Sample Category Title

US: Small Business Optimism Index Cools to Start 2025

The NFIB's Small Business Optimism Index fell 2.3 points to 102.8 in January, disappointing market expectations for a smaller decline to 104.7.

Seven out of ten subcomponents deteriorated on the month, with the remaining categories roughly unchanged. The largest declines came from the share of businesses planning to make capital expenditures (down 7 points to 20%), those planning to increase inventories (down 6 points to 0%), and those expecting the economy to improve (down 5 points to 47%).

The net share of businesses planning to increase employment fell 1 point to 18%. The share of firms with unfilled job openings was unchanged at 35%. Quality of labor concerns declined in January, with 18% of business owners identifying this as their top business problem. However, in addition to inflation, quality of labor concerns remained the top concern on the minds of small business owners.

The net share of firms currently increasing employee compensation rose 4 points to 33%, while the net share planning to do so over the next three months fell 4 points to 20% - the lowest level in five months. The share of businesses 'raising' average selling prices fell 2 points to 22% while the share of those 'planning’ to raise average selling prices also fell by 2 points to 26%.

Key Implications

Small business confidence retraced some of its post-election gains in January but remained roughly 10 points above its October level. Expectations for more accommodative fiscal and regulatory policy has bolstered optimism on the economy in the months ahead, but many of the subcomponents that track current and planned activity have seen little improvement over the past three months. Severe weather in January may have played a role in this trend, but an elevated degree of uncertainty has also likely weighed on small businesses.

Small businesses may be more optimistic than they were prior to the election, but they are also more uncertain. In January, the separate small business uncertainty index spiked back to a level it typically only hits during presidential elections. This encompasses the multitude of uncertainties currently prevailing in the market related to monetary, fiscal, and trade policy, which are all interacting simultaneously in firm expectations. With monetary policy on hold for the foreseeable future, fiscal policy grinding its way slowly through Congress, and trade policy front and center, it is likely that uncertainty will remain a constraint on business confidence over the coming months.

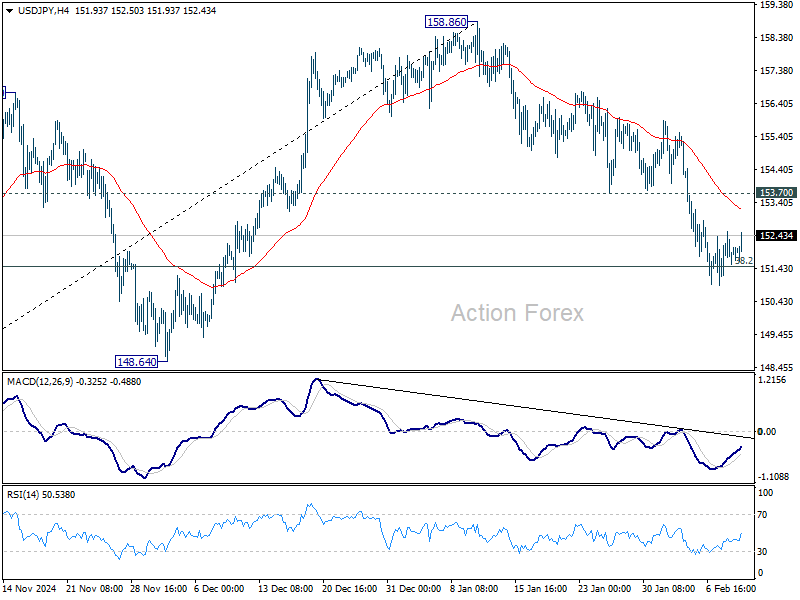

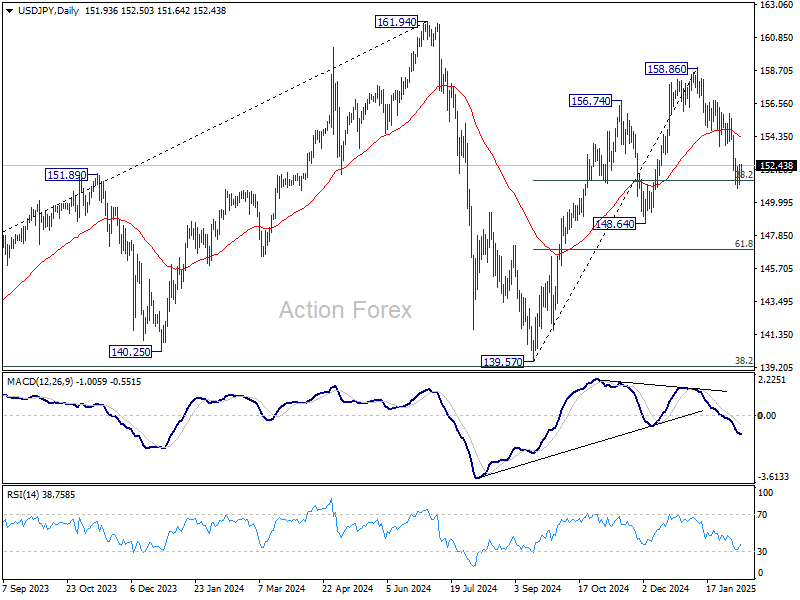

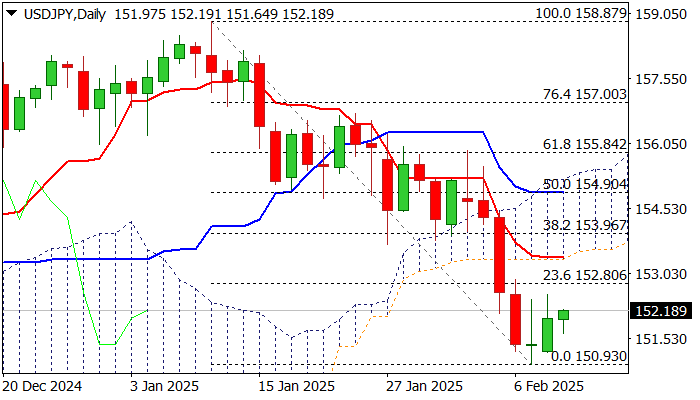

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.29; (P) 151.91; (R1) 152.63; More...

Intraday bias in USD/JPY stays neutral for the moment. Attention stays on 38.2% retracement of 139.57 to 158.86 at 151.49. Strong bounce from there, followed by break of 153.70 support turned resistance, will retain near term bullishness, and turn bas back to the upside for retesting 158.86. However, sustained trading below 151.49 will suggest that whole rise from 139.57 has completed, and bring deeper fall to 61.8% retracement at 146.32 next.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

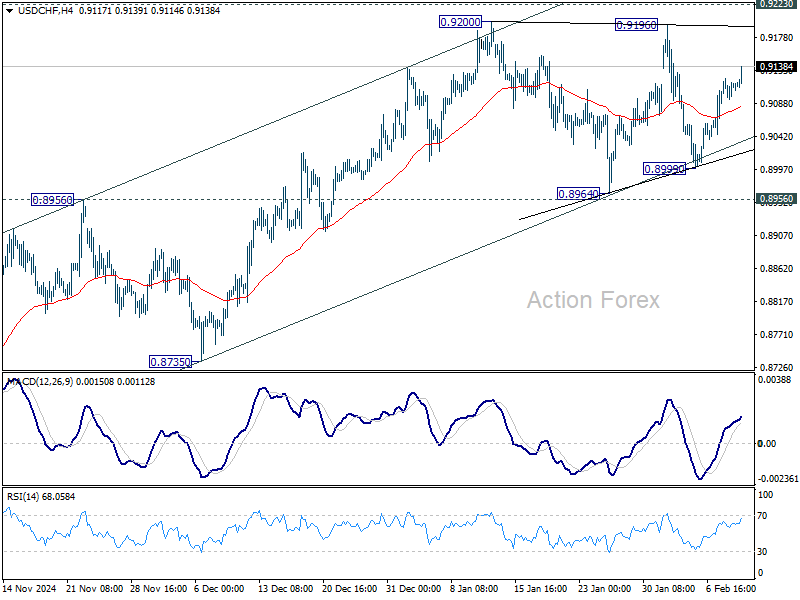

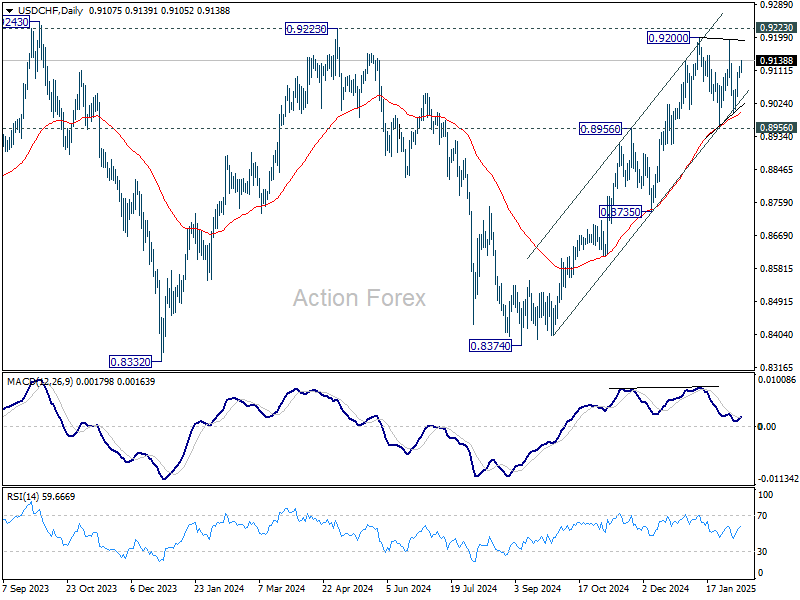

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9098; (P) 0.9110; (R1) 0.9127; More…

USD/CHF's consolidation from 0.9200 is still in progress and intraday bias remains neutral. Outlook stays bullish with 0.8956/64 support zone intact. On the upside, firm break of 0.9200/9223 will resume the whole rally from 0.8374 and carry larger bullish implication. However, sustained break of 0.8964 will be a sign of reversal and turn bias back to the downside.

In the bigger picture, decisive break of 0.9223 resistance will argue that whole down trend from 1.0342 (2017 high) has completed with three waves down to 0.8332 (2023 low). Outlook will be turned bullish for 1.0146 resistance next. Nevertheless, rejection by 0.9223 will retain medium term bearishness for another decline through 0.8332 at a later stage.

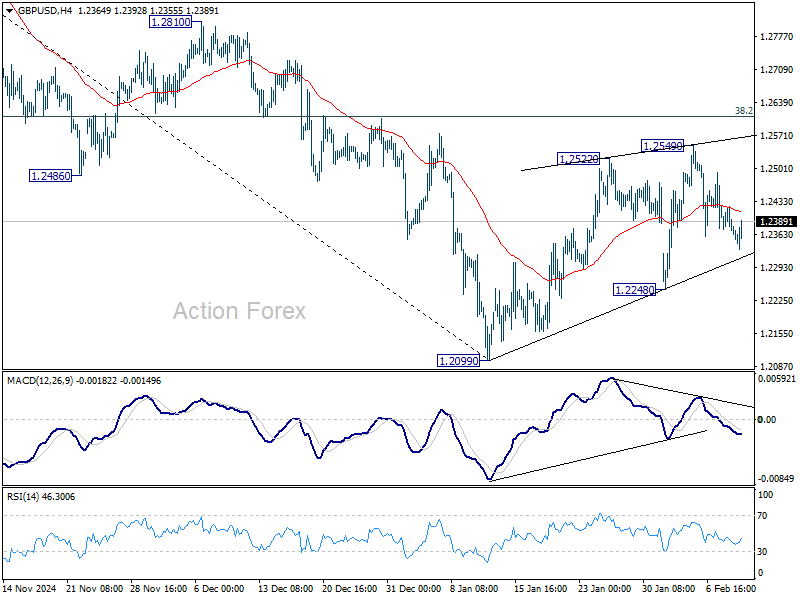

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2341; (P) 1.2381; (R1) 1.2408; More...

Intraday bias in GBP/USD's remains neutral as corrective pattern from 1.2099 is still extending. Stronger recovery might be seen but upside should be limited by 38.2% retracement of 1.3433 to 1.2099 at 1.2609. On the downside, break of 1.2248 support will bring retest of 1.2099 low. Firm break there will resume whole fall from 1.3433. However, decisive break of 1.2609 will raise the chance of near term reversal, and target 61.8% retracement at 1.2923.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

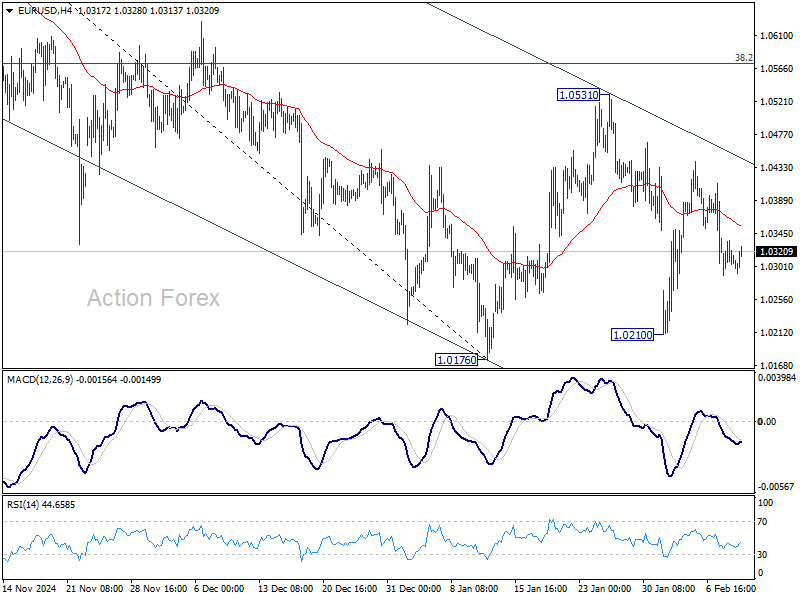

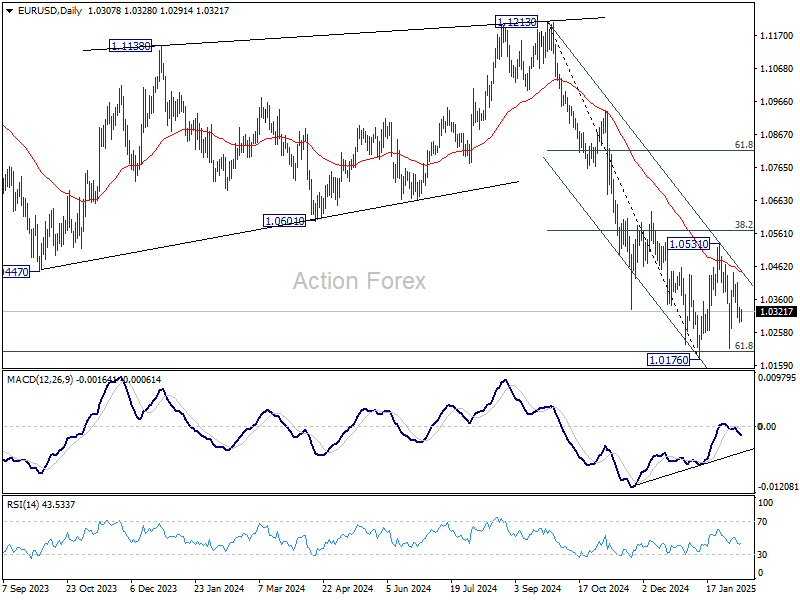

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0282; (P) 1.0310; (R1) 1.0334; More...

EUR/USD recovers mildly today but stays in the middle of the near term established range above 1.0176. Intraday bias remains neutral for the moment. Outlook will remain bearish as long as 38.2% retracement of 1.1213 to 1.0176 at 1.0572 holds. On the downside, break of 1.0176 will resume whole fall from 1.1213. However, decisive break of 1.0572 will raise the chance of reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

Cautious Trading Prevails as Markets Await Retaliations to US Tariffs

Trading is relatively subdued today across global markets as investors assess the fallout from the US steel and aluminum tariffs announced by President Donald Trump. Major European equity indexes are treading water, while US futures are slightly in the red. Treasury yields are recovering, though it remains too early to confirm a reversal of the recent downtrend. Meanwhile, Gold is having a notable pullback after an initial rejection at the key 3000 psychological level, suggesting profit-taking among traders.

European Commission President Ursula von der Leyen responded to the US move, stating that the EU will not let the "unjustified tariffs" go unanswered and pledged "firm and proportionate countermeasures" to protect European interests. However, no specific retaliatory measures have been outlined yet. Canada’s Prime Minister Justin Trudeau also criticized the tariffs as "unacceptable," reinforcing that "Canadians will stand up strongly and firmly if we need to." Markets remain cautious, awaiting concrete details on countermeasures from key US trade partners.

At a global level, IMF Managing Director Kristalina Georgieva addressed the uncertainty surrounding the tariff situation at the World Government Summit in Dubai, stating that it remains an "evolving story" and that it is "too early to say" what the full economic impact might be. This reinforces the broader market sentiment that investors are hesitant to make directional bets until more clarity emerges on trade retaliation and its economic implications.

In the forex market, Dollar has turned mixed, losing some momentum against Euro and Sterling while firming up slightly against Yen and Swiss Franc. Market focus is now shifting to Fed Chair Jerome Powell's Congressional testimony, with investors looking for signals on how long Fed’s current policy pause might last. Powell is also expected to be questioned on the impact of tariffs. Though it is unlikely he will provide any clear forward guidance on both fronts.

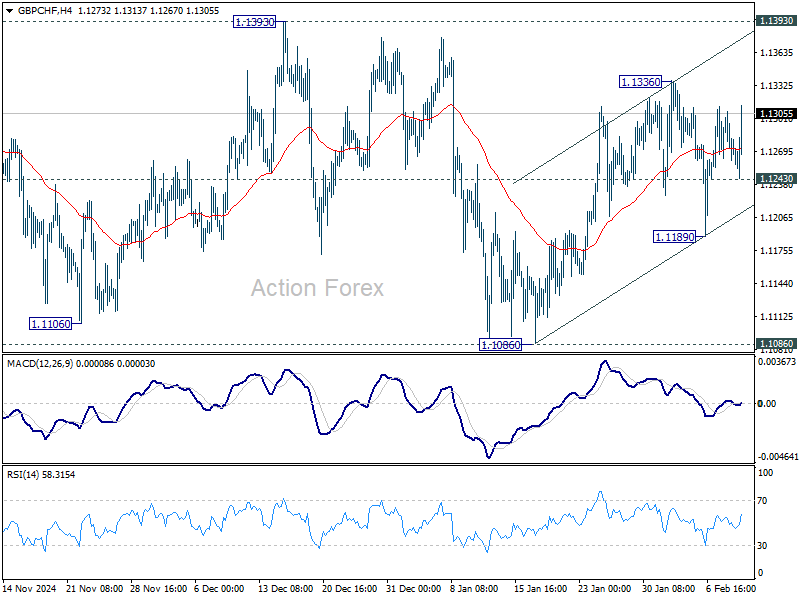

GBP/CHF could see increased volatility this week as the UK prepares to release Q4 GDP data and Switzerland reports January CPI figures. The cross has been struggling in range trading since last September. Today's bounce suggests that rise from 1.1086 is ready to resume through 1.1336 towards 1.1393. Strong resistance could be seen there to limit upside to start another falling leg. Meanwhile, break of 1.1243 should bring deeper fall through 1.1189 towards 1.1086.

In Europe, at the time of writing, FTSE is flat. DAX is up 0.27%. CAC is up 0.16%. UK 10-year yield is up 0.0317 at 4.493. Germany 10-year yield is up 0.051 at 2.416. Earlier in Asia, Japan was on holiday. Hong Kong HSI fell -1.06%. China Shanghai SSE fell -0.12%. Singapore Strait Times fell -0.37%.

US NFIB small business optimism drops as uncertainty rises, hiring challenges persist

NFIB Small Business Optimism Index declined to 102.8 in January, missing market expectations of 104.6 and falling from December’s reading of 105.1.

The decline reflects growing concerns among small business owners, as seven out of the 10 components of the index deteriorated, while only one improved. Additionally, the Uncertainty Index surged 14 points to 100, marking the third-highest reading in its history after two months of easing uncertainty.

NFIB Chief Economist Bill Dunkelberg highlighted while there is still "optimism regarding future business conditions," uncertainty is climbing. One major concern remains the persistent "hiring challenges," as businesses struggle to find qualified workers to fill vacancies. Capital investment plans are also being reconsidered.

Australia's Westpac consumer sentiment ticks up, RBA to start cutting this month

Australia's Westpac Consumer Sentiment Index rose slightly by 0.1% mom to 92.2 in February. While consumer mood improved significantly in the second half of 2024, the past three months have shown stagnation.

Westpac noted that financial pressures on households persist and a more uncertain global economic climate has also played a role in dampening optimism.

RBA is likely to begin policy easing at its next meeting on February 17–18. Westpac highlighted that recent economic data on core inflation, wage growth, and household consumption indicate that inflation is "returning to target faster" than previously expected.

These factors provide RBA with the confidence to initiate a 25bps rate cut this month, marking the first step in what is expected to be a "moderate" easing cycle through 2025.

Australian NAB business confidence rebounds to 4, but conditions remain weak

Australia's NAB Business Confidence index made a strong recovery in January, rising from -2 to 4 and returning to positive territory. However, despite this uptick in sentiment, underlying business conditions deteriorated.

Business Conditions index dropped from 6 to 3, marking a notable slowdown. Within this, trading conditions slipped from 10 to 6, while profitability conditions turned negative, falling from 4 to -2. On a more positive note, employment conditions edged up slightly from 4 to 5.

Cost pressures remained a key concern for businesses. Purchase cost growth eased to 1.1% on a quarterly equivalent basis, down from 1.4%. Labor cost growth picked up slightly to 1.8%. Meanwhile, final product price growth held steady at 0.8%, while retail price inflation inched up to 0.9%. Businesses are struggling to fully pass on rising costs to consumers.

NAB Chief Economist Alan Oster noted that while confidence improved, it is uncertain whether this momentum will be sustained. Elevated cost pressures, particularly on wages and input costs, continue to weigh on overall business conditions.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0282; (P) 1.0310; (R1) 1.0334; More...

EUR/USD recovers mildly today but stays in the middle of the near term established range above 1.0176. Intraday bias remains neutral for the moment. Outlook will remain bearish as long as 38.2% retracement of 1.1213 to 1.0176 at 1.0572 holds. On the downside, break of 1.0176 will resume whole fall from 1.1213. However, decisive break of 1.0572 will raise the chance of reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

US NFIB small business optimism drops as uncertainty rises, hiring challenges persist

NFIB Small Business Optimism Index declined to 102.8 in January, missing market expectations of 104.6 and falling from December’s reading of 105.1.

The decline reflects growing concerns among small business owners, as seven out of the 10 components of the index deteriorated, while only one improved. Additionally, the Uncertainty Index surged 14 points to 100, marking the third-highest reading in its history after two months of easing uncertainty.

NFIB Chief Economist Bill Dunkelberg highlighted while there is still "optimism regarding future business conditions," uncertainty is climbing. One major concern remains the persistent "hiring challenges," as businesses struggle to find qualified workers to fill vacancies. Capital investment plans are also being reconsidered.

Yen’s Rally Stalls But May Resume Soon

USD/JPY is consolidating near 151.96 after a temporary pause in the yen’s recent strength.

Key market factors

At the beginning of the week, the Japanese yen weakened against the US dollar as the greenback reacted to fresh US trade tariffs.

US President Donald Trump recently signed an executive order imposing a 25% tariff on steel and aluminium imports, with no exemptions for partner countries. This decision has triggered fears of a global trade war, which could, in turn, limit the Federal Reserve’s ability to cut interest rates further.

Despite this, the yen appreciated by 2% against the USD last week, driven by increasing market expectations that the Bank of Japan (BoJ) will continue its monetary tightening cycle.

BoJ policymaker Naoki Tamura reinforced this view last Thursday by suggesting that the central bank should move towards an interest rate of at least 1% in the second half of fiscal 2025. Recent Japanese economic data supports this hawkish stance, with rising wages and household spending providing a solid foundation for further rate hikes.

Technical analysis of USD/JPY

On the H4 chart, USD/JPY formed a consolidation range around 151.90 after a downward move. A break below this range is expected, targeting 148.80, with a potential continuation to 148.38. This level serves as a local target. Once the wave completes, a corrective move towards 151.90 is possible before the broader downtrend resumes, aiming for 145.50. The MACD indicator confirms this scenario, with its signal line below zero and sharply downwards, suggesting ongoing bearish momentum.

On the H1 chart, the market is developing a downward wave towards 148.40, with consolidation around 151.90. A downside breakout would confirm the continuation of the second phase of the decline. After reaching 148.40, a corrective move back to 151.90 could materialise. The Stochastic oscillator supports this outlook, with its signal line below 80 and sharply downward, indicating bearish pressure.

Conclusion

The Japanese yen’s rally has paused, but further gains remain likely, supported by expectations of continued BoJ tightening. Technical indicators suggest that USD/JPY may break lower towards 148.40, with further downside potential towards 145.50. The yen’s trajectory will depend on BoJ policy signals and further developments in US trade policy, particularly how global markets respond to Trump’s tariffs.

USD/JPY: Bears Taking a Breather Ahead of Key US Events

USDJPY remains constructive and ticks higher on Tuesday, on surprise slowdown in safe haven demand after President Trump imposed new set of tariffs on imports of metals.

Also, investors are taking a breather ahead of today’s testimony of Fed Chair Powell and Wednesday’s release of US inflation report for January, which should provide more details about inflation and further steps of the central bank on monetary policy.

Short term downtrend from 2025 peak at 158.87 (Jan 10) has found a footstep at the zone of important Fibo support (38.2% of 139.57/158.87 at 151.50), where a temporary base is forming.

Current bounce so far looks like a mild correction as daily studies are bearish, with recovery attempts facing strong resistances at 152.77 (converged 100/200DMA’s) and 153.40 (base of daily Ichimoku cloud, reinforced by daily Tenkan-sen).

Broader bears are expected to remain in play while these levels cap recovery and keep in play risk of fresh weakness, with sustained break of 151.50 (Fibo) and 150.93 (last week’s low) to signal bearish continuation.

Last week’s large bearish weekly candle additionally weighs, as the pair was in red for the four consecutive weeks and the action accelerated last week.

Res: 152.77; 153.40; 153.96; 154.90.

Sup: 151.50; 150.93; 150.00; 149.22.

Australian Dollar Drifting after Mixed Confidence Data

The Australian dollar is showing little movement on Tuesday. In the European session, AUD/USD is trading at 0.6279, up 0.05% on the day.

Australian business confidence jumps, consumer confidence stagnant

Australian confidence indicators were mixed on Tuesday. The Westpac consumer sentiment index climbed 0.1% in February to 92.2 points, which means a majority of the surveyed consumers were pessimistic about econmic conditions. The reading bounced back from a 0.7% decline in January but was shy of the forecast of 0.4%. Consumer confidence remains weak as consumers have been squeezed by high inflation and elevated interest rates. The survey noted that consumers have become more confident that the central bank will lower rates.

The National Australia Bank’s (NAB) business confidence index, which rose 6 points in January to +4. However, business conditions index dropped to +3 from +6 a month earlier, as profitability and employment weakened. The NAB survey noted that retail spending has improved and this trend would need to continue if business conditions were to improve.

The mixed confidence numbers come just one week before a crucial Reserve Bank of Australia meeting. A rate cut is virtually certain at the meeting, which would mark the RBA’s first rate cut since Nov. 2020. The RBA is yet to join the easing cycle which other major central banks have implemented as inflation has fallen.

The Federal Reserve is widely expected to continue to maintain interest rates at the March meeting. The US economy remains robust and the labor market has slowed gradually, which means there isn’t much pressure on Fed policy makers to lower rates in the coming months. Barring unexpected economic news, the Fed is expected to cut rates no more than one or two times in 2025.

AUD/USD technical

- AUD/USD tested support at 0.6267 earlier. Below, there is support at 0.6245

- There is resistance at 0.6299 and 0.6321.