Sample Category Title

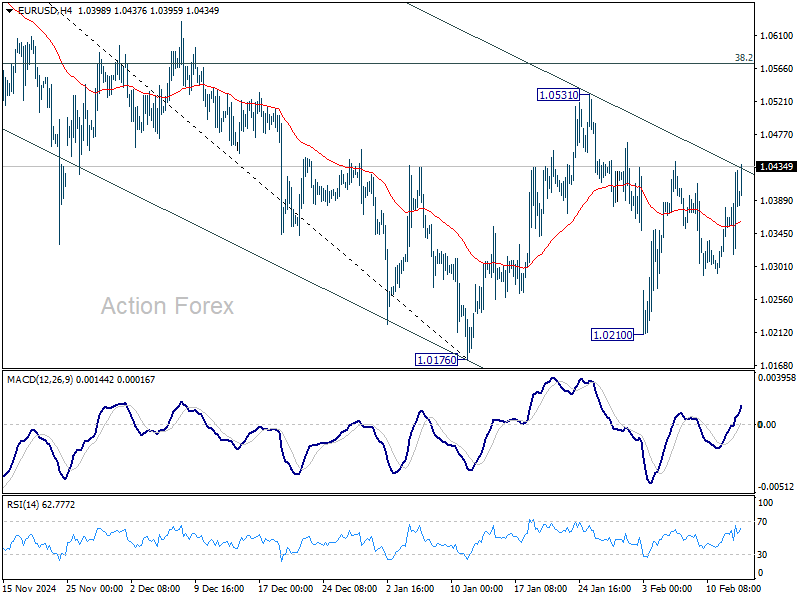

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0309; (P) 1.0345; (R1) 1.0398; More...

No change in EUR/USD's outlook as consolidations from 1.0176 is still extending. Intraday bias stays neutral at this point. Outlook will remain bearish as long as 38.2% retracement of 1.1213 to 1.0176 at 1.0572 holds. On the downside, break of 1.0176 will resume whole fall from 1.1213. However, decisive break of 1.0572 will raise the chance of reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

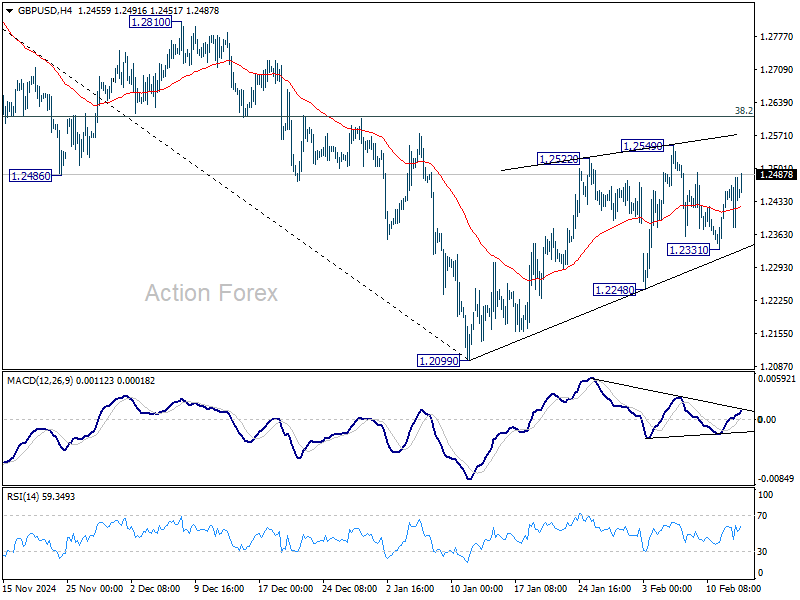

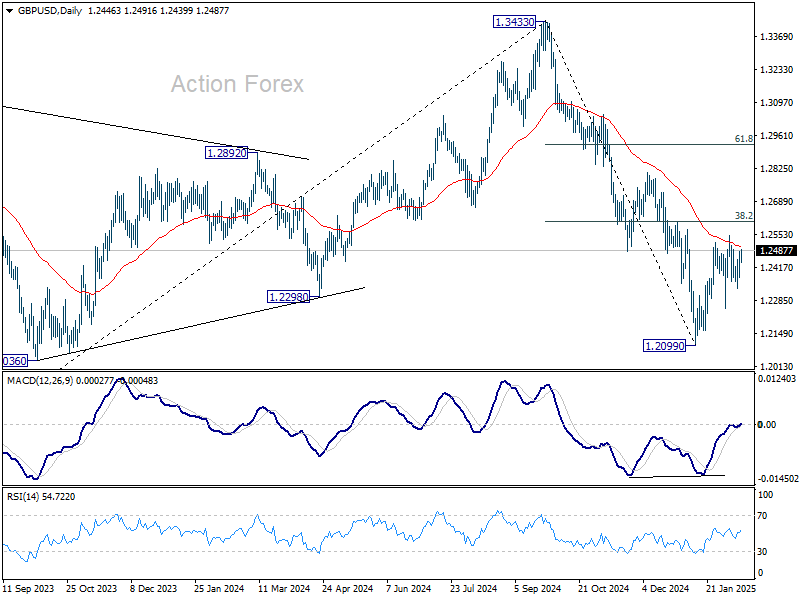

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2387; (P) 1.2435; (R1) 1.2493; More...

Intraday bias in GBP/USD stays neutral and outlook is unchanged. Corrective rebound from 1.2099 could still extend higher. But upside should be limited by 38.2% retracement of 1.3433 to 1.2099 at 1.2609. On the downside, below 1.2331 minor support will turn bias to the downside for 1.2248 support. Firm break there will argue that the correction has completed and bring retest of 1.2099 low. However, decisive break of 1.2609 will raise the chance of near term reversal, and target 61.8% retracement at 1.2923.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

Dollar Momentum Fades as UK GDP Takes Center Stage

The forex markets was subdued in Asian session today. Dollar strength faded quickly after initial boost from stronger-than-expected US inflation data. While the greenback retains most of its gains against Yen, it has started to weaken against other major currencies. The reluctance of Dollar to sustain its rally—despite reduced odds of a Fed rate cut in the first half of 2025 and ongoing tariff threats—suggests that another down leg may be on the horizon.

With US inflation data out of the way, market focus now shifts to the UK, where Q4 GDP figures are set for release. The economy is expected to have contracted -0.1% qoq, with a modest 0.1% mom expansion in December. Think tank NIESR remains cautiously optimistic, predicting subdued growth in the first half of the year before an acceleration in the second half. It expects GDP growth of 1.5% for 2025, supported by higher government spending and business investment.

For the week so far, Euro leads as the top-performing currency, followed by Sterling and Aussie. Meanwhile, Yen remains the weakest, followed by Swiss franc and Kiwi. Dollar and Loonie positioned in the middle.

Technically, Gold's strong rebound ahead of 2852.31 support suggests that traders are not giving up on 3000 psychological level yet. Decisive break of 3000 and 61.8% projection of 1810.26 to 2789.92 from 2584.24 at 3189.66 before topping. Nevertheless, firm break of 2852.31 will bring deeper pullback to 2789.92 resistance turned support and possibly below to consolidate recent gains.

In Asia, at the time of writing, Nikkei is up 1.46%. Hong Kong HSI is up 1.52%. China Shanghai SSE is down -0.12%. Singapore Strait Times is down -0.05%. Japan 10-year JGB yield is up 0.0034 at 1.350. Overnight, DOW fell -0.50%. S&P 500 fell -0.27%. NASDAQ rose 0.03%. 10-year yield rose 0.100 to 4.637.

Looking ahead, UK GDP is the main focus in European session. Germany CPI final, Swiss CPI and Eurozone industrial production will be released too. Later in the day, US PPI and jobless claims will be be featured.

Fed's Powell: New CPI data confirms “not there” yet on inflation

Fed Chair Jerome Powell acknowledged that the latest inflation data released yesterday confirms the US is making progress but is still “not there on inflation.”

Following January’s stronger-than-expected CPI report, Powell said in the Congressional testimony that Fed will "keep policy restrictive for now" to bring price pressures down.

Powell also underlined that the "economy is strong, the labor market is solid" allowing the Fed to keep a tight policy stance and wait for inflation to ease further.

He also emphasized that one month of higher readings should not be interpreted as a complete reversal of the disinflation trend, especially given that Fed’s preferred inflation measure, the Personal Consumption Expenditures index, typically runs below CPI.

Bostic: Fed needs more clarity before cutting rates

Atlanta Fed President Raphael Bostic signaled uncertainty over the timing of rate cuts, citing ongoing concerns about inflation and policy shifts under the Trump administration. Speaking at an event overnight, Bostic emphasized the need for "more clarity" before making any definitive moves on monetary policy.

He acknowledged the difficulty in assessing the current economic conditions, stating, “My view is until we have more clarity, it’s going to be impossible to make a judgment about where our policy should go and how fast and at what pace, and so we’re just going to have to get more information before we’re going to be able to move.”

He also provided his estimate for the neutral rate, which he sees in a range of 3%-3.5%. Currently, Fed's target range stands significantly higher at 4.25%-4.5%. Bostic's initial projection was to see rates move about halfway to neutral by year-end. but the timeline remains highly contingent on economic developments and inflation trends.

Nagel advocates gradual rate cuts as ECB nears neutral

German ECB Governing Council member Joachim Nagel emphasized emphasized that ECB should avoid being on "autopilot" when determining the timing of interest rate cuts.

Speaking at the London School of Economics, he stressed that as ECB approaches the neutral rate, a "gradual approach" becomes more appropriate. Given the current uncertainty, he argued, "there is no reason to act hastily."

Nagel remains confident that inflation will return to 2% target by mid-year, saying, "We are not at our target, but I’m really very convinced that we will come to our target by the midst of this year." He also dismissed concerns of an inflation undershoot.

Bundesbank staff estimates place the neutral interest rate within a range of 1.8% to 2.5%, slightly below ECB’s current deposit rate of 2.75%.

However, Nagel warned against relying too heavily on neutral rate estimates, calling it “risky” to base monetary policy decisions on uncertain theoretical benchmarks. Instead, he emphasized that the ECB relies on a variety of financial, real-economic, and other indicators to guide its policy stance.

RBNZ survey shows rate cut expectations firm up

The latest RBNZ Survey of Expectations showed a mixed shift in inflation forecasts, with short-term price pressures edging higher but long-term expectations trending lower. The survey, nonetheless, reinforces anticipation of further rate cuts.

One-year-ahead inflation expectation rose from 2.05% to 2.15%, marking a slight uptick. However, two-year-ahead inflation expectations dipped from 2.12% to 2.06%, while five-year and ten-year expectations both declined by 11-12 basis points to 2.13% and 2.07%, respectively.

RBNZ's Official Cash Rate currently stands at 4.25% following 50bps reduction in last November. Survey respondents broadly expect another 50-bps cut to 3.75% by the end of Q1. The one-year-ahead OCR expectation also moved lower, falling 10bps to 3.23%, reinforcing the view that RBNZ will continue easing policy at a measured pace.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2387; (P) 1.2435; (R1) 1.2493; More...

Intraday bias in GBP/USD stays neutral and outlook is unchanged. Corrective rebound from 1.2099 could still extend higher. But upside should be limited by 38.2% retracement of 1.3433 to 1.2099 at 1.2609. On the downside, below 1.2331 minor support will turn bias to the downside for 1.2248 support. Firm break there will argue that the correction has completed and bring retest of 1.2099 low. However, decisive break of 1.2609 will raise the chance of near term reversal, and target 61.8% retracement at 1.2923.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

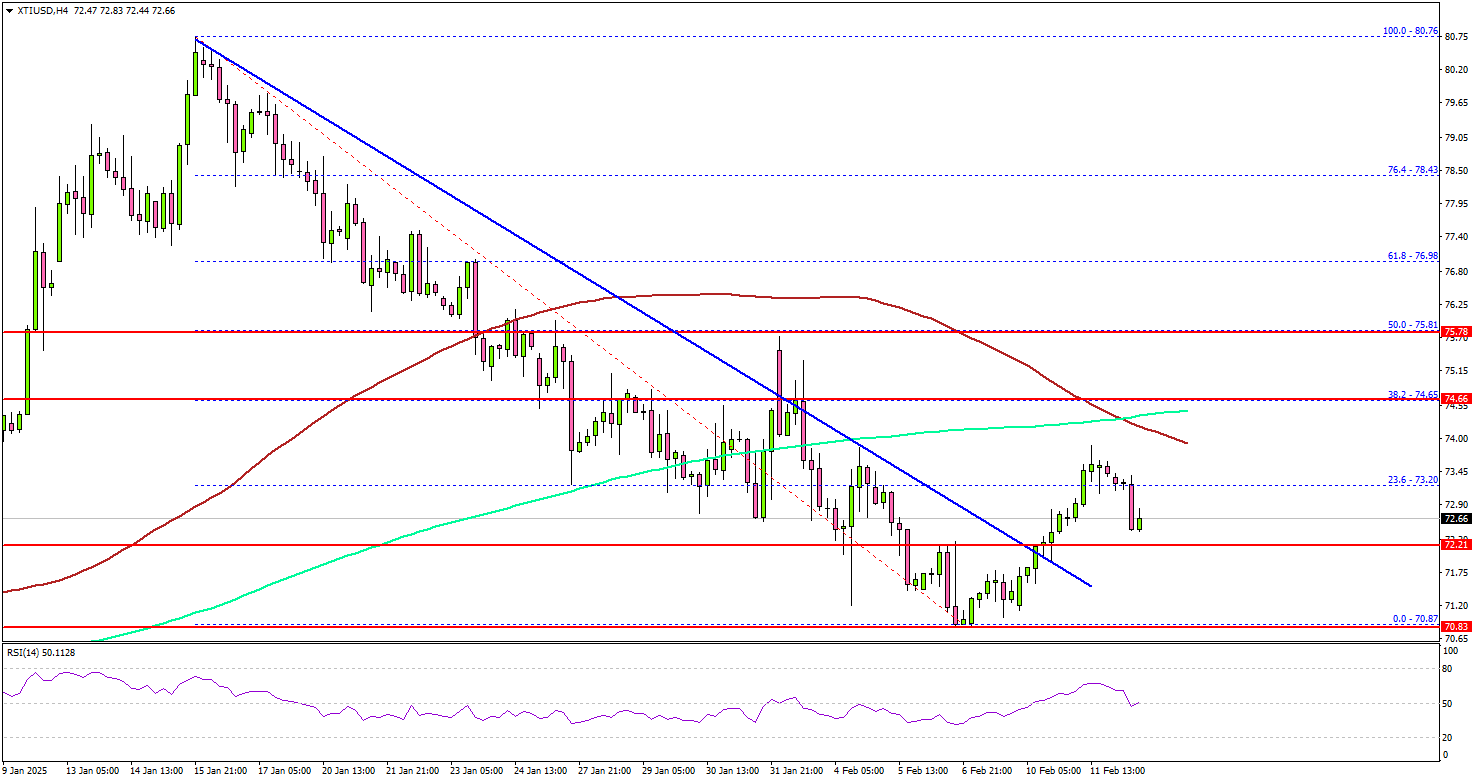

WTI Crude Oil Prices Meets Stiff Resistance—Will Bulls Push Through?

Key Highlights

- WTI Crude Oil prices started a recovery wave from the $70.80 support.

- It cleared a key bearish trend line with resistance at $72.20 on the 4-hour chart.

- Gold prices started a downside correction from the record high of $2,942.

- EUR/USD is attempting to start a fresh increase above the 1.0380 resistance level.

WTI Crude Oil Price Technical Analysis

WTI Crude Oil price started a major decline below $75.00. The price declined below the $73.00 and $72.00 levels before the bulls appeared.

Looking at the 4-hour chart of XTI/USD, the price settled below the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour). A low was formed at $70.87 and the price is now correcting some losses.

There was a move above the $71.50 and $72.00 levels. The price cleared a key bearish trend line with resistance at $72.20 on the same chart. It even spiked above the 23.6% Fib retracement level of the downward move from the $80.76 swing high to the $70.87 low.

On the upside, the price is facing hurdles near the $73.50 level. The main hurdle is now near the $74.00 zone and the 100 simple moving average (red, 4-hour), above which the price may perhaps accelerate higher.

In the stated case, it could even visit the $75.80 resistance. Any more gains might call for a test of the $78.00 resistance zone in the near term.

On the downside, the first major support sits near the $72.20 zone. A daily close below $72.20 could open the doors for a larger decline. The next major support is $70.80. Any more losses might send oil prices toward $68.00 in the coming days.

Looking at Gold, there was a strong increase above the $2,900 level and the price is now correcting some gains.

Economic Releases to Watch Today

- UK GDP for Q4 2024 (Preliminary) (QoQ) - Forecast -0.1%, versus 0% previous.

- US Initial Jobless Claims - Forecast 215K, versus 219K previous.

RBNZ survey shows rate cut expectations firm up

The latest RBNZ Survey of Expectations showed a mixed shift in inflation forecasts, with short-term price pressures edging higher but long-term expectations trending lower. The survey, nonetheless, reinforces anticipation of further rate cuts.

One-year-ahead inflation expectation rose from 2.05% to 2.15%, marking a slight uptick. However, two-year-ahead inflation expectations dipped from 2.12% to 2.06%, while five-year and ten-year expectations both declined by 11-12 basis points to 2.13% and 2.07%, respectively.

RBNZ's Official Cash Rate currently stands at 4.25% following 50bps reduction in last November. Survey respondents broadly expect another 50-bps cut to 3.75% by the end of Q1. The one-year-ahead OCR expectation also moved lower, falling 10bps to 3.23%, reinforcing the view that RBNZ will continue easing policy at a measured pace.

Nagel advocates gradual rate cuts as ECB nears neutral

German ECB Governing Council member Joachim Nagel emphasized emphasized that ECB should avoid being on "autopilot" when determining the timing of interest rate cuts.

Speaking at the London School of Economics, he stressed that as ECB approaches the neutral rate, a "gradual approach" becomes more appropriate. Given the current uncertainty, he argued, "there is no reason to act hastily."

Nagel remains confident that inflation will return to 2% target by mid-year, saying, "We are not at our target, but I’m really very convinced that we will come to our target by the midst of this year." He also dismissed concerns of an inflation undershoot.

Bundesbank staff estimates place the neutral interest rate within a range of 1.8% to 2.5%, slightly below ECB’s current deposit rate of 2.75%.

However, Nagel warned against relying too heavily on neutral rate estimates, calling it “risky” to base monetary policy decisions on uncertain theoretical benchmarks. Instead, he emphasized that the ECB relies on a variety of financial, real-economic, and other indicators to guide its policy stance.

Bostic: Fed needs more clarity before cutting rates

Atlanta Fed President Raphael Bostic signaled uncertainty over the timing of rate cuts, citing ongoing concerns about inflation and policy shifts under the Trump administration. Speaking at an event overnight, Bostic emphasized the need for "more clarity" before making any definitive moves on monetary policy.

He acknowledged the difficulty in assessing the current economic conditions, stating, “My view is until we have more clarity, it’s going to be impossible to make a judgment about where our policy should go and how fast and at what pace, and so we’re just going to have to get more information before we’re going to be able to move.”

He also provided his estimate for the neutral rate, which he sees in a range of 3%-3.5%. Currently, Fed's target range stands significantly higher at 4.25%-4.5%. Bostic's initial projection was to see rates move about halfway to neutral by year-end. but the timeline remains highly contingent on economic developments and inflation trends.

Fed’s Powell: New CPI data confirms “not there” yet on inflation

Fed Chair Jerome Powell acknowledged that the latest inflation data released yesterday confirms the US is making progress but is still “not there on inflation.”

Following January’s stronger-than-expected CPI report, Powell said in the Congressional testimony that Fed will "keep policy restrictive for now" to bring price pressures down.

Powell also underlined that the "economy is strong, the labor market is solid" allowing the Fed to keep a tight policy stance and wait for inflation to ease further.

He also emphasized that one month of higher readings should not be interpreted as a complete reversal of the disinflation trend, especially given that Fed’s preferred inflation measure, the Personal Consumption Expenditures index, typically runs below CPI.

Dow Jones (DJIA) Analysis: Inflation Impact and Market Recovery

- The Dow Jones initially fell following a US inflation report but recovered somewhat.

- US consumer prices saw their biggest jump in over a year, supporting the Federal Reserve’s stance on interest rates.

- Fed Chair Powell cautioned against reading too much into the inflation data, citing the PCE inflation gauge as the preferred measure.

- Uncertainty remains in the markets regarding how tariffs will impact global growth and inflation.

The Dow Jones fell around 400 points on Wednesday following a hot US inflation report. However, the Dow has since recovered around 300 points to trade 0.45% down for the day at the time of writing.

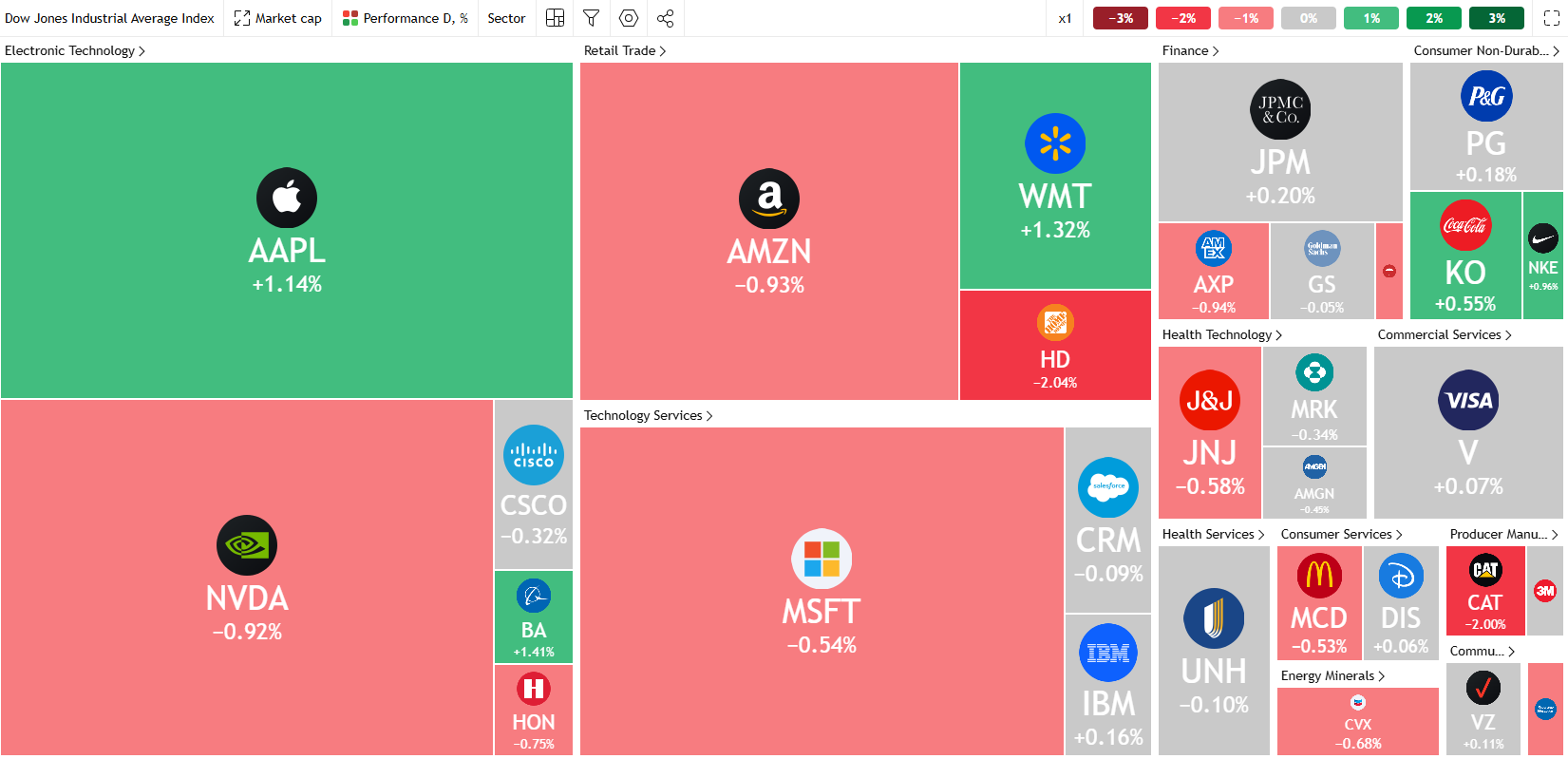

DJIA Heatmap at the time of writing

Source: TradingView

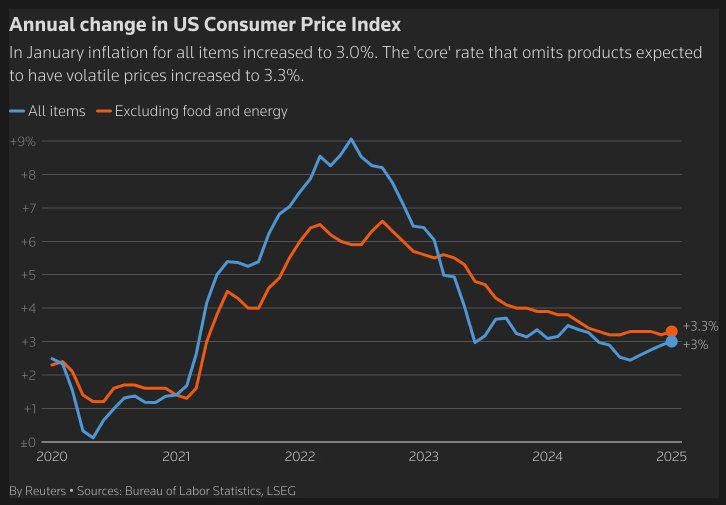

US CPI Shock – A Cautionary Tale?

Consumer prices in the U.S. saw their biggest jump in almost a year and a half this January. This supports the Federal Reserve’s stance and something that Fed Chair Powell mentioned on Wednesday. The Fed Chair remained steadfast in his assessment that the central bank isn’t ready to lower interest rates yet, especially with uncertainty surrounding the economy.

Source: LSEG

Fed Chair Powell began his second day of testimony before Congress with inflation and rate cuts remaining key. Fed Chair Powell did however mention that he would caution against reading too much into today’s inflation data, reminding everyone of the Fed’s preferred inflation gauge, the PCE data.

Some other key quotes from Fed chair Powell below:

- WE WANT TO SEE MORE PROGRESS ON INFLATION

- DIDNT SEE MUCH PROGRESS ON CORE INFLATION LAST YEAR

- WE HAVE THE LUXURY OF BEING ABLE TO WAIT FOR THAT, GIVEN STRONG ECONOMY

- LAST FEW JOB REPORTS HAVE SHOWN SIGNIFICANT JOB CREATION, MAY HAVE TICKED UP AT END OF YEAR

- OFFER A NOTE OF CAUTION ON TODAY’S CPI READING; WE TARGET PCE INFLATION WHICH IS A BETTER MEASURE

- WE’LL KNOW WHAT PCE READINGS ARE LATE TOMORROW, AFTER PPI DATA

Despite Fed Chair Powell’s comments I do not think that this report should be taken lightly. ANy future inflation readings will likely feel some strain from tariffs, which could push inflation even higher.

According to reports, President Trump’s trade advisors are preparing reciprocal tariffs on every country that charges duties on US imports.

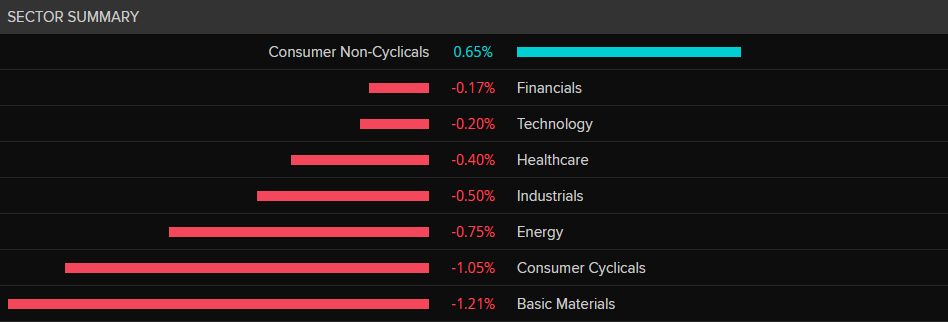

When looking at a sector breakdown, the only sector up at the time of writing was consumer non-cyclicals with basic materials down the most.

Dow Jones Sector Performance

Source: LSEG

Apple reversed higher post CPI to trade in the green for the day, but fellow magnificent 7 stocks continued to toil with NVIDIA and Amazon still in the red for the day.

Despite the CPI print markets remain cautious as there is still a lot of uncertainty in regard to how tariffs will impact both global growth and inflation.

Technical Analysis

Dow Jones

From a technical standpoint, the Dow Jones has recovered quite well post the CPI release.

The index is trading at the support level 44450 having bounced out of a key confluence area earlier in the day.

The overall trend on the daily is a mixed one with a lower high finding no follow through to print a lower low. These conditions are being seen in a few different asset classes and a sign of the uncertainty prevalent in markets.

Immediate resistance rests at 44759 and 45097, with immediate support at 44200 and 43800.

Dow Jones (US30) Daily Chart, February 12, 2025

Source: TradingView (click to enlarge)

Support

- 44200

- 43800

- 43400

Resistance

- 44759

- 45097

- 45500

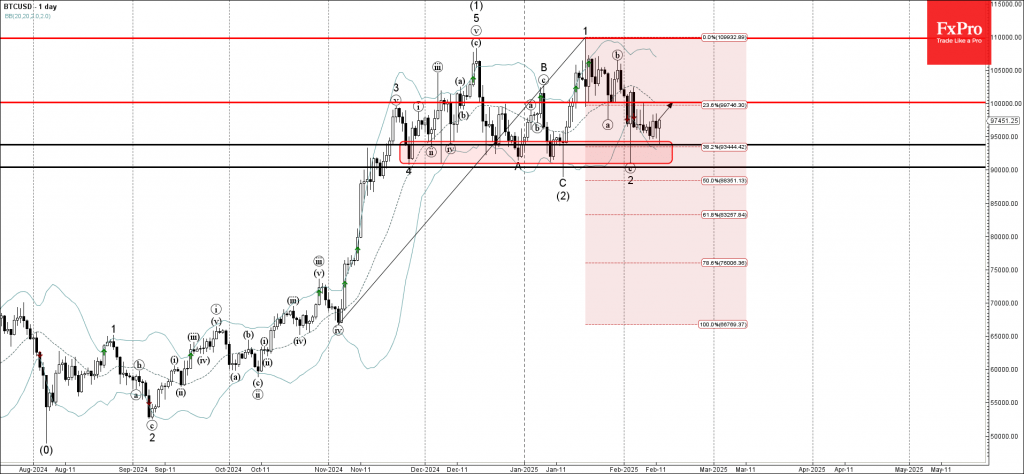

Bitcoin Wave Analysis

- Bitcoin reversed from the support area

- Likely to rise to resistance level 100,000.00

Bitcoin cryptocurrency recently reversed up from the support area between support levels 93775.00 and 90000.00. This support area has stopped the previous corrections 4, A, C and 2, as can be seen below.

This support area was further strengthened by the lower daily Bollinger Band and by the 38.2% Fibonacci correction of the upward price impulse from November.

Given the clear daily uptrend, Bitcoin cryptocurrency can be expected to rise to the next round resistance level 100,000.00.