Sample Category Title

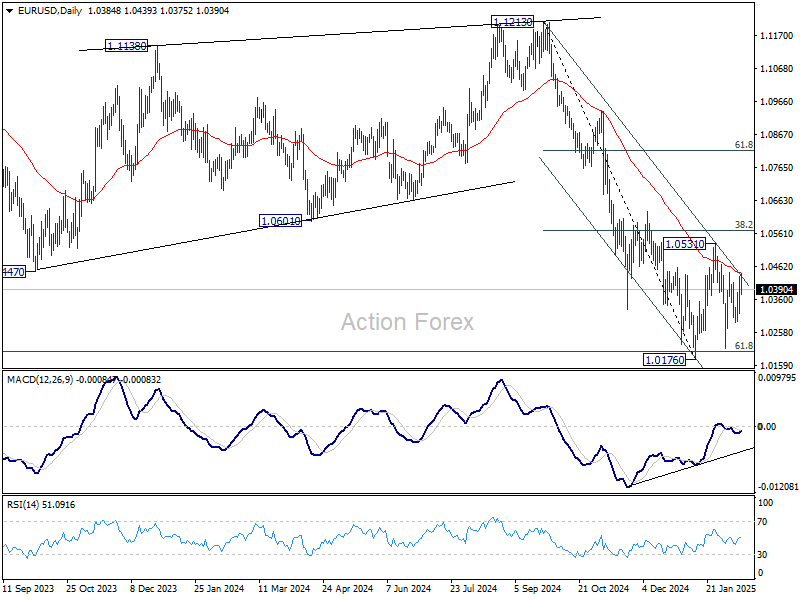

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0309; (P) 1.0345; (R1) 1.0398; More...

Intraday bias in EUR/USD remains neutral as consolidation from 1.0176 is still extending. Outlook will remain bearish as long as 38.2% retracement of 1.1213 to 1.0176 at 1.0572 holds. On the downside, break of 1.0176 will resume whole fall from 1.1213. However, decisive break of 1.0572 will raise the chance of reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

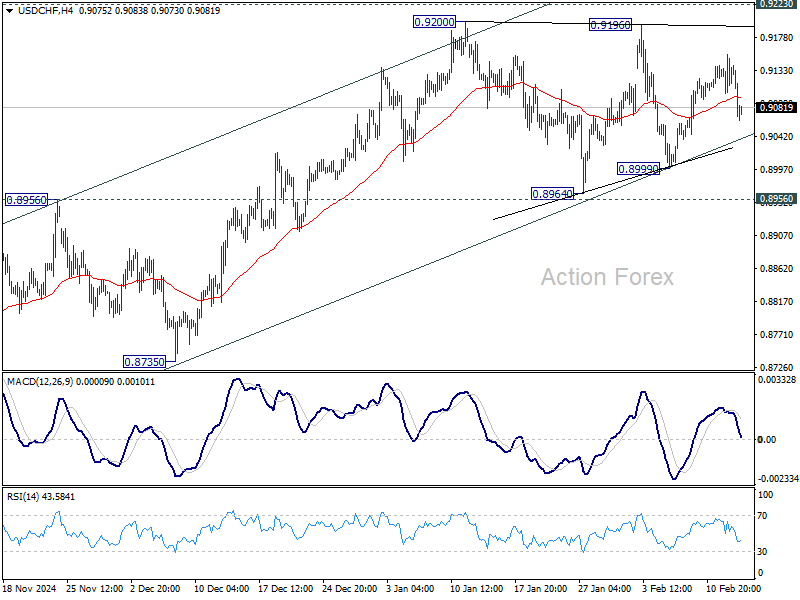

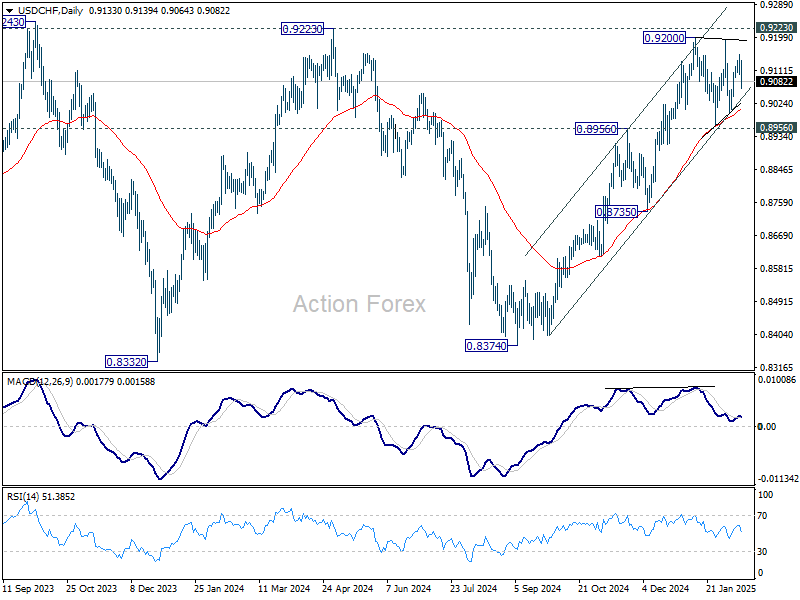

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9107; (P) 0.9132; (R1) 0.9160; More…

Intraday bias in USD/CHF remains neutral as consolidation from 0.9200 is still extending. Outlook stays bullish with 0.8956/64 support zone intact. On the upside, firm break of 0.9200/9223 will resume the whole rally from 0.8374 and carry larger bullish implication. However, sustained break of 0.8964 will be a sign of reversal and turn bias back to the downside.

In the bigger picture, decisive break of 0.9223 resistance will argue that whole down trend from 1.0342 (2017 high) has completed with three waves down to 0.8332 (2023 low). Outlook will be turned bullish for 1.0146 resistance next. Nevertheless, rejection by 0.9223 will retain medium term bearishness for another decline through 0.8332 at a later stage.

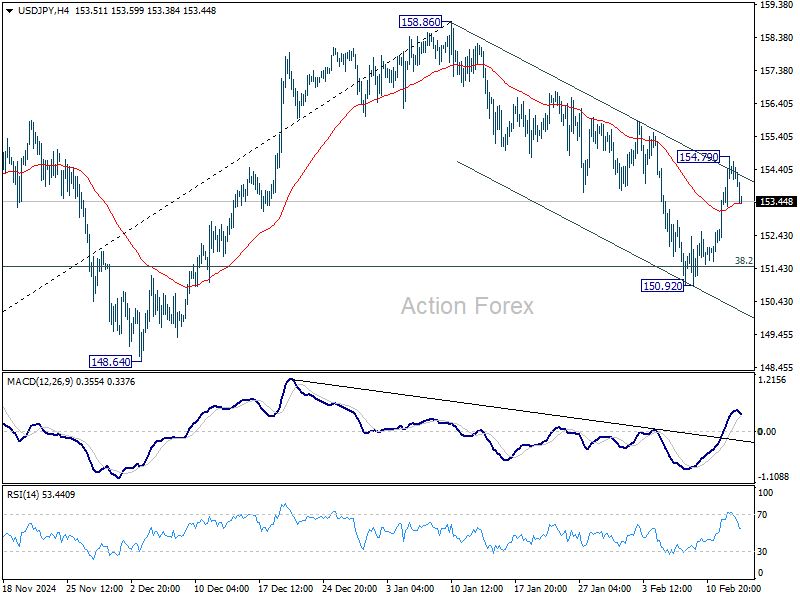

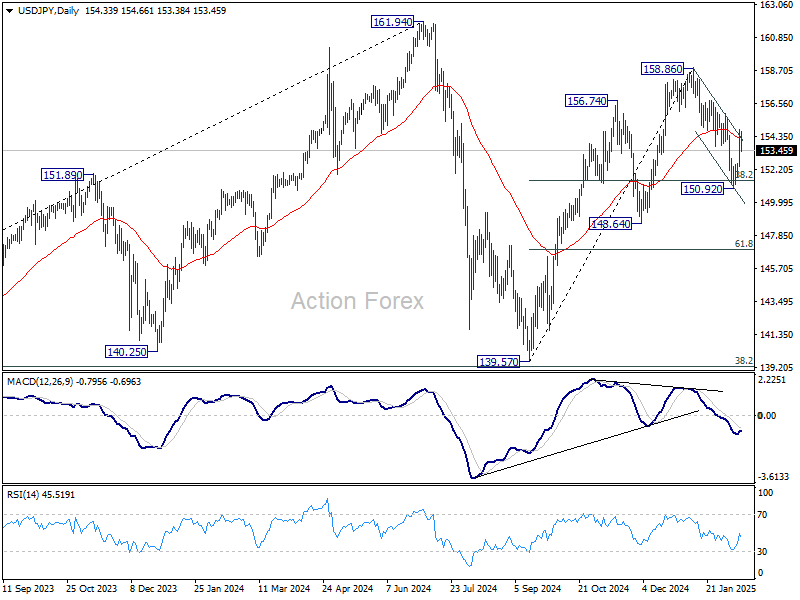

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 152.92; (P) 153.86; (R1) 155.35; More...

USD/JPY retreated after hitting 154.79 and intraday bias is turned neutral first. Outlook is unchanged that corrective fall from 158.86 should have completed at 150.92 already. Risk will stay on the upside as long as 150.92 support holds. Above 154.79 will target a retest on 158.86 first. Firm break there will resume whole rally from 139.57 to retest 161.94 high.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

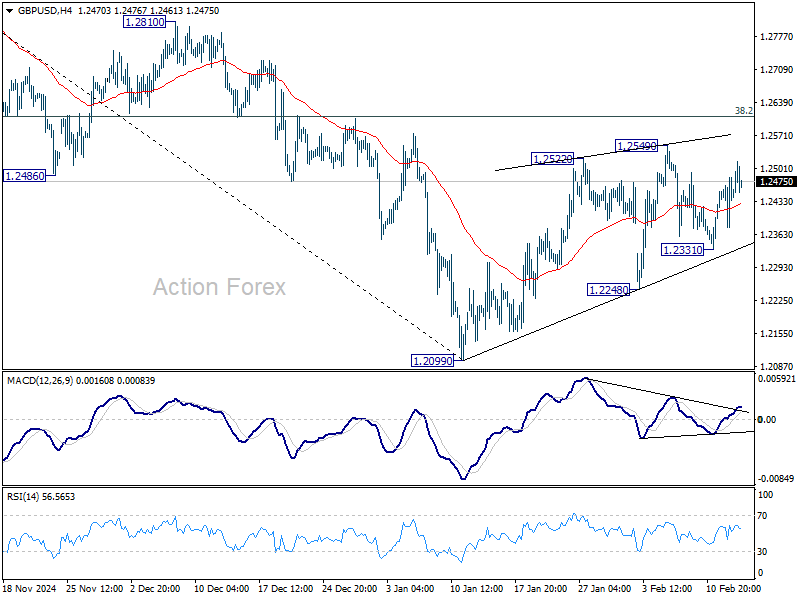

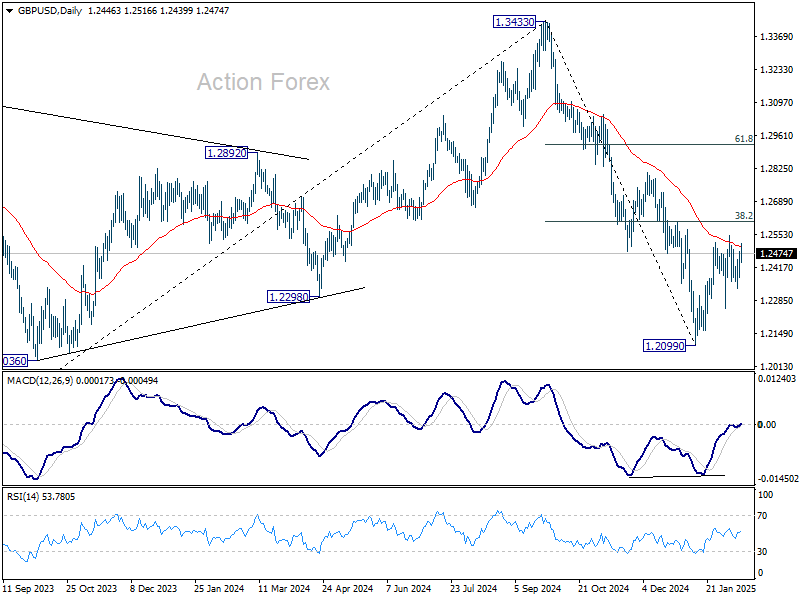

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2387; (P) 1.2435; (R1) 1.2493; More...

Outlook in GBP/USD is unchanged and intraday bias stays neutral. Corrective rebound from 1.2099 could still extend higher. But upside should be limited by 38.2% retracement of 1.3433 to 1.2099 at 1.2609. On the downside, below 1.2331 minor support will turn bias to the downside for 1.2248 support. Firm break there will argue that the correction has completed and bring retest of 1.2099 low. However, decisive break of 1.2609 will raise the chance of near term reversal, and target 61.8% retracement at 1.2923.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

Dollar Muted Despite Strong PPI, Awaits Reciprocal Tariffs

The currency markets are treading cautiously, with traders showing little reaction to stronger-than-expected US PPI data and a better-than-anticipated jobless claims report. Despite these inflationary signals, Dollar has struggled to gain further traction, as market participants hold their positions ahead of a highly anticipated announcement on US "reciprocal tariffs" from President Donald Trump. The announcement, expected later today in a news conference at the Oval Office, could provide a clearer picture of how US trade policy will evolve and its impact on global markets.

While Fed’s restrictive stance on interest rates remains intact, this week's hot CPI and PPI data suggest that inflation is proving more persistent than policymakers had hoped. Chair Jerome Powell has already reinforced that Fed is in no hurry to cut rates, and expectations for rate reductions in the first half of the year have now diminished. Market focus will now shift to upcoming US retail sales figures and additional comments from Fed officials, as traders assess how these data points might influence the central bank’s next policy moves.

Sterling briefly found some boost after stronger-than-expected UK GDP data, which helped ease immediate concerns over a recession. However, the currency’s gains were short-lived, as investors remain cautious about the country’s sluggish economic outlook. While BoE has signaled a path of gradual easing, the market are more conservative than BoE guidance, with traders still pricing in just two rate cuts before year-end. Given the uncertainty around inflation and growth, the pace of BoE rate cuts will remain a key point of debate in the coming months.

For the day, Swiss Franc leads currency gains as Japanese Yen follows behind, while Sterling holds firm too. On the weaker end, Australian and New Zealand Dollars are struggling. Dollar, despite its inflation-fueled rally earlier in the week, has lost momentum, as traders await further trade policy developments. Euro and Canadian Dollar are stuck in the middle of the pack.

In Europe, at the time of writing, FTSE is down -0.56%. DAX is up 1.64%. CAC is up 1.40%. UK 10-year yield is down -0.045 at 4.493. Germany 10-year yield is down -0.050 at 2.431. Earlier in Asia, Nikkei rose 1.28%. Hong Kong HSI fell -0.20%. China Shanghai SSE fell -0.42%. Singapore Strait Times rose 0.21%. Japan 10-year JGB yield rose 0.0028 to 1.350.

US PPI up 0.3% mom, 3.5% yoy in Jan, above expectations

US PPI for final demand rose by 0.4% mom in January, exceeding market expectations of 0.2% mom.

Final demand services increased by 0.3% mom, while final demand goods rose by 0.6% mom. Core PPI measure, which strips out volatile food, energy, and trade services, climbed 0.3% mom.

On an annual basis, headline PPI accelerated to 3.5% yoy, surpassing forecasts of 3.2% yoy. Core PPI followed closely, advancing 3.4% yoy.

US initial jobless claims falls to 213k vs exp 221k

US initial jobless claims fell -7k to 213k in the week ending February 8, below expectation of 221k. Four-week moving average of initial claims fell -1k to 216k.

Continuing claims fell -36k to 1850k in the week ending February 1. Four-week moving average of continuing claims fell -1k to 1872k.

Eurozone industrial production falls -1.1% mom in Dec, EU down -0.8% mom

Eurozone industrial production fell by -1.1% mom in December, significantly worse than the market expectation of -0.6% mom. The decline was driven by sharp contractions in intermediate and capital goods, while non-durable consumer goods provided some offset.

Breaking down the data, intermediate goods production declined by -1.9% mom. The production of capital goods fell even further, down -2.6% mom. Durable consumer goods also posted a modest decline of -0.7% mom. On the other hand, energy production rose by 0.5% mom, and non-durable consumer goods surged by 5.1% mom.

At the broader EU level, industrial production contracted by -0.8% mom, with Belgium (-6.8%), Portugal (-4.4%), and Austria (-3.3%) suffering the steepest declines. Meanwhile, Ireland (+8.2%), Luxembourg (+6.7%), and Croatia (+6.3%) posted strong rebounds.

Swiss inflation softens again as CPI slows to 0.4% in Jan

Switzerland’s CPI declined by -0.1% mom in January, in line with market expectations. Core CPI, which excludes fresh and seasonal products, energy, and fuel, also dropped by -0.1% mom. While domestic product prices ticked up by 0.1% mom, the steep -0.7% mom decline in imported product prices suggests that external factors continue to exert deflationary pressure on the Swiss economy.

On a year-over-year basis, headline inflation eased from 0.6% yoy to 0.4% yoy, also matching expectations. However, core CPI edged higher to 0.9% yoy from 0.7% yoy. Domestic product inflation slowed from 1.5% yoy to 1.0% yoy, reflecting weaker demand and subdued price pressures in the local economy. Meanwhile, imported product prices remained in deflationary territory, improving slightly from -2.2% yoy to -1.5% yoy.

UK GDP surprises to the upside, services lead the growth

The UK economy outperformed expectations in December, with GDP expanding by 0.4% mom, significantly stronger than the 0.1% growth forecast. The services sector led the way, posting 0.4% monthly growth, while production output also rebounded, rising by 0.5%. However, the construction sector remained weak, contracting -0.2% mom.

For Q4 as a whole, GDP increased by 0.1% qoq, defying expectations for a -0.1% contraction. Services grew by 0.2% in Q4, maintaining its position as the primary growth driver, while construction saw a moderate expansion of 0.5%. However, industrial production was a notable drag, shrinking by -0.8%.

For full-year 2024, GDP increased by 0.8% compared to 2023, a modest but better-than-feared outcome given the economic uncertainties. Services expanded by 1.3%, cushioning the economy, while production sector contracted by -1.7%, and construction grew slightly by 0.4%.

RBNZ survey shows rate cut expectations firm up

The latest RBNZ Survey of Expectations showed a mixed shift in inflation forecasts, with short-term price pressures edging higher but long-term expectations trending lower. The survey, nonetheless, reinforces anticipation of further rate cuts.

One-year-ahead inflation expectation rose from 2.05% to 2.15%, marking a slight uptick. However, two-year-ahead inflation expectations dipped from 2.12% to 2.06%, while five-year and ten-year expectations both declined by 11-12 basis points to 2.13% and 2.07%, respectively.

RBNZ's Official Cash Rate currently stands at 4.25% following 50bps reduction in last November. Survey respondents broadly expect another 50-bps cut to 3.75% by the end of Q1. The one-year-ahead OCR expectation also moved lower, falling 10bps to 3.23%, reinforcing the view that RBNZ will continue easing policy at a measured pace.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2387; (P) 1.2435; (R1) 1.2493; More...

Outlook in GBP/USD is unchanged and intraday bias stays neutral. Corrective rebound from 1.2099 could still extend higher. But upside should be limited by 38.2% retracement of 1.3433 to 1.2099 at 1.2609. On the downside, below 1.2331 minor support will turn bias to the downside for 1.2248 support. Firm break there will argue that the correction has completed and bring retest of 1.2099 low. However, decisive break of 1.2609 will raise the chance of near term reversal, and target 61.8% retracement at 1.2923.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

US initial jobless claims falls to 213k vs exp 221k

US initial jobless claims fell -7k to 213k in the week ending February 8, below expectation of 221k. Four-week moving average of initial claims fell -1k to 216k.

Continuing claims fell -36k to 1850k in the week ending February 1. Four-week moving average of continuing claims fell -1k to 1872k.

US PPI up 0.3% mom, 3.5% yoy in Jan, above expectations

US PPI for final demand rose by 0.4% mom in January, exceeding market expectations of 0.2% mom.

Final demand services increased by 0.3% mom, while final demand goods rose by 0.6% mom. Core PPI measure, which strips out volatile food, energy, and trade services, climbed 0.3% mom.

On an annual basis, headline PPI accelerated to 3.5% yoy, surpassing forecasts of 3.2% yoy. Core PPI followed closely, advancing 3.4% yoy.

EURUSD Found Buyers After 3 Waves Pull Back

Hello fellow traders,

In this technical article we’re going to take a look at the Elliott Wave charts charts of EURUSD forex pair published in members area of the website. As our members know, recently EURUSD made a 3-wave pullback that completed right at the equal legs level. In the following sections, we will analyze the charts and explain the Elliott Wave forecast.

EURUSD Elliott Wave 1 Hour Chart 02.07.2025

EURUSD ended cycle from the 1.0205 low as 5 waves structure- wave ((i)) black. The pair is currently giving us pull back against the 1.0205 low. Equal legs area is already reached at 1.0320-1.0262 area. We are aware that pull back can complete any moment. Although we expect to see rally from the marked area, we don’t recommend forcing the trades at this stage.

EURUSD Elliott Wave 1 Hour Chart 02.07.2025

The pair found buyers in the 1.0320-1.0262 area as expected and completed the correction at the 1.0286 low. We’d like to see a break of the ((i)) black peak to confirm further upward movement toward the 1.05129-1.05671 area.

UK GDP Beats Forecast, Gives Sterling a Lift

The British pound has edged higher on Thursday. GBP/USD is trading at 1.2460, up 0.15% on the day.

UK GDP beats forecast

The UK economy ended 2024 on a high note, as GDP rose 0.4% m/m in December. This was the fastest pace of growth in nine months and blew past the market estimate of 01.%. The surprise gain was driven by increases in services and manufacturing activity. Annually, the economy expanded 1.5% in December, its best showing since Oct. 2022. This followed a revised 1.1% gain in November and beat the market estimate of 1%.

The surprise to the upside in GDP is welcome news but is tempered by the fact that much of the growth may have been due to government spending, as business investment decreased in the fourth quarter and consumer spending was flat. GDP quarterly growth was only 0.1%, an indication that the UK economy is still weak.

Fed’s Powell comments on higher-than-expected inflation report

Fed Chair Jerome Powell testified before the House Financial Services Committee on Wednesday, just after the release of January’s hot inflation report. Headline and core CPI were both higher than expected, with headline inflation accelerating for a fourth consecutive month. Powell told lawmakers that the Fed had made “great progress” on inflation, but acknowledged there was more work to do. Powell said that the Fed doesn’t “get excited about one or two bad readings” but there are concerns that inflation could be moving in the wrong direction, away from the Fed’s 2% target.

The Fed’s battle with inflation has also become more complicated with President Donald Trump’s promise to impose tariffs on US trading partners. Trump has called on the Fed to lower interest rates, raising fears that he is trying to dictate monetary policy to the Fed, which is suppose to act independent of political considerations.

GBP/USD Technical

- GBP/USD tested resistance at 1.2493 earlier. Above, there is support at 1.2541

- 1.2435 and 1.2387 are the next support levels

New Zealand Dollar Calm After Inflation Expectations Ease

The New Zealand dollar is drifting on Thursday. NZD/USD is trading at 0.5639 in the European session, down 0.04% on the day.

NZ inflation expectations dip to 2.06% in Q1 2025

New Zealand business inflation expectations didn’t show much change in the first quarter. Two-year inflation expectations, which are closely monitored by the central bank, edged lower to 2.06%, compared to 2.12% in the fourth quarter of 2024 and higher than the forecast of 1.8%. The business sector expects inflation to remain subdued, which fits in nicely with the fact that actual inflation also remains low. In the fourth quarter, inflation was unchanged at 2.2% y/y, close to the Reserve Bank of New Zealand’s target of 2%.

The RBNZ meets on Feb. 19 and a rate cut is fully priced in, with the probability of a quarter-point or half-point cut at around 50/50. This could mean a live meeting with investors holding their breath as to the extent of the rate cut. The RBNZ has proven it can be aggressive, having chopped 125 basis points since starting the easing cycle last August. The cash rate is down to 4.25% but this is still too high, given the weak New Zealand economy.

The weak New Zealand dollar supports the case for the RBNZ to deliver a modest quarter-cut next week. The Federal Reserve is sounding more hawkish and is looking at only one or two rate cuts this year. If the RBNZ slices rates by a half-point next week it will significantly widen the New Zealand/US rate differential and put pressure on the kiwi, which has plummeted about 11% since Oct. 1.

Federal Reserve Chair Jerome Powell testified before the Senate Banking Committee on Wednesday and reiterated that the Fed is in no hurry to lower rates. The softer-than-expected inflation report, which came out just ahead of Powell’s testimony, will raise concerns that inflation is rebounding. If the next inflation release is also higher than expected, we could see calls for the Fed to consider raising rates.

NZD/USD Technical

- NZD/USD is testing support at 0.5638. Below, there is support at 0.5604

- There is resistance at 0.5676 and 0.5710