Sample Category Title

Trump and Putin Phone Call Opens Door to Ukraine Peace Talks

In focus today

From the US, January PPI and weekly jobless claims are due for release. It will be interesting to see if the PPI-figures come in higher than expected like yesterday's CPI.

In the euro area, focus turns to industrial production data for December, which is expected to show a small decline of 0.6% m/m by consensus. However, the decline will likely be larger than 0.6% m/m as German industrial production declined 2.4% m/m in a sign of a still weak industrial sector.

In Sweden, Riksbank's vice governor Per Jansson holds a speech at 08:00 CET on "Trust and flexibility going forward". We will be watching to see if Jansson aligns with Aino Bunge's dovish tones from yesterday.

Economic and market news

What happened overnight

In Japan, wholesale inflation for January printed higher than expected at 4.2% y/y (cons: 4.0%), while the monthly print was 0.3% m/m, as expected. This was the fifth consecutive acceleration in wholesale inflation, reflecting persistent price pressures and bolstering the case for further BoJ rate hikes this year, as we project.

What happened yesterday

In geopolitics, Trump and Putin had a 90 min call yesterday and the two countries have agreed to kick off negotiations to end the war in Ukraine. Trump later had a separate call with Ukraine that did not last as long, and it remains unclear what will Zelensky's/ Ukraine's role be in the upcoming talks, or if there is any. US defence secretary Pete Hegseth said that its unrealistic for Ukraine to restore its pre-2014 borders or for Ukraine to become a member of NATO.

In the US, January CPI surprised sharply to the topside as headline CPI grew by 0.5% m/m SA (cons. +0.3%, Dec +0.4%) and core inflation accelerated to 0.4% m/m SA (cons. +0.3%, Dec. +0.2%) - for more detail please see Global Inflation Watch - Tariff Uncertainty blurs the outlook, 12 February. Additionally, we will evaluate our dovish Fed view of four rate cuts in 2025 over coming days.

While having not signed any tariffs yet, Trump repeated his plans to impose reciprocal tariffs very soon. The comment comes shortly before a visit from Indian Prime Minister Narendra Modi, and the Trump administration having complained about India's high tariffs on U.S. imports. With a U.S. CPI-release on Wednesday that surprised to the upside, economists have once again highlighted the possible inflation risks associated with tariffs. Later today, we host a webinar at 10.00-10.45 CET providing an update on the whole tariff situation.

In the euro area, Bundesbank President Nagel stated that the ECB should ease its policy gradually rather than attempting to reach the elusive "neutral" interest rate, which is estimated to be between 1.75% and 2.25%, according to last week's r*-publication from the ECB. That said, the remarks are not surprising given that Nagel is viewed as one of the über-hawks of the ECB.

In Sweden, Riksbank Vice Governor Bunge was on the wire, talking about the state of the economy and monetary policy. Bunge emphasized that inflation has been close to 2% and indicators suggest that inflation will align with the target going forward. Looking at the upside surprise in January, she pointed out that it remains to be seen what caused this and stressed that individual figures should be interpreted with caution. Overall, her remarks were somewhat dovishly twisted.

Equities: Equity investors took the inflation surprise with ease. Global equities were admittedly slightly lower (MSCI World -0.1%) but that did not stop the buying in Europe and especially Germany, a full 1% higher (11% YTD). Even Nasdaq was in positive. So, inflation did not trigger a clear-cut risk off session, which we argue it should not. However, it is still surprising to see markets coping so well with negative news and yield jumps. Remember new tariffs also taken with a shrug earlier this week. Perhaps this comes down to the not overly aggressive positioning in markets. Our correction monitor admittedly shows overbought conditions but far from an outright sell signal. Defensives outperformed, but only marginally. The only sector sticking out was energy, reverting -2%. Small caps underperformed again, as has been the case the last week, taking underperformance to 1.3p.p. YTD globally. Futures are higher this morning.

FI: US Treasury yields rose significantly on the back of higher-than-expected US inflation data and the market continues to reduce expectations for future rate cuts by the Federal Reserve. Currently just one rate cut is priced in for the rest of 2025, which is a significant reduction from the autumn 2024, when 6-7 rate cuts were priced in for 2025. The negative reaction from US also sent European government bond yields upwards across the yield curve.

FX: Whipsaw action in EUR/USD with an initial flurry to the low 1.03's on the back of yesterday's hotter-than-expected US CPI print, before turning around and retracing all the way to 1.04 on Trump's announcement of his call with Putin. The EUR found broad support, with EUR/JPY and EUR/CHF moving firmly higher, the former rallying close to 1.5%. Scandies did not benefit from the EUR-move and instead ended the day close to session highs vs EUR. CEE currencies did however benefit, with PLN, CZK and HUF all outperforming the single currency.

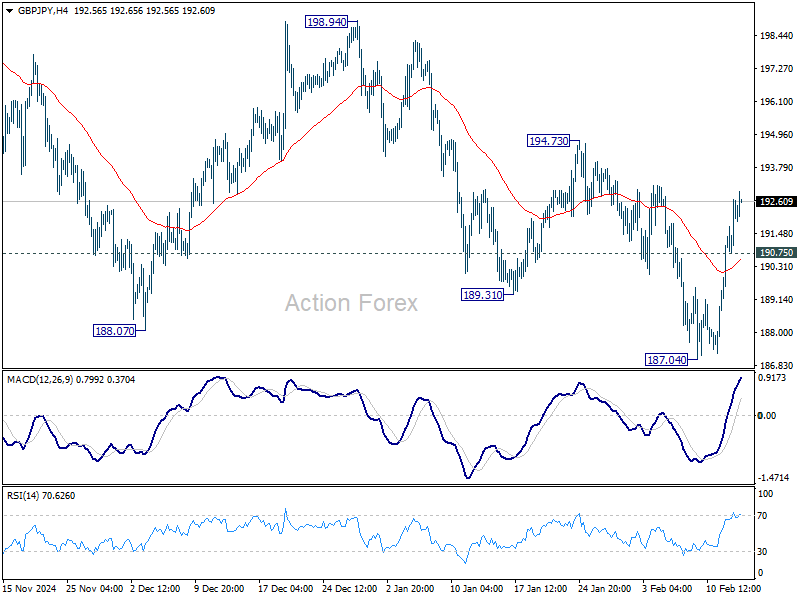

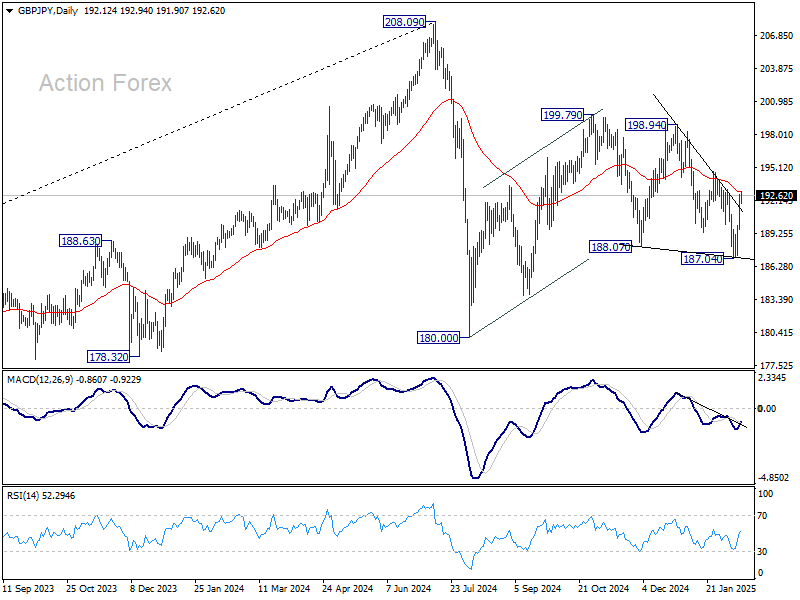

GBP/JPY Daily Outlook

Daily Pivots: (S1) 188.07; (P) 188.99; (R1) 190.74; More...

GBP/JPY's extended rebound suggests that fall from 198.94 has completed with three waves down to 194.73. Intraday bias is now on the upside for 194.73 resistance first. Firm break there will solidify this case and target 198.94 next. On the downside, below 190.75 minor support will turn intraday bias neutral again. Overall, corrective pattern from 180.00 would likely extend for a while.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall to 100% projection of 208.09 to 180.00 from 199.79 at 171.70, even still as a correction.

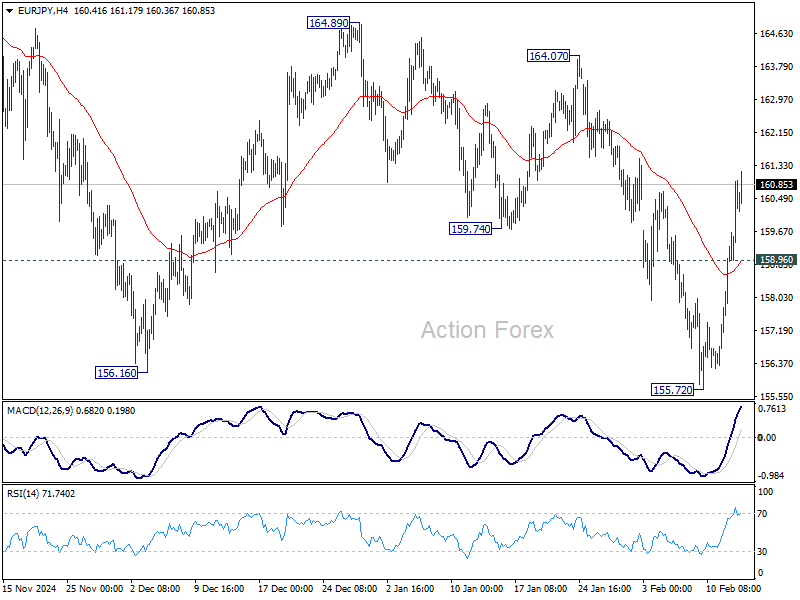

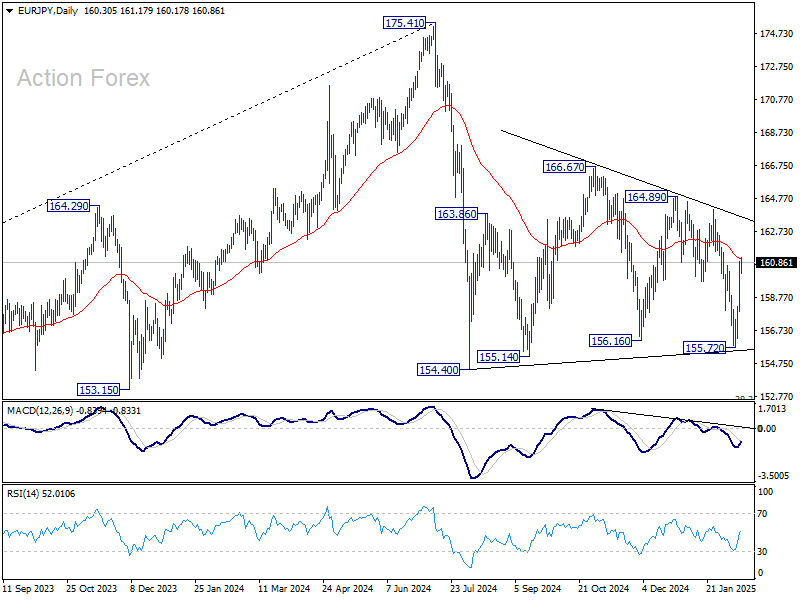

EUR/JPY Daily Outlook

Daily Pivots: (S1) 158.49; (P) 159.73; (R1) 161.56; More...

EUR/JPY's strong break of 159.74 support turned resistance suggests that fall from 164.89 has completed with three waves down to 155.72, ahead of 154.40 key support. Intraday bias is back on the upside for 164.89 or even further to 166.67. On the downside, below 158.96 minor support will turn intraday bias neutral again first. Overall, sideway pattern from 154.40 would extend further for a while.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall to 100% projection of 175.41 to 154.40 from 166.57 at 145.56, even still as a correction.

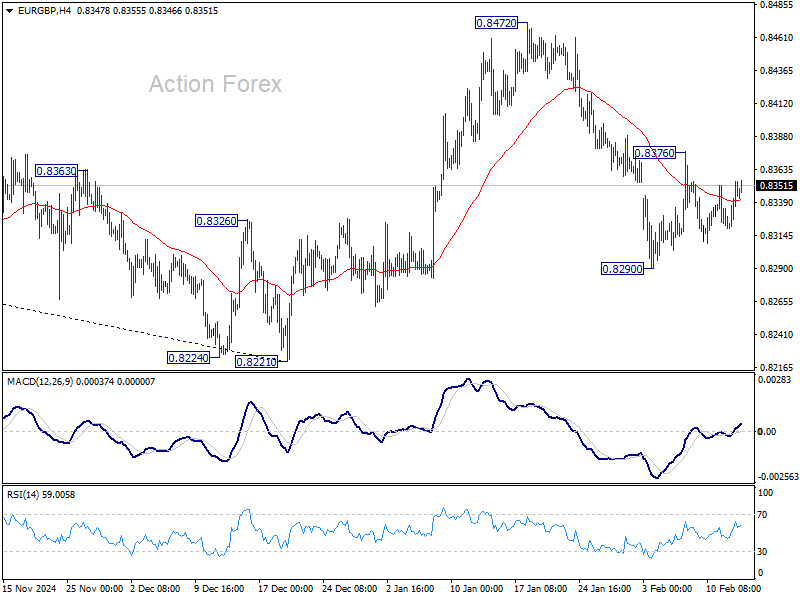

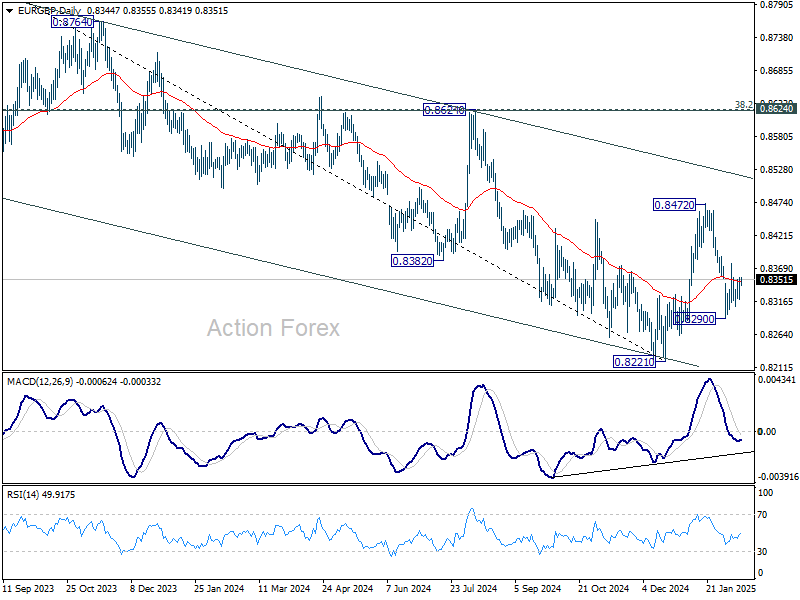

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8320; (P) 0.8338; (R1) 0.8363; More...

Intraday bias in EUR/GBP stays neutral for the moment and near term outlook is mixed. On the upside, above 0.8376 minor resistance will bring stronger rally towards 0.8472. However, on the downside, break of 0.8290 will resume the fall from 08472 to retest 0.8221 low.

In the bigger picture, rebound from 0.8221 medium term bottom could extend higher through 55 W EMA (now at 0.8435). However, medium term outlook will be neutral at best as long as 0.8624 cluster resistance zone (38.2% retracement of 0.9267 to 0.8221 at 0.8621) holds. Another decline through 0.8221 would remain mildly in favor.

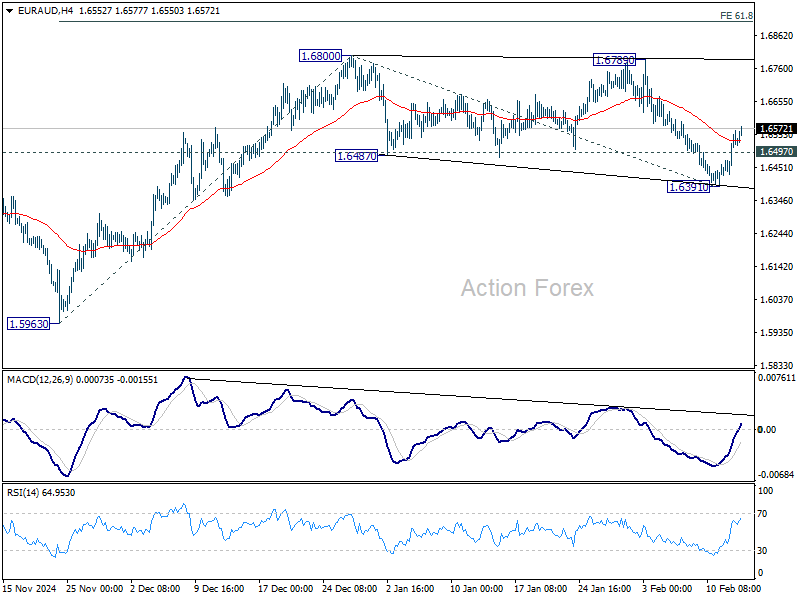

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6455; (P) 1.6512; (R1) 1.6593; More...

EUR/AUD's strong rebound argues that price actions from 1.6800 could have completed as a three wave corrective pattern to 1.6391. Intraday bias is back on the upside for retesting 1.6800 first. Decisive break there will resume whole rally from 1.5963 to 61.8% projection of 1.5693 to 1.6800 from 1.6391 at 1.6908. For now, risk will stay on the upside as long as 1.6391 support holds, in case of retreat.

In the bigger picture, with 1.5996 key support (2024 low) intact, larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5996 will indicate that such up trend has completed and deeper decline would be seen.

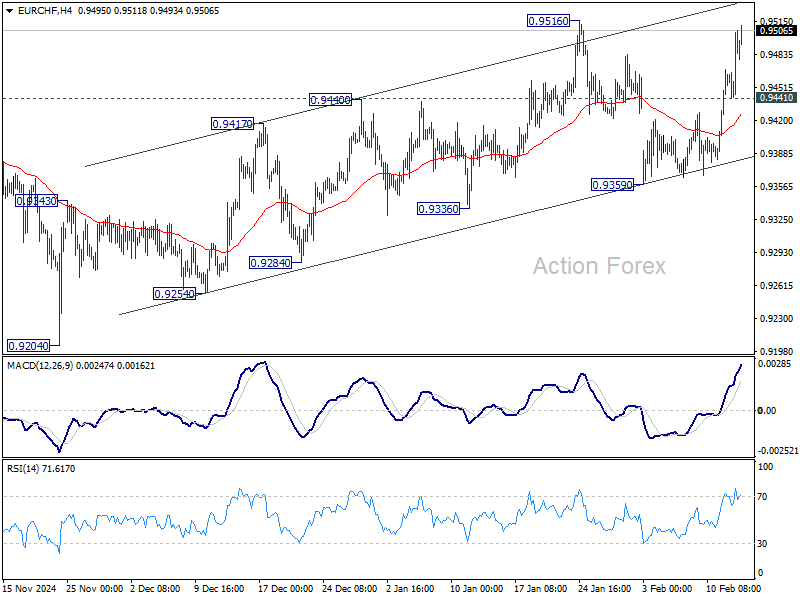

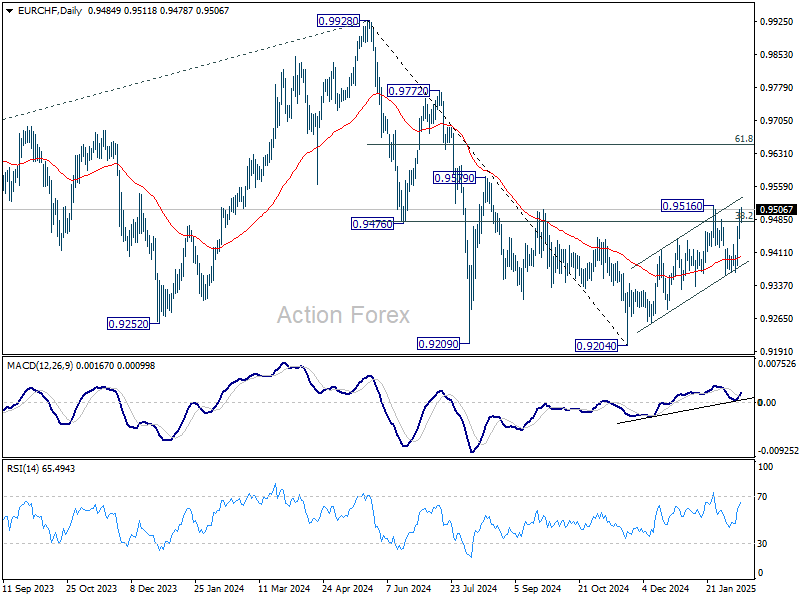

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9450; (P) 0.9479; (R1) 0.9516; More....

Intraday bias in EUR/CHF stays neutral first. On the upside, firm break of 0.9516 will resume whole rally from 0.9204. Nevertheless, below 09441 minor support will turn bias back to the downside for 0.9359 support instead.

In the bigger picture, sustain above 38.2% retracement of 0.9928 to 0.9204 at 0.9481 should confirm that whole fall from 0.9928 has completed at 0.9204. Further rally should then be seen back to 61.8% retracement at 0.9651 and above. However, another rejection by 0.9481 will keep outlook bearish for extending larger down trend through 0.9204.

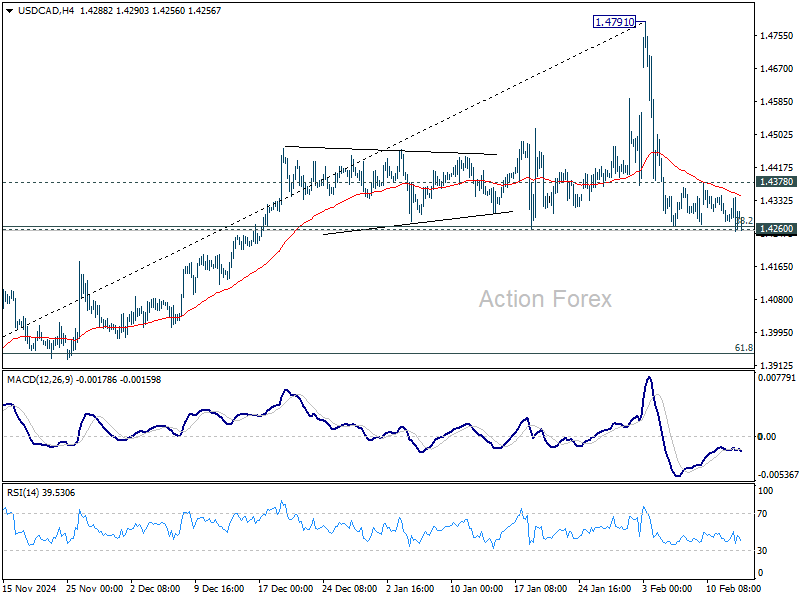

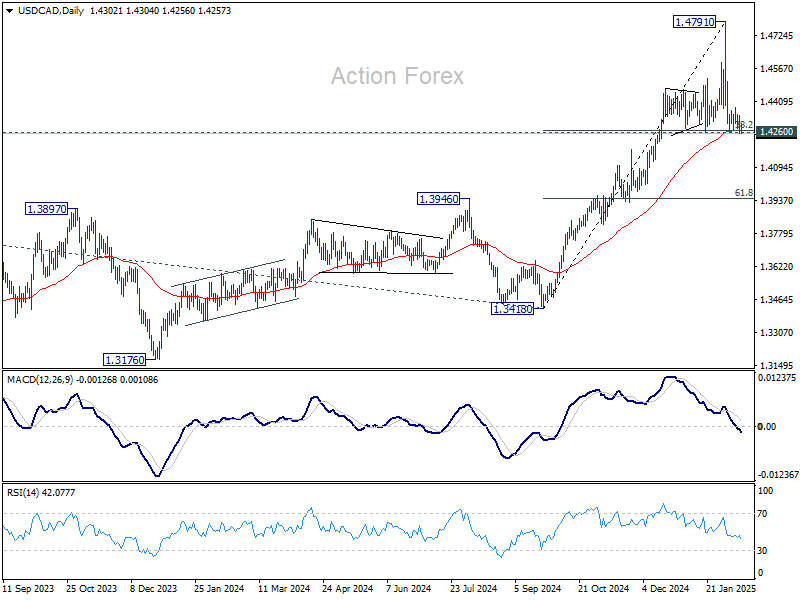

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4263; (P) 1.4303; (R1) 1.4350; More...

Intraday bias USD/CAD remains neutral for the moment. On the downside, sustained break of 1.4260 cluster support (38.2% retracement of 1.3418 to 1.4791 at 1.4267) will indicate that larger scale correction is underway. Intraday bias will be back on the downside for 61.8% retracement at 1.3942. Nevertheless, strong rebound from current level will revive near term bullishness. Break of 1.4378 minor resistance will turn bias to the upside for retesting 1.4791.

In the bigger picture, long term up trend is tentatively seen as resuming with breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.

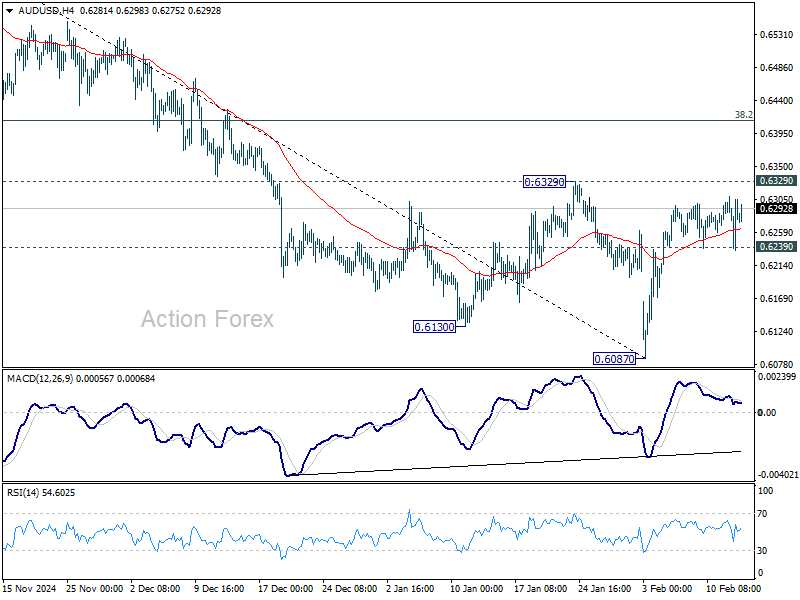

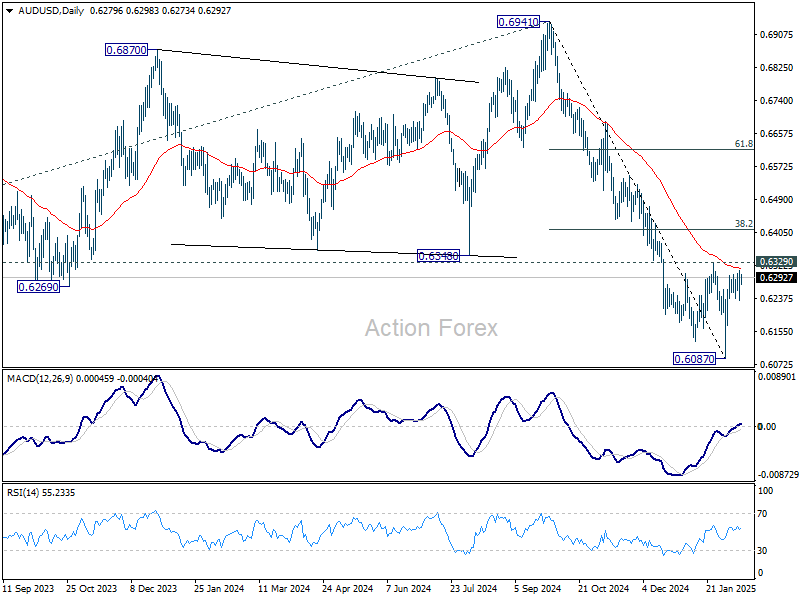

AUD/USD Daily Report

Daily Pivots: (S1) 0.6240; (P) 0.6275; (R1) 0.6315; More...

Intraday bias in AUD/USD stays neutral. With 0.6329 resistance intact, outlook will stay bearish. On the downside, break of 0.6239 minor support will turn bias back to the downside for retesting 0.6087 low. However, firm break of 0.6329 will bring stronger rebound to 38.2% retracement of 0.6941 to 0.6087 at 0.6413, even just as a corrective move.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6516) holds.

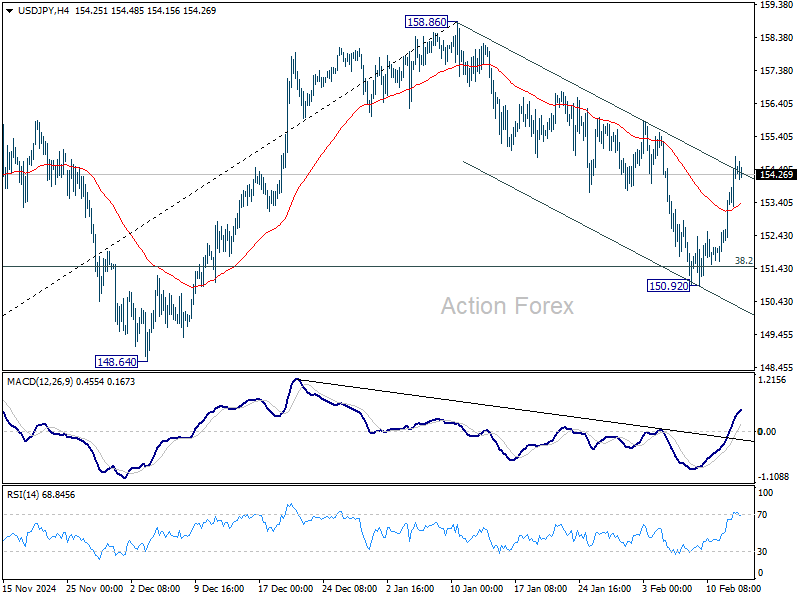

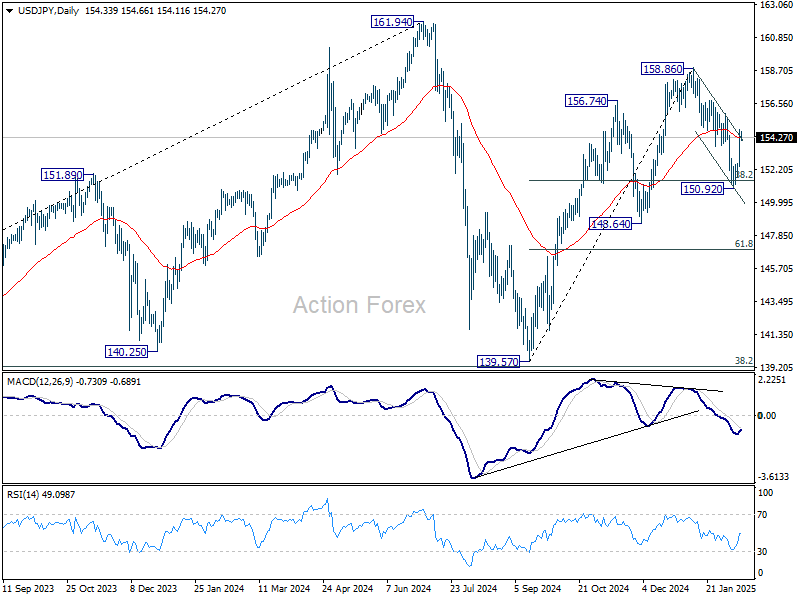

USD/JPY Daily Outlook

Daily Pivots: (S1) 152.92; (P) 153.86; (R1) 155.35; More...

Intraday bias in USD/JPY stays on the upside at this point. Corrective pull back from 158.86 should have completed at 150.92 after drawing support from 38.2% retracement of 139.57 to 158.86 at 151.49. Further rise should be seen to retest 158.86 first. Firm break there will resume whole rally from 139.57 to retest 161.94 high. For now, risk will stay on the upside as long as 150.92 support holds, in case of retreat.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

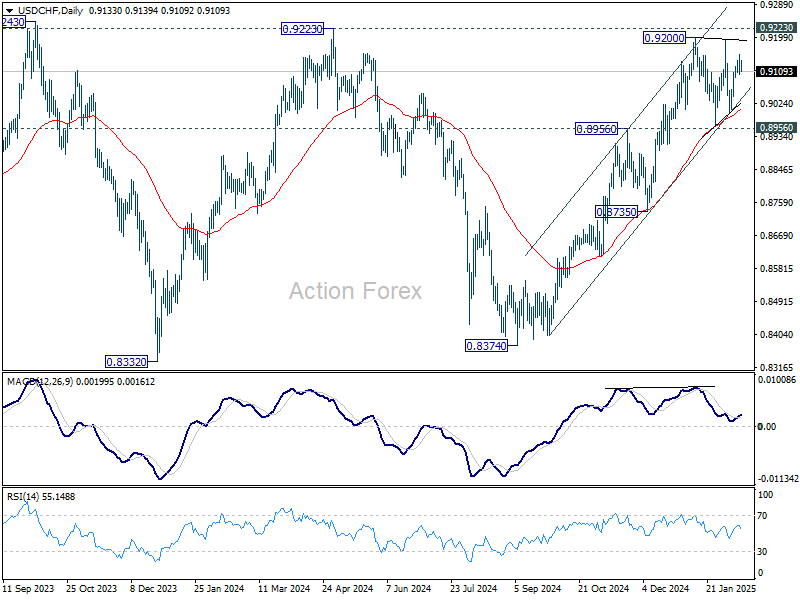

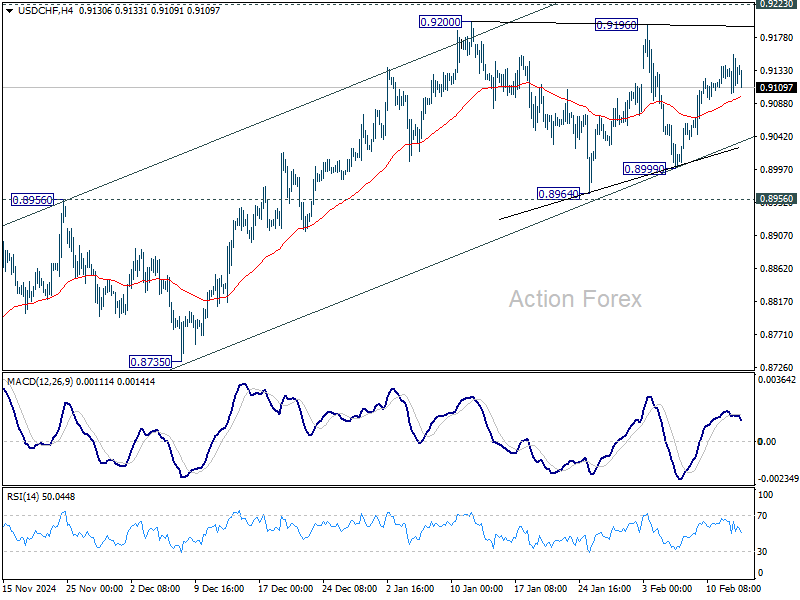

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9107; (P) 0.9132; (R1) 0.9160; More…

USD/CHF is still extending the consolidation from 0.9200 and intraday bias remains neutral. Outlook stays bullish with 0.8956/64 support zone intact. On the upside, firm break of 0.9200/9223 will resume the whole rally from 0.8374 and carry larger bullish implication. However, sustained break of 0.8964 will be a sign of reversal and turn bias back to the downside.

In the bigger picture, decisive break of 0.9223 resistance will argue that whole down trend from 1.0342 (2017 high) has completed with three waves down to 0.8332 (2023 low). Outlook will be turned bullish for 1.0146 resistance next. Nevertheless, rejection by 0.9223 will retain medium term bearishness for another decline through 0.8332 at a later stage.