUR/USD Bearish Break To Challenge 61.8% And 78.6% Fib Levels

Currency pair EUR/USD

The EUR/USD bearish break below the support trend line (dotted blue) makes it likely that price will challenge the Fibonacci levels of wave 2 (pink). A break below the 100% Fib level of wave 2 vs 1 invalidates the wave 2 (pink) and indicates an expansion of wave 4 (light purple).

The EUR/USD indeed bounced at the support trend line but the rally turned at the Fibonacci levels of wave B (blue) as expected in last week's analysis. The bearish breakout could be part of wave C (blue).

Currency pair GBP/USD

The GBP/USD is retesting the support zone (blue lines), which could lead to price making a bullish bounce again. There is also a 50% and 61.8% Fibonacci of wave 4 vs 3 (brown) that could provide support.

The GBP/USD broke below the support trend line (dotted green) and fell again to the Fibonacci levels of wave 4. A break below the 61.8% makes a wave 4 less likely.

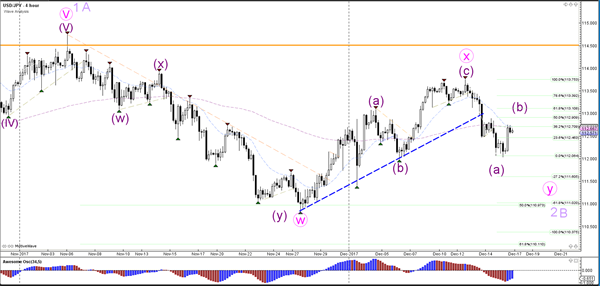

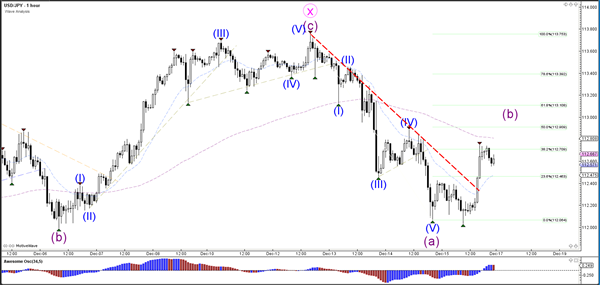

Currency pair USD/JPY

The USD/JPY indeed made a bullish bounce after reaching 112. The price action could be part of a wave B (purple) as price extends its bearish correction towards 111 and 110. A break above the 100% Fib level at 113.75 invalidates the ABC zigzag.

The USD/JPY is respecting the 38.2% Fib but could extend the correction to higher Fibs before making a bearish bounce.

Aussie Dollar Trading On A Stronger Footing In The Asian Session

For the 24 hours to 23:00 GMT, the AUD declined 0.14% against the USD and closed at 0.7649 on Friday.

LME Copper prices rose 0.2% or $12.5/MT to $6735.5/MT. Aluminium prices rose 0.9% or $19.0/MT to $2036.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7660, with the AUD trading 0.14% higher against the USD from Friday’s close.

The pair is expected to find support at 0.7634, and a fall through could take it to the next support level of 0.7607. The pair is expected to find its first resistance at 0.7691, and a rise through could take it to the next resistance level of 0.7721.

Looking forward, market participants would keep a close watch on minutes of the Reserve Bank of Australia’s (RBA) December monetary policy meeting, due overnight.

The currency pair is showing convergence with its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Trade Surplus Declined To A 3-Month Low In October

For the 24 hours to 23:00 GMT, the EUR declined 0.09% against the USD and closed at 1.1756 on Friday, after the Euro-zone's seasonally adjusted trade surplus narrowed to a three-month low of €19.0 billion in October, amid a drop in exports and a rise in imports. In the previous month, the region had posted a revised trade surplus of €24.5 billion, while markets had expected for a fall to €24.3 billion.

The greenback gained ground against a basket of major currencies on Friday, amid growing expectations that US lawmakers will pass a long-awaited tax bill before the year-end.

On the macro front, industrial production in the US advanced 0.2% on a monthly basis in November, undershooting market consensus for an increase of 0.3%, as gains in the mining sector were offset by a fall in utilities output. Industrial production had registered a revised rise of 1.2% in the prior month. Moreover, the nation's manufacturing production grew less-than-expected by 0.2% on a monthly basis in November, against market anticipations for an advance of 0.3%. Manufacturing production had registered a revised rise of 1.4% in the previous month.

Other data indicated that the New York Empire State manufacturing index eased more-than-anticipated to a level of 18.0 in December. In the prior month, the index had registered a level of 19.4, while markets had expected for a fall to a level of 18.7.

In the Asian session, at GMT0400, the pair is trading at 1.1763, with the EUR trading 0.06% higher against the USD from Friday's close.

The pair is expected to find support at 1.1730, and a fall through could take it to the next support level of 1.1697. The pair is expected to find its first resistance at 1.1804, and a rise through could take it to the next resistance level of 1.1845.

Going ahead, investors would eye the Euro-zone's final inflation numbers for November, slated to release in a few hours. Moreover, the US NAHB housing market index for December, due to release later in the day, will be on investors' radar.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

EU Leaders Agreed To Move To Second Phase Of Brexit Talks

For the 24 hours to 23:00 GMT, the GBP declined 0.76% against the USD and closed at 1.3322 on Friday, after the European Union (EU) leaders agreed to move on to the second phase of Brexit negotiations, but warned that the second phase will be significantly harder than the first.

In the Asian session, at GMT0400, the pair is trading at 1.3336, with the GBP trading 0.11% higher against the USD from Friday’s close.

The pair is expected to find support at 1.3277, and a fall through could take it to the next support level of 1.3217. The pair is expected to find its first resistance at 1.3421, and a rise through could take it to the next resistance level of 1.3505.

Going ahead, traders would look forward to UK’s CBI industrial trends total orders for December, slated to release in a few hours.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Japan’s Adjusted Merchandise Trade Surplus Unexpectedly Widened In November

For the 24 hours to 23:00 GMT, the USD rose 0.19% against the JPY and closed at 112.59 on Friday.

In the Asian session, at GMT0400, the pair is trading at 112.69, with the USD trading 0.09% higher against the JPY from Friday's close.

Overnight data revealed that Japan's adjusted merchandise trade surplus surprisingly widened to ¥364.1 billion in November, against expectations for it to narrow to a level of ¥265.0 billion. The nation had registered a revised adjusted merchandise trade surplus of ¥349.3 billion in the prior month.

Additionally, the nation's exports rose more-than-anticipated by 16.2% on an annual basis in November, pointing to robust overseas demand. Exports had risen 14.0% in the previous month, while markets were expecting for a gain of 14.7%. Meanwhile, the nation's imports grew less-than-expected by 17.2% YoY in November, after recording a rise of 18.9% in the previous month and compared to market consensus for an advance of 18.0%.

The pair is expected to find support at 112.20, and a fall through could take it to the next support level of 111.72. The pair is expected to find its first resistance at 113.00, and a rise through could take it to the next resistance level of 113.32.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.