Sample Category Title

USD/JPY Exchange Rate Recovers from Yearly Low

As shown on the USD/JPY chart, today the exchange rate aggressively surged above the 153 yen per US dollar level. This marks a strong recovery from the yearly low of around 151 yen per dollar, set last week.

Today's bullish momentum developed following a statement from Japan's Minister of Industry, Yoji Muto, who mentioned that the government had asked the United States to exempt Japan from the tariffs imposed by the Trump administration.

Can the USD/JPY rise continue?

Technical analysis of the USD/JPY chart reveals that key extremes over the last three months form the contours of an upward channel, with:

→ From a bullish perspective: The exchange rate is rising towards the median, which tends to "attract" the price as demand and supply balance in this region.

→ From a bearish perspective: The 154 yen per dollar level, which acted as support in February (shown by arrows), may hinder further growth.

The future direction of the USD/JPY pair largely depends on a key upcoming news release, which could have a significant impact on the US dollar’s value against other currencies. At 16:30 GMT+3 today, the CPI report will be published, shedding light on the current inflation situation. Be prepared for potential volatility spikes.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Pound’s Rally Stalls as Investors Await Fresh Economic Data

GBP/USD is consolidating around 1.2447 on Wednesday as traders hold back, awaiting key UK economic data releases later this week.

Key factors influencing GBP/USD

Earlier this week, the British pound faced pressure after Bank of England (BoE) policymaker Catherine Mann shifted to a more dovish stance. She stated that weak domestic demand reduces inflation risks, marking a notable change from her previously hawkish position.

Mann now believes consumer spending is slowing, limiting businesses' ability to raise prices, and contributing to a faster-than-expected decline in inflationary pressures.

The BoE expects inflation to rise to 3.7% by the end of 2025, up from 2.5% in December 2024. Meanwhile, UK GDP growth forecasts have been lowered to 0.75% for 2025, down from the earlier estimate of 1.5%.

Investors are now awaiting key UK macroeconomic data, including:

- December GDP estimate

- Preliminary Q4 2024 economic growth data

- End-of-year industrial production figures

Externally, the pound is also under pressure from a stronger US dollar. However, compared to other major currencies, GBP remains relatively stable.

Technical analysis of GBP/USD

On the H4 chart, GBP/USD declined to 1.2332, followed by a correction to 1.2458. After reaching this level, a new downside wave is expected towards 1.2279. A narrow consolidation range is likely to form around this level. If the price breaks below this range, the next targets will be 1.2100 and 1.2020, signalling a continued bearish trend. The MACD indicator supports this outlook, with its signal line positioned below zero and pointing downward, indicating a continuation of the downtrend.

On the H1 chart, GBP/USD completed a correction to 1.2458. The market is now expected to resume its downward movement towards 1.2279. The Stochastic oscillator confirms this scenario, with its signal line above 80 and trending sharply downwards towards 20, suggesting increasing bearish momentum.

Conclusion

GBP/USD is in a consolidation phase, with market participants awaiting key UK economic data. Weakening domestic demand and shifting expectations regarding the Bank of England's (BOE) policy are weighing on the pound, while external pressure from a stronger USD adds to its downside risks. Technically, further declines are expected towards 1.2279, with the potential for deeper losses to 1.2100 and 1.2020 if the economic data disappoints. Market focus remains on upcoming UK macroeconomic releases, which will determine the next significant move for GBP/USD.

Not Convinced that Higher Inflation Figure Will Trigger Sustained Further USD Gains

Markets

Fed Chair Powell’s appearance before the Senate Banking Committee yesterday didn’t yield much clues on (changes in) monetary policy in the Trump 2.0 era. The Fed Chair understandably stuck to data dependency. After having reduced policy restriction in the second half of last year, a strong economy and labour market give the Fed ample room to assess the impact of upcoming developments. In this respect Powell still held the view that it was unwise to speculate on the potential impact of the new government policy/proposals. The Fed is in no rush to cut rates. The Fed Chair also advocated to keep monetary policy out of the political debate as the best way for the Fed to serve its dual mandate. Many questions were on regulation and supervision instead on monetary policy. The US yield curve yesterday bear steepened with yields rising between 0.9 bps (2-y) and 4.0 bps (30-y), but most of this move already occurred before Powell’s testimony. The $58 bln US Treasury auction met solid investor interest. Regarding the data, there was a slightly bigger than expected decline in NFIB small business confidence, admittedly from a strong level, with quite a substantial rise in the uncertainty index (100 from 86). European yields showed tentative signs of bottoming after the end-January/early February setback. German yields added between 5.8 bps (2-y) and 7.7 bps 30-y). We didn’t see any specific trigger. US equity markets showed no clear trend (S&P 500 +0.03%) as markets still try to assesses the impact/reaction to the announcement of 25% tariffs on steel and aluminum. The EuroStoxx50 (+0.61%) again outperformed the US. Oil extended its rebound (Brent $77 p/b close). The dollar lost ground throughout the session but stays rangebound (DXY close 107.96 from 108.33, EUR/USD 1.036 from 1.0307).

Asian equities this morning are mostly trading in mildly positive territory. There are few eco data except for the US January CPI data to be released this afternoon. Consensus (headline 0.3% M/M and 2.9% Y/Y, core 0.3% M/M and 3.1% Y/Y) is broadly in line with last month. The market currently already scaled back expectations on Fed easing quite substantially (first additional 25 bps rate cut only fully discounted by September and less than 50% chance on a next step by year end). Given this starting point, an upward surprise is probably needed to further price out Fed easing. Maybe, LT yields still have some additional upside in case of an in-line/higher than expected figure. Later today, the US Treasury will sell $42 bln 10-y Notes. The dollar recently held relatively strong but failed to make further headway, despite the avalanche of announcements on tariffs. We’re not convinced that a higher inflation figure will trigger sustained further USD gains. EUR/USD 1.0442 is first intermediate resistance. Recent yen outperformance stalled as markets also grow uncertain on the potential impact of tariffs for Japanese exports. USD/JPY this morning rebounds further to 153.6 (compared to a low near 151 end last week).

News & Views

The European Commission is considering a price cap on gas prices, the Financial Times reported citing people familiar with the early-stage talks. Prices have recently surged to the highest level in more than two years on rapidly depleting stock levels and a lack of alternative (renewable) energy sources. The EC proposed a cap back in 2022, at the height of the energy crisis that followed Russia’s invasion, but it was never put in practice due to its high knock-in level compared to actual prices. Mario Draghi in his competitive report of last year recommended of bringing in “dynamic caps” instead for situations when EU gas prices diverge from global ones. One of the EU officials said they are studying Draghi’s suggestion in detail.

Bank of Japan governor Ueda appearing before parliament repeated that follow-up rate hikes will depend on the economy and price evolution. While the central bank usually looks at underlying gauges that exclude energy and fresh food to assess inflation strength, Ueda noted that "Rises in the prices of food, including fresh food, won't necessarily be temporary and there's the chance that this will impact people's mindsets and price expectations." Prices in Japan rose 3.6% y/y in December compared to the 3% core measure. Ueda also confirmed the central bank will conduct a review of its current plan to taper government bond purchases in June. In July of last year the BoJ said it plans to halve the monthly buying pace to JPY 3tn as of January-March 2026.

Chinese Tech’s Big Return?

Federal Reserve (Fed) Chair Jerome Powell’s testimony yesterday went smoothly. He said that the Fed’s ‘policy stance is now significantly less restrictive than it had been’, the economy remains strong and that they ‘do not need to be in a hurry to adjust our policy stance.’ That was in line with his previous remarks. Powell also didn’t want to get too political. He said that ‘it’s not the Fed’s job to comment on the tariff policy’, that the impact of the tariffs is unknown but could eventually increase the inflationary pressures as someone will have to pay for them. The markets didn’t give a crazy reaction. The US yields rose slightly but the dollar index gave back gains and tested the 50-DMA to the downside. In the equity space, the Dow Jones advanced 0.30%, the S&P500 was flat, while Nasdaq 100 slightly retreated.

All eyes are on today’s US inflation update. The US headline inflation is expected to steady near 2.9% y-o-y in January, core inflation may have eased from 3.2% to 3.1%. A set of softer-than-expected inflation numbers could help sooth inflation worries and encourage a deeper retreat in the US dollar and a further advance across the major peers. While a stronger-than-expected set of inflation figures could fuel worries, back a further rise in the US yields and the dollar, and weigh on risk appetite.

China appetite returns

Chinese tech stocks are surfing on the DeepSeek wave. Alibaba for example gained more than 40% since mid-January while Warren Buffet-backed BYD rallied more than 7.50% today in Hong Kong and is also up by a hefty 42% since a month. The news that the company plan to integrate software from DeepSeek in its cars and the announcement that they will offer God’s Eye – their driver assistance system – in China for free help boosting the outlook for the Chinese EV giant and narrow the gap with Tesla – which on the other hand is falling from grace on slowing sales - not only due to the slowing global appetite for electric cars but also due to Elon Musk’s involvement in world politics.

Overall, stocks in Hong Kong didn’t look this promising in a while, and there is substantial room to extend gains before retesting the 2018 and 2021 peaks. Chinese tech giants have two key advantages. 1. They have Big Tech names that have a proven track record for building game-changing technology – like Alibaba and Tencent. And 2. Chinese consumers tend to be easier to adopt new technologies allowing the technology advances to spread faster.

Does that counterweigh the political, geopolitical and trade risks? Time will tell.

Oil and Gas

US crude rallied past the 50-DMA and rebounded lower after touching the $73.70pb yesterday. The sight of a more than 9mio barrel build in US inventories suggested by yesterday’s API report somehow killed joy. The freshly breached 50-DMA could act as a short-term support for a further extension of the gains in the short run, but we may see a strong resistance approaching the $74.50 mark, near the 200-DMA and the major 38.2% Fibonacci retracement on the latest selloff.

Elsewhere, the European nat gas futures extend gains on melting gas reserves and on the upcoming cold days that will further draw down the reserves, while the US nat gas futures successfully held ground near a key Fibonacci support and remain upbeat.

In the individual space, BP – which gained more than 7% on news that Elliott Investment Management steps in to tidy up things, lost a meagre 0.62% yesterday after announcing that their income dropped 35% last quarter due to lower oil and gas prices and lower profits from its refineries. 430-445p could be an interesting entry level for investors who would like to take a chance on Elliott’s plans to shift focus from renewable to traditional energy sources.

All Eyes on US CPI

In focus today

From the US, the most important data release of the day will be the January CPI. We forecast headline inflation at +0.3% m/m (SA) and 2.9% y/y and core inflation at +0.2% m/m (SA) and 3.1% y/y. Starting from 16:00 CET, Fed Chair Powell will continue his semi-annual testimony, this time to the House Financial Services Committee at Congress. It will likely be a repeat of his testimony in the Senate Committee of Banking, so we do not expect any new messages from him.

In Sweden, Riksbank Vice Governor Bunge speaks at 10.00 local time about the economy and current monetary policies at a seminar in London hosted by JP Morgan. She will have a good opportunity here to comment on the upside January inflation surprise.

Economic and market news

What happened yesterday

In Norway, Q4 mainland GDP growth landed at -0.4% q/q, undershooting both Norges Bank's projection of 0.3% q/q, market consensus of 0.3% q/q and our projection of 0.1% q/q. In short, the negative growth is a clear indication that monetary policy is working with rate-sensitive parts of the economy hurting. Growth in employment of 0.2% q/q, better than what headline figures would suggest, remains a slight bright spot. We still pencil in four 25bp rate cuts from Norges Bank in 2025 starting at the monetary policy meeting in March.

In the US, Fed chairman Powell gave his semi-annual testimony in the Senate where he gave a balanced assessment and underlined that the Fed does not need to be in a hurry to adjust policy providing a small lift to bond yields.

Cleveland Fed president Hammack (hawk and non-voter) emphasized that the Fed should keep the funds rate steady for some time amid current economic conditions and higher policy uncertainty. New York Fed president Williams (hawk and voter) was also on the wire, stating that monetary policy is well positioned to achieving maximum employment and price stability.

US small business confidence took a hit in January after the brief sense of euphoria following the November elections, echoing what we saw in the Michigan survey last Friday. Fewer firms see this as a good time for expanding business, while price and hiring plans declined slightly. No dramatic changes or sense of sharp weakening for now, but perhaps just the reality of Trump's policies setting in.

Turning to the tariff-saga leaders of Mexico, Canada, and the European Union condemned President Trump's decision to impose 25% tariffs on all steel and aluminium imports, eliminating all country exceptions and quota deals from 12 March. While leaders from Mexico did not articulate any plans to retaliate, both Canada and the European Commission communicated that there would be firm and proportionate counter-measures. Trump stated on Monday that he would impose reciprocal tariffs on all countries that impose duties on U.S. goods.

In the Middle East, the Israeli Prime Minister Benjamin Netanyahu reiterated that the ceasefire would end, and the Israeli military would resume operations in Gaza, if Hamas does not release the Israeli hostages as planned by noon on Saturday.

Equities: Equities were unchanged at a global level yesterday, while Europe continued its outperformance, hitting a new record close. This takes Stoxx 600 almost 8% higher this year vs 3% in the US, so the outperformance is huge. Wait-and-see mode in equity markets (MSCI World 0%) without clear sector trades. Cyclicals/defensives, growth/value traded on par, while large caps continued to beat small caps. Consumer discretionary and primarily Tesla was a notable decliner though, while staples and energy were the best performing sectors. Futures are indicating another slow start to trading today.

FI: US Treasury yields rose, and the curve steepened on the back of comments from Federal Reserve Chairman Powell that the Federal Reserve is in kind of a "wait-and-see mode" in terms of rate cuts and that the Federal Reserve must stay patient given the strength of the US economy. There was a similar move in the European government bond yields and the curves steepened modestly. The 10Y spread between France and Germany as well as the 10Y spread between Italy and Germany has widened modestly in recent days.

FX: EUR/USD edged gradually higher throughout yesterday's session, further fueled by reports that Zelensky is willing to swap territory with Russia to secure a peace deal. The SEK had yet another strong session, with EUR/SEK temporarily reaching 11.22 before trading back above 11.25 once again. The NOK instead faced headwinds on the back of weak domestic growth data, resulting in NOK/SEK briefly visiting levels below 0.97. The Zloty continues to build on recent weeks' strong performance, with EUR/PLN making new lows almost daily, currently at 4.17.

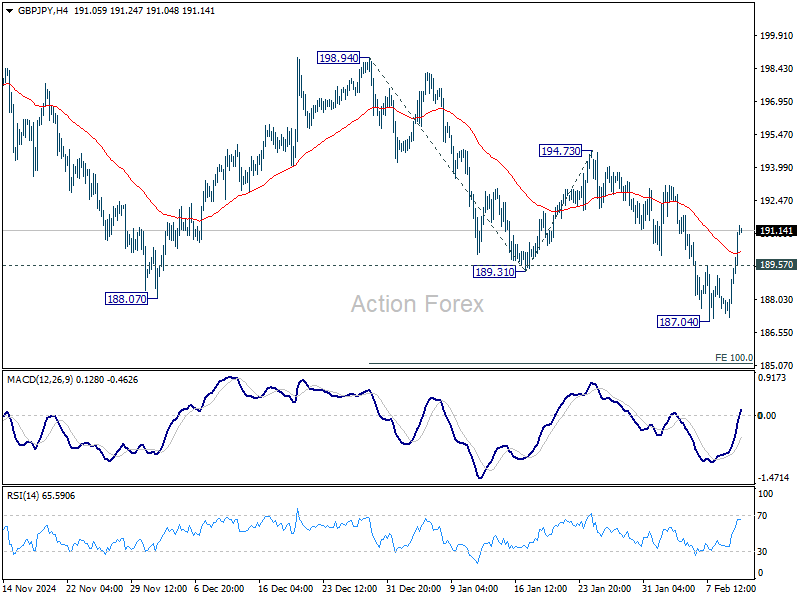

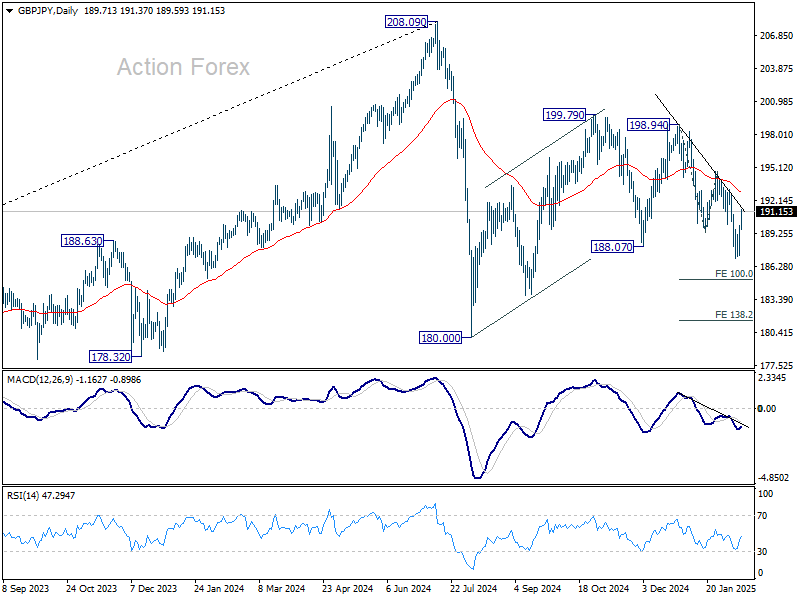

GBP/JPY Daily Outlook

Daily Pivots: (S1) 188.07; (P) 188.99; (R1) 190.74; More...

GBP/JPY's rebound extended higher today and intraday bias is turned neutral first. On the downside, break of 187.04 will resume the fall from 198.94 to 100% projection of 198.94 to 189.31 from 194.73 at 185.10. However, firm break of 194.73 resistance will suggest that the decline has completed, and turn bias back to the upside for 198.94. Overall, sideway corrective pattern from 180.00 might still extend further.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall to 100% projection of 208.09 to 180.00 from 199.79 at 171.70, even still as a correction.

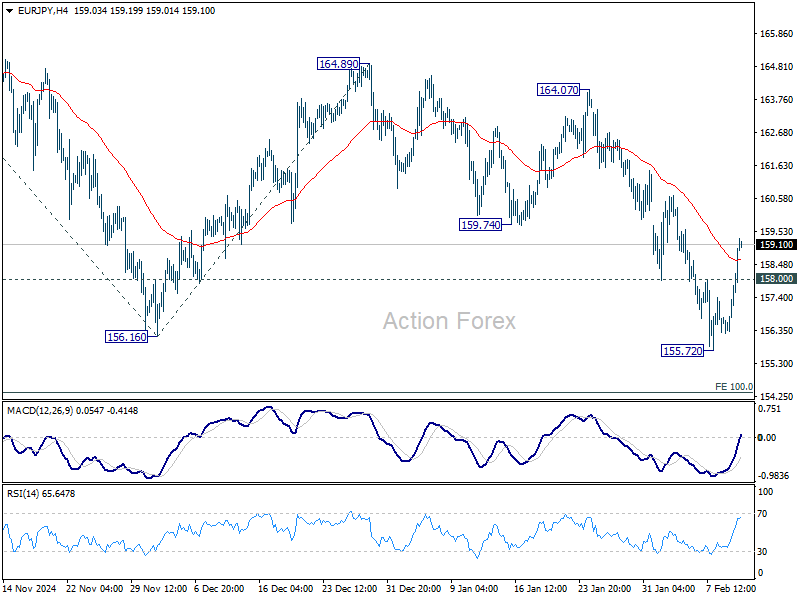

EUR/JPY Daily Outlook

Daily Pivots: (S1) 156.79; (P) 157.49; (R1) 158.72; More...

Intraday bias in EUR/JPY is turned neutral first with current strong recovery. On the downside, break of 155.72 will resume the fall from 164.89. Next target is 100% projection of 166.7 to 156.16 from 164.89 at 154.38. Nevertheless, firm break of 159.74 support turned resistance will argue that fall from 164.89 has completed, and turn bias back to the upside for this resistance. Overall, sideway corrective pattern from 154.40 might extend further.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall to 100% projection of 175.41 to 154.40 from 166.57 at 145.56, even still as a correction.

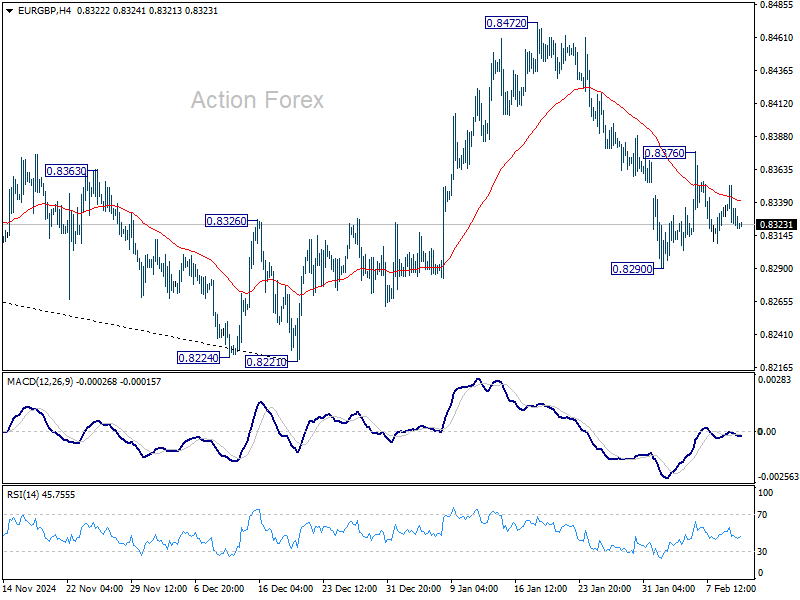

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8314; (P) 0.8334; (R1) 0.8344; More...

Intraday bias in EUR/GBP remains neutral and near term outlook is mixed. On the upside, above 0.8376 minor resistance will bring stronger rally towards 0.8472. However, on the downside, break of 0.8290 will resume the fall from 08472 to retest 0.8221 low.

In the bigger picture, rebound from 0.8221 medium term bottom could extend higher through 55 W EMA (now at 0.8435). However, medium term outlook will be neutral at best as long as 0.8624 cluster resistance zone (38.2% retracement of 0.9267 to 0.8221 at 0.8621) holds. Another decline through 0.8221 would remain mildly in favor.

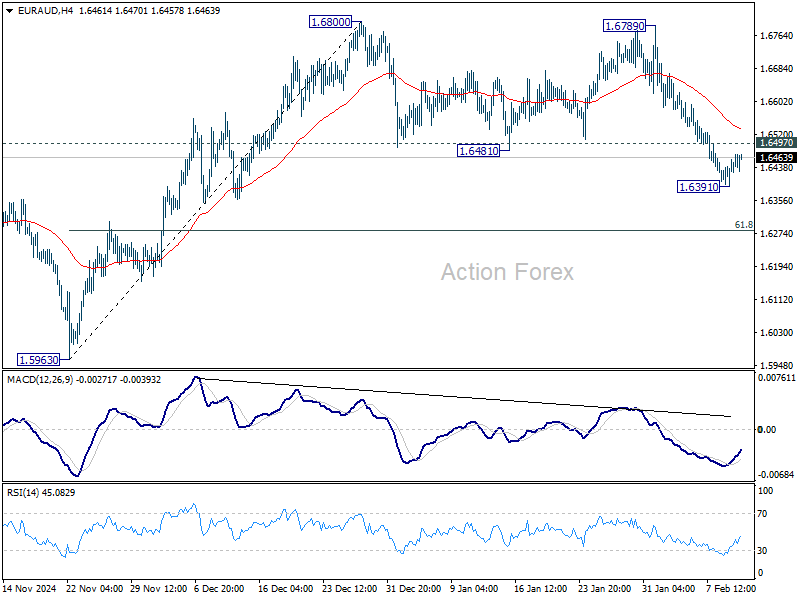

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6412; (P) 1.6442; (R1) 1.6492; More...

EUR/AUD recovered after dipping to 1.6391 and intraday bias is turned neutral first. Risk will stay on the downside for the moment. Below 1.6391 will extend the corrective fall from 1.6800 to 61.8% retracement of 1.5963 to 1.6800 at 1.6283. Nevertheless, firm break of 1.6497 minor resistance will dampen this bearish case and turn bias to the upside for rebound.

In the bigger picture, with 1.5996 key support (2024 low) intact, larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5996 will indicate that such up trend has completed and deeper decline would be seen.

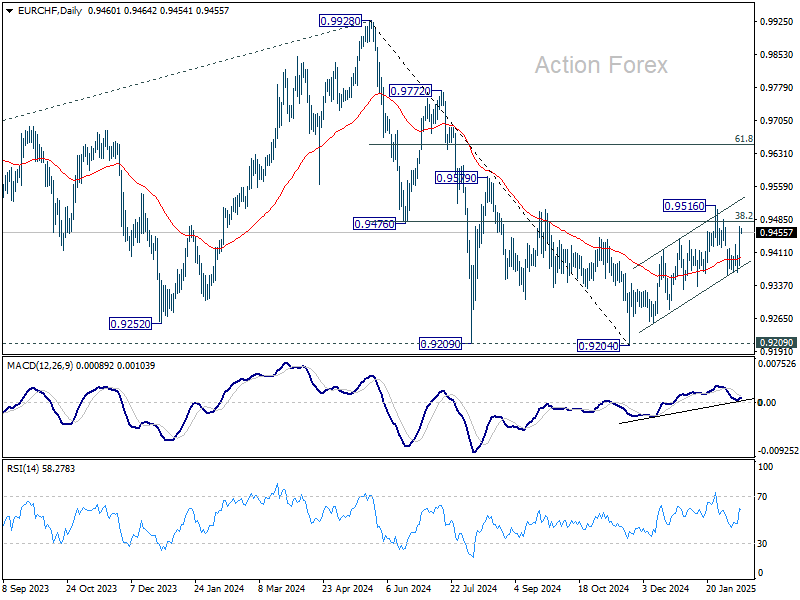

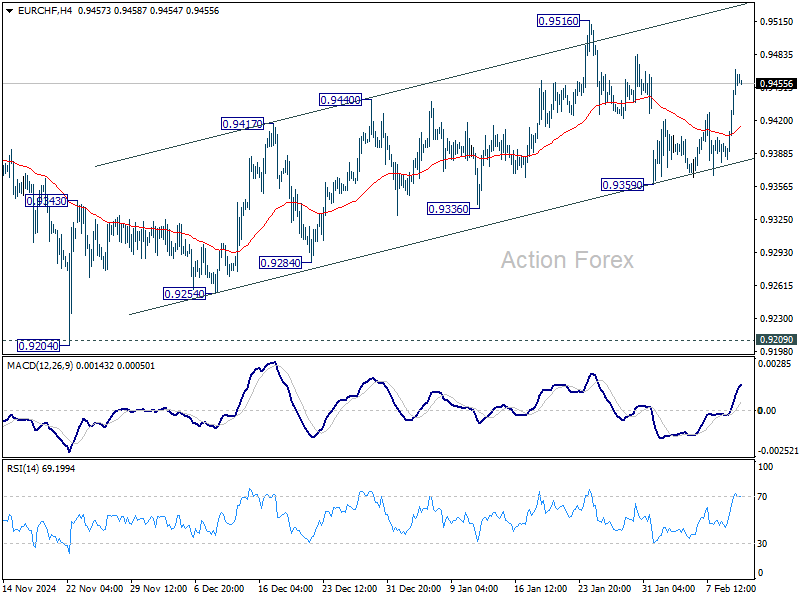

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9408; (P) 0.9439; (R1) 0.9495; More....

EUR/CHF rebounded further today but stays below 0.9516 resistance. Intraday bias remains neutral first. On the downside, break of 0.9359 should affirm the case that corrective rebound from 0.9204 has already completed at 0.9516. Deeper fall would then be seen to retest 0.9204 low. However, firm break of 0.9516 will resume the rally from 0.9204 instead.

In the bigger picture, the rejection by 55 W EMA (now at 0.9489) argues that rebound from 0.9204 has completed as a corrective move after failing to sustain above 38.2% retracement of 0.9928 to 0.9204 at 0.9481. Firm break of 0.9204/9 support zone will confirm larger down trend resumption.