Sample Category Title

USD/JPY Mid-Day Outlook

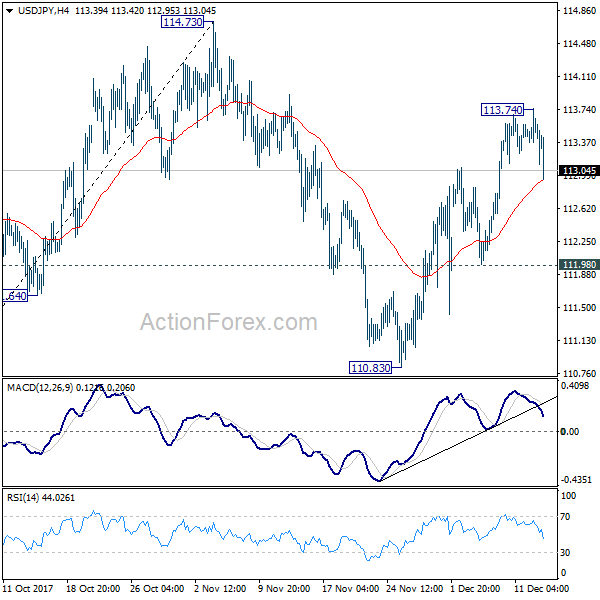

Daily Pivots: (S1) 113.36; (P) 113.55; (R1) 113.74; More...

USD/JPY's pull back from 113.74 accelerates lower in early US session. But it's seen as a correction and thus, intraday bias remains neutral first. As noted before, as long as 111.98 support holds, further rally is expected in the pair. On the upside, above 113.68 will extend the rise from 110.83 to 114.73 resistance first. Decisive break there will resume whole rise from 107.31. More importantly, that will confirm completion of medium term correction from 118.65 at 107.31. In that case, retest of 118.65 should be seen next. However, break of 111.98 support will extend the correction from 114.73 with another fall, possibly to 61.8% retracement of 107.31 to 114.73 at 110.14 before completion.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed a 107.31. And medium term rise from 98.97 (2016 low) is resuming. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this will and extend the medium term fall back to 98.97 low.

Fresh Selling in Dollar after Core CPI Miss, FOMC Next

Dollar suffers some fresh selling in early US session after weaker than expected inflation data. Headline CPI rose 0.4% mom, 2.2% yoy in November inline with consensus. However, core CPI rose just 0.1% mom, 1.7% yoy , below expectation of 0.2% mom, 1.8% yoy. The greenback will now look into FOMC rate decision and statement for the needed fuel to extend recent rebound. Elsewhere in the currency markets, Sterling is trading as the best performing one today in spite of disappointing job data. Meanwhile Swiss Franc is trading as the weakest one, followed by Euro.

Dollar recovery capped by Republican loss in Alabama

Democrat Doug Jones' win in the Alabama Senate race is seen as a factor capping Dollar's gain too. That reduces Republicans already slim majority in the Senate from 52 to 51. Republicans are dashing on reconciliation of the House and Senate versions and come up for a vote before Christmas. Jones is expected to be sworn in later this month in early January. Some Republican leaders said they expect to get the tax bill approved before Jones takes office. Jones' win could be seen as giving the Republican an extra push to speed things up.

But from a medium term perspective, Republican's loss in a deep conservative state is a big rebuke to President Donald Trump. That's a state Trump won by 28% a year ago. With Republican president, Senate and House majority, the party haven't done much this year. Tax bill is the only one they have hope for. And now, Democrats have only two seat net to work on in next year's elections. It could be even harder for the Trump lead the Congress to fulfil his own election promises then.

Fed to hike, eyes on voting and projections

Fed is widely expected to raise federal funds rate by 25bps to 1.25-1.50% today. There is little doubt about that. Janet Yellen will deliver her last press conference as Fed chair, before Jerome Powell takes over the job next year. The surprise elements could be found in the voting and the new projections. Minneapolis Fed President Neel Kashkari, who dissented the prior hikes, would very likely dissent again. Chicago Fed President Charles Evans could be another dissenter. The vote split could be seen as hawkish if only Kashkari dissents. However, three or more dissenting will signals spreading of the worries on slow inflations among policymakers. And that would be dovish. Fed will mostly upgrade GDP forecast for 2018 and 2019 while lower unemployment rate estimates. The keys will lie in the changes in inflation projections and interest rate projections. So far, hawks inside the FOMC are still expecting three more rate hikes next year.

FOMC September Projections

EU Barnier: No going back on Brexit agreements

EU leaders are expected to formally endorse the "sufficient progress" made in Brexit negotiations later this week, paving the way to start of trade talks, probably in March. EU Brexit negotiator Michel Barnier warned today that "we will not accept any going back on this joint report." He emphasized that "this progress has been agreed and will be rapidly translated into a withdrawal accord that is legally binding in all three areas and on some others that remain to be negotiated." This is in response to comments from UK Brexit Secretary David Davis, which tried to undermine the agreement as a "statement of intent" only.

UK claimant count rose 5.9k in November, above expectation of 0.4k. Unemployment rate was unchanged at 4.3% in October, above expectation of 4.2%. Average weekly earnings growth, though, accelerated to 2.5% 3moy, in line with consensus. From Eurozone, industrial production rose 0.2% mom in October, employment grew 0.4% qoq in Q3. German CPI was finalized at 1.8% yoy in November.

Tillerson: Let's just meet, North Korea

Stories of North Korea tension have slipped down the order recently. Nonetheless, it remains a threat to the region. North Korea leader Kim Jong Un said earlier this week that they're going to manufacturing "more latest weapons and equipment" to "bolster up the nuclear force in quality and quantity". US Secretary of State Rex Tillerson offered talks to North Korea in a speech and said "let's just meet". United Nations political affairs chief Jeffrey Feltman also said that "we have left the door ajar" after visiting North Korea last week. However, it's unknown if Tillerson gets full support from the White House, as it just issued a short statement that "The president's views on North Korea have not changed ... North Korea is acting in an unsafe way ... North Korea's actions are not good for anyone and certainly not good for North Korea."

Australia consumer confidence improved, but not enough for RBA hike in 2018

Australia Westpac consumer confidence rose solidly by 3.6% in December. According to Westpac, that's a "surprisingly strong result" that appears to be boosted by "less threatening outlook for interest rates". Nonetheless, while expectation for an RBA hike in 2018 cooled, Westpac "doubt whether this welcome lift to confidence will be sufficient to see the Bank achieve its ambitious growth forecast in 2018 of 3.25%." And, with inflation projected to be below target in 2018, and a cooling Sydney property market, Westpac maintained the view that RBA will stand pat through 2018.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 113.36; (P) 113.55; (R1) 113.74; More...

USD/JPY's pull back from 113.74 accelerates lower in early US session. But it's seen as a correction and thus, intraday bias remains neutral first. As noted before, as long as 111.98 support holds, further rally is expected in the pair. On the upside, above 113.68 will extend the rise from 110.83 to 114.73 resistance first. Decisive break there will resume whole rise from 107.31. More importantly, that will confirm completion of medium term correction from 118.65 at 107.31. In that case, retest of 118.65 should be seen next. However, break of 111.98 support will extend the correction from 114.73 with another fall, possibly to 61.8% retracement of 107.31 to 114.73 at 110.14 before completion.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed a 107.31. And medium term rise from 98.97 (2016 low) is resuming. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this will and extend the medium term fall back to 98.97 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Consumer Confidence Dec | 3.60% | -1.70% | ||

| 23:50 | JPY | Machine Orders M/M Oct | 5.00% | 2.70% | -8.10% | |

| 07:00 | EUR | German CPI M/M Nov F | 0.30% | 0.30% | 0.30% | |

| 07:00 | EUR | German CPI Y/Y Nov F | 1.80% | 1.80% | 1.80% | |

| 09:30 | GBP | Jobless Claims Change Nov | 5.9K | 0.4K | 1.1K | |

| 09:30 | GBP | Claimant Count Rate Nov | 2.30% | 2.30% | ||

| 09:30 | GBP | ILO Unemployment Rate 3M Oct | 4.30% | 4.20% | 4.30% | |

| 09:30 | GBP | Average Weekly Earnings 3M/Y Oct | 2.50% | 2.50% | 2.20% | 2.30% |

| 10:00 | EUR | Eurozone Industrial Production M/M Oct | 0.20% | 0.10% | -0.60% | -0.50% |

| 10:00 | EUR | Eurozone Employment Q/Q Q3 | 0.40% | 0.40% | 0.40% | |

| 13:30 | USD | CPI M/M Nov | 0.40% | 0.40% | 0.10% | |

| 13:30 | USD | CPI Y/Y Nov | 2.20% | 2.20% | 2.00% | |

| 13:30 | USD | CPI Core M/M Nov | 0.10% | 0.20% | 0.20% | |

| 13:30 | USD | CPI Core Y/Y Nov | 1.70% | 1.80% | 1.80% | |

| 15:30 | USD | Crude Oil Inventories | -3.6M | -5.6M | ||

| 19:00 | USD | FOMC Rate Decision | 1.50% | 1.25% | ||

| 19:30 | USD | FOMC Press Conference |

Canadian Dollar Quiet Ahead of Fed Rate Announcement

The Canadian dollar is almost unchanged in the Wednesday session. Currently, USD/CAD is trading at 1.2864, down 0.02% on the day. On the release front, there are no Canadian releases on the schedule. In the US, CPI is forecast to improve to 0.4%. The Federal Reserve meets for its monthly policy meeting, and is widely expected to raise rates to a range between 1.25% to 1.50%. On Thursday, Canada releases NHPI and Bank of Canada Stephen Poloz speaks at an event in Toronto. The US will release retail sales reports as well as unemployment claims.

Will the Federal Reserve press the rate trigger on Wednesday? The CME Group has priced in a quarter-point rate hike at 87%, so it would be a huge surprise if the Fed doesn't raise the benchmark rate. Even though this move has been priced in, rate hikes tend to trigger a surge of confidence among investors, and a rate hike could boost global stock markets. Today's move could be the start of a series of incremental hikes, as the odds of a January increase stand at 86%. The Fed has hinted that it could raise rates up to three times in 2018, but the pace of increases will depend to a great extent on the strength of the economy and inflation levels. The US labor market remains at full capacity and various sectors in the economy are reporting a lack of workers. Still, this has not translated into stronger wage growth, despite predictions from Janet Yellen and other Fed policymakers that a lack of workers is bound to push up wages.

It has been slim pickings for investors looking at Canadian fundamentals, as there are only two indicators this week. On Thursday, Canada releases a housing report, followed by Manufacturing Sales on Friday. The markets are expecting that the manufacturing indicator will jump to 0.9%, which could give a boost to the struggling Canadian dollar. The indicator has posted two straight gains, easily beating the estimate on both occasions. Investors will be keeping a close eye on the Fed, and the expected rate hike on Wednesday could push the Canadian dollar lower.

CAC Edges Lower, Investors Await Fed Announcement

The CAC index has posted slight losses in the Wednesday session. Currently, the index is at 5414.30, down 0.24% from the Tuesday close. In the eurozone, Employment Change remained unchanged at 0.4%, matching the forecast. Industrial Production rebounded with a gain of 0.2%, above the forecast of 0.0%. The Federal Reserve meets for its monthly policy meeting, and is widely expected to raise rates to a range between 1.25% to 1.50%. On Wednesday, the eurozone releases manufacturing PMIs, and the ECB will make a rate announcement.

With a host of key French indicators on Thursday, we could see some movement from the CAC index after their release. France will publish services and manufacturing PMIs, as well as Final CPI. The PMI reports are expected to indicate expansion, continuing the trend we've seen throughout 2017. The French economy has been marked by stronger growth and lower unemployment, and investor and business confidence has been boosted by the election of pro-business Emmanuel Macron as president. Still, inflation remains a sore point in France, reflective of low inflation levels across the eurozone. French Final CPI is expected to post a negligible gain of 0.1%, unchanged from the previous reading.

All eyes are on the Federal Reserve, which will release a rate statement later on Wednesday. The CME Group has priced in a quarter-point rate hike at 87%, so it would be a huge surprise if the Fed doesn't raise the benchmark rate. Even though this move has been priced in, rate hikes tend to trigger a surge of confidence among investors, and a rate hike could boost global stock markets. Today's move could be the start of a series of incremental hikes, as the odds of a January increase stand at 86%. The Fed has hinted that it could raise rates up to three times in 2018, but the pace of increases will depend to a great extent on the strength of the economy and inflation levels. The US labor market remains at full capacity and various sectors in the economy are reporting a lack of workers. Still, this has not translated into stronger wage growth, despite predictions from Janet Yellen and other Fed policymakers that a lack of workers is bound to push up wages.

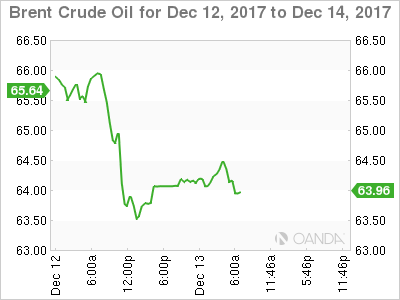

WTI Is Bullish But Watch For Crude Oil Inventories Data

Earlier this week, Oil prices rose as U.S. crude stockpiles showed a drawdown largerthan- expected late last week. In addition, Britain's largest pipeline from its oil and gas fields in the North Sea had an unexpected shutdown for several weeks due to cracks appearing. This pipeline carries about 450,000 barrels per day (bpd) of Forties crude, and causing supply constraints as the pipeline is the largest out of the five crude oil streams that underpin the Brent benchmark.

However, Oil prices fell again overnight most likely due to technical resistance at USD58.60 bbl. Even despite the massive Crude Oil Inventories drawdown last week, production from Crude Oil in the United States has steadily grown from 8.946 million bpd per week starting January this year and reaching an average of 9.707 million bpd for the week ending December1.

All eyes will be on Crude Oil Inventories data from USA later today. Technically the WTI is bullish and we see 2 POC zones where it could bounce. 57.80-58.00 is the first POC zone while 57.30-40 is the POC2. Additionally we see an inverted SHS pattern that is bullish. However if the results come worse than expected, the WTI might drop below 56.65 aiming for 55.85.

H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

Investors Cautious Ahead Of FOMC Announcement

- Economic Projections Eyed With Rate Hike Priced in;

- Trump Speech on Tax Reform Key as Republican Majority in the Senate Narrows.

We're seeing a little caution in the markets as we enter the business end of the week, with equity markets in the US poised to open flat ahead of the FOMC decision.

The decision itself shouldn't throw up any surprises with the Federal Reserve having long suggested that it will raise interest rates once more this year and investors having entirely priced it in. With that in mind, the decision itself shouldn't provide much of a boost for the dollar, however with the statement and new economic projections, including the dot plot, being released alongside it, there could be plenty of volatility.

It will be interesting to see how traders respond to the projections this evening, particularly the dot plot, given the number of changes taking place at the Fed and the vacant spots to be filled. It's possible that these are taken with a pinch of salt should they be broadly in line with the previous set, or even slightly more hawkish. Any downward revision to the inflation and growth outlook, however, could well trigger a much bigger response, with there already being doubts as to whether the inflation trajectory warrants such aggressive tightening.

We'll also hear from Janet Yellen shortly after the announcement but once again, with her term ending in February, traders may take what she has to say with a pinch of salt. While she will offer insight on the latest views of the committee and comment on any changes in the outlook, she isn't the best person to hear from when it comes to the outlook for interest rates next year and beyond. It will be interesting again to see how much attention traders pay to her comments.

A speech from US President Donald Trump on tax reform in Washington will also be monitored closely today, with investors looking for insight on its progress and where the Senate and House is planning to compromise on their respective bills. It would appear the corporation tax rate will now be slightly higher than the 20% that Trump was targeting and other amendments are expected to enable it to squeeze through Congress, a task that's become all the more difficult following the Alabama election.

Keeping the focus on the US we'll get CPI inflation data for November ahead of the FOMC decision. While this can typically get a reaction, coming a couple of weeks before the Fed's preferred core PCE price index measure, traders will likely be more focused on the central banks inflation projections.

Technical Outlook: USDJPY Is Expected To Consolidate Before Bulls Resume, 113.00 Zone Marks Solid Support

The pair is back into daily cloud on Wednesday following repeated rejection under 113.81 target (Fibo 76.4% of 114.73/110.83), with double Doji (Mon/Tue), giving initial signal of rally's stall.

Fresh downside attempts today were so far limited and strongly rejected at 113.12, however, near-term risk is expected to remain shifted lower while the price action is capped by cloud top (113.51).

Bullish setup of daily studies supports for further upside but bulls may take a breather for corrective dip, signaled by strongly overbought slow stochastic turning south on daily chart.

Buying dips towards 113.00 zone remains favored scenario.

FOMC verdict due later today is in focus for fresh signals.

Res: 113.51, 113.81, 114.34, 114.45

Sup: 113.25, 113.12, 112.90, 112.58

Technical Outlook: WTI OIL Holds In Tight Consolidation Above Tenkan-Sen Support, EIA Report In Focus

Oil price recovered slightly on Wednesday, following previous day's fall and holding for now above initial support at $57.34 (daily Tenkan-sen).

Tuesday's quick pullback which dipped to $56.85, retraced 61.8% of three-day $55.81/$58.54 recovery and undermined near-term bulls.

On the other side, bullish structure remains intact on daily chart and keeps in play fresh attempts higher while the price holds above Tenkan-sen line.

Conversely, sustained break lower would weaken near-term structure further and risk retest of Tuesday's low at $56.84 (reinforced by daily Kijun-sen) loss of which would signal an end of recovery phase from $55.81.

API report released on Tuesday showed stronger than expected fall in crude inventories but build of gasoline and distillate stocks, with EIA report due to be released later today, being in focus.

Forecast show 3.75 million barrels draw in oil inventories, compared to previous week's draw of 5.61 million barrels, which could put oil prices under pressure on lower than expected release.

Res: 57.71, 58.54, 58.86, 59.02

Sup: 57.34, 56.85, 56.45, 55.81

Move Over Alabama, Fed Next

Global equities have struggled a tad overnight as investors wait for monetary policy decisions by G10 central banks.

Note: The ECB, BoE and SNB will set monetary policy at their respective meetings on Thursday.

Later this afternoon, the Fed is widely expected to announce its third +25 bps rate increase of 2017 following today's conclusion of its two-day meeting (2 pm ETD). Expect the market to be paying close attention to the central bank's outlook for 2018.

Note: The Fed has penciled in another possible three hikes for next year and two more for 2019 before topping out near +2.75%.

To date, U.S dollar bulls have been 'paying' all year for the error of focusing on steadily rising U.S rates and mostly ignoring where the Fed's tightening path stops. “It's not where yields are, but where they end up that counts.”

Overnight, the 'big' dollar has managed to halt its longest winning streak in nearly two-years after the Democratic candidate, Doug Jones, won the Alabama Senate race, cutting the Republican majority in the U.S senate in half.

Note: Ahead of the FOMC decision, investors will be focusing on U.S consumer inflation data (08:30 am EDT)

1. Stocks struggle ahead of Fed meeting

In Japan, the Nikkei share average ended lower overnight after tech stocks lost ground as they tracked their weaker U.S counterparts. The Nikkei 225 Index fell -0.5%, while the broader Topix shed -0.2%.

Down-under, Aussie stocks overcame some mid-afternoon weakness to finish slightly higher on a takeover deal. The S&P/ASX 200 finished up +0.1%, a fresh one-month closing high and a fifth-straight gain. It's the longest winning streak since October. In S. Korea, the Kospi index rallied +0.8% as reports of S. Korea and the U.S considering delaying joint military drills until after the Winter Olympics in February helped tourist-reliant companies.

In Hong Kong, stocks rebounded overnight, supported by services and financial firms. At the close of trade, the Hang Seng index was up +1.49%, while the Hang Seng China Enterprises index rose +1.83%.

In China, stocks ended higher, aided by gains in consumer and transport firms. The Shanghai Composite index was up +0.7%, while the blue-chip CSI300 index was up +0.86%.

In Europe, regional indices trade mixed this morning ahead of the U.S open. U.S futures did see some early weakness after Democrat Doug Jones won the Alabama Senate race before paring the losses.

U.S stocks are expected to open little changed.

Indices: Stoxx600 -0.1% at at 391.4, FTSE +0.1% at 7504, DAX -0.1% at 13165, CAC-40 -0.1% at 5421, IBEX-35 +0.3% at 10318, FTSE MIB -0.4% at 22635, SMI -0.1% at 9351, S&P 500 Futures flat

2. Oil prices recover on big U.S. stock drawdown, gold trades at their lows

Oil prices remain better bid ahead of the U.S open as industry data yesterday revealed a larger-than-expected drawdown in U.S crude stockpiles. Also aiding prices is the markets expectation for an extended shutdown of a major North Sea crude pipeline.

Brent crude is up +69c, or +1.1% at +$64.03 a barrel. It had settled down -$1.35, or -2.1% yesterday on a wave of profit-taking after news of a key North Sea pipeline shutdown helped send the global benchmark above $65 for the first time since mid-2015. U.S light crude (WTI) is up +45c, or +0.8%.

U.S API data yesterday indicated that domestic crude stocks fell by -7.4m barrels last week. That is almost twice the decline of market expectations for a drop of -3.8m barrels.

Also providing support was the news that Britain's biggest pipeline from its North Sea oil and gas fields is likely to be shut for several weeks for repairs.

Investors to take their cues from todays U.S government's EIA report release (10:30 am EDT).

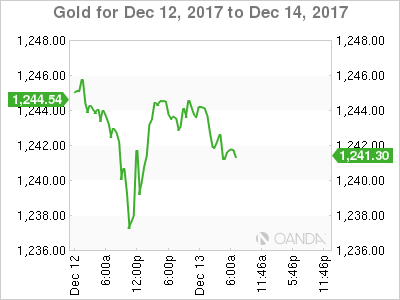

Ahead of the U.S open, gold trades atop its weakest level in almost five-months amid expectations the Fed will hike interest rates later today. The Fed has increased rates twice in 2017 and is still expected to push through three more hikes next year. Spot gold is down -0.1% at +$1,242.18 an ounce. That is not far above yesterday's intraday low of +$1,235.92, which is the lowest print since July 20.

3. Sovereign yield curves

Central banks top the list of risk events with the FOMC, BoE, ECB, SNB, Norges Bank and Turkey's central bank.

The Bank of England (BoE) is not expected to raise interest rates again until after the U.K has officially exited from the E.U, which is scheduled for March 2019. However, this is assuming that domestic inflation starts to slow in the medium-term, after the annual CPI rose by +3.1% in November earlier this week. Tomorrow, the BoE is expected to keep interest rates on hold at +0.5%, after a +25 bps rise last month.

General consensus expects Turkey's central bank (TCMB) to hike interest rates at its policy meeting tomorrow (07:00 am EDT). It is expected to raise the late liquidity lending rate between +25 bps and +225 bps from +12.25%, the first rate increase since April.

Questions around the ECB's thinking about tapering should start to feature in the Q&A session of Draghi's press conference (08:30 am EDT). However, Draghi will almost certainly not engage in this discussion. The ECB has said it will buy assets at a reduced rate from January until at least September. There is no advantage for Euro policy makers to make any decision around ending QE any sooner than is necessary – the ECB is likely to decide its next steps in middle of next year.

4. Dollar awaits Fed announcement

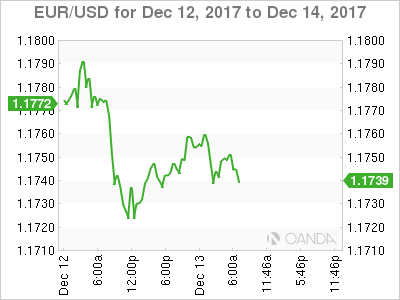

The softer USD (€1.1746, £1.3346, ¥113.37) exhibited during Asia session has somewhat disappeared in the Euro session. Alabama election results apparently have been moved aside for the time being ahead of the Fed's rate announcement.

Note: Yesterday's Alabama Senate result was a loss for congressional Republicans because it trims their Senate advantage to 51-49 as they enter some tough negotiations on spending with Democrats next year. However, it probably will not affect the expected vote on Trump's supposed business-friendly tax cuts, as the winner will not be certified until late December and sworn in in January. Republicans have been hoping to get a bill passed through both sides of Congress before Christmas.

Expect sterling (£1.3346) to remain on tenterhooks as PM Theresa May is facing another painful Brexit dilemma as her own Tory lawmakers are lining up a vote for an amendment to her bill that paves the way for the U.K's exit from the E.U. The PM's dilemma, she either caves into theses rebels who want the power to veto the final Brexit deal, or face a potentially damaging defeat.

In Italy, as expected, President Mattarella is to dissolve Parliament on Dec 28th or 29th to clear the way for elections.

5. Eurozone industrial output stronger than expected

Data this morning showed that industrial production in the eurozone was stronger than expected in October, rising by +0.2% from September and +3.7% y/y. This beat the consensus forecast of a -0.3% drop on the month and a +3.5% rise on the year.

Digging deeper, data for September were also revised slightly higher.

Net result, the E.U economic picture is consistent with the eurozone economy having a better end to the year, and firmer starts to 2018, than had been expected.

Other Euro data showed that the number of people in work rose by +0.4% during Q3, and is now at a record high. Hence, do not be surprised if the ECB raises its growth forecasts tomorrow.

DAX Edges Lower, German CPI Meets Expectations

The DAX index has posted slight losses in the Wednesday session. Currently, the DAX is at 13,155.00, down 0.22% on the day. On the release front, German Final CPI improved to 0.3%, matching the estimate. This marked a 4-month high. In the eurozone, Employment Change improved remained unchanged at 0.4%, matching the forecast. Industrial Production rebounded with a gain of 0.2%, above the forecast of 0.0%. In the US, The Federal Reserve meets for its monthly policy meeting, and is widely expected to raise rates to a range between 1.25% to 1.50%. Wednesday will be busy. On Wednesday, Germany and the eurozone release manufacturing PMIs, and the ECB will make a rate announcement.

Will the Federal Reserve press the rate trigger on Wednesday? The CME Group has priced in a quarter-point rate hike at 87%, so it would be a huge surprise if the Fed doesn’t raise the benchmark rate. Even though this move has been priced in, rate hikes tend to trigger a surge of confidence among investors, and a rate hike could boost global stock markets. Today’s move could be the start of a series of incremental hikes, as the odds of a January increase stand at 86%. The Fed has hinted that it could raise rates up to three times in 2018, but the pace of increases will depend to a great extent on the strength of the economy and inflation levels. The US labor market remains at full capacity and various sectors in the economy are reporting a lack of workers. Still, this has not translated into stronger wage growth, despite predictions from Janet Yellen and other Fed policymakers that a lack of workers is bound to push up wages.

Germany and the eurozone continue to post strong numbers, and this has helped keep the DAX at high levels. However, investor optimism softened in December. The well-respected ZEW Economic Sentiment indicator, a confidence barometer of institutional investors, slowed in December. Economic conditions on the continent are good, but investors have to keep an eye on political developments as well, and there are some worrisome developments. Germany still remains without a government, and uncertainty over Brexit continues to hover over the European Union.