Sample Category Title

RBA Opted To Leave Its Key Interest Rate Steady At 1.5%

For the 24 hours to 23:00 GMT, the AUD declined 0.07% against the USD and closed at 0.76.

LME Copper prices rose 1.1% or $73.0/MT to $6807.0/MT. Aluminium prices rose 0.3% or $6.0/MT to $2052.5/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7644, with the AUD trading 0.58% higher against the USD from yesterday's close, after Australia's retail sales rebounded in October, notching its highest level in five months.

Earlier today, the Reserve Bank of Australia (RBA), as widely expected, kept its key interest rate steady at 1.5%, citing soft wage growth and a lack of inflationary pressure. In a post meeting statement, Governor Philip Lowe, stated that the Australian economy likely grew at around its “trend rate” over the year to the third quarter and expressed optimism about future growth prospects. Further, the central bank stuck to its forecast for inflation to “pick up gradually as the economy strengthens”.

On the data front, Australia's AiG performance of services index climbed to a level of 51.7 in November, compared to a reading of 51.4 in the prior month. Moreover, the nation's seasonally adjusted retail sales rose more-than-expected by 0.5% on a monthly basis in October, easing concerns over a slowdown in consumer spending in recent months. In the prior month, retail sales had climbed by a revised 0.1%, while markets had anticipated for a gain of 0.3%.

Elsewhere, in China, Australia's largest trading partner, the Caixin services PMI climbed to a three-month high level of 51.9 in November, amid a pick-up in new business. In the previous month, the PMI index had registered a level of 51.2.

The pair is expected to find support at 0.7600, and a fall through could take it to the next support level of 0.7556. The pair is expected to find its first resistance at 0.7668, and a rise through could take it to the next resistance level of 0.7692.

Going ahead, investors would keep a close watch on Australia's 3Q GDP data, scheduled to release overnight.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Euro-Zone’s Investor Morale Deteriorated In December

For the 24 hours to 23:00 GMT, the EUR slightly declined against the USD and closed at 1.1870, after the Euro-zone's Sentix investor confidence index fell more-than-anticipated to a level of 31.1 in December. The index had recorded a 17-year high level of 34.0 in the prior month. Market participants had anticipated the index to fall to a level of 33.4.

On the macro front, in the US, data revealed that final durable goods orders dropped less than initially estimated by 0.8% MoM in October, compared to a revised rise of 2.2% in the previous month, while the preliminary figures had indicated a fall of 1.2%. Moreover, the nation's factory orders eased less-than-expected by 0.1% on a monthly basis in October, compared to market consensus for a drop of 0.4%. Factory orders had climbed by a revised 1.7% in the previous month.

In the Asian session, at GMT0400, the pair is trading at 1.1874, with the EUR trading a tad higher against the USD from yesterday's close.

The pair is expected to find support at 1.1842, and a fall through could take it to the next support level of 1.1811. The pair is expected to find its first resistance at 1.1892, and a rise through could take it to the next resistance level of 1.1911.

Ahead in the day, market participants would eye the release of final Markit services PMI for November across the Euro-zone along with the region's retail sales data for October. Later in the day, investors would focus on the US trade balance figures for October, followed by the ISM non-manufacturing and the final Markit services PMIs, both for November.

The currency pair is trading above its 20 Hr moving average and showing convergence with its 50 Hr moving average.

Britain And The EU Failed To Strike A Brexit Divorce Deal

For the 24 hours to 23:00 GMT, the GBP slightly rose against the USD and closed at 1.3474. Yesterday, the European Commission President, Jean-Claude Juncker and the British Prime Minister, Theresa May failed to reach an agreement on an initial Brexit divorce package.

Macroeconomic data indicated that Britain’s Markit construction PMI rose to a level of 53.1 in November, expanding at its fastest pace in five months, thus highlighting that the sector has regained some steam in the final quarter of this year. The PMI had recorded a reading of 50.8 in the prior month, while markets had expected for an advance to a level of 51.0.

In the Asian session, at GMT0400, the pair is trading at 1.3468, with the GBP trading marginally lower against the USD from yesterday’s close.

The pair is expected to find support at 1.3408, and a fall through could take it to the next support level of 1.3349. The pair is expected to find its first resistance at 1.3533, and a rise through could take it to the next resistance level of 1.3599.

Trading trend in the Pound today is expected to be determined by the release of UK’s Markit services PMI for November, set to release in a few hours.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Japan’s Services Sector Growth Cooled In November

For the 24 hours to 23:00 GMT, the USD declined 0.23% against the JPY and closed at 112.48.

In the Asian session, at GMT0400, the pair is trading at 112.53, with the USD trading marginally higher against the JPY from yesterday's close.

Overnight data showed that Japan's Nikkei services PMI declined to a level of 51.2 in November, after recording a two-year high level of 53.4 in October.

The pair is expected to find support at 112.24, and a fall through could take it to the next support level of 111.94. The pair is expected to find its first resistance at 112.96, and a rise through could take it to the next resistance level of 113.38.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Swiss Franc Trading Flat In The Morning Session

For the 24 hours to 23:00 GMT, the USD rose 0.25% against the CHF and closed at 0.9845.

In economic news, Switzerland’s total sight deposits rose to a level of CHF576.8 billion in the week ended 01 December, compared to a reading of CHF577.5 billion registered in the previous week.

In the Asian session, at GMT0400, the pair is trading at 0.9845, with the USD trading flat against the CHF from yesterday’s close.

The pair is expected to find support at 0.9821, and a fall through could take it to the next support level of 0.9797. The pair is expected to find its first resistance at 0.9868, and a rise through could take it to the next resistance level of 0.9891.

Amid a lack of macroeconomic releases in Switzerland today, investor sentiment would be determined by global macroeconomic news.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Loonie Trading On A Weaker Footing This Morning

For the 24 hours to 23:00 GMT, the USD declined 0.25% against the CAD and closed at 1.2684.

In the Asian session, at GMT0400, the pair is trading at 1.2667, with the USD trading 0.13% lower against the CAD from yesterday’s close.

The pair is expected to find support at 1.2640, and a fall through could take it to the next support level of 1.2614. The pair is expected to find its first resistance at 1.2710, and a rise through could take it to the next resistance level of 1.2754.

Ahead in the day, traders would look forward to Canada’s international merchandise trade balance for October.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

RBA Remains Cautious As Wage Growth Subdued

RBA left the cash rate unchanged at 1.5% in November, following the last reduction in August 2016. The accompanying statement contained little surprise. While staying confident over the employment situation, policymakers remained weary off the persistently soft inflation and wage growth. The RBA stance is largely unchanged from the previous meeting. We retain the view that the policy rate would stay unchanged for the entire 2018.

Employment Situation

Australia’s unemployment rate fell to 5.4%, lowest since January 2013, in October.

RBA acknowledged that employment has increased in all states. The decline in unemployment rate has come together with 'a rise in labour force participation'. This is a good sign for the job market. Rising participation rate signals more people enter the job market again in expectations of better economic environment and opportunities. The fall in unemployment rate in light of higher participation suggests that the job market can more than absorbing the bigger labor force. The central bank remained confident that 'solid growth in employment' could continue.

Inflation

Following a brief breach of the +2% target earlier this year, headline inflation been declining. While core CPI has been recovering after bottoming in mid-2016, it has remained below RBA’s desired level. As noted in the statement, the central bank noted that both the headline and core readings have been 'running a little below 2%, while reiterating the hopes that inflation would 'pick up gradually as the economy strengthens'. Affecting spending and hence inflation is wage growth which has remained subdued. The RBA suggested that the low-growth environment should 'continue for a while yet, although the stronger conditions in the labour market should see some lift in wage growth over time'.

Housing Market

Policymakers suggested that 'nationwide measures of housing prices are little changed over the past six months, with conditions having eased in Sydney'. While omitting the language that the housing prices in Melbourne were rising, CoreLogic data revealed that dwelling values in Melbourne rose +0.52% m/m in November. The rest of the comments about the housing market remained the same as the previous months. For instance, the RBA warned that 'growth in housing debt has been outpacing the slow growth in household income for some time' and the macroprudential measures have been implemented to curb medium-term risks associated with high and rising household indebtedness.

Australian Dollar

Given the fact the AUDUSD had fallen to a 5-month low of 0.753 last month and the pair recently has largely stayed at where it was at the November meeting, RBA noted that Aussie has been range-bounded. Yet, it continued to caution that 'an appreciating exchange rate would be expected to result in a slower pick-up in economic activity and inflation than currently forecast'.

Elliott Wave View: Nasdaq Short Term

Nasdaq Short term Elliott Wave view suggests that the rally to 6429.5 ended Intermediate wave (3). Intermediate wave (4) pullback is currently in progress to correct cycle from 8/21 low (5753.6) in 3, 7, or 11 swing before Index resumes the rally. Subdivision of Intermediate wave (4) is unfolding as a double three Elliott wave structure where Minor wave W ended at 6246 and Minor wave X ended at 6391.75. Minor wave Y of (4) is in progress towards 6096.66 – 6209.70 area, then Index should resume the rally higher from there or bounce in 3 waves at least. We don’t like selling the proposed pullback and expect buyers to appear from the above area for at least a 3 waves bounce as far as pivot at 8/21 low (5753.6) stays intact.

NQ_F Nasdaq 1 Hour Elliott Wave Chart

Denmark: No FX Intervention In November

- The Danish FX reserve was unchanged at DKK464bn in November.

- That was the eighth month in a row without FX intervention from Danmarks Nationalbank.

- We forecast EUR/DKK at 7.4425 on 1-6M and 7.4450 on 12M and for DN to keep the key policy rate unchanged at minus 0.65% on 12M.

Danmarks Nationalbank (DN) has just published November's FX reserve and central bank balance sheet. The FX reserve was unchanged at DKK464bn in November, with DN making no FX intervention. Government deposits were DKK139bn in November, down from DKK141bn in October.

That was the eighth month in a row without FX intervention, which highlights that it has been a quiet time for EUR/DKK since the French election, which prompted some FX intervention selling of DKK at the beginning of the year. EUR/DKK traded close to the 7.4400 level during November. It is furthermore the longest period of no FX intervention since the beginning of 2014, where DN went 14 months without intervening in FX markets.

In our view, EUR/DKK is stuck in the 7.4340-7.4450 range, with DN ready to step into the market around the level of 7.4330-40. We forecast EUR/DKK to trade around 7.4425 on 1-6M and 7.4450 on 12M and for DN to keep the key policy rate, the rate of interest on certificates of deposit, unchanged at minus 0.65% on 12M.

A focus on European politics in the market for EUR/DKK may return next year, with Italy set to hold elections, which could trigger demand for DKK. In addition, banks' net position will probably drop in Q1 18, which means slightly tighter DKK liquidity – another DKK positive. Finally, Danske Bank's DKK Exchange Market Pressure Index (EMPI) continues to signal persistent downwards pressure on EUR/DKK as DKK remains supported by strong economic fundamentals, e.g. a rising current account surplus. Hence, there is a risk to our forecast above that EUR/DKK will decline at the beginning of next year and put an end to the FX intervention drought.

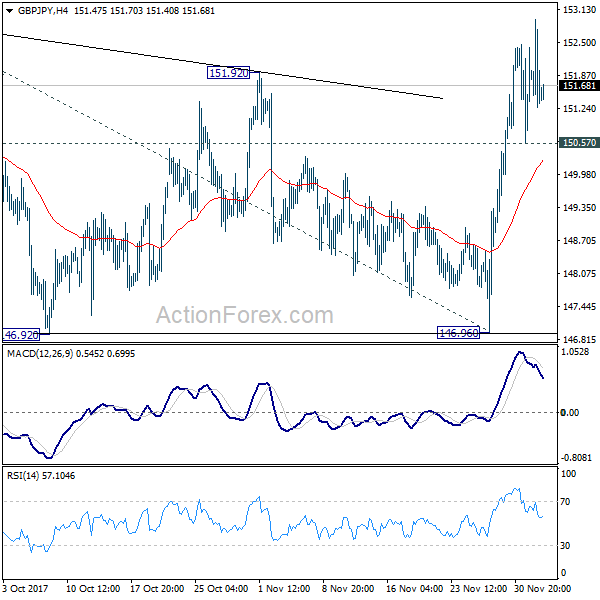

GBP/JPY Daily Outlook

Daily Pivots: (S1) 150.84; (P) 151.89; (R1) 152.55; More...

GBP/JPY lost upside momentum after breaching 152.82 resistance. But with 150.57 minor support intact, further rise is in favor. Sustained trading above 152.82 will confirm medium term rally resumption and target 61.8% projection of 139.29 to 152.82 from 146.96 at 155.32. On the downside, though, break of 150.57 minor support will dampen the bullish view and turn bias to the downside for 146.96 support again.

In the bigger picture, medium term rebound from 122.36 is still expected to resume after consolidation from 152.82 completes. Firm break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. However, break of 46.96 support will indicate rejection from 150.43 key fibonacci level. And the three wave corrective structure of rebound from 122.36 will argue that larger down trend is resuming for a new low below 122.26.