Sample Category Title

Sterling Bruised by Brexit Uncertainty, Dollar Shaky

The British Pound is weak and wobbly following disappointment that Prime Minister Theresa May was unable to secure a Brexit deal on Monday.

Talks were brought to an abrupt halt after Northern Irish politicians threw a spanner in the works with their objections to border proposals. Although May is currently fighting hard to save the deal after the DUP veto, anxiety is likely to heighten as the Brexit clock ticks. With domestic political woes and Brexit uncertainty both weighing heavily on buying sentiment, the British Pound is likely to be exposed to further downside losses.

Steering away from political developments, activity in Britain's service sector dropped more than expected in November, eroding optimism over the British economy. UK Services decreased to 53.8 in November, down from 55.6 in October as volumes of new work eased and prices rose. The mixed market reaction towards November's soft Services PMI suggests that investors are overlooking the fundamentals and focusing instead on politics and Brexit developments.

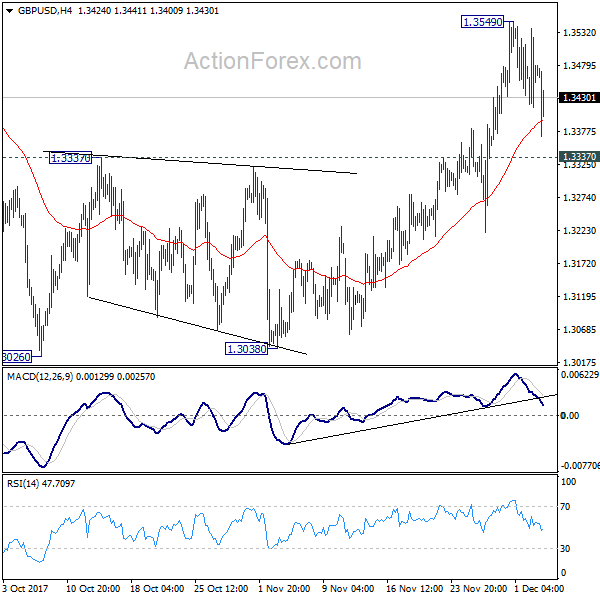

Taking a look at the technical picture, the GBPUSD bulls look exhausted and vulnerable on the daily charts thanks to Brexit uncertainty. Technical traders will continue to observe how prices react around 1.3400, with sustained weakness below this level opening a path back towards 1.3300. For bulls to snatch back control, the GBPUSD needs to break back above 1.3500.

Dollar Index wobbles above 93.00

The Greenback drifted slightly lower against a basket of major currencies on Tuesday, as investors still remained somewhat anxious despite the US Senate approving major tax cuts over the weekend. With the Senate passing its version of the tax bill, markets will be paying very close attention to how the Senate and the House of Representatives reconcile the difference between their two bills. From a technical standpoint, the Dollar Index remains under pressure on the daily charts below the 93.50 lower high. Sustained weakness below 93.50, followed by a break below 93.00, may encourage a further decline towards 92.50.

Commodity spotlight - Gold

Gold was under pressure during Tuesday's trading session, with prices trading towards $1273 as of writing. With the US non-farm payrolls data released later in the week, the yellow metal could remain range bound as investors stroll to the fence. From a technical standpoint, sustained weakness below the $1280 level, ahead of the pending NFP report may encourage a further decline towards $1267.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1836; (P) 1.1857 (R1) 1.1886; More....

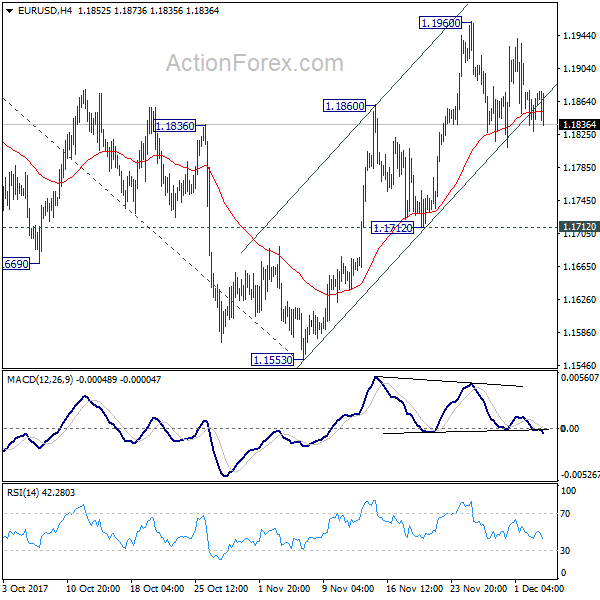

EUR/USD's consolidation from 1.1960 is still in progress and intraday bias remains neutral. With 1.1712 support intact, rise from 1.1553 is expected to resume later. Break of 1.1960 will turn bias to the upside for retesting 1.2091 high first. Break there will resume medium term up trend from 1.0339 and target 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494, which is close to 1.2516 long term fibonacci level. We'd expect strong resistance from there to bring reversal. On the downside, break of 1.1712 will indicate completion of the rise from 1.1553 and turn near term outlook bearish.

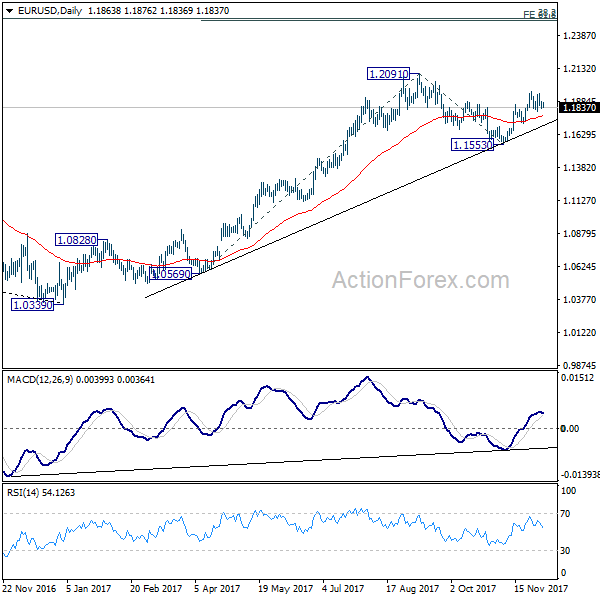

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1393) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3415; (P) 1.3476; (R1) 1.3541; More....

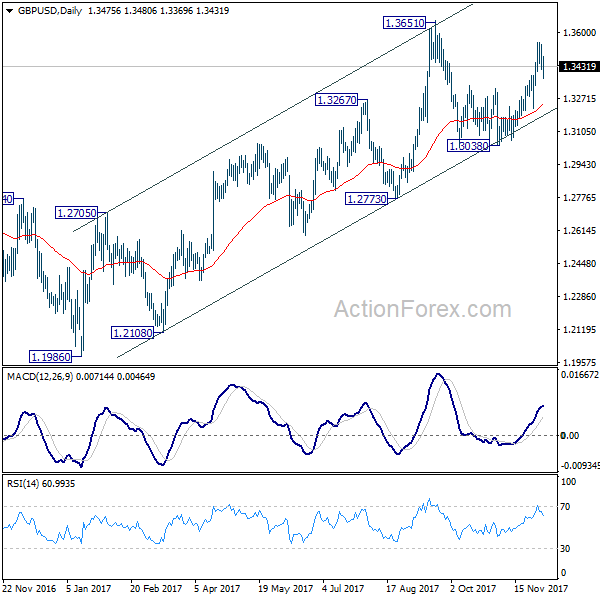

Intraday bias in GBP/USD remains neutral as consolidation from 1.3549 temporary top continues. Downside of retreat should be contained by 1.3337 resistance turned support to bring another rise. Above 1.3549 will target 1.3651 and above. However, decisive break of 1.3337 will argue that rise from 1.3038 has completed and turn bias back to the downside for this support.

In the bigger picture, while the medium term rebound from 1.1946 low is strong, it's still limited below 1.3835 key support turned resistance. As long as 1.3835 holds, we'd view such rebound as a correction. That is, we'd expect another leg in the long term down trend through 1.1946 low. However, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9804; (P) 0.9836; (R1) 0.9881; More....

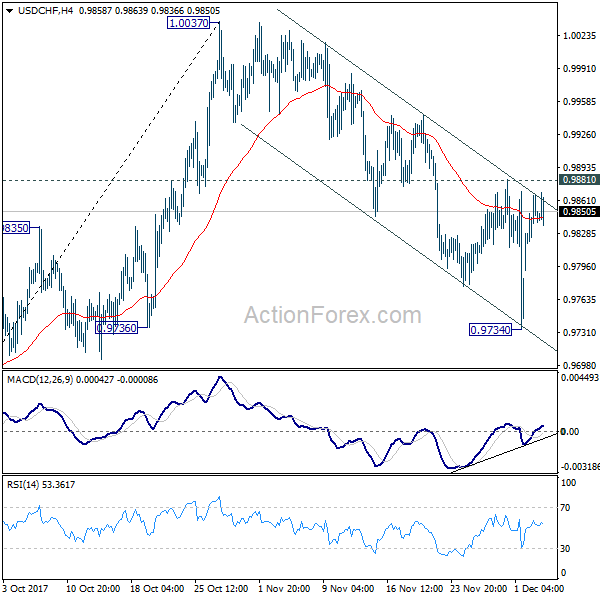

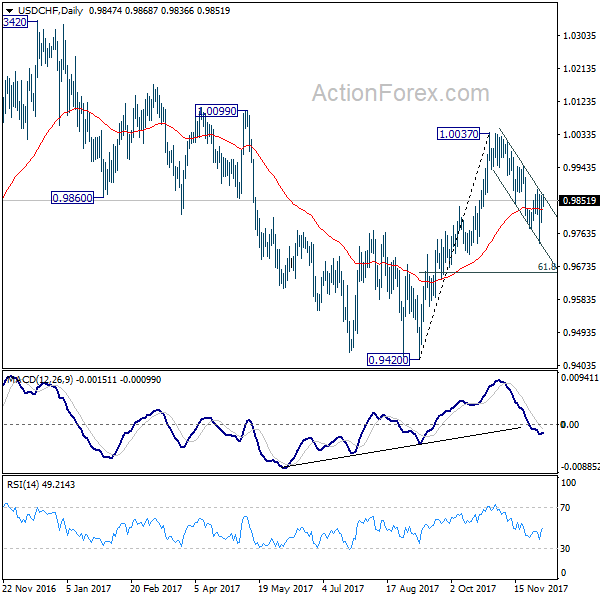

USD/CHF is staying in range of 0.9734/9881 and intraday bias remains neutral at this point. On the upside, break of 0.9881 resistance will indicate completion of the pull back from 1.0037. Intraday bias will then be turned back to the upside for retesting 1.0037. Below 0.9734 will extend the pull back. But we'll look for bottoming again below 61.8% retracement of 0.9420 to 1.0037 at 0.9656.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

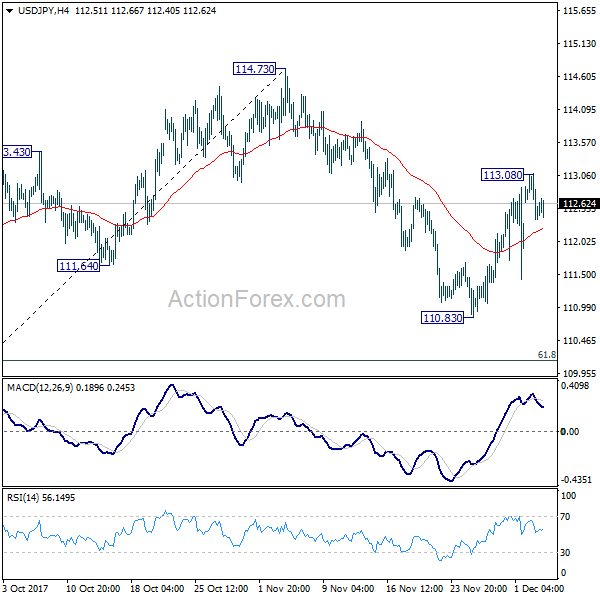

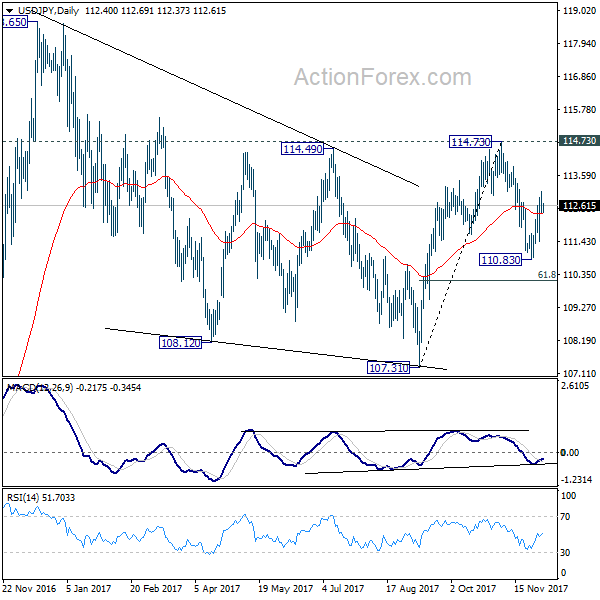

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.14; (P) 112.61; (R1) 112.86; More...

Intraday bias in USD/JPY remains neutral for consolidation below 113.08 temporary top. On the upside, above 113.08 will extend the rebound from 110.83 to retest 114.73 key resistance. Decisive break there will extend the rally from 107.31 to retest 118.65 high. On the downside, break of 110.83 will resume the decline from 114.73 instead. But in that case, we'll look for bottoming again below 61.8% retracement of 107.31 to 114.73 at 110.14.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed a 107.31. And medium term rise from 98.97 (2016 low) is resuming. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this will and extend the medium term fall back to 98.97 low.

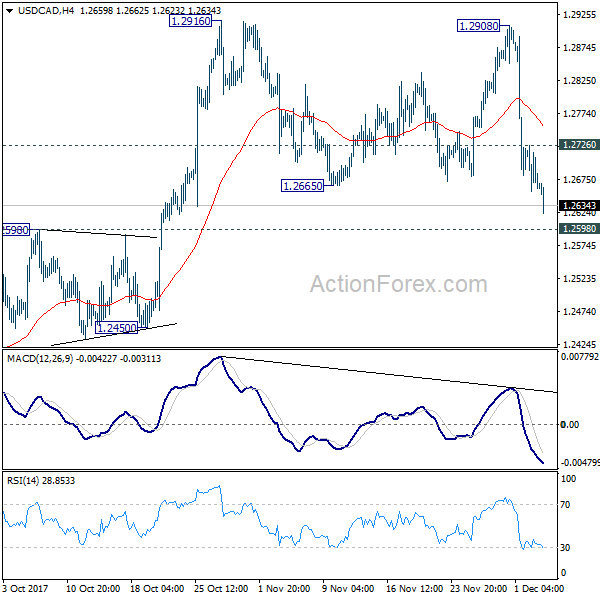

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2643; (P) 1.2685; (R1) 1.2714; More....

USD/CAD drops further to as low as 1.2623 so far as consolidation from 1.2916 continues. At this point, we'd still expect downside to be supported by 1.2598 resistance turned support to bring rise resumption. Above 1.2726 minor resistance will turn intraday bias back to the upside for 1.2916. Break of 1.2916 will resume the rally from 1.2061 and target 1.3065 medium term fibonacci level next. However, sustained break of 1.2598 will argue that rebound from 1.2061 has completed after hitting 55 week EMA (now at 1.2880). Near term outlook will be turned bearish in this case.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

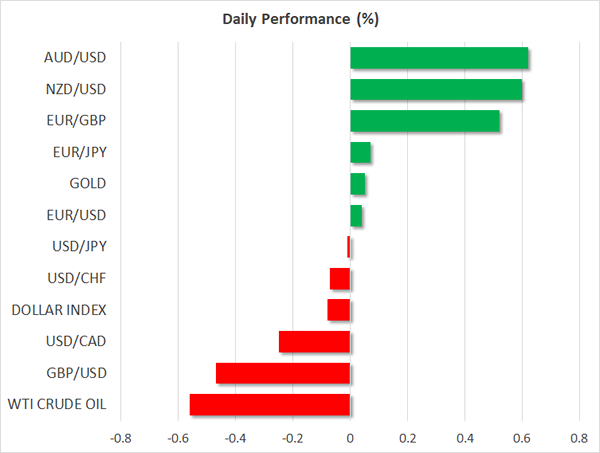

Commodity Currencies Higher, Sterling Remains Soft on Brexit Dead Lock

Sterling remains the weakest major currency today as traders are awaiting progress in Brexit negotiation. It probably takes a few more days for UK Prime Minister Theresa May to sort things out before she goes back to Brussels. Dollar regains some ground against Europeans and Yen. But commodity currencies are the ones who're shining today. In particular USD/CAD drops through 1.2665 support and is heading to 1.2598 key near term support level.

Released in US session, US trade deficit widened to USD -48.7b in October. Canada trade deficit narrowed to CAD -1.5b in October. The Senate Banking Committee will vote today on nomination of Jerome Powell as the next Fed chair. The confirmation should be smooth and it's generally expected that full Senate approval will be completed by early February.

UK PMI services disappointed in November

UK PMI services dropped to 53.8 in November, down from 55.6 and below expectation of 55.0. Markit chief business economist Chris Williamson pointed to the surge in prices in November that hurt services industry. He noted that "rising oil prices were again to blame in November, with firms also reporting the need to pass higher costs of a wide variety of other inputs on to customers as a result of the weak pound having driven up import prices." Also, "as such, the survey data suggest that inflationary pressures have yet to peak."

Nonetheless, "slower service sector growth comes as a disappointment after the improved performances of both manufacturing and construction in November. However, despite the weaker service sector expansion, the latest survey data indicate that the economy is on course to enjoy robust growth in the fourth quarter. The survey data are so far consistent with the economy growing at a quarterly rate of 0.45 per cent in the closing months of 2017."

UK PM Theresa May to brief Cabinet on Brexit

UK Prime Minister Theresa May will meet with her cabinet to brief the situation regarding Brexit negotiation with EU. Then May will try to persuade DUP leader Arlene Foster on the issue of Irish border, before going back to Brussels by the end of the week. Foster intervened the meeting between May and European Commission President Jean Claude Juncker, expressing her objection to the Irish border arrangement, which then caused the collapse of the talk. The pro-Brexit DUP was deeply concerned that the deal would make Northern Ireland leaving EU on different terms then other part of the UK.

European Commission chief spokesperson Margaritis Schinas said today that "there are some topics still open, which will need further consultation and negotiation, notably in London. The show is now in London. We stand ready here in the Commission to resume talks with the United Kingdom at any moment in time when we get the sign that London is ready."

ECB to pause asset purchase during Christmas holidays

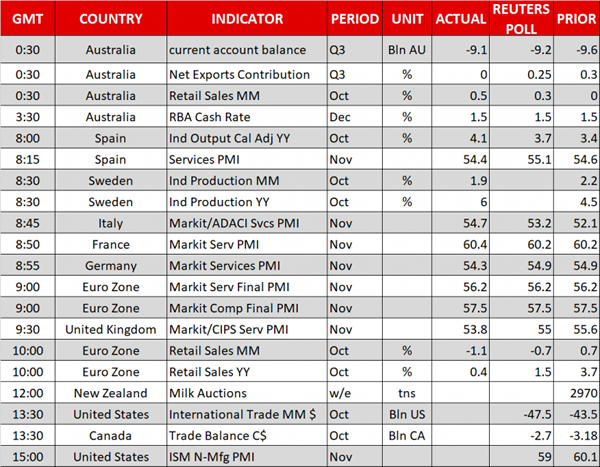

ECB will pause bond buying from December 21 to December 29 as market liquidity will drop sharply during Christmas holidays. And, ECB also said that purchases in December will be somewhat frontloaded to take advantage of the relatively better market conditions expected during the earlier part of the month. Purchases will resume on January 2 2018. From Eurozone, retail sales dropped -1.1% mom in October, worse than expectation of -0.7% mom. Eurozone services PMI was finalized at 56.2 in November, unchanged. German services PMI was revised down by 0.6 to 54.3. France services PMI was revised up by 0.2 to 60.4. Italy services PMI rose to 54.7 in November, above expectation of 53.2.

RBA stands pate, weary of soft inflation and wage growth

RBA left the cash rate unchanged at 1.5% today, following the last reduction in August 2016. The accompanying statement contained little surprise. While staying confident over the employment situation, policymakers remained weary of the persistently soft inflation and wage growth. The RBA stance is largely unchanged from the previous meeting. We retain the view that the policy rate would stay unchanged for the entire 2018. More in RBA Remains Cautious As Wage Growth Subdued.

Australia dollar was lifted earlier today by stronger than expected retail sales, which grew 0.5% mom, versus consensus of 0.3% mom. Also from Australia, current account deficit narrowed slightly to AUD -9.1b in Q3. Elsewhere, China Caixin PMI services rose to 51.9 in November, up from 51.2, above expectation of 51.5.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2643; (P) 1.2685; (R1) 1.2714; More....

USD/CAD drops further to as low as 1.2623 so far as consolidation from 1.2916 continues. At this point, we'd still expect downside to be supported by 1.2598 resistance turned support to bring rise resumption. Above 1.2726 minor resistance will turn intraday bias back to the upside for 1.2916. Break of 1.2916 will resume the rally from 1.2061 and target 1.3065 medium term fibonacci level next. However, sustained break of 1.2598 will argue that rebound from 1.2061 has completed after hitting 55 week EMA (now at 1.2880). Near term outlook will be turned bearish in this case.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:01 | GBP | BRC Retail Sales Monitor Y/Y Nov | 0.60% | -1.00% | ||

| 00:30 | AUD | Current Account Balance (AUD) Q3 | -9.1B | -8.8B | -9.6B | -9.7B |

| 00:30 | AUD | Retail Sales M/M Oct | 0.50% | 0.30% | 0.00% | 0.10% |

| 01:45 | CNY | Caixin PMI Services Nov | 51.9 | 51.5 | 51.2 | |

| 03:30 | AUD | RBA Rate Decision | 1.50% | 1.50% | 1.50% | |

| 08:45 | EUR | Italy Services PMI Nov | 54.7 | 53.2 | 52.1 | |

| 08:50 | EUR | France Services PMI Nov F | 60.4 | 60.2 | 60.2 | |

| 08:55 | EUR | Germany Services PMI Nov F | 54.3 | 54.9 | 54.9 | |

| 09:00 | EUR | Eurozone Services PMI Nov F | 56.2 | 56.2 | 56.2 | |

| 09:30 | GBP | Services PMI Nov | 53.8 | 55 | 55.6 | |

| 10:00 | EUR | Eurozone Retail Sales M/M Oct | -1.10% | -0.70% | 0.70% | |

| 13:30 | CAD | International Merchandise Trade (CAD) Oct | -1.5B | -2.3B | -3.2B | -3.7B |

| 13:30 | USD | Trade Balance Oct | -48.7B | -46.2B | -43.5B | -44.9B |

| 14:45 | USD | Services PMI Nov F | 55.3 | 54.7 | ||

| 15:00 | USD | ISM Non-Manufacturing/Services Composite Nov | 59 | 60.1 |

Canadian Dollar Improves to 2-Week High, Trade Balance Next

The Canadian dollar continues to move higher on Tuesday, after starting the week with slight gains. Currently, USD/CAD is trading at 1.2644, down 0.24% on the day. On the release front, both Canada and the US release Trade Balance, and the US will also publish ISM Non-Manufacturing PMI. On Wednesday, the Bank of Canada will set the benchmark rate and the US releases ADP Nonfarm Employment Change.

The Bank of Canada is expected to maintain interest rates at 1.00% on Wednesday, but may have to consider another rate hike early in 2018, if Friday's sparkling numbers Friday continue. Canadian employment change soared to 79.5 thousand, crushing the estimate of 10.2 thousand. This marked 12 straight months of job gains and helped drive the unemployment rate down to 5.9%. As well, September GDP rebounded with a gain of 0.2%, edging above the estimate of 0.1%. The impressive numbers boosted the Canadian dollar by some 1.6% on Friday, its strongest 1-day gain in 2017. If the BoC rate statement sounds optimistic about the Canadian economy, the Canadian dollar could continue to rally.

The US Senate passed a tax reform bill on the weekend, but the vote was a razor thin 51-49. The vote went along party lines, with one Republican voting against the bill. Now that that the House and the Senate have passed tax bills, a conference committee will try and hammer out a uniform bill which can be sent to President Trump and signed into law. There are some differences in the two bills, notably individual tax rates, the alternative minimum tax, mortgage interest deductions and the estate tax. The Senate and House will have to work out their differences quickly, as the new "merged" bill will have to pass through in both houses. If the bill does become law, it will mark the first major tax reform in the US in 30 years, and could boost the US dollar against the euro and other major currencies.

US Futures Mixed, Major Sector Rotation Taking Place

The European technology sector is mimicking what happened over on Wall Street

UK and EU walked away yesterday without having any deal

Spanish industrial number painted more cheerful painting

US futures are mainly focused on any new development on the US reform. Markets have priced in the impact of the US tax reform to a large extent, despite the fact that these changes are yet to be signed by President Trump and become a law. The fact is that the road for these changes to become a law isn't that smooth yet and any bumps could bring some shocks for investors. The European technology sector is mimicking what happened over on Wall Street. A major sector rotation is taking place. Money is coming out of technology sector and moving in those sectors which are going to be the beneficiary of the US tax overhaul. Hence the performance of the US financial and energy sector has anchored during the past few days.

After yesterday's breakdown in the Brexit negotiations, we aren't experiencing much enthusiasm for the risk on trade over in Europe. Both sides walked away yesterday without having any deal. Investors were optimistic that both sides will able to sign a deal for the U.K. leaving the European block.

The uncertainty around the first phase of Brexit negotiations has brought more than usual volatility for Sterling. Fairly recently, the heavy sell off in sterling has come off from its peak, triggered by the fear that the deadlock in Brexit negotiations isn't going anywhere and the optimism around it was over inflated. The UK services data is also having an influence on sterling today as it confirmed that the services sector is picking up some chill and inflation has further accelerated- a combination which is fatal for the UK's economy.

Over in Europe, the Spanish industrial number painted more cheerful painting for the Spanish economy. The economy is gaining more momentum, thanks to the broad rebound in the eurozone economy. Countries like Greece have also started to perform much better. The most encouraging element is that the strife in Catalonia hasn't left any catastrophic impact on the region. We also had the European retail sales data which showed that shoppers were not generous towards their shopping habit in eurozone during October. However, we only have a modest drop of 0.5 percent.

Sterling Struggles As Brexit Fears Loom, Stocks Down, Dollar & Loonie Gather Attention

Here are the latest developments in global markets:

Forex: The Australian dollar continued to trade around three-week highs at $0.7645 (+0.63%) following upbeat data on retail sales and the RBA’s decision to keep rates steady at record low levels. In the Eurozone though, retail sales disappointed markets with the measure diving unexpectedly to a three-week low as food prices fell sharply. Euro/dollar retreated in the wake of the data but erased its losses afterwards, trading flat at $1.1872. Sterling dipped to a five-day low of 1.3369 before it bounced back above the 1.34 key level (-0.50%) after the British service PMI missed forecasts. However, stalled Brexit talks were the main drag on the market. Euro/pound approached a one-week high at 0.8866 (+0.56%). Dollar/yen was moving sideways around 112.40.

Stocks: European stocks were on the backfoot as sell-off in tech and healthcare shares gained momentum. The pan-European STOXX 600 declined by 0.53%, the German DAX 30 fell by 0.66% while the French CAC 40 retreated by 0.70%. The British FTSE was steady, finding support on a weaker pound.

Commodities: Oil prices remained weak, with the WTI crude falling by 0.63% to $57.11 per barrel amid concerns over rising US supply output. Brent declined by 0.35% to $62.23. Gold stood flat at $1,276.40 per ounce.

Day ahead: US & Canada release trade figures; US ISM non-manufacturing PMI also in spotlight

Trade data out of the US and Canada will be closely watched in the coming session, while US PMI figures and the global dairy price index will be also in focus.

At 1330GMT, US trade data are likely to show a wider trade deficit in October, with the amount climbing by $4 billion m/m to $47.50 – a six-month high – whereas in Canada, the trade deficit will likely narrow by C$0.48bn to C$2.70bn in the aforementioned period, reaching the lowest level in five months.

Later in the day, US non-manufacturing PMI readings published by the Institute of Supply Management are expected to pull back to 59.0 in November after touching a more than a two-year high of 60.1 in October.

In energy markets, investors will look forward to the API weekly report due at 2130GMT which tracks the level of the US crude, gasoline and distillates stocks as concerns over rising US output linger in the market.

In other commodities, global milk auctions will be also eyed probably, bringing some volatility to the kiwi as New Zealand is a major dairy exporter. However, the release is tentative.

In the political front, the UK Prime Minister, Theresa May will meet with cabinet members later today before she begins talks with the DUP on Wednesday in order to persuade Ireland to drop its veto on the Irish border issue which is crucial for Brexit negotiations to move to the second stage of trade talks.