Sample Category Title

Yen’s Roller-Coaster Ride Continues

The Japanese yen continues to take investors and traders on a roller-coaster ride. After climbing 1.2% on Wednesday, USD/JPY gave almost all of those gains on Thursday, declining 1.05%. The yen has taken a breather today and is trading at 152.63 in the European session, down 0.19% on the day.

Japan’s PPI keeps accelerating

Producer prices in Japan climbed 4.2% y/y in January, up from an upwardly revised 3.9% in December and above the market estimate of 4.0%. PPI accelerated for a fifth consecutive month and posted its highest level since May 2023. The gain was driven by higher food prices. Monthly, PPI eased to 0.3%, down from 0.4% in December and in line with the market estimate.

The hotter-than-expected PPI report reflects persistent inflationary pressures and follows the core CPI reading for December, which hit 3%, its highest annual level in 16 months. With inflation moving higher, expectations are growing that the Bank of Japan will raise interest rates further in the near term.

The Bank has signaled that it will raise rates if wage growth increases and keeps inflation sustainable at the BoJ’s 2% target. In anticipation of higher interest rates, Japan’s 10-year bond yields have been rising and are close to a 15-year high.

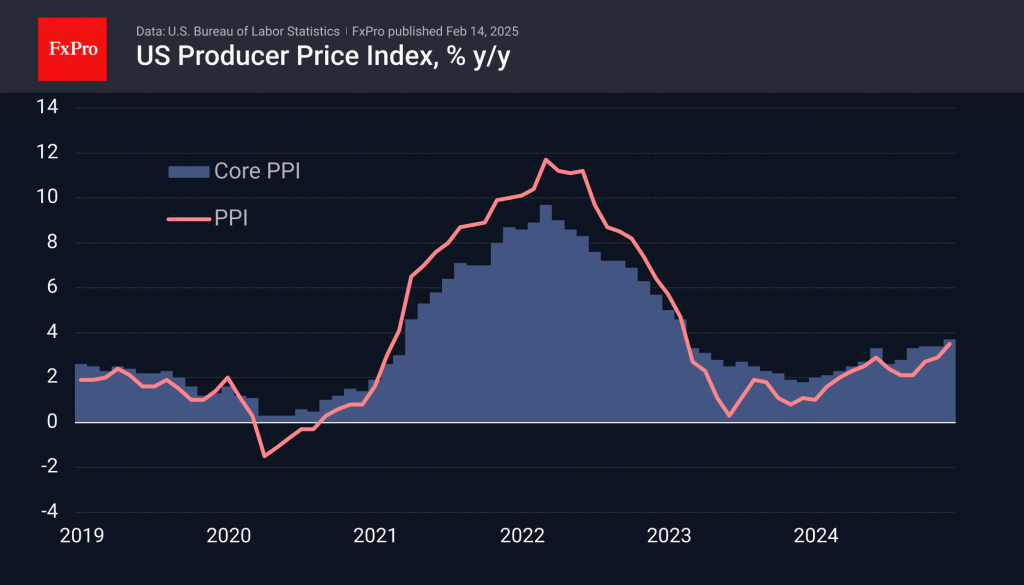

In the US, the PPI release showed little change in January. PPI rose 0.4% m/m, after an upwardly revised 0.5% gain in December. This was higher than the market estimate of 0.3%. Annually, PPI rose 3.5%, after an upwardly revised 3.5% gain in December.

The US wraps up the week with the January retail sales report. The markets are bracing for a contraction, with a market estimate of -0.1%, after the 0.4% gain in December. Annually, retail sales are expected to dip to 3.7%, after a 3.9% gain in December.

USD/JPY Technical

- USD/JPY is testing support at 152.73. Below, there is support at 152.29

- 153.00 and 153.44 are the next resistance lines

Dollar Has Rolled Back to Local Lows

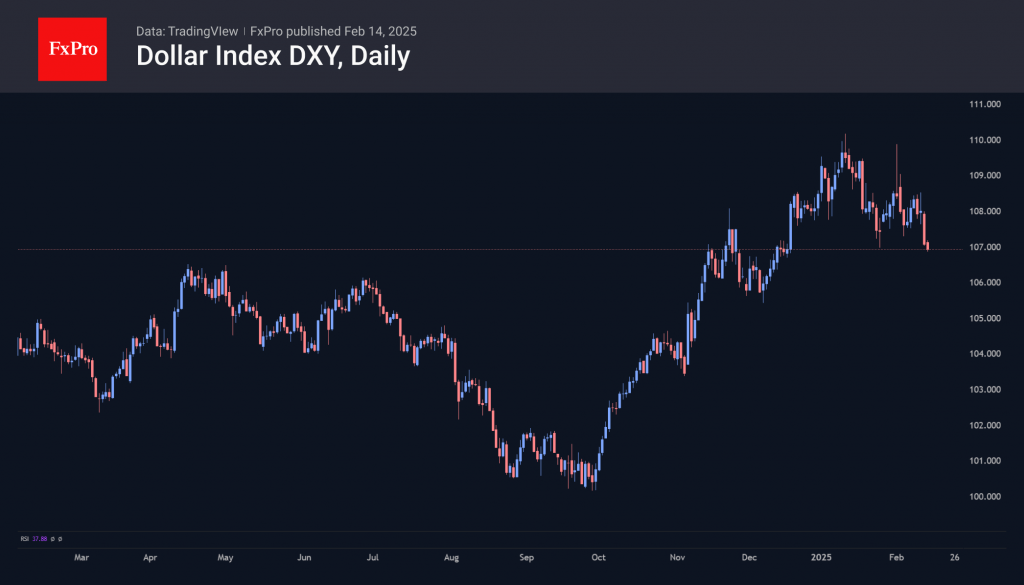

The US dollar has retreated to the lower levels it has visited multiple times since the end of January. The decline at the end of last week was driven by reports that US ‘retaliatory’ tariffs have been postponed until April, allowing time for negotiations and potential easing of terms. This development proved more significant for the dollar than the Federal Reserve’s further hawkish stance and the unexpected rise in inflation.

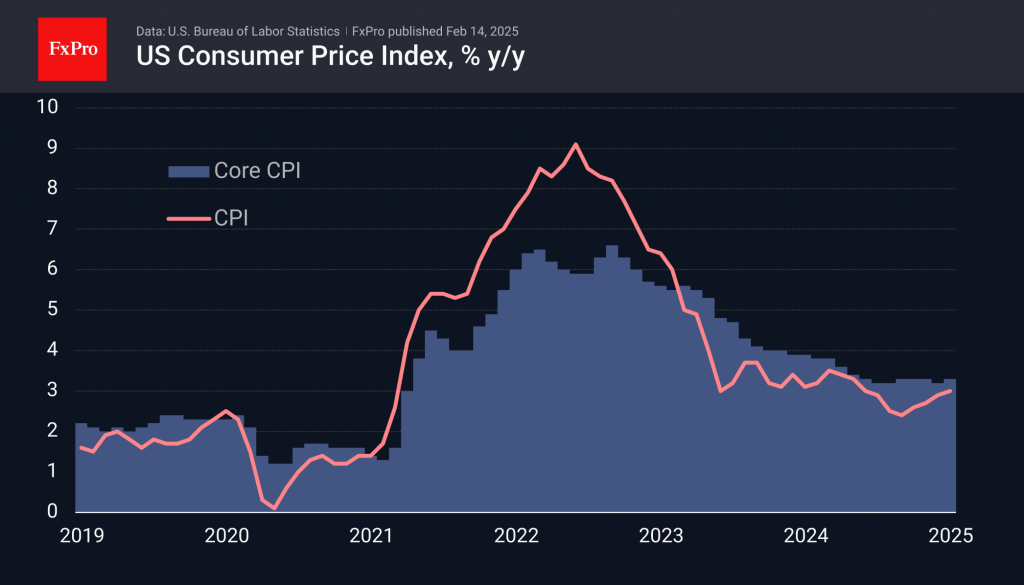

Data released mid-week indicated that consumer inflation accelerated to 3.0% year-over-year, marking a six-month high and a notable increase from September’s low of 2.4%. Core inflation remained stable at 3.3% over the past eight months. Additionally, the producer price index, a leading indicator of inflation, rose to 3.5% year-over-year, the highest rate since early 2023.

An inflation rate above the target compels the Federal Reserve to adopt a restrictive approach, maintaining the key interest rate above inflation to suppress it. This strategy may present a bullish scenario as other major central banks signal their intent to ease policy.

Narket Reaction to Tariff Announcement Muted

Markets

US yields easily returned most of Wednesday’s rise incurred after stronger than expected January CPI data. The move is telling on the current market positioning/assessment. The ‘correction’ started after and despite higher than expected US January PPI data. Markets apparently concluded that the bar is extremely high for the Fed to consider raising rates from current levels (economically and politically). With no more than one Fed rate cut discounted toward the end of this year, markets risk/reward see some value in US bonds after Wednesday’s sell-off. Treasuries started a comeback to finish the day between 4.8 bps (2-y) and 9.5 bps (30-y) lower. A $25bn 30-y US Treasury auction tailed, but after all didn’t hamper the intraday rally. German yields followed the US move with yields declining between 4.9 bps (2-y) and 6 bps (5-10y). Interesting/remarkable: the EMU yield move decoupled from an impressive rally in European equities. This is at least partially inspired by market hope that (US-led) negotiations on the war in Ukraine might at least remove one of the uncertainties for the region’s ailing economy. The Eurostoxx 50 index closed just a whisker away from the March 2000 all-time record! After the close of European markets, US president Trump announced a wide-ranging plan to impose reciprocal tariffs on the US’s trading partners. The system will work on a country-by-country basis. It will not only take into account tariffs, but also non-tariff barriers including regulations that are seen as unfavourble for US trade, subsidies and domestic taxing policy e.g. VAT and sales taxes that are applied by some trading partners. Trump also indicated that he intends to put in place additional taxes on autos, chips and pharmaceuticals on top of the reciprocal system. The market reaction to the announcement was muted. As it can take until April (or maybe later) for the system to be operational, markets conclude that there is still time to negotiate. US equity gains accelerated even after the announcement with major US indices closing between 0.7% (Dow) and 1.50% (Nasdaq) higher. The broad risk-on and sharp decline in US yields put the dollar on the backfoot. The DXY index dropped to 107.31 (from 107.87). USD/JPY almost fully reversed Wednesday’s jump higher (close 152.8). EUR/USD closes at 1.046.

Risk sentiment remains constructive in Asian dealings this morning. Later today, the calendar contains details of EMU Q4 GDP growth (0% Q/Q) and US retail sales. Headline retail sales are expected to decline by 0.2% M/M (weather-related). Control group sales are expected at 0.3% M/M. Considering this week’s price action, (FI and FX) markets might be a bit more sensitive to a weaker than to a stronger than expected figure. We also keep an eye at EUR/USD. The 1.0533 January top is the next reference on the technical charts. Both euro strength and USD softness might be in play. DXY also nears key support just below 107.

News & Views

Swiss National Bank board member Tschudin showed willingness to return to sub-zero interest rates if necessary to achieve price stability (inflation between 0% and 2%). “It allows us to steer the rate differential also in a low-interest environment in a way that the franc becomes less attractive than other currencies and therefore doesn’t appreciate excessively.” The key Swiss policy rate currently stands at 0.50%. The comments came after Swiss data yesterday showed inflation easing further in January (-0.1% M/M & 0.4% Y/Y). While not a fan, SNB president Schlegel earlier kept the option of negative policy rates open as well. Tschudin added that the SNB will continue to intervene in FX markets to prevent a too strong Swiss franc even as it risks being labeled a currency manipulator by the US. The EUR/CHF 0.92-0.93 bottom is becoming stronger with the pair testing first resistance in the 0.95 area.

The European Commission’s vice-president in charge of digital policy told the Financial Times that the EU wanted to help and support companies when applying AI rules. Virkkunen wants to cut back tech regulation: “we are committed to cut bureaucracy and red tape”. The EC has this week withdrawn a planned AI liability directive and an upcoming code of practice on AI, expected in April, will limit reporting requirements to what is included in the existing rules. Virkkunen insisted that the deregulatory push in an EU-initiative and not dependent on the US.

Anxious Optimism

The US is planning to impose tit-for-tat tariffs globally, but studying tariffs case by case requires time and the tariffs won’t be effective until April. I don’t know if you could call it good news, but the markets’ reaction suggests that the latter has been perceived as good news and helped keeping appetite afloat yesterday. The US dollar index was sharply sold despite the broadening tariff war, despite the rising worries about the US/Russian negotiations about Ukraine – which do not involve Ukraine nor the Europeans, and despite the mix of stronger-than-expected US PPI and better-than-expected weekly jobs figures.

One of the reasons that could explain the weakness of the yields and the dollar on normally dollar-supportive inflation and tariff news is the fact that some of the components in that PPI report that feed into the PCE index – the Federal Reserve’s (Fed) favourite gauge of inflation – pointed at weakness (these items include healthcare and airfares). But given that Jerome Powell, himself, told US politicians this week about his concerns about inflation and how the progress has stalled since last year, I believe that a part of yesterday’s selloff has to do with investors closing the crowded long dollar positions, rather than a meaningful shift in the macroeconomic dynamics.

In Europe

The final German inflation figures released yesterday printed negative monthly numbers in January. The Spanish figures will likely point at slowing price pressures in Spain as well, while the Eurozone’s GDP will confirm a no growth in Q4. The combination of slowing inflation and zero growth could only back the idea of further rate cuts from the European Central Bank (ECB) at a time the bets for Fed rate cuts are being kicked down the road. Therefore, the weakness of the US dollar will likely remain limited and the strength of the euro against the dollar will likely be topped. But in the short run, a soft looking retail sales data from the US could keep the USD under pressure, letting the dollar rally lose some more steam. This being said, many traders may chose not to go short the US dollar into the weekend. You never know, two days is a long time with Donald Trump.

In equities, though, the European stocks continue to ignore the tariff threats and chose to surf on the rotation trade. The Stoxx 600 rallied to a fresh ATH yesterday, while FTSE 100 also hit a fresh high but gave back gains and closed in the negative. Robust earnings and favourable ECB expectations support the positive move. On the individual front, the German champion Siemens – which generously contributes to the Stoxx 600 gains – jumped more than 7% yesterday after announcing a set of better-than-expected Q4 results, while encouraging earnings from Michelin boosted mood among carmakers. Stellantis for example gained 4.5% yesterday. They will report their earnings on February 26th, but they had announced a 27% decline in last quarter sales – to say that the convergence rebound is interesting but the upside will likely remain limited by the gloomy fundamentals of the continent – that could, on top of all the financial struggles of the moment – may need to find a way to increase their military spending in accordance with the US demands that warns that the transatlantic partner is no longer willing to offer security to its old friends for free. No wonder the BAE systems rose more than 3% yesterday. The European defense stocks are certainly stepping into a new era...

China

The S&P500 flirted with its ATH levels and Apple added nearly 2% yesterday on news that the new low-price iPhones will be out as early as this month and that the company will use Alibaba’s AI to boost the iPhone sales in China. Alibaba, on the other hand, extended rally to the highest levels in three years in Hong Kong on nascent AI optimism in China. Overall, the Hang Seng index this week has extended gains to nearly 20% since mid-January on optimism that the inflowing Chinese AI models could be pivotal for the Chinese technology stocks that have been heavily battered since 2021. If you ask me, I'm less concerned about government interference in tech (at least negatively). With a worsening demographic and property crisis, alongside deteriorating trade and geopolitical relations, Beijing can hardly afford another crackdown on its tech champions—the last card Xi has left to play.

Trump Takes First Steps Towards Implementing Reciprocal Tariffs

In focus today

In the US, January retail sales and industrial production data will be released. Especially the former will be interesting for the markets given that private consumption remains by far the most important driver of economic growth in the US.

In the euro area, the focus shifts to employment data for 2024 Q4, which we expect to show a 0.1% q/q increase, mainly driven by Spain. It will be interesting to see if employment continued to rise, as the labour market remains crucial for the growth outlook this year.

Economic and market news

What happened yesterday

In the US, like the CPI print, the annual PPI was higher than expected in January, with the final demand excl. food and energy measure coming in at 3.6% y/y (cons: 3.3%). Conversely, the monthly measure was more in line with consensus at 0.3% m/m (cons: 0.3%) relative to the CPI counterpart. Decomposing the details indicates that components such as the financial and healthcare services sectors were to the lower side, which feed into the estimates of the upcoming PCE release, explaining the downtick in yields following the release.

President Trump has started devising plans for the reciprocal tariffs, he mentioned earlier in the week. Though no tariffs have been implemented yet, he signed a memo ordering his team to start calculating duties that match those other countries charge the US and to counteract non-tariff barriers. He also emphasised that tariffs would target countries with high VAT, a move that appears to be aimed at the EU. Trump, who campaigned on a pledge to bring down consumer prices, acknowledged that prices could go up in the short term because of the tariffs. The news triggered risk-on sentiment, resulting in lower US yields, a weaker USD, and higher equities.

In an interview with the Wall Street Journal, Vice President JD Vance mentioned the US could impose sanctions or take military action against Moscow if Russia does not agree to a peace deal ensuring Ukraine's long-term independence. Meanwhile, Trump stated that Ukraine would participate in peace talks with Russia - following Wednesday's opening for such discussions. Attention now turns to this weekend's Munich Security Conference for possible new signals towards ending the war, although Kyiv emphasized it would be premature to speak with Moscow at the conference.

Additionally, Trump said he would "love" to have Russia back in G7 (which would become the G8 with Russia), while also eyeing a summit with Putin and Xi Jinping, during which, among other things, he would propose to discuss cutting the countries' military budgets in half.

In the euro area, industrial production was lower than expected at 1.1% m/m in December (cons: 0.6%), primarily attributing to capital goods, likely reflecting the continued low appetite for investments in the euro area amid low capacity utilization. We expect the weakness in the industry to continue the coming six months before falling interest rates and rising real incomes should help stabilise the manufacturing sector.

In the UK, data showed a stronger than expected GDP growth of 0.1% q/q in Q4 2024 (cons: -0.1%) with December coming in significantly stronger than expected at 0.4% m/m. For December, the topside surprise was broad-based with industrial production, services and manufacturing production offering positive contributions while construction contracted. More broadly, in Q4 private consumption was weaker than expected posing no growth and net exports posed a drag. We expect private consumption to pick up the coming quarters.

In Switzerland, January inflation surprised to the topside in core terms at 0.9% y/y (cons: 0.6%), while headline inflation stood at 0.4% y/y (cons: 0.4%). In their latest set of forecasts from the December meeting, the Swiss National Bank (SNB) forecasted inflation at 0.3% y/y in Q1 2025. We get another inflation print before the next SNB meeting on 20 March.

In Norway, the oil investment survey confirmed our expectations of a gradual slowdown in oil investments during 2025 and a drop next year, which is important as this leaves room for a stimulus to the rate sensitive parts of the economy.

The annual address from Norges Bank's governor Ida Wolden Bache contained no new policy signals. Instead, she reflected on Norway as a small, open economy heavily reliant on trade and stressed the importance of international cooperation and flexible economic policies.

Equities: Risk-on was back in fashion on Thursday. US rebounded, driven by big tech as yields dropped. VIX dropped to 15 as Trump unveiled his reciprocal tariff plans, which is the lowest level in three weeks. Growth cyclicals leading the gains, taking both the S&P 500 and Stoxx 600 up 1.1%. Increased risk appetite still not benefitting small caps which performed in line with markets yesterday. Futures are unchanged this morning.

FI: Global bond yields declined and shrugged off most the rise from Wednesday after the stronger than expected US CPI data. Furthermore, the stronger than expected US PPI data better than expected Jobless Claims did not have much impact on global bond markets. The rally was driven from the long end of the curve and there was a solid bullish flattening.

FX: Big swings in FX as Trump's announcement to impose reciprocal tariffs initially sent EUR/USD below 1.04 before retracing towards session highs as the open-ended tariff process sent US yields lower across the curve. The Sterling found support in stronger-than-expected growth data and the CHF had a strong session on the back of a topside surprise to Swiss inflation. After a brief setback on Wednesday, the SEK had yet another strong run yesterday, with EUR/SEK tracking lower towards 11.20.

Cliff Notes: Resilience Offers Promise

Key insights from the week that was.

In Australia, the Westpac-MI Consumer Sentiment Index was broadly unchanged in February, nudging just 0.1% higher from 92.1 to 92.2. Though, this ‘cautiously pessimistic’ tone marks a material improvement from the last two-and-a-half years of deep pessimism, aided by more constructive views on future conditions. Indeed, the constituent sub-indexes tracking the one-year and five-year economic outlooks have both moved above their long-run averages, and the year-ahead outlook for family finances is also within striking distance. Views on current conditions are still weak however, both the ‘family finances vs. a year ago’ and ‘time to buy a major household item’ indexes notably below historic averages. This composition emphasises the weak starting point of consumers, having been battered by cost-of-living pressures and real income declines over 2022-24. That said, moderating inflation (as discussed by Chief Economist Luci Ellis this week) and the ‘Stage 3’ tax cuts combined with imminent interest rate relief are expected to support a recovery in time.

Businesses’ perspective on the economy looks to be broadly aligned with the consumer view. The latest NAB business survey confirmed business conditions continue to track the steady decline in place since 2022. This trend, alongside our own evidence from card activity and the Westpac-DataX Consumer Panel, is consistent with lingering downside risks concentrated in consumer spending. Business confidence meanwhile remains broadly neutral but extremely volatile month-to-month. With the combination of building expectations for rate cuts, a Federal Election, and an extremely fluid global backdrop, this is likely to remain the case for some time.

A final note for Australia on housing. The latest batch of loan approval data, now released on a quarterly frequency, revealed a softer finish to the year. The total value of finance approvals (excl. refinancing) rose 1.4% in Q4 despite fewer loans being approved (–0.4%qtr) owing to higher average loan sizes – a dynamic responsible for more than half the growth in total housing finance value since Q2 2022. Indeed, despite pulling back from a stellar annual pace of +25%yr in September, total housing finance values are still tracking +16%yr, reflecting the backdrop of robust house price growth over 2023/24 and stretched affordability.

Before moving further afield, this week our New Zealand economics team released their latest quarterly Economic Overview, detailing in depth their baseline expectations for New Zealand and the key risks.

Over in the US, last Friday’s January nonfarm payrolls print was solid at 143k and came with a +100k revision to the prior two months. Annual revisions in contrast cut 589k jobs from the level at March 2024. The average pace of nonfarm payrolls growth is now estimated to have slowed from 380k in 2022 to 216k in 2023 then 165k since the beginning of 2024. Arguably, gains since the beginning of 2023 are consistent with a labour market in balance.

Adjustments were also made to the level of household survey employment at January; as such, the December 2024 and January 2025 employment outcomes are not comparable. The ratios are unaffected however and provided a positive update, the unemployment rate edging down from 4.1% to 4.0%, a rate also consistent with a balanced labour market. January's strong average hourly earnings gain of 0.5% is likely a one-off given the series has, on average, increased 0.3% per month since the beginning of 2024 and the Employment Cost Index also continues to point to a trend deceleration in wage and compensation growth.

January’s CPI subsequently printed above expectations, total prices up 0.5% and the core sub-set 0.4%. Annual headline and core inflation edged higher as a result to 3.0% and 3.3% respectively. On the services side, transport and recreation services both reaccelerated, pointing to capacity constraints. Shelter inflation was also a touch stronger in the month and the annual rate, while slowly trending lower, is still materially above its long-run average. As we begin to consider the potential implications of US tariffs on domestic inflation, it is important to recognise that the highly-beneficial deflationary trend for core goods looks to have come to an end, with three of the past five readings positive and the annual change now just -0.1%. The PPI also came in stronger than expected at 0.4%mth and the history was revised up. However, components that feed into the calculation of PCE inflation, the FOMC's preferred consumer inflation gauge, were favourable, health care costs and airfares both down in the month.

Reflecting on the latest employment and CPI readings, during testimony to Congress, FOMC Chair Jermone Powell reaffirmed the FOMC is in no hurry to ease monetary policy further. He noted that “reducing policy restraint too fast or too much could hinder progress on inflation” and characterised the labour market as “broadly in balance” and “not a source of significant inflationary pressure”. When questioned on tariffs, Chair Powell kept his comments apolitical, but did note they could impact monetary policy’s stance. Overall, it is clear the FOMC is confident in the underlying health of the US economy and believe they have time on their side to judge the persistence of inflation and the consequences of the new administration's policies.

On government policy, this week saw US President Donald Trump announce a 25% tariff on steel and aluminium imports into the US, with no immediate exceptions. The pathway to implementing reciprocal tariffs is also to be studied. Reciprocal tariffs would arguably have the greatest impact on emerging markets, in particular countries such as India and Thailand where tariffs have been put in place to protect the development of critical domestic industry, including the supply of everyday essentials to household sectors with limited financial means.

The Flaw of Averages

There will always be items in the CPI basket with price inflation a long way from the RBA’s 2–3% target. That is no reason to dismiss measures of underlying inflation, such as the trimmed mean, as an indicator of current inflation pressures.

The RBA’s mandate involves an inflation target of 2–3%, always aiming for the 2½% midpoint, while recognising that there will be times when flexibility is needed. The overall CPI inflation result can be pushed around by one-off movements in particular components that say nothing about future trends. That is why the RBA also focuses on various measures of ‘underlying’ or trend inflation. They particularly focus on the trimmed mean measure, which is calculated by excluding the largest increases and decreases that quarter, then taking the average over what remains. Trimmed mean inflation is not the target, but it is the best available single indicator of current momentum in inflation. It is also the measure the RBA uses in most of its forecasting models.

Within both total and trimmed mean inflation, particular subcategories can have inflation rates that are very different from the 2–3% target. Some of these are the results of transitory supply shocks, like the 17% increase in lamb and goat meat prices over 2024, or policy changes, like the 12% increase in tobacco prices over the same period. These shifts typically get excluded from the trimmed mean calculation. As such, there is no real need to remove selected items and then perform the trimmed mean calculation.

(Be sceptical, too, when people advocate removing one policy-affected item, such as electricity, but not another policy-affected item moving in the opposite direction, such as tobacco. In any case, Westpac Senior Economist Justin Smirk has previously calculated that removing electricity before calculating the trimmed mean makes very little difference to the result.)

There are, however, plenty of categories where the trend rate of inflation is materially different from the overall inflation rate. For example, insurance prices have risen at an annual rate of more than 5% over the past 20 years. On the other side, prices of garments, adults’ shoes and household appliances have fallen overall over the same period. Not all these categories will be trimmed out in a particular quarter. It depends on how extreme those trend price changes are relative to the overall distribution of inflation by component.

The important point here is that the RBA’s mandate is not to get prices of every single category in the CPI basket increasing at 2–3%. As long as the average is in the range – and, per the latest Statement on the Conduct of Monetary Policy, heading towards its midpoint – then the mandate is being fulfilled. There will always be items with price inflation a long way from that range. Changes in relative prices are a natural and desirable part of a well-functioning market economy. They are central to the way buyers and sellers – in this case, consumers and producers – respond to real-world changes.

This is why one should be wary of arguments that the RBA should set monetary policy in a specific way because some subset of the inflation basket is showing price growth above the 2–3% target range, even though overall inflation is at or near target. It depends on the context.

For example, for much of the inflation-targeting period since the mid-1990s, services inflation has run faster than goods inflation. Is that difference a reason to run tight policy? Not necessarily. It depends on whether the low-inflation category is likely to stay that way.

That question became particularly salient in the post-pandemic period. Goods inflation increased considerably as supply chains were disrupted. If goods inflation normalised (to below-target rates) as supply chains normalised, then services inflation could also normalise to its above-target average rate, and overall inflation could settle within the target as intended.

The wrinkle would be if goods prices reverted some way back to their pre-pandemic norms. That would mean goods inflation would spend some time below normal, possibly involving some outright price declines, before presumably reverting to average. If overall inflation had returned to target on the back of a temporary period of below-normal goods inflation, then clearly above-trend services inflation would not be compatible with keeping inflation sustainably in the target range once goods inflation normalised.

This has been part of the concern in the US. Like Australia, services inflation typically runs faster than goods inflation there. Rolling 10-year average inflation rates have generally been 1ppt or so higher for US services than US goods, similar to the post-2000 picture in Australia. But unlike the situation in Australia, goods inflation fell noticeably below its pre-pandemic average recently, flattering the overall rate of inflation. Given recent tariff announcements, it seems unlikely that goods prices will continue falling for an extended period. Indeed, a period of US goods inflation above historical averages is probably on the cards. Falling housing-related inflation may help offset this, but one can’t help thinking that the sustainability of US inflation near target is more fragile than is the case for Australia.

Some may object that current rates of inflation for services in Australia are still well above pre-pandemic rates. Recall, though, that overall inflation undershot the RBA’s target for several years pre-pandemic, partly because services inflation was running at a persistently below-average pace. So that is not the best benchmark period for comparison. Current services inflation is also a bit above the average of the first decade of the 21st century, but not drastically so. And the ongoing unwind in rents and insurance inflation, as pandemic effects continue to wash out, should help narrow the gap.

Perhaps we should be more concerned that, despite weak household demand, goods inflation didn’t see the same period of decline as in the US. Part of this might be the pause in the long-running trend decline in prices of audiovisual and computing equipment in Australia. We also observe, though, that homebuilding costs are included in the CPI in Australia but not in the US, and that the pandemic surge in these costs is unwinding.

Whatever the main driver of the difference, the main point here is that goods inflation is not temporarily flattering the total inflation result in Australia. And since electricity prices are currently excluded from the trimmed mean inflation rate, they are not flattering underlying inflation either. Economy-watchers, including the RBA, can therefore be confident that the 3.2% result for trimmed mean inflation over 2024 (and an annualised rate of 2.7% over the second half of the year) is indeed giving a sufficiently accurate picture of current inflation pressures in Australia, and act accordingly.

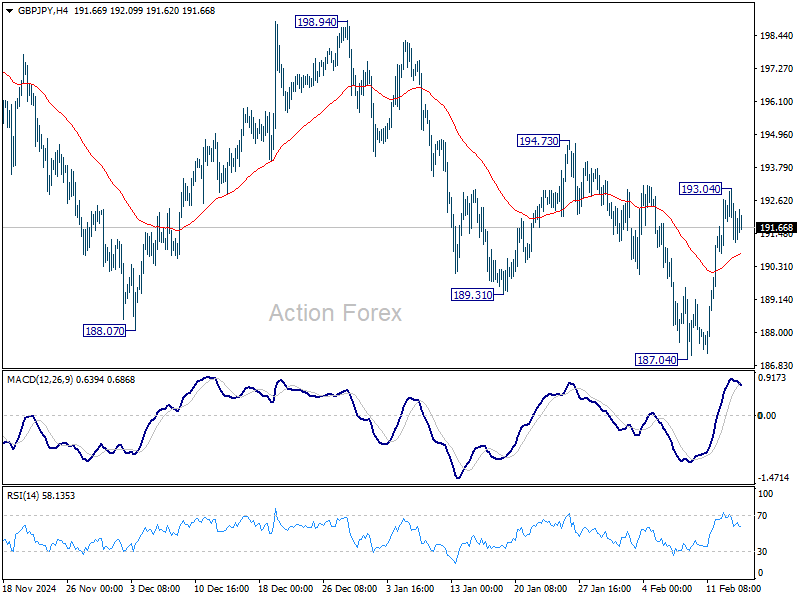

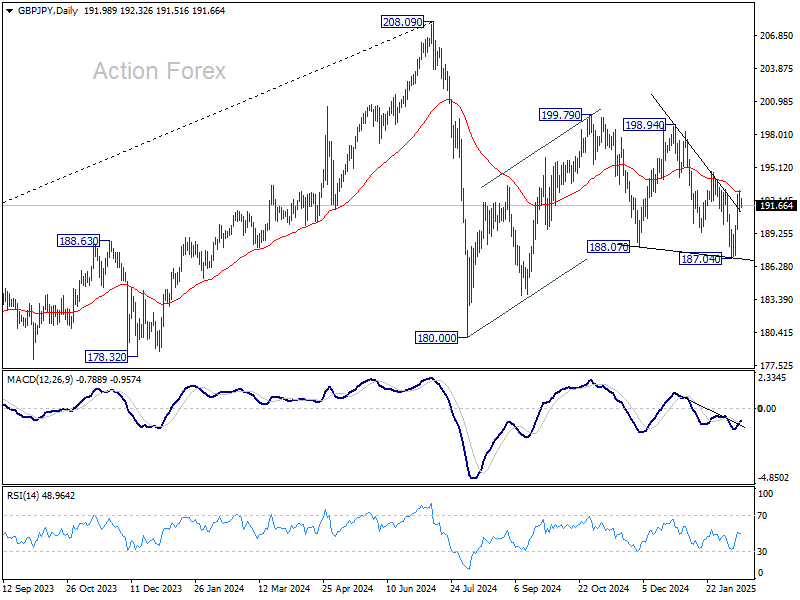

GBP/JPY Daily Outlook

Daily Pivots: (S1) 191.11; (P) 192.09; (R1) 192.99; More...

GBP/JPY retreated after rising to 193.04 and intraday bias is turned neutral first. Overall, corrective pattern from 180.00 is extending, possibly with rebound from 187.04 as another upleg. Above 193.04 will target 194.73 resistance first. Firm break there will solidify this case and target 198.94 next.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall to 100% projection of 208.09 to 180.00 from 199.79 at 171.70, even still as a correction.

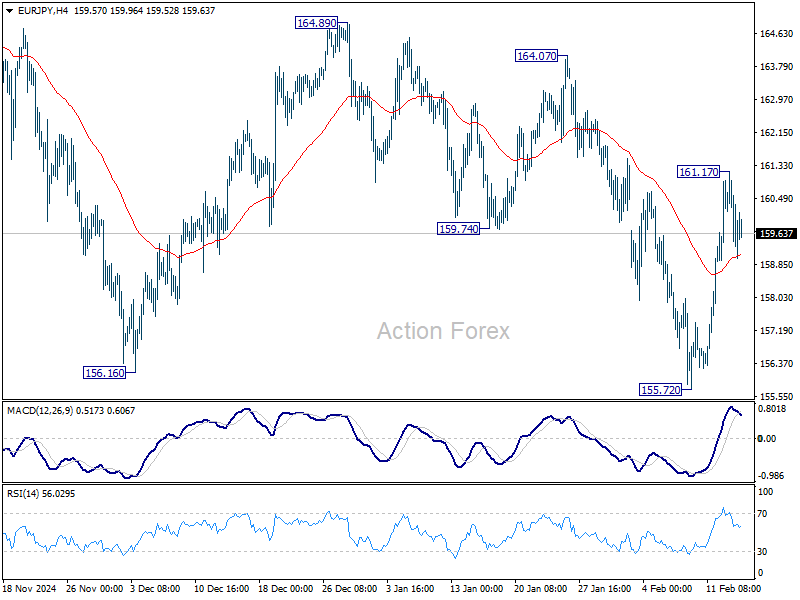

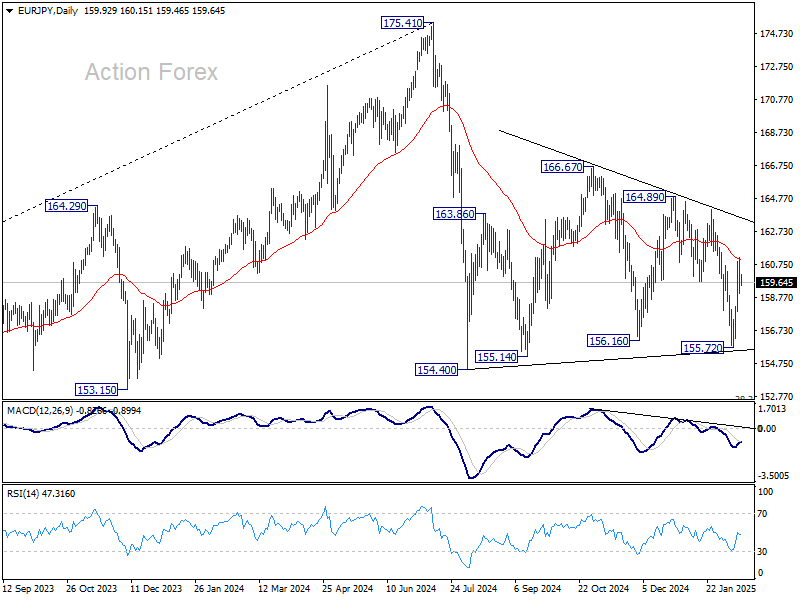

EUR/JPY Daily Outlook

Daily Pivots: (S1) 158.88; (P) 160.04; (R1) 161.07; More...

EUR/JPY retreated after rising to 161.17 and intraday bias is turned neutral first. Overall, sideway pattern from 154.40 is still extending with another upleg. On the upside, above 161.17 will target 164.07 resistance and then 164.89.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall to 100% projection of 175.41 to 154.40 from 166.57 at 145.56, even still as a correction.

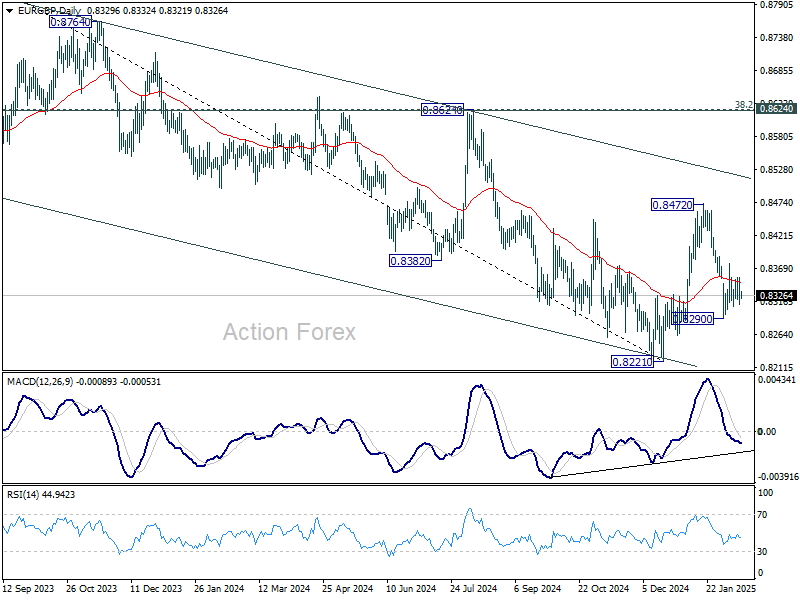

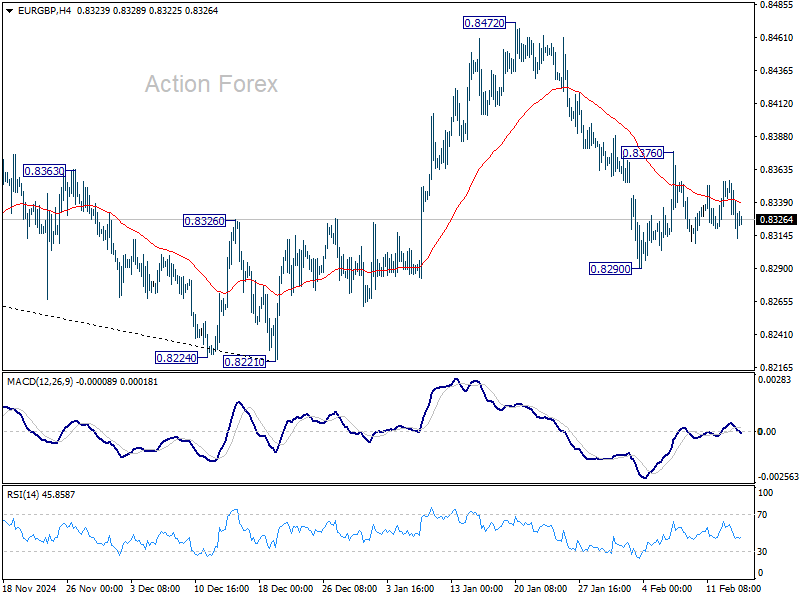

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8306; (P) 0.8336; (R1) 0.8358; More...

Intraday bias in EUR/GBP remains neutral and near term outlook stays mixed. On the upside, above 0.8376 minor resistance will bring stronger rally towards 0.8472. However, on the downside, break of 0.8290 will resume the fall from 08472 to retest 0.8221 low.

In the bigger picture, rebound from 0.8221 medium term bottom could extend higher through 55 W EMA (now at 0.8435). However, medium term outlook will be neutral at best as long as 0.8624 cluster resistance zone (38.2% retracement of 0.9267 to 0.8221 at 0.8621) holds. Another decline through 0.8221 would remain mildly in favor.