Sample Category Title

AUD/USD Pushing Higher

AUD/USD's upside pressures are growing. Hourly resistance is given at a distance at 0.7695 (15/12/2017 high). Support stands at 0.7502 (08/12/2017 low). Expected to push even higher.

In the long-term, the trend is turning positive. Key supports stands at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8164 (14/05/2015 high) is needed to invalidate our long-term bearish view.

USD/CAD Monitoring 1.29

USD/CAD is testing hourly resistance at 1.2917 (27/10/2017 high). Expected to show continued buying pressures.

In the longer term, the pair has broken longterm support that can be found at 1.2461 (16/03/2015 low). Strong resistance is given at 1.4690 (22/01/2016 high). The pair is likely to head further lower.

USD/CHF Riding Downtrend Channel

USD/CHF is trading lower. Yet, the technical structure indicates further downside risks. The pair has failed to hold consistently above the parity. Expected to go even lower.

In the long-term, the pair is still trading in range since 2011 despite some turmoil when the SNB unpegged the CHF. Key support can be found 0.8986 (30/01/2015 low). The technical structure favours nonetheless a long term bullish bias since the unpeg in January 2015.

USD/JPY Ready For Another Leg Lower

USD/JPY is ready to push lower. Hourly resistance is given at 113.75 (12/12/2017 high) while hourly support is given at 112.03 (15/12/2017 low). The technical structure suggests further weakness.

We favor a long-term bearish bias. Support is now given at 99.02 (10/08/2013 low). A gradual rise towards the major resistance at 125.86 (05/06/2015 high) seems unlikely. Expected to decline further support at 93.79 (13/06/2013 low).

GBP/USD Riding Short-Term Downtrend Channel

GBP/USD continues to move lower within downtrend short-term channel. The technical structure indicates further weakness. Support is given at a distance at 1.3302 (15/12/2017 low).

The long-term technical pattern is reversing. The Brexit vote had paved the way for further decline. Long-term support can be found at 1.1841 (07/10/2017 low). Long-term resistance given around 1.35 is at stake and indicates a long-term reversal in the negative trend. Yet, it is very unlikely at the moment.

EUR/USD Consolidating Above 1.1700

EUR/USD's short-term bearish momentum has abruptly ended. Hourly resistance is given at 1.1961 (27/11/2017 high). Hourly support given at 1.1718 (12/12/2017 low). Expected to show sideways price action.

In the longer term, the momentum is now turning largely positive. We favour a continued bullish bias. Key resistance is holding at 1.2252 (25/12/2014 high) while strong support lies at 1.0341 (03/01/2017 low).

Market Update – European Session: Voting Said To Be Close In South Africa Ruling ANC Party Leadership Race

Notes/Observations

US Tax reform poised to be enacted as votes secured for its passage in Congress

PM May to meet with her Brexit committee to determine the shape of the future EU-UK trade deal

Awaiting outcome of South Africa ruling ANC party leadership elections (two presidential candidates are Nkosazana Dlamini-Zuma and Cyril Ramaphosa)

Catalonia's upcoming elections on Thurs, Dec. 21st probably be no new attempt to split off Catalonia from Spain for the time being

Asia:

PBoC raised the yield on 28-day reverse repo by 5bps; (**Note: Following last Wednesday’s Fed rate hike, the PBoC raised interest rates on its 7-day and 28-day reverse repo operations by 5bps. It also raised the rate on its 1-year medium-term lending facility by 5bps)

President Trump to lay out new US national security strategy on Monday, Dec 18th and to be based on “America First” policy and will make clear that China was a competitor (would be the most aggressive economic response to China since 2001.

Australian government 2017/18 Mid-Year Economic & Fiscal Outlook: Cuts 2017/18 GDP from 2.75% to 2.5%

Moody’s affirmed Australia AAA sovereign rating; Outlook Stable

Europe:

German SPD’s Schulz said to wants party to claim Finance Ministry position in possible coalition negotiations with Merkel

Austria People's Party Leader Kurz and Freedom Party agreed to form a govt which would be sworn in on Monday, Dec 18th

France Fin Min Le Maire: French Govt will continue to cut public spending; French deficit will be less than 3% in 2018

France Financial Stability Council: plans to limit systemic banks exposure to highly indebted large companies to 5% of bank capital

Chancellor of Exchequer Hammond (Fin Min): UK and China have agreed to accelerate preparations for London/Shanghai stock connect initiative. To also study feasibility of a bond market connect

PM May will meet with her Brexit cabinet to discuss for the 1st time what the UK’s future relationship with the EU should be

UK Foreign Sec Johnson said to have called for a “liberal Brexit” because the advantages of leaving have not been properly outlined to the public

Fitch raised Portugal sovereign rating to investment grade from junk; raises two notches to BBB from BB+; outlook Stable from Positive

Fitch raised Ireland sovereign rating one notch to A+ from A; outlook Stable

Canadian ratings agency DBRS affirmed UK sovereign debt rating at AAA, outlook stable

Americas:

Congressional Conference Committee released final text of tax reform bill. Corporate tax rate cut to 21% effective in 2018 (did not sunset). Pass through deduction set at 20% (raised from 17.4% currently). Did not include a corporate AMT; individual AMT remained but exemptions raised to $500K for individuals and $1M for couple. Seven individual tax bracket remain but some are reduced including top tax rate cut to 37% (down from 39.6% currently). Individual tax cuts expired in 2025. Standard Deduction is approx doubled (to $12K individual and $24K married) and personal exemption is repealed

Senator Rubio (R-FL) confirmed he would now support the tax bill; Sen Corker (R-TN) to also support GOP tax reform bill

(US) Spokesperson for US Senator McCain (R): Senator to return to D.C in Jan (to miss Senate vote on tax bill)

Economic Data:

(ES) Spain Q3 Labour Costs Y/Y: +0.4% v -0.2% prior

(CZ) Czech Nov PPI Industrial M/M: -0.1% v +0.3%e; Y/Y: 0.9% v 1.3%e

(HK) Hong Kong Nov Unemployment Rate: 3.0% v 3.0%e

(IT) Italy Oct Trade Balance: €5.0B v €2.8B prior; Trade Balance EU: €0.7B v €0.2B prior

(EU) Euro Zone Nov Final CPI Y/Y: 1.5% v 1.5%e; CPI Core Y/Y: 0.9% v 0.9%e

Fixed Income Issuance:

(NO) Norway sold NOK6.0B vs. NOK6.0B indicated in 12-month Bills; Avg Yield: 0.28% v 0.42% prior; Bid-to-cover: 1.90x v 2.31x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 +0.8% at at 391.2, FTSE +0.3% at 7512, DAX +1.2% at 13258, CAC-40 +1.2% at 5413, IBEX-35 +0.7% at 10217, FTSE MIB +0.8% at 22274, SMI +0.3% at 9425 , S&P 500 Futures +0.3%]

Market Focal Points/Key Themes:

European Indices start the weak on the front foot, trading higher across the board, with trading near 6 week highs, with optimism over the US tax plan continuing to prop global markets. The banking sector outperforms along with Technology, Autos and construction.

In the M&A space, Gemalto trades higher after accepting a €51/shr offer from Thales, while Buwog is to be acquired by Vonovia in a €4.8B deal and Unilever sells its Spreads business to KKR for over $7B. In the US shares of Amplify Snacks trade higher in the premarket after its reportedly to be acquired by Hershey for $12/shr, and Campbell Soup is reportedly in late stage talks to acquire Snyder Lance. Brokerage firms IG, Plus500 and CMC trade sharply lower after the ESMA proposes actions to improve protection for retail clients.

Equities

Consumer Discretionary [SRP [SRP.FR] -21% (Cuts Q4 outlook),

Financials [IG Group [IGG.UK] -10%, Plus500 [PLUS.UK] -15%, CMC Markets [CMCX.UK] -13% (ESMA announcements), Buwog [BWO [BWO.AT] +15% (to be acquired)

Industrials [Assa Abloy [ASSAB.SE] +2.7% (New CEO)]

Technology [Gemalto [GTO.NL] +5.5%, Thales [HO.FR] +8% (Thales to acquire Gemalto for €51/shr)]

Healthcare [Biom'UP [BUP.FR] +7.3% (FDA marketing approval)]

Speakers

ECB's Liikanen (Finland) Strong economic recovery supported Euro Area inflation. ECB policy assumed to be easy until 2020 (in-line with Staff forecasts)

ECB's Villeroy: France unemployment rate to decline in 2019; PM Macron's reforms go in the right direction

Czech Central Bank (CNB) to raise its Counter-Cyclical Buffer Rate to 1.25%from 1.00%; effective in Jan 2019

Poland Central Bank's Zubelewicz: 2018 CPI seen averaging 2.0% (**Note: Poland has 2.5% target)

Poland Development Min Kwiecinski: Poland making own economy less reliant on EU funds. Tensions with EU affected talks on future funding. Brexit could have impact on EU budget flows. Saw Polish Q4 GDP pace being similar to the Q3 rate of 3.9% y/y

Indonesia Fin Min Indrawati saw relatively good GDP growth of 5.3% in 2018 supported by global recovery

Currencies

USD was mixed against the major as tax reform bill moved closer to ratification. EUR/USD higher by 0.3% but holding below the 1.18 level. USD/JPY higher by 0.1% at 112.60 area.

South African rand was adding to its Friday's 3% gain ANC party was poised to announce its next leader. Hopes that business-friendly candidate and current deputy President Cyril Ramaphosa would win

Fixed Income

Bund futures trade 163.44 down 16 ticks, and continuing to respect the November highs. Continued upside sees 163.63 then 164.25. A reversal targets 162.50 then 162.38. Portuguese government bonds outperform the rest of the market in early trade Monday, after Fitch Ratings on Friday upgraded the country to investment grade, a move widely anticipated by the market.

Gilt futures trade at 126.49 down 2 ticks near the mid-point for the 2017 trading range. Continued upside eyeing 126.75 then 127.25. Downside targets include 125.75 then 125.24.

Monday’s liquidity report showed Friday's use of the marginal lending facility fell to €124M from €203M prior.

Corporate issuance - Primary expected to close for the year

Looking Ahead

(BR) Brazil Dec CNI Consumer Confidence: No est v 101.0 prior

(BR) Brazil Dec CNI Industrial Confidence: No est v 56.5 prior

(CO) Colombia Nov Consumer Confidence: No est v -10.6 prior

(SA) Saudi Arabia Oct Oil Production: No est v 9.973M in Sept – JODI

05:25 (BR) Brazil Central Bank Weekly Economists Survey

05:30 (BR) Brazil Oct Economic Activity Index (monthly GDP) M/M: 0.0%e v 0.4% prior; Y/Y: 2.8%e v 1.3% prior

06:00 (UK) Dec CBI Industrial Trends Total Orders: 15e v 17 prior

06:45 (US) Daily Libor Fixing

08:00 (PL) Poland Nov Employment M/M: 0.1%e v 0.1% prior; Y/Y: 4.4%e v 4.4% prior

08:00 (PL) Poland Nov Average Gross Wages M/M: 1.1%e v 2.3% prior; Y/Y: 7.0%e v 7.4% prior

08:05 (UK) Baltic Dry Bulk Index

08:30 (CA) Canada Oct Int'l Securities Transactions (CAD): No est v 16.8B prior

08:55 (FR) France Debt Agency (AFT) to sell combined €3.3-4.5B 3-month and 6-month BTF Bills

09:00 (BE) Belgium Dec Consumer Confidence: No est v 3 prior

09:30 (EU) ECB announces Covered-Bond Purchases

09:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tender

10:00 (US) Dec NAHB Housing Market Index: 70e v 70 prior

10:00 (CO) Colombia Oct Trade Balance: -$0.6Be v -$0.3B prior; Imports: $3.9Be v $3.7B prior

11:30 (US) Treasuries to sell to 3-month and 6-month bills

16:00 (US) Weekly Crop Progress Report

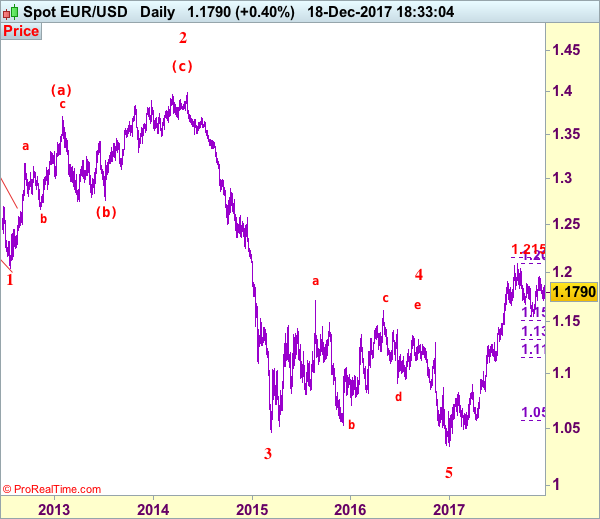

EUR/USD Elliott Wave Analysis

EUR/USD – 1.1790

EUR/USD: Wave (c) of 2 ended at 1.3993 and wave 3 of III has commenced for weakness to 1.0411 (1.236 of wave 1), then 1.0000.

The single currency met resistance at 1.1863 last week and has retreated, retaining our view that further consolidation below resistance at 1.1961 would be seen and test of support at 1.1713-17 cannot be ruled out, however, break there is needed to signal the rebound from 1.1554 has ended at 1.1961, bring further fall to 1.1660-65, then towards 1.1620-25 but said support at 1.1554 should remain intact. .

Our preferred count on the daily chart remains that a wave (II) from 1.2329 ended at 1.5145 with A-leg ended at 1.4720, followed by wave B at 1.2457, the wave C from there was also a 3 legged move and is labeled as (a): 1.3739, (b): 1.2885, the wave iii of the 5-waver (c) from 1.2885 has ended at 1.4339 and wave iv is a triangle ended at 1.3878 and wave v formed a top at 1.5145. The decline from there is a 5-waver (C) with minor wave (i) of I of (C) ended at 1.4218 with wave (ii) ended at 1.4580, wave (iii) ended at 1.3267 and wave (iv) ended at 1.3692 and wave (v) ended at 1.1876, this is also the low of wave I of (C) and wave II ended at 1.4940, hence wave III is now in progress with a diagonal wave 1 ended at 1.2042, the breach of previous support at 1.1876 (wave I trough) adds credence to our view that the wave 2 has ended at 1.3993, wave 3 has commenced for further weakness to 1.0411, then towards 1.0000.

On the upside, whilst another recovery to 1.1863 cannot be ruled out, reckon upside would be limited to 1.1900 and bring another decline later. Only above 1.1940 would revive bullishness and signal the retreat from 1.1961 has ended, bring retest of said resistance, break there would extend the rise from 1.1554 to 1.2000. Looking ahead, only a break above resistance at 1.2035 would retain bullishness and signal early upmove has resumed for retest of 1.2093 first. A break of this resistance would confirm resumption of recent upmove from 1.0340 low for headway to 1.2150-55 (61.8% projection of 1.1119-1.1910 measuring from 1.1662), then 1.2200-10

Recommendation: Stand aside for this week.

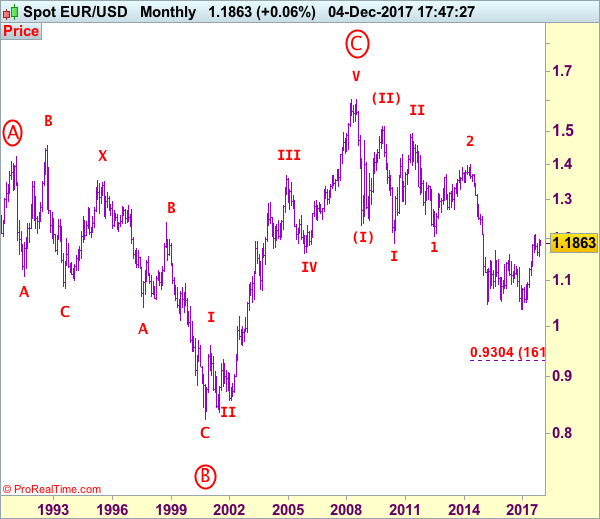

Euro's long-term uptrend started from 0.8228 (26 Oct 2000) with an impulsive structure. The rise from 0.8228 to 0.9593 (5 Jan 2001) is labeled as wave I, the retreat to 0.8352 (6 Jul 2001) is wave II and the rally to 1.3670 (31 Dec 2004) is wave III. Wave IV from there ended at 1.1640 (15 Nov 2005), the subsequent upmove to 1.6040 (July 15, 2008) is treated as wave V, the major selloff from the record high of 1.6040 to 1.2329 (October 27, 2008) signals a reversal has taken place with (I) leg ended at 1.2329 and once (II) ended at 1.5145, wave (III) itself is an extended move with I: 1.1876 and complex wave II ended at 1.4902, wave III has commenced with wave 1 and 2 ended at 1.2042 and 1.3993 respectively, wave 3 of III is now unfolding for weakness towards parity.

EUR/USD Plunges Amid Tax Reform Progress

Due to bearish pressure exercised by the 55-, 100- and 200-hour SMAs the currency exchange rate ended previous trading session below the 38.2% Fibonacci retracement level at 1.1760.

In result of this movement, the pair broke through the bottom boundaries of two junior ascending channels.

Despite the minor recovery of Euro the downward movement is expected to continue, being mainly driven by optimism surrounding tax reform.

From technical perspective, the surge of the Euro should be neutralized by a combination of the above moving averages together with the updated weekly PP at 1.1777.

In case these barriers are broken, the rate would still have another resistance line set up by the monthly PP at 1.1807.

The opposite side, in contrast, is does not contain any notably obstacles up until support zone located between the 1.1730 and 1.1722 levels.

GBP/USD Plunges Amid Brexit News

Due to existence of a strong selling pressure in the area between 1.3440 and 1.3450 marks, the cable could not climb higher and was forced to make a rebound.

However, as this turnaround matched with news coming from Brussels, the Pound lost more than 100-pips against the Dollar and ended the week at the psychological 1.3300 support level.

Today the pair is expected to resume the upward movement, even though it is unlikely to exceed the 1.3380 mark, as this area is reliably secured by the weekly and monthly PP as well as the slipping 55-, 100- and 200-hour SMA.

In other words, without another fundamental impulse the pair will be forced to retreat once again. In larger perspective it looks like the Friday's plunge led to transformation of a medium descending channel into the falling wedge formation.