Sample Category Title

Market Update – European Session: Plethora Of Rate Decisions Over The Next 24 Hours, Tax Reform Expected To Proceed...

Notes/Observations

Democrats gain seat in US Senate follow Jones victory in Alabama special election; not expected to impact the GOP's plan to pass tax reform, as Republican leaders are racing to approve the tax legislation by early next week

Plethora of central bank rate decisions over the next 24 hours including the FOMC today and BOE and ECB on Thursday.

Focus on FOMC rate decision later today with 3rd rate hike for 2017 expected; markets eye dots for 2018 rate outlook

Asia:

US/EU/Japan Joint Statement at WTO: vowed to work together to fight market-distorting trade practices and policies that have fueled excess production capacity (in-line with speculation)

Japan Govt said to keep the assumed interest rate at record low of 1.1% in FY18/19 budget draft

Asian Development Bank (ADB) raised 2017 Developing Asia GDP growth forecast to from 5.9% to 6.0%; maintains 2018 forecast at 5.8

Europe:

PM May is facing another painful Brexit dilemma as Tory lawmakers are lining up vote for an amendment to her flagship law that paves the way for the UK's exit from the EU. Faces the issue whether to cave in to rebels in her Conservative Party who want the power to veto the final Brexit deal or face a potentially damaging defeat.

Italy President Mattarella to dissolve Parliament on Dec 28th or 29th to clear the way for elections(in-line with recent speculation)

Americas:

Alabama special election has Democrat Jones defeating Republican candidate Moore

Energy:

Weekly API Oil Inventories: Crude: -7.4M v -5.5M prior

OPEC Sec Gen Barkindo: Affirms re-balancing of oil market ‘on its way'; strong economic growth, especially in China, is positive. Reiterated saw 2018 global oil demand up 1.5M B/D, in line with 2017

Economic Data:

(DE) Germany Nov Final CPI M/M: 0.3% v 0.3%e; Y/Y: 1.8% v 1.8%e

(DE) Germany Nov Final CPI EU Harmonized M/M: 0.3% v 0.3%e; Y/Y: 1.8% v 1.8%e

(DE) Germany Nov Wholesale Price Index M/M: 0.5% v 0.0% prior; Y/Y: 3.0% v 3.0% prior

(ZA) South Africa Nov CPI M/M: 0.1% v 0.1%e; Y/Y: 4.6% v 4.7%e

(ZA) South Africa Nov CPI Core M/M: 0.0% v 0.2%e; Y/Y: 4.4% v 4.5%e

Iceland Central Bank (Sedabanki) left its 7-day Deposit Rate unchanged at 4.25%

(IT) Italy Oct Industrial Production M/M: 0.5% v 0.7%e; Y/Y: 0.7% v 0.8%e, Industrial Production WDA Y/Y: 3.1% v 3.4%e

(UK) Nov Jobless Claims Change: +5.9K v +6.5K prior; Claimant Count Rate: 2.3% v 2.3% prior

(UK) Oct Average Weekly Earnings 3M/Y/Y: 2.5% v 2.5%e; Weekly Earnings ex Bonus 3M/Y: 2.2% v 2.2%e

(UK) Oct ILO Unemployment Rate: 4.3% v 4.2%e, Employment Change 3M/3M: -56K v -40Ke

(EU) Euro Zone Q3 Employment Q/Q: 0.4% v 0.4% prior; Y/Y: 1.7% v 1.6% prior

(EU) Euro Zone Oct Industrial Production M/M: 0.2% v 0.0%e; Y/Y: 3.7% v 3.2%e

Fixed Income Issuance:

(IS) Iceland to sell EUR-denominated 5-year notes; guidance seen +45bps to mid-swaps

(IN) India sold total INR110B vs. INR110B indicated in 3-month, 6-month and 12-month bills

(DK) Denmark sold total DK4.64B in 3-month and 6-month bills

(SE) Sweden sold SEK2.0B vs. SEK2.0B indicated in % 2028 bonds; Avg Yield: 0.7161% v 0.7373% prior; bid-to-cover: 1.86x v 2.31x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.1% at at 391.4, FTSE +0.1% at 7504, DAX -0.1% at 13165, CAC-40 -0.1% at 5421, IBEX-35 +0.3% at 10318, FTSE MIB -0.4% at 22635, SMI -0.1% at 9351 , S&P 500 Futures flat]

Market Focal Points/Key Themes: European Indices trade mixed this morning following mixed futures in the US after a flat close in Wall Street yesterday. US Futures did see initial weakness after Democrat Doug Jones wins the Alabama Senate race before paring the losses. Retailers were on the front foot this morning with Spanish Clothing giant Inditex lifting the Ibex after 9M results, while Electronics Firm Dixons Carphone trades over 4% higher after encouraging holiday season trading. Elsewhere following their Investor day Serco rises sharply, after lifting guidance, with shares of Nexans in Paris also higher after ther longer term outlook. Looking ahead looking out for guidance from the likes of Honeywell and United Health.

Equities

Consumer Discretionary [Dixons Carphone [CD.UK] +4% (Earnings), Inditex [ITX.ES] +3.0% (Earnings), TUI [TUI.UK] +0.8% (Earnings), Metro [B4B.DE] +1.1% (Earnings)]

Financials [Serco [SRP.UK] +8% (Investor day, lifts outlook)

Industrials [John Wood Group [WG.UK] -1.3% (Outlook), Aurubis [NDA.DE] -3.8% (Earnings)

Technology [Wirecard [WDI.UK] +0.8% (FY18 outlook), Nexans [NEX.FR] +1.4% (Investor day)]

Real Estate [Purple Bricks [URP.UK] -7% (Trading update)]

Speakers

Brexit Min Davis sent a letter to his conservative law makers that reiterated view that UK would not ratify the EU deal without Parliamentary approval (Seen as an attempt to ward off party in-fighting)

EU Chief Brexit Negotiator Barnier reiterated last week's Brexit agreement was complex; to recommend moving into phase 2 of negotiations

German SPD Dep leader Stegner reiterated party view that would not join Merkel coalition at any price

Iceland Central Bank (Sedabanki) policy statement noted that lower headline inflation would be offset by waning effects of past appreciation of exchange rate. Outlook was for continued strong demand pressures in domestic economy. Called for a tight monetary stance

Czech Central Bank Vice Gov Hampl: More rate hikes might be needed compared to current forecast. Saw risks of stronger domestic inflation pressure

Sweden Employment Service (PES) raised 2017 Unemployment forecast from 6.6% to 6.8% while cutting 2018 Unemployment forecast from 6.7% to 6.6%

German DIW institute raised 2017 and 2018 GDP growth forecasts in its Economic outlook Report. Raised GDP from 1.9% to 2.1% for both years

Brazil Fin Min Meirelles: 2018 GDP growth seen close to 3.0%. Believed that pension reform will be approved

China and UK said to hold bilateral trade talks between Dec 15-16th

UAE Oil Min Mazrouei: To early to speculate on any exit from OPEC/Non-Opec production cuts

Currencies

The softer USD exhibited during Asia saw that trend dissipate as the EU morning progressed. Alabama election results apparently get moved aside ahead of the Fed's pronouncements

There are a plethora of central bank rate decisions over the next 24 hours including the FOMC today and BOE and ECB on Thursday.

Some dealers were quite perplexed that the GBP failed to gain traction after the recent headline CPI reading of 3.1% and higher than expected wage data in today's session. While ILO unemployment rate matched a 4 decade low the employment change saw its 2nd straight decline. GBP/USD at 1.3340 area just ahead of the NY morning.

Fixed Income

Bund futures trade 163.36 down 16 ticks, easing back marginally. Continued upside sees 163.63 then 164.25. A reversal targets 162.50 then 162.38.

Gilt futures trade at 125.73 up 7 ticks after UK wages come roughly in line while jobless claims and ILO unemployment rate miss expectations. Continued upside eyeing 126.15 then 126.65. Downside targets include 125.24 then 124.75.

Wednesday's liquidity report showed Tuesday's use of the marginal lending facility rose to €M from €283M prior.

Corporate issuance saw 5 issuers raise $1.9B in the primary market

Looking Ahead

OPEC Dec Monthly Oil Report

05:30 (CL) Chile Central Bank's Traders Survey

05:30 (UK) DMO to sell 0.125% 2036 I/L Gilts

06:00 (BR) Brazil Oct Retail Sales M/M: 0.1%e v 0.5% prior; Y/Y: 5.0%e v 6.4% prior

06:00 (BR) Brazil Oct Board Retail Sales M/M: -0.2%e v +1.0% prior; Y/Y: 9.3%e v 9.3% prior

06:00 (IL) Israel Nov Trade Balance: No est v -$1.7B prior

06:00 (ZA) South Africa Oct Retail Sales M/M: +0.2%e v -0.7% prior; Y/Y: 5.3%e v 5.4% prior

06:30 (IS) Iceland to sell 6-month Bills - 06:45 (US) Daily Libor Fixing

07:00 (RU) Russia to sell combined RUB40B in 2021 and 2028 OFZ bonds

07:00 (US) MBA Mortgage Applications w/e Dec 8th: No est v 4.7% prior

07:00 (UK) PM May Question Time in House of Commons

07:30 (FI) Finland PM Sipila on upcoming EU Leader Summit

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) Nov CPI M/M: 0.4%e v 0.1% prior; Y/Y: 2.2%e v 2.0% prior

08:30 (US) Nov CPI Ex Food and Energy M/M: 0.2%e v 0.2% prior; Y/Y: 1.8%e v 1.8% prior

08:30 (US) Nov CPI Index NSA: 246.816e v 246.663 prior; CPI Core Index SA: 253.932e v 253.428 prior

08:30 (US) Nov Real Avg Weekly Earnings Y/Y: No est v 0.4% prior, Real Avg Hourly Earning Y/Y: No est v 0.4% prior

08:30 (CA) Canada Nov Teranet/National Bank HPI M/M: No est v -1.0% prior; Y/Y: No est v 10.0% prior, House Price Index: No est v 218.13 prior

10:30 (US) Weekly DOE Crude Oil Inventories

14:00 (AR) Argentina Q3 Unemployment Rate: No est v 8.7% prior

14:00 (US) FOMC Rate Decision: Expected to raise Funds Target Range 25bps to 1.25%-1.50%

14:30 (US) Fed Chair Yellen post rate decision press conference

USD Consolidates Ahead Of FOMC Meeting And CPI Report

Busy day for the greenback

After surging across the board yesterday, the US dollar partially reversed gains during the Asian session, with the dollar index returning towards 94 followinga positive surprise in the PPI Index. November’s headline producer prices gauge rose 3.1% year-over-year, beating median forecast of 2.9% and previous month reading of 2.8%. This is the largest increase since January 2012. Excluding the most volatile components, such as energy and food prices, the measure increased 2.4%y/y, matching market expectations. The surprise in the headline gauge is not exclusively due to the solid gains in crude oil prices throughout November but also due to the distortions created by the Hurricane season.

November’s consumer price index is due for release today. The headline gauge is expected to notch up to 2.2%y/y from 2% in October. The core measure should remain stable at 1.8%y/y. An upside surprise in the headline measure appears likely, especially against the backdrop of positive pressures from energy prices. However, the market remains cautious regarding the inflation outlook as the 1y breakeven inflation currently stands at around 1.43%y/y.

Finally, the December FOMC meeting will be the main event today. Fed members will provide their latest update on both the inflation and growth outlook. The main question today is not whether the Fed will raise borrowing costs today, as it already priced in at 100%, but rather how dovish/hawkish Janet Yellen will sound during the press conference. Any significant change in the dot-plot could affect significantly the USD outlook. So far, the market is expecting at least two rate hikes next year, if not three.

SNB Happy on the sidelines

The SNB is not moving, unwilling to disrupt the markets current narrative. From the SNB vantage point macro and domestic conditions are in a sweet spot for current policy. Inflation rates have improved but are nowhere near the SNB target rate while the short CHF is on most analyst top calls for 2018. All the while growth outlook has improved, led by export and manufacturing, supported by the weak CHF. The SNB will remain on the sideline, keeping rate unchanged and reiterating its pledge to intervene in the FX markets is needed.

SNB members will continue to sound cautions on exchange rate believe the CHF remain overvalued. Despite the improving backdrop its unlikely the SNB will get ahead of the ECB in tighten. This would put the first hike well into 2019 indicating that current pricing it too optimistic. We remain long on EURCHF.

EUR/USD Drops To 1.1730 Amid PPI Release

In accordance with expectations, until release of information on the US PPI the currency rate was slowly fluctuating near the 55- and 100-hour SMAs. But since the data was better than analysts' expected the pair broke through the 38.2% Fibonacci retracement level and once again ended up in support zone located between the 1.1730 and 1.1722 marks.

Until release of an update on the American inflation the rate is expected to continue fluctuating near the upper boundary of a minor descending channel. In case of disappointing result, depreciation of the buck might elevate the pair up to the 1.1800 level.

However, the rate is still expected to plunge to the area between the 23.6% retracement level at 1.1681 and the monthly S2 at 1.1652 due to alleged interest rate hike.

GBP/USD Slips To 1.3300 Again

Until release of data on the American PPI, the cable was moving below the monthly PP, as expected. But then publication of better than anticipated result led to active appreciation of the buck, which pushed the rate through support zone located between the 1.3338 and 1.3331 marks.

Accordingly, yesterday's trading session the pair ended near the 1.3300 psychological level. As this support line crosses the bottom boundary of a senior descending channel, the Pound should try to restore some value today.

However, the fact that it is simultaneously moving in other two descending channels makes such scenario unlikely. Moreover, the pair constantly experiences pressure from the slipping 55- and 100-hour SMAs. But most importantly is that expectations of the upcoming interest rate hike increases bearish sentiment that might result in a deep plunge to the 1.3230 mark.

USD/JPY Fluctuates Around 55- And 100-Hour SMAs

Despite release of better than expected US PPI data, bulls could not push the pair through resistance zone located between the 113.67 and 113.74 marks. Accordingly, this barrier triggered a rebound that lasted until the pair reached the 100-hour SMA.

Until publication of an update on the American inflation, the currency rate is expected to move horizontally between the 55- and 100-hour SMAs. In case of a negative result, the pair is likely to plunge to support zone located near the 50% Fibonacci retracement level at 113.00.

However, the subsequent Fed decision is likely to lead to aggressive acquisition of the buck, which will drive the rate above the 114.00 mark. In best case scenario the currency rate might end up this trading session near July maximum located at 114.50.

XAU/USD Still Trades Near 55-Hour SMA

Due to anticipation of the upcoming decision on the interest rate hike, the exchange rate continued to move horizontally between the 55-hour SMA and the monthly S2 from the top as well as the 50% Fibonacci retracement level and the weekly S1 from the bottom.

Until release of data on the American inflation the rate is expected to continue its steady movement around the 1,244.00 mark. Subsequently, the pair might temporarily surge to the 100-hour SMA located near the 1,250.00 level.

However, the fact that southern side is practically barrier-free and the rate is fluctuating in a two-week long descending channel suggests that the further advance to the top is unlikely.

GBP/USD: UK Consumer Price Index

The British Pound received only temporary support from the UK data indicating the country's inflation at the six-year high in November. The GBP/USD exchange rate rose 17 pips or 0.12%, but weakened rapidly and failed to sustain the position, continuing trading in the 1.3320 area.

Britain's inflation accelerated growth pace unexpectedly, causing a tighter squeeze of household incomes. The Office for National Statistics stated that consumer inflation hit a yearly rate of 3.1% in November, driven by computer games, air fares and chocolate prices, reflecting the Sterling's plunge after the Brexit vote. The current rate, being more than 1% above the BoE target, would force the Bank's Governor to write a letter about further steps to the UK Finance Minister.

EUR/USD: German ZEW Economic Sentiment

The Euro slipped against the US Dollar on the report, revealing some signs of pessimism among the German investors this month. The EUR/USD currency pair lost 13 base points or 0.11%, to touch the presumed level of support at 1.1770.

German investors' mood worsened more than anticipated in December, reflecting uncertainties over the regulations of a government to be formed, reforms in the EU and Britain's quit from the bloc. The Mannheim-based Centre for European Economic Research stated that its German Economic Sentiment Index came in at 17.4 points for the current month, compared with 18.7 in November. Meanwhile, a separate gauge of the current conditions' assessment rose to 89.3.

Democrats Win In Alabama | Traders Focused On Fed | Oil Up After Inventory Data

Big blow to Trump pushed dollar lower

Fed's interest rate hike already priced

Oil moved higher on back of inventary data

Gold under pressure ahead of Fed announcement

Getting anything meaningful across the line and facing failures may become even more regular routine for President Trump due to the victory of Doug Jones, a Democrat and a winner of the Alabama Senate race.

President Trump has faced many failures throughout this year mainly because his own party has not supported his views. Investors have even more negative views about the prospects of any GOP’s economic agenda changing into a law under the newly developed situation. Jone’s win would only bring more complications for president Trump because this is going to bring another blow for GOP Senate majority down to 51 seat. The tax overhaul deal, which has been the primary reason in the recent week behind the rally for the US equity markets, could start to see some gas coming out.

European futures are trading somewhat flat and the Asian session has failed to provide any clear direction and the projected win of Democrats in Alabama is not providing any aid either. Investors are going to remain mostly on the side lines as they await the decision from the Federal Reserve Bank. Although, it is widely known and priced in the market that the Fed is going to increase the interest rate by another twenty five basis points. However, what really matters for the dollar bulls and the equity markets is the future path of interest rate in 2019 which is currently divided between two or three rate hikes.

Investors would also like to know some information from the Fed if they are going to allow any room in their monetary policy if the tax overhaul does become a law.

In the commodity space, investors have jumped back in to the oil trade as the inventory data has suggested that the stock piles have dropped more than indicated. But we do not expect any major upside here because the US supply of oil in 2019 may outpace the demand, and it would impact the OPEC’s efforts to fade the global oil glut.

Precious metal is also trading mostly flat and we expect no major moves ahead of the Fed announcement. If the Fed comes out of the gate with more hawkish views on the economy and see inflation improving, it could impact the dollar index. Any further strength in the dollar index would push the gold price lower.

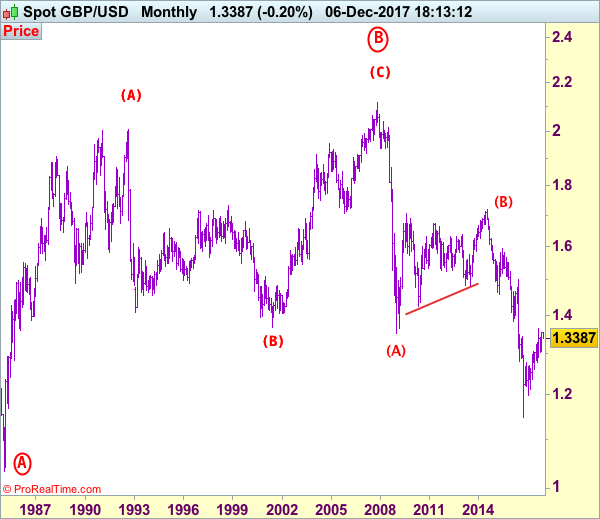

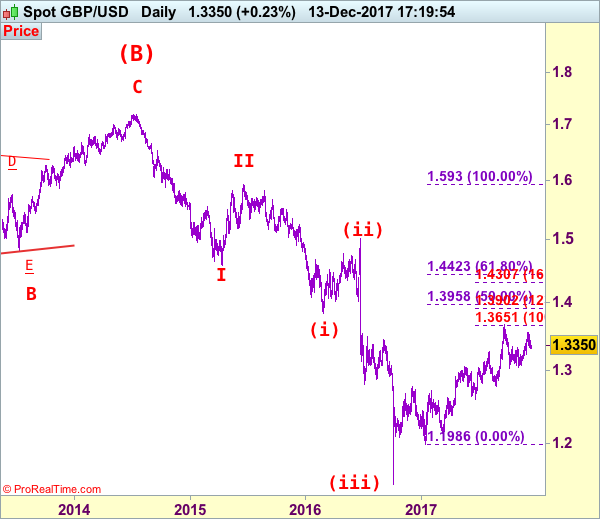

GBP/USD Elliott Wave Analysis

GBP/USD – 1.3350

Although cable rebounded last week to as high as 1.3521, renewed selling interest emerged there and the British pound has slipped again, retaining our view that further consolidation below 1.3550 would be seen and mild downside bias remains for weakness to 1.3300, then 1.3470, however, a break of indicated support at 1.3221 is needed to signal top has been formed at 1.3550, bring further fall towards 1.3250-60 later.

Our preferred count on the daily chart is that cable's rebound from 1.3500 (wave (A) trough) is unfolding as a wave (B) with A ended at 1.7043, followed by triangle wave B and wave C as well as wave (B) has possibly ended at 1.7192, below support at 1.4232 would add credence to this count, then further fall to 1.4000 level would follow but reckon downside would be limited to 1.3655 support and price should stay above previous support at 1.3500.

On the upside, whilst initial recovery to 1.3400-10 cannot be rude out, reckon 1.3430-40 would limit upside and bring another decline later. Above said resistance at 1.3521 would abort and bring retest of 1.3550, break there would signal the rise from 1.3027 is still in progress for gain to 1.3595-00 but break there is needed to confirm early upmove has resumed for retest of 1.3658 resistance first.

Recommendation: Hold short entered at 1.3470 for 1.3270 with stop lowered to break-even.

Longer term - Cable's rise from 1.0520 (Feb 1985) to 2.0100 (September 1992) is seen as [A], the decline to 1.3682 is labeled as (B) and (C) wave rally has ended at 2.1162 (9 Nov, 2007) which is also the top of larger degree wave B with circle. The selloff from there is a 5-waver with wave (A) ended at 1.3500 (23 Jan 2009), wave (B) itself is labeled as A: 1.6733, triangle wave B: 1.4813 and wave C as well as top of wave (B) ended at 1.7192 (2014), hence the selloff from there is an impulsive wave (C) with wave I : 1.4566, wave II 1.5930, an extended wave III is unfolding and already exceeded our downside target at 1.3500 and 1.3000, hence weakness to 1.2500 and possibly 1.2000 cannot be ruled out, however, price should stay well above psychological level at 1.0000.