Sample Category Title

GBPUSD Intraday Bearish Below 1.3450 Level

The British pound has moved lower against the U.S dollar, hitting 1.3418, before recovering, as the UK failed to reach a Brexit deal with the EU on Monday. British Prime Minister has until December 15th to finalize a deal with the European Union, and now needs to work with the Northern Irish coalition party leader, to find a solution to border issues. GBPUSD price-action currently holds above the 1.3450 level, although bearish pressure is mounting on sterling. Traders now look to the release of the UK Services PMI for the month of November, for the next directional move in the pair.

The GBPUSD pair is bullish while trading above the 1.3450 technical level. Further upside towards 1.3510 and 1.3549 appears possible.

A higher time-frame close below the 1.3450 level, may lead to a sell-off towards the 1.3400 and 1.3360 support regions. Extended weekly GBPUSD support is found at the 1.3303 level.

Eurozone Data Headline Tuesday Session

A deluge of economic data will make headlines on Tuesday, with the Eurozone region set to take primacy. Action begins early and will continue for the rest of the day leading into the North American session.

IHS Markit will release several PMI reports beginning at 08:15 GMT. The research institute will report on Germany, France, Italy and the 19-member Eurozone through a series of service and composite PMIs. Markit will also report on British PMI early on Tuesday.

The European Commission's statistics agency is also scheduled to release the latest Eurozone retial sales numbers at 10:00 GMT. Receipts at retail stores are expected to fall 0.7% in October.

In North America, Markit and ISM will each release their own versions of US services PMI. The ISM report is more closely followed by the financial markets.

Earlier in the session, Caixin China reported stronger than expected services sector growth for the world's second-largest economy. The Caixin services purchasing managers' index (PMI) rose to 51.9 in November from 51.2 the previous month.

According to the official release:

'The Caixin PMI readings in November showed the economy has maintained stability and there was no imminent risk of a significant decline in its growth rate. But we should be cautious because the economy may come under rising inflationary pressure at the start of next year due to continued price increases.”

Meanwhile, the Reserve Bank of Australia (RBA) held its trend-setting interest rate at a record low of 1.5%, where it has stood since mid-2016.

The RBA has remained on the sidelines in support of economic growth and inflation. There is currently no timeline as to when policymakers will vote for higher interest rates.

AUD/USD

The Australian dollar rose after the RBA decision, with the AUD/USD exchange rate climbing 0.4% to 0.7643. The upside move came even as the near-term momentum indicators appeared mixed at the start of Tuesday trading. The pair faces immediate support at the 0.7587 level, which also corresponds with the 21 SMA. On the opposite side of the ledger, AUD/USD has breached the 0.7627 and 0.7640 resistances. The next resistance test is likely to come at 0.7675.

EUR/USD

Europe's common currency slipped at the start of Tuesday trading, with the EUR/USD falling further below the 1.1900 handle. The pair was last seen trading at 1.1874, and faces immediate resistance around 1.1930. A deluge of economic data later in the week could dictate where this pair ends up in the short run.

GBP/USD

Cable was little changed on Tuesday, as investors awaited fresh trading catalysts later in the day. The GBP/USD exchange rate was last seen holding steady around 1.3472 after slipping from two-month tops above 1.3500. That level continues to offer strong psychological resistance. On the support side, cable is likely to find demand around 1.3430.

Senate’s Tax Bill Vote Fails To Impress Dollar Bulls

Despite U.S. equities closing at new records on the tax breakthrough, it was interesting to see the dollar retreating slightly against its major counterparts. It seems investors are still anxious about how the Senate will reconcile its tax bill with the House of Representatives before it goes to President Trump to sign it into law. There's no doubt the differences between both Houses are vast. However, it's in the best interest of the Republicans to get the deal done, or they risk losing the majority in November's 2018 election,and this is why it looks like just a matter of time before the final bill reaches Trump for his final blessings. This scenario will probably continue to provide the greenback support for the remainder of 2017, with pullbacks seen as an opportunity for bulls. However, the longer-term outlook may not be as bright, especially that long-term bond yields are not reflecting stocks markets' optimism. U.S. 10-year bond yields are trading below 2.4% early Tuesday, and the yield curve continues to flatten.

Friday's non-farm payrolls report is the key macro risk event on the U.S. calendar, and if no material development seen on the political side, investors aren't likely to make huge bets. Nonfarm payrolls are expected to have increased by 198,000 in November, after climbing by 261,000 in October, but it's the wages figure that will determine the dollar's direction. A reading of 0.4% or above, will support the central bank's argument that low inflation should be attributed to temporary factors, and this should lead to steepening the yield curve.

Sterling made most of the headlines yesterday. After moving higher on reports of growing confidence that the first phase of negotiations is drawing closer to a successful conclusion, GBPUSD fell sharply as Theresa May and Jean-Claude Juncker failed to reach an agreement, with Irish border being the main obstacle. The next 10-days are very critical for the Pound, as the decision to proceed to phase two of talks, will be made at the EU summit, on 14 & 15 December. Pound traders are likely to ignore fundamentals for the next couple of days and react on how the story over the Irish border develops from its currentstage.

Forex: Moderate Gains For USD

On Monday, the US Commerce Department released Factory Orders data for October, indicating that the continued strength in the Manufacturing sector will help support the growing US economy. With the markets forecasting a drop of 0.4% in October, Factory Goods Orders only dipped 0.1% in the midst of a fall in demand for both civilian and defense aircraft after an upwardly revised 1.7% jump in September. The modest decrease in Factory Orders came as orders for durable goods fell by 0.8 %, more than offsetting a 0.7% increase in orders for non-durable goods.

Eurozone Producer Price data from Eurostat on Monday showed a faster than expected easing in October. Producer prices climbed 2.5% annualized in October, slower than September’s 2.8% rise, which was revised down from 2.9%. The markets had forecast PPI to drop to 2.6%. PPI excluding energy increased slightly to 2.3% from the previous 2.2%. Industrial producer prices rose in all EU member states, with the largest increases recorded in Belgium, Bulgaria, Poland, Hungary and Ireland.

GBP gave back some of its recent gains on reports that the discussions between Prime Minister May and EU Commission President Juncker had ended on Monday without a formal agreement. The Prime Minister is under pressure to get an agreement on EU divorce issues before European leaders meet on December 14th to decide whether to give formal approval to start talks on post-Brexit trade. The stumbling blocks appear to center around the Irish border and the role of the European Court of Justice in overseeing EU citizens’ rights in the UK after Brexit. Talks are believed to resume on Wednesday in Brussels.

USD has held onto recent gains following the passing of the US Tax Reform Bill in the Senate over the weekend. Both the Senate and the House of Representatives now need to reconcile each of their versions of the Bill – a process that is likely to face some challenges. This is standard practice and there is no reason to suggest that it will not be successful. There is every possibility that this Bill will be made law by the end of this year.

In an unsurprising move, the Reserve Bank of Australia (RBA) has left the cash rate on hold again today at 1.5%. This marks the fifteenth meeting in a row the RBA has held rates steady, with the last rate movement taking place in August 2016 with a 25-basis point rate cut. Being the last rate update for this year, the RBA board will next meet on 6 February 2018.

EURUSD is unchanged overnight, currently trading around 1.1873.

USDJPY is marginally higher in early Tuesday trading at around 112.55.

GBPUSD is unchanged in early session trading at around 1.3470.

AUDUSD is 0.7% higher, following the RBA decision to leave interest rates unchanged, currently trading around 0.7652.

Gold is slightly lower overnight, currently trading around $1,274.75.

WTI is 0.2% higher, currently trading around $57.55.

Major data releases for today:

At 08:55 GMT: Markit Economics will release German PMI and Composite PMI for November. Both PMI and Composite PMI are forecast unchanged at 54.9 and 57.6 respectively. Any significant deviation from forecast will likely see EUR volatility.

At 09:00 GMT: Markit Economics will release Eurozone Composite & Services PMI for November. Both data releases are forecast to be unchanged at 57.5 and 56.2 respectively. Any significant deviation from forecast will likely see EUR volatility.

At 13:30 GMT: the US Bureau of Economic Analysis and the U.S. Census Bureau will release the US Trade Balance for October. Forecasts are calling for an increase from the previous reading of -$43.5B to -$43.8B.

At 14:45 GMT: Markit Economics will release US Services & Composite PMI for November. Services PMI were previously 54.7 and Composite PMI was 54.6.

At 15:00 GMT: The Institute for Supply Management (ISM) will release US Non-Manufacturing PMI for November. Forecasts are calling for a lower release of 59.3 compared to the previous reading of 60.1. Any significant deviation from the forecast is likely to cause USD volatility.

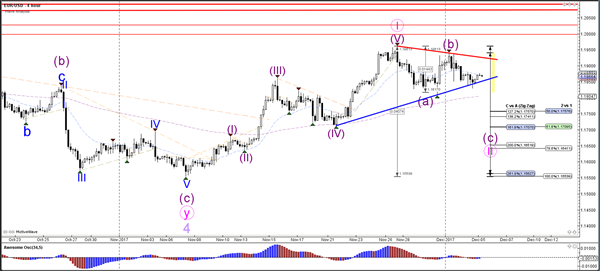

GBPUSD In Bullish Phase But Rally Pauses On Overbought Conditions

GBPUSD is in a bullish phase in the near term and is poised to re-test the September peak at 1.3656. In the medium term, the pair is neutral and appears to be trapped between the key levels of 1.3000 and 1.3600.

Last week's high of 1.3549 remains a strong resistance level. Near-term upside momentum has weakened after RSI reached overbought levels at 70. The overbought conditions in the market could lead to a consolidation phase at current levels.

Any downside is expected to be contained in the support zone near 1.3300 and the 38.2% Fibonacci retracement level (1.3447) of the upleg from 1.2773 to 1.3656. A further retreat would target the 50-day moving average (1.3240) and 50% Fibonacci (1.3215). The market needs to remain above this area to keep the short-term bullish bias in place.

The overall outlook remains positive based on bullish technicals and only a move back below 1.3000 would erase the latest bullish move.

Can British Pound Break 1.3600 Vs US Dollar?

Key Highlights

- The British Pound is moving higher and is currently trading above the 1.3420 support against the US Dollar.

- There is a crucial bullish trend line forming with support at 1.3430 on the 4-hours chart of GBP/USD.

- The US Factory Orders declined by 0.1% in Oct 2017, less than the forecast of -0.4%.

- Today, the UK Services PMI for Nov 2017 will be released, which is forecasted to decline from 55.6 to 55.0.

GBPUSD Technical Analysis

The British Pound is gaining bullish momentum above 1.3450 against the US Dollar. The GBP/USD pair might soon break 1.3550 for a move towards 1.3600 in the near term.

After a downside spike, the pair found support at 1.3220 and started an upside move. It traded higher and broke the 1.3400 and 1.3500 resistance levels. A high was formed at 1.3549 from where the pair corrected lower.

It tested the 38.2% Fib retracement level of the last wave from the 1.3220 low to 1.3549 high. On the downside, there is a crucial bullish trend line forming with support at 1.3430 on the 4-hours chart.

The trend line and support area near 1.3420 are important. As long as the pair stays above 1.3420, it could continue higher towards 1.3600 and it might even break it for further gains.

US Factory Orders

Recently in the US, the Factory Orders report for Oct 2017 was released by the US Census Bureau. The market was looking for a decline of around 0.4% in orders compared with the previous month.

The actual result was better as the decline in orders was only 0.1% in Oct 2017. However, the outcome was disappointing when compared with the last increase of 1.7% (revised up from +1.4%).

The GBP/USD pair was neutral after the release, but remained elevated above the 1.3420 support.

Economic Releases to Watch Today

Germany's Services PMI for Nov 2017 – Forecast 54.9, versus 54.9 previous.

France Services PMI Nov 2017 – Forecast 60.2, versus 60.2 previous.

Spanish Services PMI for Nov 2017 – Forecast 55.2, versus 54.6 previous.

Euro Zone Services PMI for Nov 2017 – Forecast 56.2, versus 56.2 previous.

UK Services PMI for Nov 2017 – Forecast 55.0, versus 55.6 previous.

US Services PMI for Nov 2017 – Forecast 55.4, versus 54.7 previous.

Europe Lower Ahead Of PMIs And As Brexit Talks Stall Again

- AUD Lifted By Retail Sales Data and RBA Statement;

- China Gets PMI Releases Off to a Positive Start;

- Irish Border Issues Preventing Progress in Brexit Negotiations;

- Tax Reform Remains Key For US Investors.

European equity markets are expected to open a little lower on Tuesday following a softer session in Asia, which came as US equity markets took a negative turn after posting fresh record highs at the open.

AUD Lifted By Retail Sales Data and RBA Statement

There was plenty of movement in the Australian dollar overnight as stronger retail sales data for October followed by a slightly more hawkish tone from the Reserve Bank of Australia lifted the currency around 0.7% against the greenback. The growth in consumer spending is the highest we’ve seen since May and comfortably exceeded expectations, while the September reading was also revised higher.

While the data was largely responsible for the Aussie move overnight, the RBAs reference to a tighter labour market did appear to push the currency a little further. That said, while we are seeing progress, the probability of a rate hike any time soon appears slim and the post announcement move was probably largely aided by the momentum gathered in the aftermath of the retail sales release. The RBA left rates unchanged at today’s meeting.

China Gets PMI Releases Off to a Positive Start

The Caixin services PMI rose more than expected overnight, which follows a similar bounce in the official reading last week. As has been expected, we are seeing a dip in the surveys in the latter part of the year and yet they are showing some resilience despite the fact that stimulus efforts have been reined in. Improvements in the global economic environment will be going some way to filling this gap and should continue to aid the transition in China for the foreseeable future.

There’s plenty more services PMI surveys being released across Europe this morning, although many of these will be revised readings and may therefore have little impact. The UK reading is expected to ease off a little from October but remain elevated at 55.

Irish Border Issues Preventing Progress in Brexit Negotiations

This comes as negotiations between the UK and the EU appear to finally be making some progress. The two sides still have a little further to go before they can proceed onto the next stage and discuss future trade but there appears to be a more optimistic feeling that this can be achieved before the deadline in just over a week. The pound has already rallied in anticipation of a deal on the financial settlement and citizens’ rights although as ever complications, this time around the Irish border, are preventing these being wrapped up just yet.

Tax Reform Remains Key For US Investors

The passage of tax reform through Congress will likely be the key focus for US investors between now and year-end, with a rate hike this month almost entirely priced in. While these discussions take place though there is plenty of data to keep an eye on including of course this Friday’s jobs report. Today it’s the ISM non-manufacturing PMI that will steal the focus, as well as the services PMI reading, both for November.

Oil Prices Dropped

Market movers today

The talks about a US tax deal continue to be the main topic in markets. Also, the market will monitor comments on Brexit negotiations after the talk yesterday between the UK's Theresa May and the EU's Jean-Claude Juncker did not result in a deal.

There is no tier-1 data today on the global front but a number of tier-2 data is due to be released: PMI services are released for the euro area and the UK and US will release the ISM non-manufacturing index. The latter is the most interesting as it reached the highest level in more than a decade in the past two months. Although growth is robust in the US, it seems a bit overdone and we could be in for a small decline for November.

Euro retail sales are set to show a decline in October (consensus is -0.7% m/m) after a big increase in September. Overall, the euro consumer is in good shape as signalled by record high consumer confidence.

In Sweden, it is time for industrial orders/production. Also, the Swedish Financial Stability Council will host a press conference at 13:30 CET and the Riksbank Governor Stefan Ingves will give a speech on the risk of a new banking crisis (15:00). In Norway, the Norwegian Regional Network Report and house prices will give more input on the state of the Norwegian economy. (for more on Scandies, see page 2).

Selected market news

China's Caixin service PMI showed a large increase to 51.9 in November from 51.2 in October, which brought the composite PMI to 51.6 from 51.0. The higher activity in the service thus mitigated the slightly slower activity in the manufacturing sector reported last week. In Japan, the service PMI dropped to 51.2 from 53.4 sending the composite PMI down to 52.2 from 53.4.

Brexit negotiations between the UK's Theresa May and EU's Jean-Claude Juncker yesterday did not end with a deal. However, negotiations will continue this week with the aim of reaching a deal before the EU summit next week and potentially already before the end of this week. EUR/GBP rose on the news as the market had priced in a chance of a breakthrough yesterday.

Oil prices dropped yesterday with the price on Brent falling to USD62/bbl. Overnight, it was reported that Saudi Arabia has conducted an airstrike on Yemen – news which is likely to have helped halt the slide in prices. It could further put geopolitical risks back in the spotlight of the oil market this week. According to a Bloomberg survey, OPEC's crude output dropped in November before the group's second bi-annual meeting. Coincidently, that brought OPEC's output down to the lowest level since May when the group first bi-annual meeting to place.

The US Supreme Court yesterday announced that US President Trump's proposed travel ban could take full effect, restricting people from six Muslim countries from entering the US.

Thomas Barkin was announced yesterday to take over as President at the Federal Reserve Bank of Richmond from Jeffrey Lacker. It means there is one seat less to be filled on the FOMC (there are still four vacant seats on the Board of Governors and no replacement has been announced for New York Fed President Dudley, who will step down next summer).

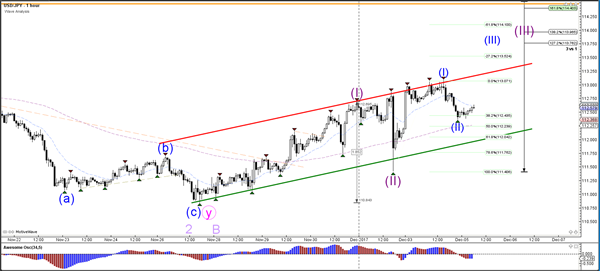

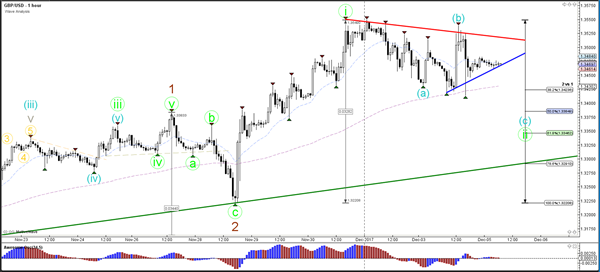

Daily Wave Analysis: USD/JPY, GBP/USD Build Sturdy Trend Channels

Currency pair USD/JPY

The USD/JPY is in an uptrend channel which could be part of a larger bullish wave 3 pattern. This is invalidated if price breaks below the support trend line (green) of the uptrend channel. A bullish breakout above the channel resistance would confirm the bullish breakout.

The USD/JPY will need to break above the resistance (red/orange) now or later to confirm the wave 3 pattern (purple). For the moment, the Fibonacci levels and the support trend line could stop price from falling.

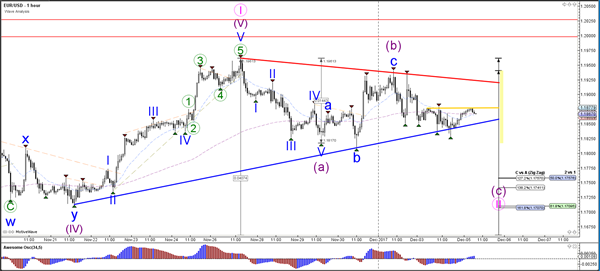

Currency pair GBP/USD

The GBP/USD is probably in a wave 1-2 (green) unless price breaks below the 100% Fibonacci level of wave 2 vs 1. The current bearish channel could also be a bear flag pattern if price manages to break above it.

The GBP/USD is also showing a triangle pattern. A break below or above the triangle could indicate a potential breakout.

Currency pair EUR/USD

The EUR/USD could be in a wave C (purple) of a larger bearish ABC retracement. An impulsive wave C could develop if price is able to break below the support trend line (blue). A bearish breakout could see price fall and challenge the Fibonacci levels of wave 2 vs 1 (pink) whereas a bullish breakout will face other layers of potential resistance.

The EUR/USD break above the resistance trend line (red) could be part of a larger wave 1 (pink), although new resistance levels are nearby (red lines). A break below the support trend line (blue) could see price fall towards the Fibonacci levels of wave C and 2.

Market Update – Asian Session: RBNZ Spencer Comments Boost Kiwi

Headlines/Economic Data

General Themes: Asian tech stocks weaker after declines seen in NY session; Taiwan Semi -2%

Markets generally pare opening losses

Japanese and South Korean steelmakers outperform; track earlier gains in US Steel

China Caixin Nov services PMI rises, in line with official data released on Nov 30th

Japan

Nikkei 225 opened -0.5%; closed -0.4%

Tech and Chip-related shares track weakness in US companies: SUMCO -3.5%, Tokyo Electron -2%, Softbank -0.9%; Olympus Corp -1.6% (priced secondary offering)

TOPIX Iron & Steel Index +1.5%; Nippon Steel said to reduce orders accepted for steel pipes by 20-30% as production cannot keep up with the increase in demand from large-scale projects ahead of the 2020 Tokyo Olympics (press)

TOPIX Securities Index +1%

Japan Nov PMI Services: 51.2 v 53.4 prior, PMI Composite: 52.2 v 53.4 prior

(JP) Bank of Japan (BOJ) Gov Kuroda: No discussions about second term as Gov - speaking after lunch with Abe; No comment on whether willing to continue as BOJ Gov (**Note: current 5-year term due to end April 2018)

Bank of Japan (BOJ) Gov Kuroda recent references to the "reversal rate" may signal a shift to a more hawkish policy bias, even though there are no expectations of a near term policy change – FT (**Note: The reversal rate is the level where rate cuts by BOJ could hurt economy)

Japan Fin Min Aso: Wants income tax changes to be revenue neutral and consider ‘work style’ changes

China and Japan officials to hold 8th round of discussions regarding maritime affairs during Dec 5-6th period - financial press

(JP) Japan's four biggest oil companies are expected to beat FY forecasts – Nikkei

(JP) Bank of Japan (BOJ) Gov Kuroda: BOJ bought ¥105T in JGBs in year through Oct

Japan MoF sells ¥2.3T v ¥2.3T indicated in 0.1% 10-yr JGBS; avg yield 0.059%; bid-to-cover 3.70x

9983.JP Reports Nov Domestic SSS +8.9%; Uniqlo sales +8.9% y/y; +3%

Korea

Kospi opened -0.4%

Samsung Electronics -0.7%

Posco Steel +2%

Korean Won (KRW) +0.3%

(KR) South Korea President Moon: Trade faces difficulties including 'strong' Won (KRW); S. Korea should create more jobs through exports

(KR) South Korea Nov Foreign Reserves: $387.3B (record high) v $384.5B prior

(KR) South Korea Oct Current Account Balance: $5.7B v $12.3B prior; Balance of Goods (BOP): $8.6B v $15.0B prior

China/Hong Kong

Markets open lower: Hang Seng -0.8%; Shanghai Composite -0.2%

Hang Seng Information Technology Index -1.2% (Tencent -2%)

China defense names stronger on report that China has encouraged asset injections – press

(CN) China reportedly will keep exempting 10% purchase tax on electric vehicles to 2020 - press

(CN) China Nov Caixin PMI Services: 51.9 v 51.2 prior, PMI Composite: 51.6 v 51.0 prior

(HK) Hong Kong Nov PMI: 50.7 v 50.3 prior

PBoC skips open market operation for 3rd straight session, reiterates liquidity at ‘high level’; net drain CBY170B v CNY90B prior

(CN) PBoC sets yuan reference rate at 6.6113 v 6.6105 prior

(CN) Chinese Think Tank (State Info Center): Recommends China 2018 GDP target be set around 6.5%

(CN) China should cut real interest rate – China Securities Journal

(CN) Former PBoC Adviser Yu Yongding: Investment growth to slowdown in 2018 amid further slowdown in property investment; monetary policy should stay appropriate and 'not too tight’; Urges China to introduce property tax

(CN) PBOC Financial Research Institute Head Sun Guofeng: New monetary policy framework is taking shape; monetary policy targets should consider financial cycles; Central banks need to influence long-term interest rates.

(CN) China Vice Fin Min Zhu Guangyao: Sees worldwide economy recovery momentum in 2017; Attention needed to impact of Fed balance sheet reduction; Whether the ECB is to quit QE is yet to see

(CN) China should ‘brace’ for fallout from US tax cuts as they could challenge domestic manufacturing sector; China should take steps to cut enterprise costs – China Press

(CN) China Premier Li: China and Canada agree to uphold trade liberalization; to continue talk on bilateral free trade agreement (FTA)

Australia/New Zealand

ASX 200 opened -0.1%; Closed:

ASX 200 Financials Index -0.3%; Utilities Index +0.9%

Rio Tinto [RIO.AU] -1.6% (gained 1.2% during prior session)

Qantas [QAN.AU] -1.6%

AWE Ltd [AWE.AU] -11% (China Energy Reserve withdrew takeover offer yesterday)

Aussie rises amid better than expected Oct retail sales; Q3 data (Current Account, Net Exports of GDP) below ests

(AU) AUSTRALIA OCT RETAIL SALES M/M: 0.5% V 0.3%E

(AU) AUSTRALIA Q3 BOP CURRENT ACCOUNT (A$): -9.1B V –9.6B PRIOR; NET EXPORTS OF GDP: 0.00 V 0.30 PRIOR

Aussie adds to gains following RBA statement

(AU) RESERVE BANK OF AUSTRALIA (RBA) LEAVES CASH RATE TARGET UNCHANGED AT 1.50%; AS EXPECTED (16TH CONSECUTIVE HOLD IN CURRENT EASING CYCLE); The Australian dollar remains within the range that it has been in over the past two years; One continuing source of uncertainty is the outlook for household consumption

Kiwi rises following comments from RBNZ Gov Spencer

(NZ) RBNZ Gov: Persistently low inflation has prompted central bank to think about whether it needs to ‘tweak’ its approach to monetary policy; Should be cautious about making any recommendations for change in current framework

(NZ) NEW ZEALAND Q3 VOLUME OF ALL BUILDINGS Q/Q: 2.7% V 2.0%E

(NZ) New Zealand Government 4-Month budget balance (NZ$): -308M v -217Me

(NZ) New Zealand Nov ANZ Commodity Price: -0.9% v -0.3% prior

AWE.AU China Energy Reserve formally withdrew offer -15%

Looking Ahead: Australia Q3 GDP due to be released on Wednesday

North America

US equity markets pared gains and closed mixed amid passage of Senate tax bill: Nasdaq -1.1%, S&P 500 -0.1%, Dow Jones +0.2%, Russell 2000 -0.3%

S&P 500 Technology Sector -1.6%, Healthcare -1.2%

MasterCard raised quarterly dividend by 14% and announced new $4.0B buyback plan

M&A: 21st Century Fox: Reportedly favors Disney as prospective acquirer for its studio and media assets – press

Packaging company Bemis Co said to hire adviser to examine options – US Press

Tax Reform: (US) House votes for motion to go to conference with Senate on tax bill (as expected)

Government Funding: (US) US Republicans: Will pursue stop-gap government spending measure through Dec 30th – US financial press (**Note: According to prior speculation, a potential govt shutdown is looming on Dec 8th unless Congress can pass a new spending bill. Republicans are preparing a two week stop gap spending bill)

(US) Democratic Leaders Pelosi and Schumer to meet with Pres Trump and GOP leadership on Thurs – press

Looking Ahead: US Nov ISM Non-Manufacturing data to be released on Tuesday

Europe

(UK) EU's Juncker: it was not possible to make a complete Brexit deal today (comments from Monday); will need further talks to reach a complete deal; did make considerable progress - comments in Brussels; Will continue discussions with the UK this week; there are only two or three points still open; Has confidence we can make sufficient progress by time of leaders' summit (Dec 14-15)

(UK) Prime Min May: we had a constructive meeting with the EU; have been negotiating hard and want to move forward together; We need more consultations on some issues; positive that the two sides will conclude this positively

(UK) Nov BRC Sales LFL Y/Y: +0.6% v -1.0% prior

(EU) Eurogroup President-designate Centeno: deeper discussions are needed on a euro zone fiscal union; there is a long way to go

(EU) Portugal Fin Min Mario Centeno wins Eurogroup chairmanship race; term starts in Jan - press

(GR) ESM's Regling: it's a bit premature to be precise about the size of the Greece tranche; It's more likely that there's one more review left in the Greek program

Levels as of 01:00ET

Nikkei225 -0.2%, Hang Seng -0.5%; Shanghai Composite -0.2%; ASX200 -0.2%, Kospi +0.2%

Equity Futures: S&P500 +0.2%; Nasdaq100 +0.1%, Dax +0.3%; FTSE100 +0.4%

EUR 1.1877-1.1862; JPY 112.63-112.38; AUD 0.7654-0.7596;NZD 0.6908-0.6852

Feb Gold +0.1% at $1,278/oz; Jan Crude Oil +0.1% at $57.51/brl; Mar Copper +0.1% at $3.09/lb