Sample Category Title

Pound Edges Lower, British CPI Rises

The British pound has ticked lower in the Tuesday session. In North American trade, GBP/USD is trading at 1.3324, down 0.12% on the day. On the release front, British CPI came in at 3.1%, edging above the estimate of 3.0%. In the US, PPI posted a gain of 0.4%, matching the estimate. Core PPI came in at 0.3%, above the estimate of 0.2%. On Wednesday, the Federal Reserve is expected to raise rates to a range between 1.25% to 1.50%. As well, the US releases CPI reports.

Brexit negotiations are back on track, and the European Union is expected to give a green light to the talks shifting to trade issues. For months, the talks have been stuck over three issues: 1) the size of Britain's divorce bill; 2) the role of the European Court of Justice; and 3) Northern Ireland's borders with the UK and Ireland. After some feverish negotiations, sufficient progress has been made on these issues to satisfy the EU, which holds a key summit next week. What will a new trade relationship look like? Brexit policymakers appear divided on this question. On Sunday, Brexit minister David Davis said he envisions a comprehensive trade deal with Europe, which would be signed just after Britain leaves the bloc. The EU recently signed a free-trade treaty with Canada, and Davis said that he wants an agreement "Canada plus plus plus", meaning that the deep trading ties between the sides and access to European markets would remain intact. International Trade Secretary Liam Fox went a step further on Tuesday, saying that he wants a post-Brexit trading relationship with the EU that is "virtually identical" to the current relationship. It's questionable whether the EU would agree with Fox's comments, as Brussels doesn't want to give Britain too sweet a deal which could give other EU members any ideas about departing from the bloc.

All eyes are on the Federal Reserve, which meets on Wednesday for a policy meeting. The markets are expecting a quarter-point rate hike. Another rate hike is expected in January, with fed futures pricing a rate hike at 87%. The Fed has hinted that it could raise rates up to three times in 2018, and this upward movement in rates will likely propel the US dollar upwards. The US labor market remains at full capacity and various sectors in the economy are reporting a lack of workers. Still, this has not translated into stronger wage growth, despite predictions from Janet Yellen and other Fed policymakers that a lack of workers is bound to push up wages.

Crude Oil Trading In A Bullish Impulse and Aiming For 60/61 Per Barrel

Good day traders and welcome to the US session.

Today, let's talk about crude oil, its short and medium time frame.

On the daily chart crude oil has completed a complex correction labeled as wave II or B at the 42.03 level from where we started to track a new bullish impulse. An impulse is a five wave pattern, so there is room for much more gains on energy market since we see current leg up as blue wave 3 of an impulse. Wave 3) has in general five clear waves, which means oil price can still climb up to 60/61.9$ per barrel.

Crude oil, daily

Regarding the 4h chart of crude oil, we can see that energy found a possible base for higher degree wave 4) at the 55.77 level; near the Fibonacci support ratio of 38.2 and near the lower EW base channel line. A bounce followed from there, which can suggest higher degree wave 5) to be in progress towards 60.0 region and above in impulsive fashion. This means in clear five waves.

Crude oil, 4h

USDJPY Return above Daily Cloud is Bullish Signal

The dollar regained traction and returned above cloud top, boosted by better than expected US data.

Fresh bullish acceleration posts new highs (the highest in one month) and on track for the third consecutive close above daily cloud top which would boost bullish signal for test of immediate target at 113.81 (Fibo 76.4% of 114.73/110.83 descend) and possible extension towards key short-term barrier at 114.73 (06 Nov peak).

Fed's verdict tomorrow is expected to further boost the greenback on hawkish post-rate decision comments.

Res: 113.81; 114.27; 114.45; 114.73

Sup: 113.51; 113.25; 113.06; 112.83

Yen Remains Unchanged, Japanese Data Beats Estimates

The Japanese yen is unchanged in the Tuesday session. In North American trade, USD/JPY is trading at 113.65, up 0.17% on the day. On the release front, Japanese indicators pointed upwards and beat their estimates. PPI rebounded with a gain of 3.5%, above the estimate of 3.3%. Tertiary Industry Activity gained 0.3%, edging above the estimate of 0.2%. In the US, PPI posted a gain of 0.4%, matching the estimate. Core PPI came in at 0.3%, above the estimate of 0.2%. Later in the day, Japan releases Core Machinery Orders, which is expected to gain 2.8%. On Wednesday, the Federal Reserve is expected to raise rates to a range between 1.25% to 1.50%. As well, the US releases CPI reports.

All eyes are on the Federal Reserve, which meets on Wednesday for a policy meeting. The markets are expecting a quarter-point rate hike. Another rate hike is expected in January, with fed futures pricing a rate hike at 87%. The Fed has hinted that it could raise rates up to three times in 2018, and this upward movement in rates will likely propel the US dollar upwards. The US labor market remains at full capacity and various sectors in the economy are reporting a lack of workers. Still, this has not translated into stronger wage growth, despite predictions from Janet Yellen and other Fed policymakers that a lack of workers is bound to push up wages.

Is the Bank of Japan preparing the ground for a change in monetary policy? Kuroda has long insisted that there will be no reduction of stimulus until the Bank's inflation target of 2% is met. There has been pressure on him to reconsider, given the marked improvement in Japanese economy this year. However, the governor has recently dropped subtle hints about easing monetary policy. Last week, Kuroda said that a change in economic conditions could lead the BoJ to raise its yield target, which would be a significant change to current policy. Kuroda noted that an exit from quantitative and qualitative easing would be "quite an important topic" to communicate to the markets. Although the BoJ is unlikely to tighten policy before next year at the earliest, these deliberate hints indicated that the Bank is preparing for a time when conditions will warrant tightening monetary policy, after years of an ultra-accommodative stance.

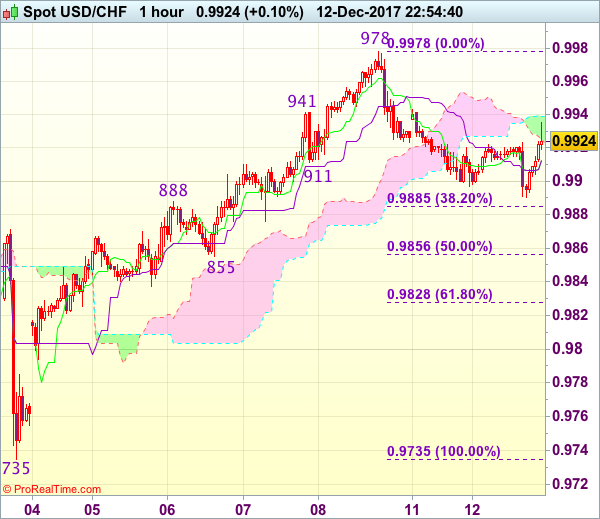

Trade Idea Wrap-up: USD/CHF – Buy at 0.9860

USD/CHF - 0.9929

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 0.9913

Kijun-Sen level : 0.9913

Ichimoku cloud top : 0.9939

Ichimoku cloud bottom : 0.9923

Original strategy :

Buy at 0.9860, Target: 0.9970, Stop: 0.9825

Position : -

Target : -

Stop : -

New strategy :

Buy at 0.9860, Target: 0.9970, Stop: 0.9825

Position : -

Target : -

Stop : -

Although the greenback has rebounded after finding support at 0.9890, reckon upside would be limited to 0.9950 and risk remains for another corrective fall, below said support would bring retracement of recent rise to 0.9885 (38.2% Fibonacci retracement of 0.9735-0.9978) is likely, however, downside should be limited to 0.9855-60 (50% Fibonacci retracement) and bring another rise later, above 0.9950 would suggest the retreat from 0.9978 has ended, bring retest of this level, break there would signal recent upmove has resumed and extend gain to 1.0000 but price should falter below recent high at 1.0038.

In view of this, would not chase this rise here and we are looking to buy dollar on subsequent pullback as 0.9855 support should contain downside. Only below 0.9825-30 (61.8% Fibonacci retracement of 0.9735-0.9978) would abort and signal top has been formed, bring further fall to 0.9800.

USD Holds Cautious Positive Bias ahead of Fed Decision

- European equity markets recovered from opening weakness and currently trade with small gains. US stock markets opened mixed. The S&P and the Dow show marginal gains. The Nasdaq opened little changed.

- US producer price inflation surprised on the upside last month amid a rebound in oil prices driving up costs for businesses. The producer price index - a key measure of industrial inflation - was up 0.4% M/M in November. November NFIB Small Business Optimism unexpectedly surged to 107.5, the highest level since 1983.

- EU countries have toughened their stance on Brexit negotiations, making clear that talks on a future EU-UK relationship will not begin until March, and insisting that Britain will stay fully covered by EU rules during a transition period after it leaves the bloc in 2019.

- British inflation unexpectedly rose to its highest level in nearly six years in November, tightening the post-Brexit vote squeeze on households whose spending is the main driver of the country's economy. Consumer price inflation hit an annual rate of 3.1% in November, pushed up by air fares, computer games and the price of chocolate.

- The mood among German investors worsened more than expected in December, a ZEW survey showed, reflecting uncertainty over the policies of a government yet to be formed, Britain's expected exit from the EU and reforms in the bloc. The expectations component declined from 18.7 to 17.4. The current situation index rose from 88.8 to 89.3.

- Swedish inflation came in higher than the central bank's estimate for a second consecutive month, giving policy makers an excuse to start winding back their extraordinary stimulus measures. Underlying consumer prices, which adjust for changes in mortgage costs, rose 2.0% in November, beating the 1.8% consensus.

- Europe's energy markets were rattled for a second consecutive day after an explosion at a natural gas hub in Austria threatened supplies already pinched from a closed pipeline in the North Sea and a cold snap across the continent.

Rates

Higher oil prices, strong data and recovering stocks

Global core bonds lost slightly ground today. The Bund opened stronger in line with gains for the US Note future on the back of Asian risk aversion. Several factors contributed to a change from the European start onwards. First European stock markets gradually recovered. Second, oil prices increased further as an explosion in an Austrian gas hub rattled European energy markets for a second consecutive day. Third, global eco data beat forecasts with upside CPI surprises in the UK and Sweden, higher PPI in the US, a stellar NFIB small business optimism and good German ZEW.

At the time of writing, the US yield curve bear flattens with yields 2.5 bps (2-yr) to 1.2 bps (30-yr) higher). Traders continue to put themselves in line with the FOMC's scenario of 3 rate hikes next year. We expect tomorrow's new dot plot to confirm this. The German yield curve bear steepens with yield changes ranging between -0.3 bps (2-yr) and +2.3 bps (30-yr). The German 10-yr yield is finally (slowly) moving away from 0.3% support. On intra-EMU bond markets, 10-yr yield spread changes versus Germany widen 3 bps for Portugal, Spain and Italy. Greece outperforms (-12 bps).

First details of next year's Belgian funding plans appeared. The debt agency is aiming to use a new bond via syndication in Q1 2018 with a tenor of 15-year or more. They also plan to frontload issuance again and are readying a first ever green bond. Last year, Poland and France already did the same.

Currencies

USD holds cautious positive bias ahead of Fed decision

Markets showed no clear trend in Europe this morning. A very strong NFIB small business confidence and a higher than expected PPI finally tilted the intraday balance in favour of the dollar, but the moves remained modest ahead of tomorrow's Fed decision. EUR/USD trades near 1.1740. USD/JPY holds in the mid 113 area.

Asian equities opened mixed, but lost ground as trading proceeded. There was no obvious driver. Oil extended its recent rebound, with Brent trading at the highest level in 2 ½ year, but there were again few spill-off effects on other markets. The trade-weighted dollar held near the highest level in two weeks. USD/JPY stabilized in the mid 113 area, despite softer equities. EUR/USD held in the 1.1775 area.

European equities lost temporary a few ticks after the open, but soon decoupled from the risk-off sentiment in Asia and returned back into positive territory. The Bund opened marginally stronger, but core yields soon bottomed. Changes in interest rate differentials were limited, but USD/German (EMU) spreads held at/close to the recent peak protecting the downside of the dollar. German ZEW investor confidence was close the expectations and no issue for markets. EUR/USD and USD/JPY held extremely tight ranges. If anything, the dollar received a cautious bid going into the start of the US trading session.

US NFIB small business confidence jumped from 103.8 to 107.5, the highest level since 1983! US producer prices also rose slightly faster than expected. Headline PPI rose 0.4% M/M and 3.1% Y/Y (from 2.8 %; 2.9% Y/Y was expected). One couldn't expect PPI data to change market sentiment in a profound way ahead of tomorrow's CPI and Fed policy decision, but the report didn't pass unnoticed. US bond yields headed further north with the 2-year yield setting yet another cycle top (1.84 area). The dollar also gained a few ticks, in particular against the euro. EUR/USD trades in the 1.1745 area. USD/JPY showed little reaction and hovers in the mid 113 area. So, the dollar held up quite well today. EUR/USD even near last week's pre-payrolls low (1.1730 area).

Sterling doesn't profit from 3%+ UK inflation

Sterling showed a diffuse picture today. Overnight headlines from UK government members including Trade Secretary Liam Fox and Brexit minister Davis on the nature of last week's Brexit/separation deal (non-legally binding) caused quite some nervousness amongst EU officials. Sterling trades with a slightly negative bias this morning, but the move had no strong momentum. UK headline inflation was higher than expected at 3.1% Y/Y. Core inflation was largely as expected (2.7% Y/Y). Sterling showed some nervous swings after the publication of the report, but again didn't capture a clear trend. Investors probably assume that it will be difficult for the BoE to raise rates as long as real wage growth remains low/negative. EUR/GBP finally declined to the 0.88 area, partially inspire by the intraday decline of EUR/USD. Cable developed an erratic trading pattern in in the mid 1.33 area. Tomorrow, the UK labour market data, including the earnings data, will be published.

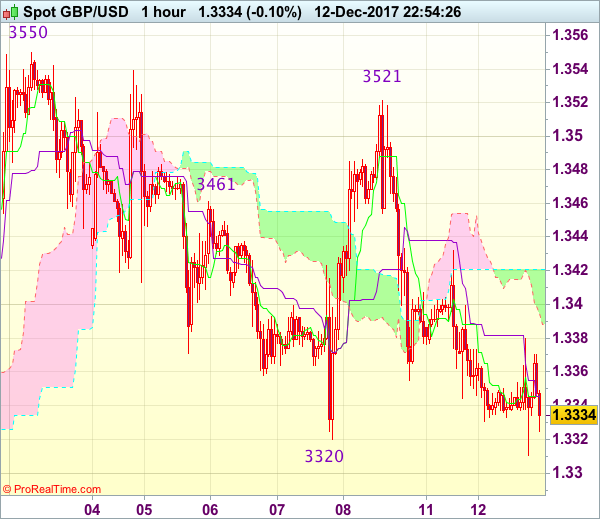

Trade Idea Wrap-up: GBP/USD – Stand aside

GBP/USD - 1.3333

Most recent candlesticks pattern : N/A

Trend : Sideways

Tenkan-Sen level : 1.3346

Kijun-Sen level : 1.3346

Ichimoku cloud top : 1.3421

Ichimoku cloud bottom : 1.3388

New strategy :

Stand aside

Position : -

Target : -

Stop : -

Although cable’s retreat from 1.3521 has kept sterling under pressure and near term downside risk remains for weakness towards 1.3310-20, however, as outlook remains consolidative, reckon downside would be limited and further choppy trading would take place. A drop below 1.3310-20 would revive bearishness and signal top has been formed at 1.3550 earlier, bring retracement of recent rise to 1.3280, then towards 1.3250 but support at 1.3221 should remain intact.

In view of this, would not chase this fall here and would be prudent to stand aside for now. On the upside, expect recovery to be limited to 1.3400 and the Ichimoku (now at 1.3418-21) should hold, bring another decline later. Above resistance at 1.3432 would bring a stronger rebound to 1.3475–80 but still reckon resistance at 1.3521 would hold from here, bring retreat later.

Trade Idea Wrap-up: EUR/USD – Sell at 1.1835

EUR/USD - 1.1745

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 1.1764

Kijun-Sen level : 1.1774

Ichimoku cloud top : 1.1778

Ichimoku cloud bottom : 1.1773

Original strategy :

Sell at 1.1835, Target: 1.1735, Stop: 1.1870

Position : -

Target : -

Stop : -

New strategy :

Sell at 1.1835, Target: 1.1735, Stop: 1.1870

Position : -

Target : -

Stop : -

Although the single currency retreated after meeting resistance at 1.1812, as long as support at 1.1730 holds, near term upside risk remains for another corrective bounce to said resistance, then towards 1.1835 (50% Fibonacci retracement of 1.1940-1.1730), however, reckon upside would be limited and bring retreat later, below said support at 1.1730 would confirm recent decline has resumed and extend weakness to previous key support at 1.1713. Looking ahead, only break there would retain bearishness for subsequent decline towards 1.1660-70.

In view of this, we are looking to sell euro on further subsequent recovery as said resistance at 1.1815 should limit upside and bring another decline. Above 1.1845-50 would defer and suggest low is formed, bring a stronger rebound to 1.1875-80 first.

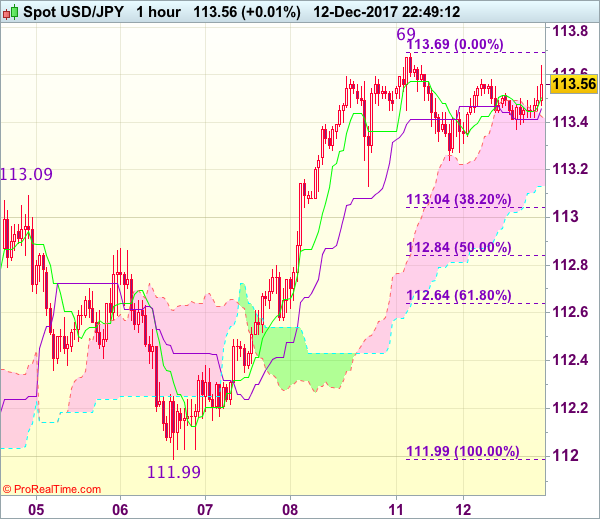

Trade Idea Wrap-up: USD/JPY – Buy at 112.90

USD/JPY - 113.57

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 113.48

Kijun-Sen level : 113.41

Ichimoku cloud top : 113.49

Ichimoku cloud bottom : 113.03

Original strategy :

Buy at 112.90, Target: 114.00, Stop: 112.55

Position : -

Target : -

Stop : -

New strategy :

Buy at 112.90, Target: 114.00, Stop: 112.55

Position : -

Target : -

Stop : -

Dollar’s retreat after rising to 113.69 yesterday has retained our view that consolidation below this level would be seen and pullback to 113.00-05 (38.2% Fibonacci retracement of 111.99-113.69), however, reckon 112.80-85 (50% Fibonacci retracement) would hold and bring another rise later, above said resistance at 113.69 would extend recent rise from 110.84 low to resistance area at 113.91-114.07 but a sustained breach above this region is needed to signal early uptrend has resumed for headway to 114.34.

In view of this, would not chase this rise here and would be prudent to buy dollar again on pullback as 112.90-00 should limit downside and bring another rise later. Below 112.80-85 (50% Fibonacci retracement of 111.99-113.69) would defer and risk test of 112.55-60 but only break of latter level would signal top is formed instead, bring subsequent fall to 112.20-25.

US: Producer Prices Show Strengthening Inflation

The Producer Price Index (PPI) for final demand rose 0.4 percent in November as energy prices moved up again. Ex-food, energy and trade services, however, the PPI also points to inflation picking up.

Broad Gains in Producer Prices

- Producer prices rose more than expected in November with the index rising 0.4 percent for a third straight month. The PPI for final demand is now up more than 3 percent over the past year.

- Goods prices led the charge. While energy prices increased 4.6 percent, food and core goods prices both rose 0.3 percent.

- The services index was up 0.2 percent despite a pullback in the trade services component, which is measured as margins.

Core Strength

- Excluding food, energy and trade services, the PPI also rose 0.4 percent. Over the year, the "core-core" improved to 2.4 percent.

- Since methodology changes in 2014, the PPI has diverged more noticeably from the more closely watched CPI and PCE measures. Nevertheless, the pickup over the year will be welcomed by the Fed as an indication that inflation is gradually moving up.