Sample Category Title

Market Update – European Session: EU And UK Officials Still Remain Optimistic On Achieving Agreement On Brexit To Move...

Notes/Observations

Brexit conundrum as Ireland might not agree to a proposed border deal with UK (**Note: nine days until the EU Leader summit begins)

Major European Services PMI mixed (Beats: France, Italy; Misses: Germany, Spain; In-line: Euro Zone)

Asia:

RBA left its Cash Target Rate unchanged at 1.50% (as expected) for its 16th straight pause in the current easing cycle. RBA removed references to "higher exchange rate damping inflation" and "inflation likely to remain low over time"

China Nov Caixin PMI Services: 51.9 v 51.2 prior

Bank of Japan (BOJ) Gov Kuroda: Appropriate to patiently continue bold monetary easing under current framework, still far from 2% inflation target. No discussions about second term as Gov

RBNZ Gov Spencer (acting Gov): Persistently low inflation has prompted central bank to think about whether it needs to ‘tweak' its approach to monetary policy

Europe:

Portugal Fin Min Mario Centeno won the Eurogroup chairmanship race; term starts in Jan

EU's Juncker: it was not possible to make a complete Brexit deal on Monday but did make considerable progress; would need further talks to reach a complete deal

Ireland PM Varadkar noted that talks had made substantial progress and hope to reach an agreement in coming days. Most difficult issue was agreement of no hard border. Should listen to the DUP but have to listen to other Northern Ireland constituencies as well; should not forget that a majority in Northern Ireland voted against Brexit. Happy to give May more time; there was plenty of time before the Dec 14 EU leaders summit

Economic Data:

(IN) India Nov Services PMI: 48.5 v 51.7 prior (1st contraction in 5 months); PMI Composite: 50.3 v 51.3 prior

(IE) Ireland Nov Services PMI: 56.0 v 57.5 prior (63rd month of expansion), Composite PMI: 57.7 v 56.0 prior

(RU) Russia Nov Services PMI: 57.4 v 53.5e (22nd month of expansion), Composite PMI: 56.3 v 53.2 prior

(RO) Romania Q3 Preliminary GDP (2nd reading) Q/Q: 2.6% v 2.6% advance; Y/Y: 8.8% v 8.8% advance

(ZA) South Africa Nov PMI (whole economy): 48.8 v 49.6 prior

(SE) Sweden Nov Services PMI: 61.8 v 61.4 prior

(TW) Taiwan Nov CPI Y/Y:+0.4% v -0.1%e v -0.3% prior, CPI Core Y/Y: 1.3% v 1.1%e v 1.1% prior, WPI Y/Y: 1.6% v 1.3%e

(HU) Hungary Q3 Final GDP Q/Q: 0.9% v 0.8% prelim; Y/Y: 3.9% v 3.6%e

(ES) Spain Nov Services PMI: 54.4 v 55.0e (49th month of expansion), Composite PMI: 55.2 v 55.1 prior

(IT) Italy Nov Services PMI: 54.7 v 53.2e (18th month of expansion), Composite PMI: 56.0 v 55.0e

(FR) France Nov Final Services PMI: 60.4 v 60.2e (confirms 17th month of expansion), Composite PMI: 60.3 v 60.1e

(DE) Germany Nov Final Services PMI: 54.3 v 54.9e (confirms 53rd month of expansion), Composite PMI: 57.3 v 57.6e

(EU) Euro Zone Nov Final Services PMI: 56.2 v 56.2e (confirms 53rd month of expansion, Composite PMI: 57.5 v 57.5e

(NO) Norway Nov Region Survey: Output Past 3 months: 1.22 v 1.23 prior; Output next 6 months: 1.19 v 1.11 prior

(UK) Nov Services PMI: 53.8 v 55.0e (16th month of expansion), Composite PMI: 54.9 v 55.8e

(ZA) South Africa Q3 GDP Annualized Q/Q: 2.0% v 1.7%e v 2.5% prior; Y/Y: 0.8% v 0.8%e

(EU) Euro Zone Oct Retail Sales M/M: -1.1% v -0.7%e; Y/Y: 0.4% v 1.6%e

Fixed Income Issuance:

(ZA) South Africa sold total ZAR3.3B vs. ZAR3.3B indicated in 2-35, 2040, 2044 and 2048 bonds

(ES) Spain Debt Agency (Tesoro) sold total €4.61B vs. €4.0-5.0B indicated in 6-month and 12-month Bills

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.2% at 386.8, FTSE +0.2% at 7355, DAX -0.1% at 13043, CAC-40 -0.3% at 5375, IBEX-35 -0.3% at 10177, FTSE MIB -0.1% at 22343, SMI -0.1% at 9323, S&P 500 Futures +0.1%]

Market Focal Points/Key Themes: European Indices trade this morning, after strong gains yesterday. The FTSE outperforms as Cable drops on continued stumbling blocks on Brexit negotiations. On the M&A front Cineworld trades lower after confirming to acquire Regal and the subsequent launch of a £1.7B right offering. On the earnings front NeoPost falls sharply after a fall in Rev, while IG Index trades over 5% higher following a positive trading update, whilst Dialog Semicoductor rebounds after a sharp drop yesterday following a business update. Provident Financial trades over 10% lower after the FCA informs of an investigation into Moneybarn. Looking ahead, notable earners include Autozone, HD Supply and GIII apparel.

Equities

Consumer discretionary [Cineworld [CINE.UK] -4.2% (Confirm to acquire Regal, to launch rights issue), - Ferguson [FERG.UK] +0.4% (Q1 results), Neopost [NEO.FR] -11% (Earnings)]

Financials: [ IG Group [IGG.UK] +5.4% (Trading update), Provident Financial [PFG.UK] -13% (FCA to investigate MoneyBarn)]

Technology: [Dialog Semi [DLG.DE] +5% (Rebound following business update)]

Healthcare: [Gensight [SIGHT.FR] +1.2% (Postiive 1/II trial data)]

Speakers

BOE Financial Policy Committee (FPC) Nov 27th Minutes: Agreed to raise the UK countercyclical capital buffer (CCyB) rate from 0.5% to 1.0%, with binding effect from Nov 28th 2018. Did considered raising banks' capital requirements last week by more than it had previously signaled to tackle risks to the financial system including those from Brexit. Would reconsider adequacy of the 1.0% CCYB during H1 2018

Chancellor of Exchequer Hammond (Fin Min) stated that was very confident of moving the Brexit deal forward

Scotland First Min Sturgeon: Could be the moment for opposition to force a different approach and push to keep the whole UK in the single market and customs union

Italy Stats Agency (ISTAT) Monthly Economic Note: Growth is strengthening in the short term

Norway Central Bank (Norges): Employment growth seen remaining moderate

Czech Central Bank Gov Rusnok reiterated view that would gradually raise interest rates

Czech Central Bank Vice Gov Hampl: Cannot exclude raising the countercyclical buffer Various Finance Ministers comment ahead of EcoFin meeting

EU's Moscovici: There was no tax haven in the EU. Black list of tax havens to include approx 20 States. Must keep pressures on tax havens

EU's Dombrovskis: US tax reform will be discussed at today's meeting

Germany Fin Min Altmaier: Tax blacklist was an important 1st step

Currencies

GBP/USD maintained a heavy tone following Monday's disappointment that no breakthrough was made on the Brexit negotiations. The current conundrum as Ireland might not agree to a proposed border deal with UK. There are only nine days until the EU Leader summit begins (Dec 14th) and the UK needs to show by then that sufficient progress has been made to move on to trade negotiations. GBP/USD at 1.3425 just ahead of the NY morning and some 40 pips off its worst levels

Fixed Income

Bund futures trade 163.11 up 14 ticks, trading in a narrow range. Continued downward pressure sees 162.10 followed by 161.50. A reversal targets 163.40 then 163.75.

Gilt futures trade at 125.11 up 22 ticks, as the pound extends losses on Brexit fears. Continued upside eyeing 125.15 then 125.65. Downside targets include 124.01 then 123.75.

Tuesday's liquidity report showed Monday's excess liquidity rose to a record high of €1.915T from €1.912T. Use of the marginal lending facility rose to €394M from €243M prior.

Corporate issuance saw no deals price in high-grade primary

Looking Ahead

05.30 (UK) Weekly John Lewis LFL sales data

05:30 (EU) ECB allotment in 7-day Main Financing Tender (MRO) tender

05:30 (HU) Hungary Debt Agency (AKK) to sell in 3-month Bills

05:30 (UK) DMO to sell £2.75B in 0.75% July 2023 Gilts

05:30 (BE) Belgium Debt Agency (BDA) to sell €1.2B in 3-month and 6-month bills

06:00 (IE) Ireland Nov Unemployment Rate: no est v 6.0% prior

06:00 (IE) Ireland Oct Industrial Production M/M: No est v 0.7% prior; Y/Y: No est v -3.2% prior

06:00 (BR) Brazil Oct Industrial Production M/M: 0.1%e v 0.2% prior; Y/Y: 5.2%e v 2.6% prior

06:00 (PL) Poland Central Bank (NBP) Interest Rate Decision: Expected to leave Base Rate unchanged at 1.50%

06:30 (CL) Chile Oct Economic Activity Index (Monthly GDP) M/M: -0.1%e v -0.1% prior; Y/Y: 2.9%e v 1.3% prior, Economic Activity (ex-mining) Y/Y: No est v 0.7% prior

06:30 (TR) Turkey Nov Effective Exchange Rate (REER): No est v 87.96 prior

06:30 (EU) ESM to sell €1.5B in 3-month Bills; Avg Yield: % v 0.6730% prior; Bid-to-cover: x v 4.8x prior (Nov 7th 2017)

07:00 (BR) Brazil Nov Services PMI: No est v 48.8 prior, PMI Composite: No est v 49.5 prior

07:00 (RU) Russia announces weekly OFZ bond auction .

07:45 (US) Weekly Goldman Economist Chain Store Sales

08:00 (NZ) Fonterra Global Dairy Trade Auction

08:05 (UK) Baltic Dry Bulk Index

08:30 (US) Oct Trade Balance: -$47.5Be v -$43.5B prior

08:30 (CA) Canada Oct Int'l Merchandise Trade (CAD): -2.7Be v -3.2B prior

08:30 (SK) Slovenia Debt Agency (Ardal) to sell 12-month Bills - 08:55 (US) Weekly Redbook Sales

09:00 (EU) Weekly ECB Forex Reserves

09:00 (MX) Mexico Sept Gross Fixed Investment: No est v 0.3% prior

09:00 (SE) Sweden Central Bank (Riksbank) Gov Ingves

09:45 (US) Nov Final Markit Services PMI: 55.2e v 54.7 prelim, Composite PMI: No est v 54.6 prelim

10:00 (US) Nov ISM Non-Manufacturing Composite: 59.0e v 60.1 prior

10:00 Poland Central Bank Gov Glapinski to hold post rate decision press conference

11:30 (US) Treasury to sell 4-Week and 52-Week Bills

15:00 (MX) Mexico Citibanamex Survey of Economists

16:00 (AU) Australia ANZ Roy Morgan Weekly Consumer Confidence Index

16:30 (US) Weekly API Oil Inventories

19:00 (CO) Colombia Nov CPI M/M: 0.1%e v 0.0% prior; Y/Y: 4.1%e v 4.1% prior

Euro Ticks Lower As German Services PMI Misses Expectations

The euro has posted small losses in the Tuesday session. Currently, EUR/USD is trading at 1.1854, down 0.09% on the day. On the release front, German Final Services PMI edged lower to 54.3, short of the forecast of 54.9 points. Eurozone Final Services improved to 56.2, matching the forecast.

The good news is that the Brexit talks have gained some momentum, but a breakthrough on the non-trade issues has not been reached. There were hopes that a breakthrough would be announced on Monday, following talks between Prime Minister May and European Commission President Jean-Claude Juckner, but the gaps on two issues remain, for now. One thorny issue is that of northern Ireland and its border. The UK will clearly not remain in a customs union with the EU, but Ireland is insistent that there not be a hard border with the North, while the DUP, which is propping up the May government, is strongly against any border between the UK mainland and Northern Ireland. The second issue is whether the European Court of Justice will have a role protecting European citizens in the UK. The EU is in favor of a role for the court, while many British lawmakers feel that such a move would impinge on British sovereignty. The EU holds a meeting on December 12, and May is anxious to wrap up the non-trade sticking points and move on to trade talks by that date.

The US Senate passed a tax reform bill on the weekend, but the vote was a squeaker, 51-49, as the vote went along party lines, with one Republican voting against the bill. Now that that the House and the Senate have passed tax bills, a conference committee will try and hammer out a uniform bill which can be sent to President Trump and signed into law. There are some differences in the two bills, notably individual tax rates, the alternative minimum tax, mortgage interest deductions and the estate tax. The Senate and House will have to work out their differences quickly, as the new “merged” bill will have to pass through in both houses. If the bill does become law, it will mark the first major tax reform in the US in 30 years, and could boost the US dollar against the euro and other major currencies.

Technical Outlook: WTI OIL – Risk Of Deeper Pullback On Loss Of 20SMA Support

WTI oil price remains in red for the second day and pressure support at $57.10 (20SMA) which guards pivot at $56.75 (29 Nov higher low).

Break here would signal increased risk of deeper pullback as loss of $56.75 handle would complete daily failure swing pattern and open way for extended correction from $59.02 (24 Nov peak).

Extended correction could travel to $56.41 and $55.80 (Fibo 61.8% and 76.4% of $54.80/$59.02 upleg respectively) with extended bearish acceleration to unmask key near-term support at $54.80 (14 Nov trough).

Early downside rejection (ideally above 20SMA) would signal an end of corrective phase and shift near-term focus higher as overall structure remains bullish.

Release of API US crude stocks data, due later today, is in focus.

Res: 57.62, 57.88, 58.31, 58.86

Sup: 57.10, 56.75, 56.41, 55.80

Technical Outlook: AUDUSD Generated Bullish Signal On Post-RBA Rally

Recovery is gaining pace as the pair accelerated higher on Tuesday after RBA left interest rates unchanged at 1.5% as expected. The following statement showed no changes from the previous monetary policy meeting and indicating that the central bank would remain neutral and on hold for some time.

AUDUSD accelerated to fresh three-week high at 0.7653 after release. This marks pivotal resistance (Fibo 61.8% of 0.7729/0.7530 downleg) and sustained break here would trigger fresh extension higher and expose key barriers at 0.7691/0.7729 (200SMA / 02 Nov high).

Fresh bullish acceleration which eventually took out important barrier at 0.7607 (20SMA), turned techs on lower timeframes into full bullish setup while daily studies improved and regained bullish momentum.

Broken 30SMA (0.7634) now acts as initial support with extended downticks expected to hold above broken 20SMA.

Res: 0.7653, 0.7691, 0.7729, 0.7776

Sup: 0.7634, 0.7607, 0.7594, 0.7579

Technical Outlook: USDJPY – Rising Downside Risk On Repeated Rejection At Cloud Top

The pair ticked higher on Tuesday, leaving temporary footstep at 112.36 (Mon/Tue lows) intact but remaining below initial barrier at 112.78 (daily Kijun-sen).

Monday's close in red and repeated rejection at daily cloud top, as well as repeated failure to close above Kijun-sen, was bearish signal.

Risk of deeper pullback on loss of 112.36 handle and extension below 111.96 (daily Tenkan-sen) remains in play and scenario would include extension towards layers of strong supports, provided by converged 10SMA (111.80), 200SMA (111.68) and 100SMA (111.57).

Alternative scenario requires sustained break above cloud top (113.12) to signal continuation of recovery from 110.83 (27 Nov low).

Res: 112.78, 113.12, 113.24, 113.81

Sup: 112.36, 111.96, 111.80, 111.68

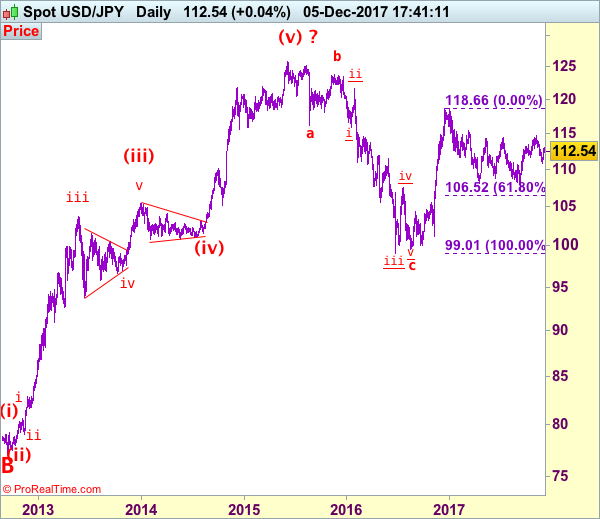

USD/JPY Elliott Wave Analysis

USD/JPY - 112.50

USD/JPY – Wave V of larger degree circle V has possibly ended at 75.31 and major correction has commenced and already met indicated target at 125.00.

Dollar found renewed buying interest at 111.41 on Friday and has staged a strong rebound, dampening our bearishness and suggesting low has been formed at 110.84 last week, hence consolidation with upside bias is seen for gain to 113.10-15, then 113.30-35, however, a daily close above resistance at 113.91 is needed to signal the pullback from 114.74 has ended, bring further rise to 114.30-35, then retest of said recent high which is likely to hold from here.

Our preferred count is that, triangle wave IV (with circle) ended at 101.45 and the circle wave V brought dollar down to the record low of 75.31 in 2011 and the subsequent rebound signal major correction has commenced with A leg ended at 84.19, followed by wave B at 77.14 and impulsive wave C is now unfolding (indicated upside target at 125.00 had been met) for gain towards 127.00 level. In the event dollar drops below support at 99.01, this would confirm medium term decline from 125.86 top (2015 high) has resumed for subsequent weakness to 98.00 and possibly 97.00.

Under this count, this wave C is unfolding as impulsive waves with (1) (2), 1 2 ended at 80.67, 79.07, 82.84 and 81.69 respectively, hence the extended wave 3 has ended at 103.74 and wave 4 correction of recent upmove should bring weakness to 92.57, then towards 90.88 but psychological support at 90.00 should limit downside and bring another rally later in wave 5, indicated target at 125.00 had been met and gain to 127.00 cannot be ruled out but reckon price would falter below 130.00.

On the downside, whilst initial pullback to 112.00 cannot be ruled out, reckon said Friday’s low at 111.41 would remain intact and bring another rebound later. A drop below this support would suggest the rebound from 110.84 has ended, then retest of this support would follow, a drop below this level would revive bearishness and extend the fall from 114.74 top to 110.50, then 110.00, however, near term oversold condition should prevent sharp fall below support at 109.55 and reckon 109.00 would hold from here, risk from there is seen for another rebound to take place later.

Recommendation: Exit short entered at 112.50 and stand aside for this week.

On the monthly chart, we have changed our preferred count that an impulsive wave is unfolding with major wave III with circle ended at 79.75, then followed by wave IV with circle and is labeled as a triangle with A: 147.64 (11 August, 1998), B: 101.25, C: 135.20, D: 101.67 and E leg ended at 124.14 to end the wave IV with circle. Hence, wave V with circle commenced from there and hit a record low of 75.31, however, the subsequent strong rebound signals this circle wave V has possibly ended there, hence gain to (indicated upside target at 122.00 and 125.00 had been met), the retreat from 125.86 suggests wave A of major correction has ended there and wave B correction back to 99.00, then 95.00 would be seen, however, reckon downside would be limited to 90.00, bring another rebound in wave C next year.

XAU/USD Analysis: Moves Horizontally Near 1,276

As it was anticipated, yesterday’s trading session the exchange rate spent in a flat movement between support and resistance zones located at the 1,270 and 1,275 marks. As long as there are no substantial news coming from the United States, the pair is not expected to jump above the 1,280.42 level that represents location of the monthly PP and the 100-hour SMA. The similar assumption holds for the 1,270.00 mark that is crossed by the bottom boundary of a dominant ascending channel. In larger perspective it is still unclear whether the above dominant pattern will sustain or it will be broken amid the pressure from a medium-term descending channel. Most probably until the market sentiment turns bearish the rate will manage to keep gradual advance.

USD/JPY Analysis: Meets Strong Resistance At 113.00

As it was suggested yesterday, the currency exchange rate made a fully-fledged breakout from a rising wedge formation after encountering resistance posed by the 50% Fibonacci retracement level at 113.00. However, the plunge was not deep, as southern side was secured by two moving averages and another 50% retracement level located at 112.45. As long as there are no disappointing political news coming from the United States, the rate is projected to keep climbing back to the 113.00 mark. But before that it might be temporarily stopped by the monthly PP at 112.70. Nevertheless, the rising 55- and 100-hour SMA are expected to continue stimulating the upwards movement and simultaneously secure the bottom boundary of a currency active junior ascending channel.

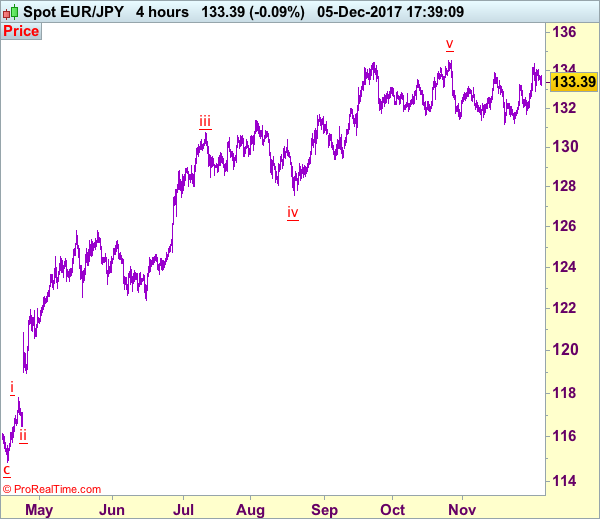

Trade Idea: EUR/JPY – Stand aside

EUR/JPY - 133.35

New strategy :

Stand aside

Position: -

Target: -

Stop:-

Despite staging a rebound from 132.91 to 134.05 (yesterday’s high), lack of follow through buying and the subsequent retreat suggest further choppy trading would be seen and weakness towards said support at 132.91 cannot be ruled out, however, break there is needed to signal a temporary top has been formed at 134.38, bring retracement of recent rise to 132.65 and later towards 132.00-10 but support at 131.72 should remain intact.

On the upside, expect recovery to be limited to 133.75 and said resistance at 134.05 should remain intact, bring further choppy trading. Only a daily close above yesterday’s high at 134.05 would revive bullishness and signal the retreat from 134.38 (last week’s high) has ended, bring retest of this level later, above there would bring test of strong resistance at 134.50 but only break there would retain bullishness and extend gain to 135.00-10 first.

Our latest preferred count is that wave (ii) is ABC-X-ABC which ended at 123.33 and wave (iii) is unfolding with wave iii ended at 100.77, followed by wave iv at 111.57 and wave v as well as the wave (iii) has ended at 97.04, followed by wave (iv) at 111.43 and wave (v) has ended at 94.12 which is also the end of the larger degree v, this also implied the major wave (C) has also ended there, hence major correction has commenced from there with (A) leg unfolding in its lower degree wave c which has possibly ended at 145.69. Under this count, A-B-C wave (B) has commenced with A leg ended at 136.23, wave B at 143.79 and wave C has possibly ended at 149.79.

Our larger degree count is that the decline from 139.26 is wave (C) and is sub-divided into a diagonal triangle i-ii-iii-iv-v with wave i - 105.44, wave ii- 123.33, wave iii - 97.03, wave iv - 111.43, followed by the final wave v as well as the end of wave (C) at 94.12, this also mark the bottom of larger degree wave B. Under this count, major rise in wave C has commenced as an impulsive wave with minor wave III ended at 145.69, wave V is still in progress for further gain to 150.00. Having said that, this so-called wave V could well be the first leg of larger degree 5-waver wave C and this wave C should bring at least a retest of wave A top at 169.97 (July 2008).

GBP/USD Analysis: Jumps Up And Down From Political News

In general, previous trading session the currency rate spent moving downwards, as expected. Apart from rebound from the two month maximum at 1.3550, the drop was driven by anxiety over affirming vote on tax bill as well as new report that no agreement on Brexit has been reached yet. From technical point of view, today the pair is squeezed between the 50% Fibonacci retracement level, the 55- and 100-hour SMAs from the top and the weekly PP plus the 200-hour SMAs from the bottom. These boundaries point out of further correction of the cable. Theoretically, one of the scheduled data releases for today might stimulate the rate to make a breakout. However, this scenario seems unlikely, as markets are mainly focused on political news