Sample Category Title

Challenging To Find A Trend In Currency Markets

Challenging to find a trend in currency markets

It's difficult to determine a trend into year-end as USD has been dominated by Washington noise of late, be it the tax bill debate or the reports around the Mueller investigation.

As we enter the business end of the of the week for currency traders, position adjustments are steering markets as the focus is shifting to Fridays AHE release while the exhaustive Tax Reform process remains in the centre of all debate.

Hopefully, when we get closure on Tax reform, the balance of risks will move from political filibuster to economics and central bank policy.

The U.S. trade deficit increased to a nine-month high in October because of rising oil prices and the widening of America's long-established deficits with China and Mexico.

US 10 year yields failed to hold above 2.4 % while two-year yields touched their highest level since Oct 2008. On the short end of the curve, investors are pricing in multiple US rate hikes while the markets insatiable appetite for long-dated notes was on display again after the trade deficit widened to its highest level since January.

AS the yield curve shifts flatter than a pancake, it is sending a clear and unmistakable signal that while the tax reform will be a boon to tax-sensitive sectors, bond markets are not buying into the boost to economic growth bluster the GOP have been dishing out.

Institute for Supply Management (ISM) said its non-manufacturing index fell in November, missing economists' expectations which has caused a bit of dollar retracement but overall the market has bigger fish to fry. November wage growth is the most critical data point following firmer core CPI and PCE in October. Expectations are for the data to shift higher to 2.7%YoY, based stronger November reading. But we should expect both the dollar and bond market to be reactive to any data delta +or – while equity market likely remains unprejudiced.

The jury remains out on the Tax reform trade as both bond and currency markets remain in flux trying to determine Tax Reforms transitory boost to real GDP growth a the cost of a cost of massive deficits and more debt.

Equities market are likely feeling tax fatigue, and it took little more than a weaker ISM to shift the bullish sentiment as US equity markets declined modestly in New York

The British Pound

Brexit Buzz strikes again!!.Reports are circulating that Boris Johnson and Michael Gove will lead a Cabinet revolt against Theresa May over fears she is forcing a soft Brexit.The pound fell 40 pips in a blink with little to no volume. Trade should remain at the mercy of incoming headlines and given the low GBP liquidity in Asia even more so in early Asia; things could get a bit chippy as market eyes 1.3400. Fortunately, long positioning is not too heavy, so we're not expecting any gap trap or falling knife scenarios

The Euro

So much for the Euro being the markets driving force this week. The Euro seems more than comfortable holding on to the 1.18 handle, but as we've continued to make lower highs the past few session, from a positioning perspective, it suggests we could see a move lower despite the positive medium-term outlook.

The Japanese Yen

The USDJPY is trading constructively despite US ten-year yields falling and tax reform euphoria losing steam. Although some traders remain in buy the dip mode, far too much ambiguity persists to get pent up bullish right now. Likely best to sit on the fence with AHE looming.

The Malaysian Ringgit

Its been a fantastic 24 hours for the Ringgit despite pulling back from yesterday highs. To recap: The move below 4.06 initially triggered a wave of exporter selling to a low of 4.0470 But fast money speculators also got into the act after the China PMI's came in above expectation which spread positive sentiment across regional currencies. But after breaking the critical 4.05 level offers were far and few between and profit taking flow drove the USD higher.

Oil prices remain stable to higher after OPEC reduction which offers benefits asymmetrically to MYR as Malaysia is net oil exporter and fiscal recipient of the proceeds. Also, ” Fair value” quantification peg the Ringgit closer to the 3.9 -3.80 USDMYR suggesting the MYR rally could run deeper if the economic and monetary policy stars align. While upcoming elections could cause a hic-up, a stronger currency would be a definite signpost that the economy is doing exceptionally well so we could see the government lend support to the stronger MYR narrative for an election campaign bounce.

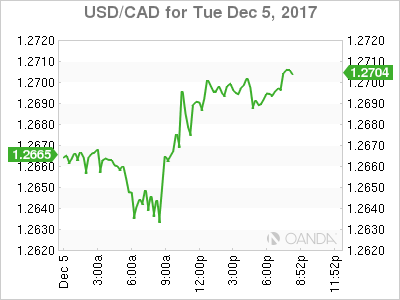

USD/CAD Canadian Dollar Lower Ahead Of Bank Of Canada

US Dollar rebounds ahead of ADP payroll report

The USD appreciated on Tuesday as the US tax reform appears to have entered its final stretch. The two versions, one by the US congress and other passed by the Senate will reconcile into a final version before being presented to President Trump. The economic calendar this week was always going to be dominated by the employment releases. Private payroll processor ADP will release employment data on Wednesday, December 6 at 8:15 am EST. The report is forecasted to show a gain fo 191,000 jobs in November. The report will pave the way for the major jobs report due on Friday with more than 200,000 positions forecasted to have been added, but once again the emphasis will be on the rise of hourly wages as a signal of higher inflation.

The Bank of Canada (BoC) will release its benchmark rate statement on Wednesday, December 6 at 10:00 am EST. The central bank is anticipated to keep rates unchanged at 1.00 percent after already hiking twice in 2017. Canadian jobs data defied estimates and gained 79,500 jobs in November raising the probability of the next Canadian interest rate hike coming sooner rather than later, but the data will not influence the decision on Wednesday.

The official Energy Information Administration (EIA) figures will be released on Wednesday, December 6 at 10:30 am EST. The API weekly data showed a big drawdown of crude which was contrasted with a large buildup of gasoline and distillates. The price of crude will be impacted by the final number delivered tomorrow as global demand has risen while the Organization of the Petroleum Exporting Countries (OPEC) and other producers remain committed to reducing supply.

The EUR/USD lost 0.33 percent in the last 24 hours. The single currency is trading at 1.1825 after the US tax reform continues to push the dollar higher. The US Congress and Senate will be working together to merge their separate approved tax bills. The USD has faced a tough 2017 as the Trump rally started fading as the new Administration was faced with different obstacles some of their own making. The tax promised tax reforms are arriving almost a year late with some a difficult final stretch.

Despite economists pointing to three rate lifts from the U.S. Federal Reserve in 2018, the EUR is expected to appreciate next year as the European economy over-performs as the European Central Bank (ECB) starts removing some stimulus in their way to normalizing monetary policy.

Private payroll processor ADP will release employment data on Wednesday, December 6 at 8:15 am EST. The report is forecasted to show a gain fo 191,000 jobs in November. The U.S. Bureau of Labor Statistics will release the non farm payrolls (NFP) report on Friday, December 8 at 8:30 am EST. The economy is forecasted to have added 200,000 positions in November. Once again the emphasis will be on average hourly wages for signs on inflationary pressure.

The USD/CAD gained 0.17 percent on Tuesday. The currency pair is trading at 1.2694. The USD appreciated ahead of the release of employment data starting with the ADP payroll report. The loonie posted a five week high on Friday after the strong jobs report in Canada and the improved third quarter GDP. Some of the gains were taken back by the rise in the USD after the weekend’s vote on the Senate tax bill. As the tax reform process enters the final phase and with a potential strong employment data, some of the gains from the Canadian jobs report rally could be erased as the week continues.

A Reuters survey of 103 economists revealed that three US interest rate hikes are expected in 2018. The poll also showed that the December rate hike has a high probability and will come in at 25 basis points, the third rate hike of 2017. The BoC will be monitoring the economic indicators, but is not expected to modify monetary policy until next year when more of the unknowns such as the NAFTA renegotiation become clear and the impact on Canadian growth could be anticipated.

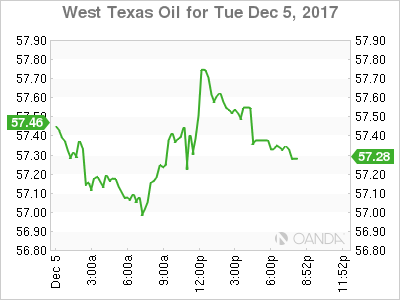

Oil rose in the last 24 hours. The price of West Texas Intermediate is trading at $57.50 ahead of the weekly inventory data out of the US. There are expectations of a stronger global demand for energy that combined with the 9 month extension to the Organization of the Petroleum Exporting Countries (OPEC) and other major producers production cut agreement. The API oil inventories fell 5.5 million barrels of crude, but rose 9.5 million barrels of gasoline and 4.3 million barrels of distillates. The official Energy Information Administration (EIA) figures will be released on Wednesday, December 6 at 10:30 am EST.

Market events to watch this week:

Wednesday, December 6

8:15am USD ADP Non-Farm Employment Change

10:00am CAD BOC Rate Statement

10:00am CAD Overnight Rate

10:30am USD Crude Oil Inventories

7:30pm AUD Trade Balance

Thursday, December 7

8:30am USD Unemployment Claims

11:00am EUR ECB President Draghi Speaks

Friday, December 8

4:30am GBP Manufacturing Production m/m

8:30am USD Average Hourly Earnings m/m

8:30am USD Non-Farm Employment Change

8:30am USD Unemployment Rate

Gold Slumps To 8-Week Low As Dollar Climbs

Gold continues to lose ground this week. In Tuesday's North American session, the spot price for an ounce of gold is $1264.55, down 0.90% on the day. In the US, In the US, ISM Non-Manufacturing PMI slowed to 57.4, missing the estimate of 59.2 points. On Wednesday, the US releases ADP Nonfarm Employment Change, with several key employment indicators to follow on Friday.

If Republican lawmakers have their way, President Trump will sign a tax relief bill in a few short weeks. The US Senate passed a tax reform bill on the weekend, but the vote was a squeaker, 51-49, as the vote went along party lines, with one Republican voting against the bill. Now that that the House and the Senate have passed tax bills, a conference committee will try and hammer out a uniform bill which can be sent to President Trump and signed into law. There are some differences in the two bills, notably individual tax rates, the alternative minimum tax, mortgage interest deductions and the estate tax. The Senate and House will have to work out their differences quickly, as the new “merged” bill will have to pass through in both houses. If the bill does become law, it will mark the first major tax reform in the US in 30 years, and could boost the US dollar and weigh on gold prices.

The markets are widely expecting the Federal Reserve to continue to raise rates in the near future, and this sentiment continues to weigh on gold prices. The CME has priced in a rate hike for both December and January at 85%, a slight drop from last week, but still at very high levels. If the US economy continues to perform at its impressive pace into 2018, we could see the Fed raise rates up to three times next year.

Bank of Canada Decides Next on Rates; Expected to Stand Pat

Next on the list of central bank policy meetings is the Bank of Canada which is expected to follow its Australian counterparts and keep interest rates on hold at 1.0% at its last rate-decision for 2017 on Wednesday. Although the economy seems to be approaching full capacity conditions, the central bank is likely to maintain monetary stimulus for the moment as recent data indicated that the economy is growing at a slower pace, while inflation is still trending far below the central bank's target.

Last Friday, the Canadian unemployment rate dropped surprisingly to a nine-year low of 5.9% in November, while the labour market added 79,500 jobs in the aforementioned period, posting twelve consecutive months of gains and reaching the highest increase in four years. However, another report showed that annualized GDP growth weakened to 1.7% q/q in the third quarter from the previous mark of 4.3% (downwardly revised from 4.5%) due to lower exports and household spending as well as to a cooling housing market.

Besides that, Canadian households remain among the most highly indebted in the world as sluggish wage growth and higher interest rates render it difficult for them to meet their obligations, while inflation is still near the lower bound of the BOC's target range of 1-3.0% due to an appreciating local currency which pressures import prices. Given the previous, another rate hike tomorrow would not seem suitable under the current state of the economy.

Uncertainties surrounding NAFTA negotiations could be also one of the reasons for policymakers to avoid further rate increases. In their fifth round of negotiations ending on November 21, the US, Canada, and Mexico failed to make progress on key elements of the treaty, spreading fears to local companies whose trade activities are heavily dependent on the US economy.

The BOC has raised interest rates twice this year, but markets are currently pricing a 20% chance of another increase on Wednesday. However, the monetary policy statement following the decision at 1500GMT would be in main focus for any hawkish comments which could give a lift to the loonie.

Looking at the technical picture, dollar/loonie holds a neutral to bearish bias as the pair is currently trending slightly below the 50-day exponential moving average, while market action is trying to push the price below the range of 1.2612-1.2915. The RSI maintains a negative slope below 50, hinting that a correction might take place in the near-term. If the pair indeed moves down, immediate support could be met at the lower bound of the range at 1.2612. From here any violation of this point would shift focus to 1.2430, which has been tested repeatedly in October and consequently paint a clear bearish picture. The two-year low of 1.2060 could also act as a barrier to steeper decreases. On the upside, resistance is likely to come from the 200-day EMA at 1.2840 and the previous top of 1.2915. Any close above this level would shift focus to the 1.3000 key-level.

US Trade Gap Widened in October

Recent Unites States trade data shows the widening of the trade deficit in October which reflects increases in imports of oil and other foreign goods and the slowdown in exports. According to the commerce department, the trade gap in services and foreign goods expanded 8.6% as compared to the previous month which was adjusted to 48.73 billion USD for October. Data showed that the US not only imported more oil as compared with the previous month but also at a higher average price. Strong consumer spending and high consumer confidence also drove imports higher. On the other hand, exports remained unchanged in October. The overall trade deficit has widened to 11.9% so far this year as compared with the same period in 2016.

Later Today, PMI data from the UK fell in November meaning activity in the UK's most profitable service sector eased in November. The service sector which accounts for 80% of the UK's economy fell to 53.8 in November from 55.6 in October. Keep in mind that the 50-point mark separates expansion from contraction. Instead of weaker expansion in the service sector, the latest data indicates that the economy is showing robust growth for the world's fifth largest economy.

EUR/USD

The EUR/USD is expected to trade with a bearish outlook. The pair is trading below its key resistance level at 1.1960 (last week's high), which is expected to limit the upside potential. A bearish cross has been identified between the 20-day moving average and the 50-day moving average. Additionally, the relative strength index lacks upward movement. Therefore, as long as 1.1960 (last week's high) holds on the upside, look for a new decline to 1.1805 and 1.1760. Alternatively, above 1.1960 look towards 1.2010 and 1.2045.

USD/CAD

The USD/CAD is under pressure and expected to extend its downside movement. Yesterday's high at 1.2726 is playing a resistance role and is likely to post new weaknesses. Both the 20 and 50 day moving averages are above the prices and should continue to push the prices lower. In which case, as long as 1.2726 is resistance, look for targets 1.2630 and 1.2590. Alternatively, above 1.2726, look for 1.2775 and 1.2805.

GBP/USD

The GBP/USD is expected to trade with a bearish outlook below 1.3537 (yesterday's high). The relative strength index is mixed to bearish and below its neutrality area. The 20 day moving average is turning down, confirming a negative outlook. To sum up, as long as 1.3537 is resistance look for 1.3369 (today's low) and 1.3320. Alternatively, above 1.3537 look for 1.3550 (last week's high) and 1.3580.

Pound Dips as Services Sector Growth Slows

The British pound has posted slight losses in the Tuesday session. In North American trade, GBP/USD is trading at 1.3451, down 0.22% on the day. On the release front, British Services PMI disappointed, slowing to 53.8 points. This missed the estimate of 55.2 points. In the US, ISM Non-Manufacturing PMI slowed to 57.4, missing the estimate of 59.2 points. On Wednesday, the US releases ADP Nonfarm Employment Change, the kickoff to several key employment indicators late in the week.

Just when the Brexit talks appeared to be on track, hopes of a major breakthrough were dashed on Monday. There had been hopes of a major announcement following a meeting between Prime Minister May and European Commission President Jean-Claude Juckner. However, it became apparent that wide gaps remain on two key issues – Northern Ireland and the European Court of Justice. With the UK leaving the European Union, something will have to be done about the border between Northern Ireland and Ireland, as the latter is a member of the EU. Another wrinkle is that the UK could put up a border with Northern Ireland, but the DUP, which is propping up the May government, is strongly against any border between the UK mainland and Northern Ireland. The second issue is whether the European Court of Justice will have a role protecting European citizens in the UK. The EU is in favor of a role for the court, but many British lawmakers feel that such a move would impinge on British sovereignty. The EU holds a key summit on December 12, and May, who is facing pressure at home over her handling of Brexit, is anxious to wrap up the non-trade issues and move on to trade talks by that date.

The US Senate passed a tax reform bill on the weekend, but the vote was a razor thin 51-49. The vote went along party lines, with one Republican voting against the bill. Now that that the House and the Senate have passed tax bills, a conference committee will try and hammer out a uniform bill which can be sent to President Trump and signed into law. There are some differences in the two bills, notably individual tax rates, the alternative minimum tax, mortgage interest deductions and the estate tax. The Senate and House will have to work out their differences quickly, as the new "merged" bill will have to pass through in both houses. If the bill does become law, it will mark the first major tax reform in the US in 30 years, and could boost the US dollar against the euro and other major currencies.

CRUDE OIL: Weakens, Eyes The 56.73 Zone

CRUDE OIL: The commodity faces further downside pressure as it looks to follow through lower on Tuesday. On the downside, support resides at the 57.00 level where a break will expose the 56.50 level. A cut through here will set the stage for a run at the 56.00 level. Further down, support resides at the 55.50 level. On the upside, resistance resides at the 58.00 level. Further out, resistance comes in at the 58.50 level. A break above here will aim at the 59.00 level and then the 59.50 level followed by the 60.00 level. All in all, CRUDE OIL remains biased to the downside

Yen Edges Higher, BOJ Inflation Unchanged

The Japanese yen has edged lower in the Tuesday session. In North American trade, USD/JPY is trading at 112.69, up 0.25% on the day. On the release front, BoJ Core CPI remained unchanged at 0.5%, matching the estimate. US ISM Non-Manufacturing PMI slowed to 57.4, missing the estimate of 59.2 points. On Wednesday, the US releases ADP Nonfarm Employment Change, the kickoff to several key employment indicators late in the week.

Another speech, same message. Bank of Japan Governor Haruhiko Kuroda spoke on Monday, and reiterated that the Bank would maintain its ultra-accommodative monetary policy in order "to achieve the 2 percent inflation target as soon as possible". The BoJ has been forced to constantly lower its inflation projections, yet the Bank has stubbornly stuck to the 2 percent target. Although the labor market remains tight, this has not translated into higher wages for workers, and nervous consumers have held tight to their purse strings, further contributing to a lack of inflation. Kuroda noted that global economic growth had improved, although he sounded a note of concern about President's Trump isolationist policy, saying that he hoped that global trade would be conducted under the multilateral trading system.

Tax reform legislation is picking up steam, as both houses of Congress have now passed tax bills. The Senate passed a tax reform bill on the weekend, but the vote was a razor thin 51-49. The vote went along party lines, with one Republican voting against the bill. Now that that the House and the Senate have passed tax bills, a conference committee will try and hammer out a uniform bill which can be sent to President Trump and signed into law. There are some differences in the two bills, notably individual tax rates, the alternative minimum tax, mortgage interest deductions and the estate tax. The Senate and House of Representatives will have to work out their differences quickly, as the new "merged" bill will have to pass through in both houses. If the bill does become law, it will mark the first major tax reform in the US in 30 years, and could boost the US dollar against the yen and other major currencies.

US: Non-Manufacturing Sector Momentum Remains Upbeat in October

The Institute for Supply Management's (ISM) non-manufacturing index dropped 2.7 points to 57.4 in November, marking a much sharper drop than the 1.1 point expected by markets as the effects of Hurricanes Harvey and Irma faded. Having said that, the index remains in healthy expansionary territory.

All of the main subcomponents declined, with new orders (-4.1 to 58.7) seeing the largest loss, followed by employment (-2.2 to 55.3), prices paid (-2.0 to 60.7) and business activity (-0.8 to 61.4). These moves partially reversed the hurricane-induced gains that materialized in the previous two months.

The supplier deliveries index was 4.0 points lower at 54.0 as longer lead times due to hurricane-related supply chain disruptions in the previous month faded, bringing the index closer to normal.

New export orders pulled back by 3.0 points but at 57.0 remains healthy.

The prices paid sub-index extended last month's loss, with the continued pull-back stemming from the dissipation of the temporary hurricane effects. Still, at 60.7, the index remains well above average levels seen over the past twelve months and is one of the best prints since 2012.

Comments from survey contacts remain positive, with some reporting a levelling off in business as the holiday season approaches. Additionally, construction industry contacts noted labor shortages in the West. Sixteen industries reported an expansion in November, and only one - agriculture, forestry, fishing & hunting - reported a contraction.

Key Implications

A pullback in the headline index was anticipated as the recent uptick resulting from hurricane-related supply chains disruptions faded. However, the headline index still remains at a healthy level, matching June's print. Going forward, we expect the robustly expanding U.S. economy and a rebounding energy sector will shore up performance in the non-manufacturing sector in the quarters ahead. Additionally, Hurricanes Harvey and Irma have highlighted the tightness of the labor market with shortages in the construction sector reported as preventing expansion.

In addition to existing strong demand fundamentals, the Republican tax reform plan should provide an added boost to profits, and may bolster business investment while benefitting producers whose margins are squeezed by rising input costs, including those in the construction and transportation industries, amongst others. All told, this report confirms that the services side of the economy will continue to support strong growth in the quarters ahead.

Dollar Profits Slightly from Rising Interest Rate Support

- European equities opened mixed, but gradually ceded ground throughout the day, showing losses of around 0.5%. In the US, the S&P and the Dow opened little changed. The Nadasq outperforms (+ 0.45%), recouping part of yesterday's setback.

- Growth in Britain's dominant services sector slowed and inflation accelerated during November. The services PMI declined from 55.6 to 53.8 (vs 55.0 expected).

- The EMU services PMI was confirmed at a strong 56.2. The composite PMI printed at 57.5, indicating ongoing strong growth in the fourth quarter.

- The Republican-controlled US House of Representatives voted to go to conference on tax legislation with the Senate, moving Congress another step closer to a final bill.

- Poland's central bank kept interest rates at a record low 1.5% after its "wait-and-see" stance came under question when inflation unexpectedly hit its target last month for the first time since 2012.

- Growth in the US services industry cooled from a 12-year high. The headline non-manufacturing ISM index eased from 60.1 to 57.4, while only a decline to 59.00 was expected. Earlier this afternoon the US October trade deficit widened more than expected to $48.7bn (from $44.9bn) as exports stabilized while imports rose on a monthly basis.

- Canada's hard-hit export sector showed unexpected signs of strength in October, posting the first increase since May on higher shipments to the United States while imports continued to disappoint. Canada's trade deficit declined to a five-month low of C$1.47 billion from C$3.36 billion in September.

Rates

Core bonds settle in narrow sideways ranges

Global core bonds settled in the same narrow sideways ranges from yesterday. Second tier EMU eco data didn't influence trading. October retail sales disappointed while the November services PMI was confirmed at a strong 56.2. Details showed signs of wage pressures within Italian, French and German services sectors. European stock markets lost slightly ground while Brent crude hovered around $62.5/barrel. During US dealings, focus turned to politics but markets shrug off the uncertainty for now. House and Senate members hope to streamline their US tax reform proposals before the end of the year, special prosecutor Mueller's investigation into alleged Russian ties with Trump's presidential campaign widens and a new debt ceiling (Dec 08) comes closer.

At the time of writing, the German yield curve bull flattens marginally with yields 1.7 bps (2-yr) to 0.7 bps (30-yr) lower. US yields increase by 1.6 bps (2-yr) to 2 bps (5-yr). On intra-EMU bond markets, 10-yr yield spread changes versus Germany narrow up to 2 bps with Greece outperforming (-56 bps). Today is the first trading day for five new bonds that were issued as part of €25.5 bn debt swap which occurred last week. The swap is a way to build a more normal yield curve and an entry point to market funding next year.

Currencies

Dollar profits slightly from rising interest rate support

There were few data with market moving potential today. The EMU services PMI remained strong as expected, but didn't cause any sustained USD gains. US ST yields rose further later in the session, widening the interest rate differential in favour of the dollar. Of late, the dollar often ignored the guidance form interest markets, but this time it helped the US currency to some cautious gains. EUR/USD trades in the 1.1830/35 area. USD/JPY is changing hands near 112.70.

Asian equity indices show a mixed picture, but gradually lost further ground as the trading session developed. A new setback in US tech stocks also affected (parts of) the Asian markets. Still, the dollar 'bottomed' after yesterday's late session setback. USD/JPY traded in the 112.60 area. EUR/USD changed hands near 1.1870.

European equities initially remained quit resilient considering the price action in the US and in Asia this morning. The final EMU services PMI (56.2) and the composite PMI (57.5) printed as expected, confirming the strong momentum in the economy. There was little impact on the euro. Later during the European morning session, European equities gradually drifted south. Initially, this decline weighted slightly on the dollar. However, fortunes changed again in favour of the US currency as US traders joined the fray. Interest rate differentials between the US and Germany/EMU widened further, especially at the short end of the curve. Of late this widening was often of little help for the dollar, but this time the dollar captured a better momentum. The October US trade balance widened more than expected as exports stabilized while imports rose. However, the report had little negative impact on the dollar. USD/JPY trades currently in the 112.50/60 area. EUR/USD is changing hands in the 1.1835 area. The jury is still out, but there are tentative signs that the big (ST) interest rate differential is gradually giving the dollar some additional downside protection.

Fall-out from Brexit failure on sterling remains modest

Sterling remained under pressure this morning. Yesterday's last minute failure to strike a deal on the separation topics in the Brexit negotiations kept the UK currency in the defensive. Especially the issue of the Irish border looks a high, complex hurdle for the UK government. DUP party, which supports May's government, doesn't want a different status for Northern Ireland from the mainland UK. Regarding the data, the UK services PMI came out slightly softer than expected at 53.8 from 55.6 (55.00 was expected). At the same time, price indictors in the report rose quite sharply, indicating risks of higher inflation even as activity slows. Sterling traded already off the recent lows at the time of the release of the report. EUR/GBP initially hovered in the mid-0.88 area, but drifted back lower later in the session as the euro ceded ground across the board. Cable finally settled in the low 1.34 area. In a broader perspective, the sterling loss due to yesterday's failed separation agreement was not excessive. EUR/GBP still holds a sideways consolidation pattern between 0.8733 and 0.9033. There is probably already quite some bad news on Brexit discounted and markets still hope on a final breakthrough further down the road.