Sample Category Title

Trade Idea : USD/JPY – Buy at 111.10

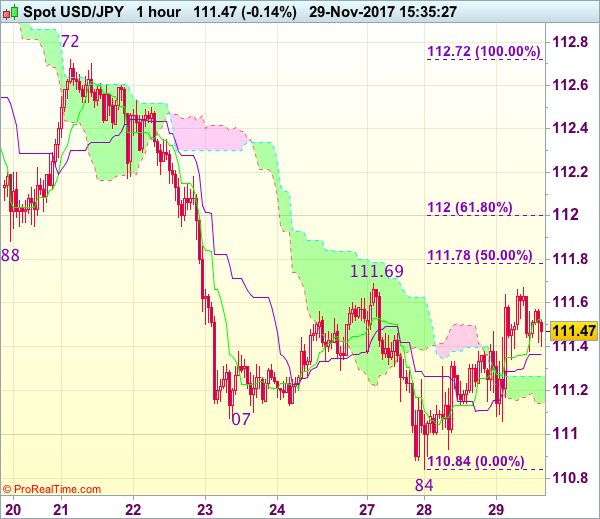

USD/JPY - 111.47

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 111.53

Kijun-Sen level : 111.37

Ichimoku cloud top : 111.27

Ichimoku cloud bottom : 111.14

Original strategy :

Buy at 111.00, Target: 112.00, Stop: 110.65

Position : -

Target : -

Stop : -

New strategy :

Buy at 111.00, Target: 112.00, Stop: 110.65

Position : -

Target : -

Stop : -

As the greenback found good support at 110.84 earlier this week and has rebounded, retaining our view that further consolidation above this level would be seen and corrective bounce to previous support at 111.88 is likely, however, reckon upside would be limited to 112.00-10 and price should falter below 112.35-40 and bring another decline later this week.

In view of this, we are still looking to buy dollar on dips. Below said support at 110.84 would signal recent decline is still in progress and may extend weakness to 110.70 and possibly towards 110.50 but loss of momentum should limit downside to 110.20-25 and reckon 110.00 would hold from here.

In The US, The Second Estimate Of GDP Growth In Q3 Is Due Out

Market movers today

Today is slightly more interesting than the past two days with inflation data out of Germany and Spain ahead of the euro inflation release tomorrow. In Europe , we also get consumer and business confidence indicators across countries today. In the US, the second estimate of GDP growth in Q3 is due out and the Fed is due to release its Beige Book.

Also in the US, Fed Chair Janet Yellen is due to appear before the Joint Economic Commit tee of Congress. However, given that markets have already priced in a December rate hike and Yellen is leaving the Fed soon, it is not really a market mover.

In the UK, BoE Governor Mark Carney and t he BoE’s Dave Ramsden are due to speak today.

In Sweden, the FSA is due to publish its Financial Stability Report , which is likely to mirror t he message from the Riksbank’s report published recently. We will also get consumer confidence where we will look for signs of whether the recent development in the housing market is spilling over to confidence.

Selected market news

Fed Chair nominee Jerome Powell’s confirmation hearing yesterday supported the view that he will stick to Yellen’s monetary policy strategy by continuing the gradualhiking cycle and ‘quanti tative tightening’ although admitting tthere may still be more slack left in the labour market. It was interesting that he was more vocal about his own target for the future level of the Fed’s balance sheet , which he thinks is between USD2,500 -3,000bn and should be reached within three to four years. In our view, this may be too optimistic, as we wrote in March earlier this year (see Research US: Fed’s regulatory hurdle for starting quantitative tightening, 13 March 2017).

As expected, the US Senate Budget Committee passed the Senate tax bi l l yesterday, meaning that there can be a full Senate vote as soon as Thursday. This is likely to be a very complicated process, as the Republicans can only afford to lose two votes (see e.g. Bloomberg).

Yesterday, The Telegraph wrote that EU and UK have agreed on the principle of the divorce bill , meaning that the UK is going to pay EU between EUR45-55bn after Brexit due to long-term liabilities, leading to a fall in EUR/GBP. Still, this may not be enough for the EU leaders to say there has been ‘sufficient progress’ in phase 1 of the negotiations (citizens’ rights, the divorce bill and Irish border) due to the increasing tension about the Ireland border issues. So, while the likelihood of a deal at the EU summit has increased, it is still not a given that the negotiations will move to phase 2 (future relationship). We st ill think it is st ill too early to price out Brexit risk premiums, as there are still many unresolved issues about what Brexit really means even if (when?) phase 1 is concluded. We st ill see EUR/GBP within the 0.8650- 0.90 range incoming months with risks becoming more balanced. In the absence of any further posit ive news today, we could see EUR/GBP climbing back above 0.89 again.

Risk sentiment in global financial markets has been mixed overnight following the advance in the US tax bill and North Korea launching another test missile.

Forex: North Korea Missile Test Fails To Rattle Markets

Earlier today, North Korea launched an ICBM that flew higher and further than any previous test firing. The missile was launched from just north of Pyongyang, reaching a height of nearly 3 kilometers and landed 600 miles east, in the Sea of Japan. This latest test firing, 2-months on from the last, is a direct challenge to President Trump, with the US Defense Secretary, James Mattis, commenting that the latest test firing demonstrates that North Korea has the ability to hit 'everywhere in the world'. Early comments from Trump have been that the US 'will handle' the situation. Trump also said, 'We will take care of it,' adding later that North Korea 'is a situation that we will handle.' This latest test appears to have had little effect on the markets with USD holding steady and only a slight demand for safe-haven Gold.

USD received a boost following news that the prospects for a US tax cut have improved after Senate Republicans forcibly pushed forward their bill in a partisan committee vote that set up a full vote by the Senate as soon as tomorrow, although details of the measure remained unclear. Republican leaders admitted that they have yet to round up the votes needed for passage in the Senate, where they hold a slim 52-48 majority.

Data released on Tuesday showed US consumer confidence has surged close to a 17-year high in November, due to a strong labor market, while house prices rose in September, which should underpin consumer spending and boost economic growth. The US Conference Board said its consumer confidence index increased 3.3 points to 129.5 in November, within striking distance of 132.6, which was touched in November 2000.

Jerome Powell, the Fed Chair nominee, appeared before the US Senate confirmation hearing on Tuesday and seemed to be continuing in his predecessor’s steps, stating that the case for a December rate hike 'is coming together'. Powell pledged to continue the Fed’s current approach to monetary policy, by gradually raising interest rates so long as economic growth remains healthy.

EURUSD is little changed overnight, currently trading around 1.1850.

USDJPY is unchanged in early Tuesday at trading around 111.52.

GBPUSD is 0.25% higher in early session trading at around 1.3367.

Gold is 0.15% higher, currently trading around $1,295.75.

WTI is 0.1% lower overnight, currently trading around $57.70.

Major data releases for today:

All Day: OPEC will host a meeting in Vienna, Austria with representatives from 13 oil-rich nations.

At 13:00 GMT: Destatis will release German Harmonized Index of Consumer Prices (YoY) for November. HICP is a measure of prices used by the Governing Council of the EU to define and assess price stability in the euro area as a whole in quantitative terms. The forecast is for a slightly higher release of 1.7%, compared to the previous 1.5%. Any significant deviation from forecast is likely to cause EUR volatility.

At 13:30 GMT: the US Bureau of Economic Analysis will release Gross Domestic Product Annualized for Q3. The forecast is for an improvement to 3.2% from the previous release of 3%. A higher release could see USD move higher, conversely, a lower than forecast release will see USD come under pressure.

Core Personal Consumption Expenditures (QoQ) for Q3 will also be released. As an important indicator of US inflation, forecasts are suggesting a higher release of 1.4% (prev. 1.3%), which will further confirm a growing US economy and a higher probability of a December rate hike from the Fed.

At 14:00 GMT: Bank of England Governor Mark Carney is scheduled to speak at the FMSB – Two Years on From the Fair and Effective Markets Review Event in London.

At 15:00 GMT: Federal Reserve Chair Janet Yellen is scheduled to testify on the economic outlook before the congressional Joint Economic Committee in the US.

At 15:30 GMT: the US Energy Information Administration will release Crude Oil Stocks change for the week ended November 24th. A higher drawdown of -3.150M is expected, compared to the previous draw of -1.855M. With OPEC meeting in Austria, the markets will be looking to see how crude oil stocks have changed in the world’s largest oil consuming nation and how that will affect the price of both WTI and Brent.

Euro At Risk Of Declines Vs Japanese Yen

Key Highlights

- The Euro is trading in a broad range above the 131.20 support area against the Japanese Yen.

- There is a crucial bearish trend line forming with resistance at 133.25 on the 4-hours chart of EUR/JPY.

- Japan's Retail Trade in Oct 2017 was unchanged, whereas the market was looking for a 0.2% rise (MoM).

- The US GDP figure for Q3 2017 will be released today, which is forecasted to grow by 3.2%.

EURJPY Technical Analysis

The Euro struggled to remain above the 133.00 handle against the Japanese Yen. The EUR/JPY pair moved down and remains at a risk of more declines toward 131.40.

Looking at the 4-hours chart of EUR/JPY, there is a crucial bearish trend line forming with resistance at 133.25. The pair recently traded as high as 133.23 and started a downside move. It traded below the 38.2% Fib retracement level of the last wave from the 131.22 low to 133.23 high.

On the downside, there is a major support forming near 132.40 and 131.20. It seems like the pair might continue to trade in a range above the mentioned support levels. On the upside, the pair needs to break the trend line resistance at 133.25-30 to gain bullish traction. On the flip side, a break below 131.00 could ignite further losses in the near term.

Japan's Retail Trade

Recently in Japan, the Retail Trade for Oct 2017 was released by the Ministry of Economy, Trade and Industry. The market was looking for a rise of 0.2% in Oct 2017 compared with the previous month.

However, the actual result was on the lower side as there was no change in the Retail Trade in Oct 2017. In terms of the yearly change, there was a decline of 0.2%, which was disappointing when compared to the last revised increase of 2.3%.

Overall, the result was negative and might help EUR/JPY in the short term.

Economic Releases to Watch Today

Euro Zone Consumer Confidence Nov 2017 – Forecast 0.1, versus 0.1 previous.

Euro Zone Services Sentiment Nov 2017 – Forecast 16.8, versus 16.2 previous.

Euro Zone Industrial Confidence Nov 2017 – Forecast 8.7, versus 7.9 previous.

Euro Zone Economic Sentiment Indicator Nov 2017 – Forecast 114.6, versus 114.0 previous.

German Consumer Price Index for Nov 2017 (YoY) (Prelim) – Forecast +1.7%, versus +1.6% previous.

German Consumer Price Index for Nov 2017 (MoM) (Prelim) – Forecast +0.3%, versus 0.0% previous.

US Gross Domestic Product Q3 2017 (Preliminary) – Forecast 3.2% versus previous 3.0%.

US Personal Consumption Expenditures Prices for Q3 2017 (QoQ) – Forecast +1.5%, versus +1.5% previous.

US Core Personal Consumption Expenditures for Q3 2017 (QoQ) – Forecast +1.4%, versus +1.3% previous.

AUDUSD Increasingly Bearish After Break Below 200-Day MA

AUDUSD continues its downward trajectory and is hovering at its lowest levels in more than 5 months. The outlook has turned increasingly bearish after the market broke below the 200-day moving average.

The recent bounce off 0.7531 (November 21 low) was capped at the 61.8% Fibonacci retracement level (0.7630) of the 0.7328 – 0.8124 rise. Breaking above this level would ease immediate downside pressure but prices would meet a resistance zone between 0.7693 – 0.7724 (200-day MA and 50% Fibonacci). Only a rise above 0.7900 would indicate the bearish phase has ended. Clearing the 0.8124 peak would see a resumption of the uptrend from May.

Failure to break above 0.7630 in the near term would keep downside momentum in play with scope to target 0.7460 before re-visiting the 0.7328 low and consequently erasing the May – September uptrend. Such a move would confirm the start of a new medium-term downtrend.

Technicals are pointing to a bearish bias. The RSI is below 50. The 50-day MA is falling and there is risk of an imminent bearish crossover with the 200-day MA.

RBA To Hike Benchmark Interest Rate Soon, Predicts OECD

For the 24 hours to 23:00 GMT, the AUD slightly declined against the USD and closed at 0.7600.

Yesterday, the OECD stated that the Australian economy will continue to expand at a robust pace, with the labour market strengthening further and added that the Reserve Bank of Australia (RBA) is expected to hike interest rate soon. The organisation predicted Australia’s GDP growth to be 2.5% in 2017, 2.8% in 2018 and 2.7% in 2019.

LME Copper prices declined 1.3% or $92.0/MT to $6800.0/MT. Aluminium prices declined 0.5% or $9.5/MT to $2100.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7584, with the AUD trading 0.21% lower against the USD from yesterday’s close.

The pair is expected to find support at 0.7571, and a fall through could take it to the next support level of 0.7559. The pair is expected to find its first resistance at 0.7608, and a rise through could take it to the next resistance level of 0.7633.

Going ahead, Australia’s HIA new home sales and building approvals data, both for October, scheduled to release overnight, would attract a lot of market attention.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

OECD Boosted Euro-Zone’s And Global Economic Growth Estimates, Urges Higher Business Investment To Maintain Global Growth

For the 24 hours to 23:00 GMT, the EUR declined 0.44% against the USD and closed at 1.1848.

In economic news, Germany's GfK consumer confidence index remained unchanged at 10.7 in December, in line with market expectations.

Meanwhile, the Organisation for Economic Cooperation and Development (OECD), in its latest economic outlook, lifted Euro-zone's growth forecast for this year and next, citing stronger growth in key European countries. The organisation expects the common currency region to grow 2.4% in 2017 and 2.1% in 2018, up from previous projections of 2.1% and 1.9% respectively. However, it further predicted that growth would sink back below 2.0% in 2019. The organisation also warned that the European Central Bank (ECB) should hold on raising interest rates before the end of the decade as raising rates too quickly “could weigh on the recovery in countries with high unemployment and large output gaps”.

Additionally, the OECD indicated that global economic growth in 2017 will be the best in seven years, but raised concerns about the longer-term outlook, citing “clear weaknesses and vulnerabilities”. Moreover, the Paris-based organisation expects the global economy to grow 3.6% in 2017 and 3.7% in 2018, before easing to 3.6% in 2019. Nevertheless, it warned that growth would slow from 2019 without new measures to promote business investment, productivity and more inclusive growth.

The US Dollar climbed against its key counterparts, following upbeat US consumer confidence data.

The CB consumer confidence index surprised to the upside, advancing to a nearly 17-year high level of 129.5 in November, amid optimism over the nation's labour market. In the prior month, the index had registered a revised level of 126.2, while markets had envisaged for a drop to a level of 124.0.

On the other hand, the nation's advance goods trade deficit widened more-than-anticipated to $68.3 billion in October, compared to market expectations for a deficit of $64.9 billion. In the prior month, the nation reported a trade deficit of $64.1 billion. Further, the nation's seasonally adjusted flash wholesale inventories unexpectedly dropped 0.4% on a monthly basis in October, defying market consensus for a gain of 0.4% and compared to an increase of 0.3% in the previous month.

The OECD inched up its growth outlook for the US economy, now expecting the world's largest economy to post a growth of 2.2% this year and 2.5% in 2018, stating that proposed tax cuts would give economic growth a temporary boost. However, growth is forecasted to slip back to 2.1% in 2019.

In the Asian session, at GMT0400, the pair is trading at 1.1854, with the EUR trading marginally higher against the USD from yesterday's close.

The pair is expected to find support at 1.1814, and a fall through could take it to the next support level of 1.1774. The pair is expected to find its first resistance at 1.1907, and a rise through could take it to the next resistance level of 1.1960.

Moving ahead, investors would draw their attention to Germany's flash consumer price inflation figures for November along with the Bundesbank monthly report, both due to release in a few hours. Moreover, the US annualised 3Q GDP, the Beige book report and pending home sales data for October, all set to release later in the day, will garner significant amount of investor attraction. Also, a speech by the Federal Reserve (Fed) Chair, Janet Yellen will keep investors on their toes.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Britain’s Banks Could Survive A ‘Disorderly Brexit’, Says Mark Carney

For the 24 hours to 23:00 GMT, the GBP rose 0.24% against the USD and closed at 1.3354, in the wake of a report which revealed that UK and the European Union (EU) have agreed a deal over Britain's Brexit divorce bill, which could unlock vital trade talks next month.

Meanwhile, the Bank of England (BoE) Governor, Mark Carney stated that leading financial institutions in Britain could cope up and even support Britain through a 'disorderly' Brexit. However, Carney stressed that this would be 'painful' as it would hamper households and businesses and hurt the nation's economic growth.

Separately, the OECD, in its latest global outlook, warned that the UK economy would continue to slow in 2018 and 2019, due to heightened uncertainty around Brexit and the impact of higher inflation on households. Economic growth in Britain is expected to grow 1.5% in 2017, before slipping down to 1.2% in 2018 and 1.1% in 2019.

In the Asian session, at GMT0400, the pair is trading at 1.3361, with the GBP trading a tad higher against the USD from yesterday's close.

The pair is expected to find support at 1.3259, and a fall through could take it to the next support level of 1.3157. The pair is expected to find its first resistance at 1.3425, and a rise through could take it to the next resistance level of 1.3489.

Ahead in the day, market participants would look forward to UK's net consumer credit and mortgage approvals data, both for October, slated to release in a few hours.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

BoJ Should Rethink On Monetary Policy If Inflation Remains Elusive

For the 24 hours to 23:00 GMT, the USD rose 0.41% against the JPY and closed at 111.50.

Yesterday, the OECD, warned that the Bank of Japan (BoJ) should reassess its loose monetary policy if it is unable to meet its inflation target for a prolonged time, otherwise it could end up holding too much government debt. The OECD slightly lowered Japanese economic growth forecast to 1.5% in 2017 and added that the nation’s economic growth is expected to slow from 2018 as the government provides less fiscal stimulus.

In the Asian session, at GMT0400, the pair is trading at 111.45, with the USD trading slightly lower against the JPY from yesterday’s close.

Overnight data revealed that Japan’s retail trade remained flat on a monthly basis in October, against market expectations for a rise of 0.2%. Retail trade had advanced 0.8% in the prior month. Meanwhile, the nation’s large retailers’ sales declined less-than-anticipated by 0.7% in October, compared to a gain of 1.9% in the prior month, while markets were anticipating for a fall of 0.8%.

The pair is expected to find support at 111.12, and a fall through could take it to the next support level of 110.78. The pair is expected to find its first resistance at 111.73, and a rise through could take it to the next resistance level of 112.00.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Swiss Franc Trading Marginally Lower, Ahead Of Swiss ZEW Expectations Data

For the 24 hours to 23:00 GMT, the USD rose 0.26% against the CHF and closed at 0.9838.

In the Asian session, at GMT0400, the pair is trading at 0.9841, with the USD trading a tad higher against the CHF from yesterday’s close.

The pair is expected to find support at 0.9816, and a fall through could take it to the next support level of 0.9792. The pair is expected to find its first resistance at 0.9859, and a rise through could take it to the next resistance level of 0.9878.

Investors would focus on Switzerland’s ZEW expectations index for November as well as the UBS consumption indicator for October, both set to release in a while.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.