Sample Category Title

Cable Has a Catalyst

Separate reports suggested UK PM Theresa May's government is close to a breakthrough on negotiations around the Brexit bill. Cable jumped on the headlines and was the top performer on the day while the euro lagged. Japanese retail sales are due up next. 2nd EURUSD trade has been issued. Tomorrow marks Janet Yellen's final testimony to Congress' joint economic committee. The video for Premium subscribers is posted below, highlighting the existing and future trades.

It was a lively day of trading that included heavy newsflow. The pound suffered early and cable was down more than a cent when a Telegraph report said a deal was largely done that would put the exit bill at 45-55B euros. Cable jumped more than 120 pips then fell back down when a government spokesman denied it. A second report, this time from the FT, added more detail, indicating the deal could be part of a broader deal on the Ireland border and EU citizen's rights. That sent cable near 1.3400 from as low as 1.3220 on the day.

More importantly, it's a fresh catalyst for cable. If confirmed, it's a sign that negotiations are bearing fruit and progressing towards some sort of a deal. At this point, nearly any kind of resolution or progress is good for sterling.

Across the Atlantic, the US dollar was buoyed by economic data as consumer confidence rose to the best level since 2000 and the Richmond Fed hit an all-time high. New home sales also beat expectations, but trade and inventory reports led to downgrades of Q4 growth estimates.

The tax plan also made progress but once again that buoyed stock markets while leaving the US dollar behind. The S&P 500 surged 26 points to a record 2627.

In geopolitical news, North Korea tested a missile but the dip was merely a buying opportunity in USD/JPY and stock markets.

Amidst all that, Fed chair nominee Powell was grilled in his confirmation hearing but most of the time was eaten up trying to score political points on the tax plan. On monetary policy, he did his best Yellen impression and said gradual rate hikes was the best path forward. At the same time, he struck a few dovish notes by warning on low wage inflation and some signs of slack.

Looking ahead, we will continue to monitor the North Korea fallout but also watch for retail sales from Japan at 2350 GMT. The consensus is for a +0.2% m/m rise after a 0.8% m/m jump in Sept. Comments from the BOJ's Nakaso are also due at 0700 GMT.

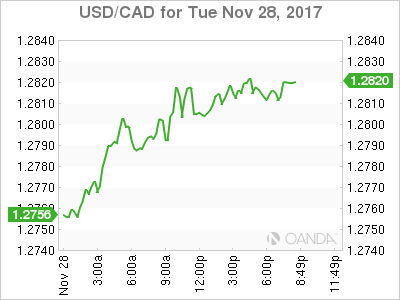

Canadian Dollar Lower After Strong US Consumer Confidence

The Canadian dollar depreciated on Tuesday with the US dollar gaining on confident consumers and improving housing prices in the United States. Canadian producer prices rose 1.0 percent in October thanks to auto prices being sensitive to a currency fluctuations. Raw materials rose 3.8 percent as energy prices keep rising. Despite the rise in inflation indicators the loonie could not gain a foothold against the USD. The Bank of Canada (BoC) presented its Financial System Review and Governor Poloz held a press conference to discuss the findings of the economic assessment.

In the last review six months ago the central bank had struck notes of concerns regarding high levels of household debt and rising house prices. Now with two rate hikes between them and new regulation in place to avoid a housing bubble the BoC was seen as optimistic, but gone were the hawkish undertones of the summer. The Canadian central bank remains concerned with household debt as it exposes borrowers to higher rates but that could be offset by a strong jobs component with growing wages. Poloz said that the risks were unchanged, but the policy changes in housing finance are a step in the right direction. The BoC is not expected to make another adjustment to the Canadian benchmark rate until 2018 as there are improvements in the indicators, but the jury is still out on the price fo crude and the fate of NAFTA.

Trade relations between the US and Canada just got thornier after the latter just initiated a WTO case against the US for the duties it imposed on Canadian lumber. This follows the NAFTA challenge issued in early November. The renegotiation of the 23 year old trade agreement have not gone to plan and in some best case scenarios the deal would be close to being wrapped up before the end of the year. The reality is that the negotiating teams are far apart, specially the US Trade representatives who are pushing an America First agenda that leaves little room to compromise.

The USD/CAD gained 0.36 percent on Tuesday. The currency pair is trading at 1.2815 after Fed Chair nominee went before the US Senate to testify. He remains a hawk in the style of Janet Yellen and talking about the December rate hike. The rise of consumer confidence as reported by the Conference Board is now at a 17 year high, which bodes well for tomorrow's release of the second estimate of third quarter gross domestic product (GDP) data. The Bank of Canada (BoC) Financial System Review and the word form Governor Poloz could not offset the strong US data and the loonie depreciated.

The Bank of Canada (BoC) hiked twice in 2017, but that only put the Canadian benchmark rate back to 1 percent where it was when Governor Poloz cut the rate twice to boost the economy ahead of the fall of oil prices. The loonie will face more pressure as the Fed continues its monetary policy tightening pace, while the BoC will be more cautious as it monitors rising household debt.

Job numbers will be released in Canada on Friday, December 1. Statistics Canada will publish the monthly GDP figures as well as the employment report both at 8:30 am EST. GDP is expected to have shrunk by 0.1 percent and there is some anxiety on the job front as the first ADP job report for Canada showed a loss of 5,700 in October. The US GDP for the third quarter is expected to have improved between the first and second estimates, and if the Canadian economy continues to show signs of cooling it will put more pressure not the CAD ahead of the December monetary policy meetings of both central banks.

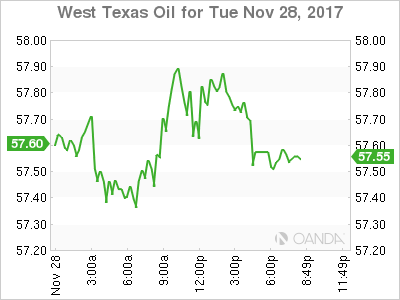

Oil prices recovered some ground in the last 24 hours. West Texas Intermediate is trading at $57.73 awaiting the news to come out of the Organization of the Petroleum Exporting Countries (OPEC) meeting in Vienna. The price of oil has already priced in an extension as multiple comments from OPEC and non-OPEC members have pointed to increasing the deadline past March 2018. The main remaining issue is how long will the agreement be extended by. The consensus at this point is for a 9 month extension with a meeting at the six month mark to review.

Earlier today a committee made up by OPEC and non-OPEC members recommended the extension until the end of 2018, with the option of a review in June. Comments from energy Ministers have been supportive, but the duration of the deal is still up for debate in the next couple of days.

US production has increased and with the Keystone pipeline restarted operations, but still at reduced capacity. Disruptions in North America due to weather and forest fires has kept production lower than otherwise expected with the OPEC doing the heavy lifting on price stability. The market will be watching for developments in Vienna as the floor of energy pricing has been put in place by the OPEC production cut, and once it reaches its end crude prices will be vulnerable if global demand for energy has not recovered at the same rate as production.

Market events to watch this week:

Wednesday, November 29

- All Day All OPEC Meetings

- 8:30am USD Prelim GDP q/q

- 10:30am USD Crude Oil Inventories

- 7:00pm NZD ANZ Business Confidence

- 7:30pm AUD Private Capital Expenditure q/q

Thursday, November 30

- 8:30am USD Unemployment Claims

Friday, December 1

- 4:30am GBP Manufacturing PMI

- 8:30am CAD Employment Change

- 8:30am CAD GDP m/m

- 10:00am USD ISM Manufacturing PMI

*All times EDT

Gold Ticks Higher, Markets Digesting Powell Testimony

Gold has posted slight gains on the Tuesday session. In North American trade, the spot price for an ounce of gold is $1295.91, up 0.12% on the day. In the US, CB Consumer Confidence jumped to 129.5, crushing the estimate of 123.9 points. In Washington, Fed Chair Designate Jerome Powell testified at his confirmation hearing before the Senate Banking Committee.

The markets were listening closely, as Jerome Powell testified before a senate committee. Powell said that he favored tailoring regulations for small banks, leaving the toughest regulations for the big players. Powell was cautious and diplomatic during the hearing, saying that the case is building for a December rate hike, and refused to express an opinion on the Trump tax bill. He will replace Janet Yellen in February, and is widely expected to continue Yellen's monetary stance of small, gradual rate hikes.

Powell inherits an economy that is in excellent shape, but persistently low inflation remains a nagging problem. Fed policymakers have differing views on what to do about inflation, with some members proposing that the Fed drop its 2 percent target, in favor of a "gradually rising path" for prices. The Fed remains confounded by low inflation and wage growth, despite a labor market that is at full capacity. Still, the Fed will likely pull the rate trigger next month, and could raise rates up to 3 more times in 2018 if the economy continues to expand at its current pace.

Pound Slips as Carney Spooks Markets

The British pound has posted considerable losses in the Tuesday session. In North American trade, GBP/USD is trading at 1.3223, down 0.66% on the day. On the release front, the Bank of England published the results of its bank stress tests and the semi-annual Financial Stability report. In the US, CB Consumer Confidence jumped to 129.5, crushing the estimate of 123.9 points. In Washington, Fed Chair Designate Jerome Powell is testifying at his confirmation hearing before the Senate Banking Committee.

There was positive news from the banking sector on Tuesday, as all seven major UK banks passed the BoE's stress tests. This is a reliable indication that the banking sector is in decent shape, despite nagging concerns about the toll that Brexit could take the British economy. Still, investors were quick to seize on negative comments from BoE Governor Mark Carney, who warned that in the case of a "disorderly" Brexit, the financial sector would face "some quite material economic costs". Carney's warning has sent the pound lower on Wednesday. Prime Minister May is expected to improve on its offer for its Brexit divorce bill, which could smooth some feathers in Brussels. Until now, the Europeans had demanded EUR 60 billion, while the UK had countered with EUR 20 billion. Another headache for May is the issue of the border between Northern Ireland and Ireland and its status after Brexit. The DUP party, which is propping up May in parliament, does not want a hard border between Ireland and Northern Ireland. However, if Britain does not remain in a customs union with the EU after Brexit, the result would likely be a hard border, given that there would be different regulatory schemes in Ireland and Northern Ireland.

All eyes are on the Federal Reserve on Tuesday, as Jerome Powell is testifying before the Senate Banking Committee. Investors will be listening closely, as Powell faces questions from lawmakers about his plans as head of the powerful central bank. Powell is widely expected to maintain Janet Yellen's cautious monetary stance, which has been marked by small, incremental rate hikes. Powell inherits an economy that is in excellent shape, but persistently low inflation remains a nagging problem. Fed policymakers have differing views on what to do about inflation, with some members proposing that the Fed drop its 2 percent target, in favor of a "gradually rising path" for prices. The Fed remains confounded by low inflation and wage growth, despite a labor market that is at full capacity. Still, the Fed will likely pull the rate trigger next month, and could raise rates up to 3 more times in 2018 if the economy continues to expand at its current pace.

Strong US Data May Fail to Lift Dollar as Tax Plan Concerns Weigh

GDP estimates and data on personal consumption expenditures (PCE) are two keenly awaited releases this week in the United States as the December FOMC meeting approaches when a rate hike is widely anticipated. However, the data will likely get overshadowed by the Senate debate on the Republican tax plan, where a vote could come as early as November 30.

The US dollar remains vulnerable to negative developments on the tax front but solid economic indicators should provide some support at the very least even if they don't manage to lift the currency.

The second estimate of third quarter GDP is due on Wednesday, with an upward revision from 3.0% to 3.2% expected. The US economy has been gaining momentum this year, after growing only moderately in 2016. It is the first time since 2014 that annualized GDP growth has equalled or exceeded 3% for two consecutive quarters after growing by 3.1% in the second quarter.

Faster growth has yet to generate higher price pressures though, at least not according to the Fed's preferred measure of inflation – the core PCE price index. While headline CPI has risen above 2% in recent months, the core PCE price index has eased from 1.9% year-on-year at the start of 2017 to 1.3% in September. It is expected to tick higher to 1.4% in October in Thursday's data – still well below the Fed's 2% objective.

Thursday's PCE data will also include the latest personal income and spending figures. Personal income growth is forecast to moderate slightly from 0.4% to 0.3% month-on-month in October. Personal consumption is expected to see a sharper slowdown from 1% to 0.3%, but the drop is mainly due to the distortion seen in September when motor vehicle sales surged as a result of the damage caused by the hurricanes.

Any upside surprises to this week's data would only reinforce expectations that the Fed will raise the fed funds rate to a target range of 1.25-1.50% when it meets on December 12-13. But with a rate hike next month already priced in and with renewed concerns about a prolonged undershoot of inflation, the longer-term path of interest rates will likely be influenced by whether or not the tax plan is passed by Congress.

Investor angst about a possible delay or watering down of the tax plan has been weighing on the dollar recently, contributing to its month-long decline against the yen and other majors. Having passed the vote in the House of Representatives, the legislation has now moved to the Senate where Republican support is proving much trickier, especially as the party's majority is just two.

Reasons for opposition by some Republican Senators range from concerns about increasing the government deficit by $1.5 trillion over 10 years to demands for bigger tax cuts for pass-through businesses and displeasure for linking the bill with the repeal of the Obamacare individual mandate. It is thought there could be as many as 10 Republican Senators ready to oppose the bill in its current form if the Senate Budget Committee approves for the vote to go ahead on Thursday as expected.

Pressure is high on Republicans to pass the bill before the end of the year as President Trump badly needs a major legislative success for his first year in office. However, the rush to get it done before the year-end could jeopardise the tax plan by not giving lawmakers enough time to debate and improve the bill.

If the Senate postpones the vote this week or fails to pass it, the delay could add further downside pressure to the dollar, forcing a breach of the 111-yen handle. Failure to hold above 111 yen could trigger further declines towards the bottom of its 2017 range around 108 yen.

Consumer Confidence: Let the Party Continue

Consumer confidence surged to the highest level in 17 years, at 129.5 in November. Consensus was expecting a slight decline for the month. The Index was upwardly revised in October, from 125.9 to 126.2.

Consumers Enter the Holiday Season Upbeat

According to the Conference Board's Consumer Confidence Index, American consumers are heading into this year's holiday season with the highest confidence in 17 years. We have to go back to November of 2000 to see a higher consumer confidence level and this is no small feat. However, what is even better today is that consumer confidence back in November 2000 was actually coming down, while today's consumer confidence is still climbing. Not only is consumer confidence the highest in 17 years, it is also still improving compared to what was happening in November 2000.

The Present Situation Index was higher in November, up to 153.9 from a print of 152.0 in October, while the Expectations Index increased from 109.0 in October to 113.3 in November. According to the Conference Board's report, one of the biggest drivers of consumers' expectations was the improvement in the labor market.

Furthermore, both the assessment of business conditions as well as employment conditions improved during the month. Those considering business conditions as "good" improved from 34.4 percent to 34.9 percent, while those indicating business conditions were "bad" declined from 13.5 percent to 12.7 percent. Meanwhile, the assessment of the labor market also continued to improve. Those assessing that jobs were "plentiful" increased from 36.7 percent to 37.1 percent, while those that said jobs were "hard to get" decreased further, from 17.1 percent to 16.9 percent.

Perhaps the biggest issue is not how confident consumers are, but if they are willing to borrow in order to increase holiday purchases this year. Although consumer confidence has improved for several household income segments, it is still not homogeneous.

It is clear that those in the upper levels of income have been the most upbeat since late last year, while those in the lower income levels have had their issues with confidence.

Overall, as shown in the bottom graph, while consumer confidence has continued to improve and income expectations have followed through, disposable income growth has remained muted over the last year or so. Thus, consumers will have to continue to bring down the saving rate, as they have done for more than a year, and/or they will have to demand more credit to make this holiday season as merry as what the consumer confidence index has been indicating. Since, as we pointed out above, we are still in the upswing phase of consumer confidence, the probability that consumers will act on this higher confidence is high today.

EURGBP Advances on Weaker Pound

The cross advances on weaker pound and broke above barrier at 0.8955 (100SM, meeting next target at 0.8973 (Fibo 76.4% of 0.9013/0.8841). Today's action was supported by daily cloud base (0.8916) with fresh advance on track to form bullish outside day and generate signal for fresh upside. Daily techs are turning to full bullish setup and extension towards next targets at 0.9019 (15 Nov high) and more significant 0.9026 barrier (top of thick daily cloud). Sustained break above daily cloud (also former tops of 20/12 Oct) will be strong signal fur bullish continuation pf recovery leg from 0.8732 (01 Nov low). Cloud base is expected to hold and keep bulls in play.

Dollar Moves Higher as US Consumer Confidence Touches 17-Year High; Irish Worries Ease

The day's main release pertained to US consumer confidence figures released late in the session. Those came in at a multi-year high, creating a positive backdrop for the greenback for the remainder of the day. Beyond this, new Fed chief Jerome Powell appearing before US senators, US tax reform deliberations and developments that could affect the outcome of Brexit negotiations were also gathering attention.

Powell's confirmation hearing before the Senate Banking Committee has begun at 1500 GMT, with senators having the opportunity to pose questions; market moving comments are not to be ruled out. Through his prepared remarks, which were released during late US session yesterday, he supported a gradual rise in interest rates, representing an element of continuity from Janet Yellen. He also indicated willingness to move "decisively" against "new and unexpected threats" to the economy, while making reference to flexibility and independence from political interference in policy setting. Powell is set to succeed Fed chair Yellen once her term expires in February.

US tax reform is also on the forefront with President Trump holding discussions with Senate Republicans to steer developments in the direction his administration desires. The US Senate will be debating the tax-cut bill with a vote potentially taking place on Thursday.

The dollar index was 0.3% up on the day at 1532 GMT, distancing itself from yesterday's two-month low of 92.50. Dollar/yen was 0.2% higher at 111.30, but not far above yesterday's two-and-a-half-month low of 110.83. Euro/dollar traded 0.1% lower at 1.1879 after touching 1.1960 on Monday, a level last experienced in late September.

The US Conference Board's consumer confidence index for the month of November surprised to the upside, coming in at 129.5 to hit a fresh 17-year high, contrasting expectations for a minor slowdown to 124.0. October's reading was also revised upwards to 126.2 from 125.9. The US currency recorded gains relative to major rivals following the release.

Earlier in the day, the S&P Case-Shiller home price index showed house prices rising in September with the broadest indicator recording an increase by 6.2% y/y, advancing at a slightly faster pace than analysts' projections of 6.1%. August's respective reading was revised to 5.8% from the previous 5.9%. The index is advancing "at the fastest annual rate since June 2014" said S&P Dow Jones indexes managing director David Blitzer, while stating that indicators support the case for additional gains in home prices. Dollar/yen didn't react much within the first minutes of data release.

Unlike the year before, the Bank of England's stress tests for the current year saw all banks pass. The central bank also said that UK banks can withstand a disorderly Brexit, while acknowledging the costs from such an outcome. In addition, effective next November, the BoE doubled the counter-cyclical buffer large banks must hold to 1.0%. This is to be reviewed next year and is estimated to result in an increase in costs by around 6 billion pounds (close to $8bn).

The Irish border issue, a key consideration and one holding Brexit discussions back from moving to the next level, was getting even more complicated in recent days with the Irish government being at the brink of collapse. The party supporting the minority government was demanding the resignation of deputy prime minister Frances Fitzgerald over a police scandal in order to continue backing the government. Fitzgerald decided to resign today, perhaps easing the UK government's concerns as it was given a December 4 deadline to present improved positions on the key Brexit issues in order for EU leaders to approve the beginning of talks on trade relations between Britain and the EU during the December 14-15 summit. Pound/dollar was last 0.4% down on the day at 1.3262 and euro/pound traded 0.25% up at 0.8955.

Dollar/loonie was 0.3% up on the day and just above the 1.28 handle ahead of the Bank of Canada's Governor Stephen Poloz and Senior Deputy Governor Carolyn Wilkins participating in a press conference at 1630 GMT.

In commodities, gold was flat at $1,294.60 an ounce. Yesterday, it came close to the $1,300 level, recording a one-and-a-half-month high. WTI and Brent crude were lower by 0.1% and 0.3% at $58.04 and $63.64 per barrel respectively. The API weekly report which includes information on US crude stocks is due at 2130 GMT.

Yen Gains Ground, Investors Eyeing Powell Testimony

The Japanese yen has posted gains in the Tuesday session. In North American trade, USD/JPY is trading at 111.31, up 0.18% on the day. In the US, CB Consumer Confidence jumped to 129.5, above the estimate of 123.9 points. Fed Chair Designate Jerome Powell is testifying at his confirmation hearing before the Senate Banking Committee. Later, in the day, Japan releases Retail Sales, which is expected to slow to 0.1%. On Wednesday, the US publishes Preliminary GDP and Pending Home Sales and Janet Yellen will testify before a congressional committee.

The changing of the guard at the Federal Reserve has kicked off on Tuesday, as Jerome Powell is testifying before the Senate Banking Committee. Investors will be listening closely, as Powell faces questions from lawmakers about his plans as head of the powerful central bank. Powell is widely expected to maintain Janet Yellen's cautious monetary stance, which has been marked by small, incremental rate hikes. Powell inherits an economy that is in excellent shape, but persistently low inflation remains a nagging problem. Fed policymakers have differing views on what to do about inflation, with some members proposing that the Fed drop its 2 percent target, in favor of a "gradually rising path" for prices. The Fed remains confounded by low inflation and wage growth, despite a labor market that is at full capacity. Still, the Fed will likely pull the rate trigger next month, and could raise rates up to 3 more times in 2018 if the economy continues to expand at its current pace.

With the Japanese economy showing moderate growth, there has been speculation that the Bank of Japan is giving some thought to tapering its massive stimulus program. Any tapering to the program could give a significant boost to the yen, so the markets are closely monitoring BoJ statements and comments from BoJ policymakers, looking for clues. However, a stronger yen would hurt exports, which has been a catalyst for the stronger economy. Inflation and wage growth remain low, and if we are to take BoJ Governor Haruhiko Kuroda at his word, the Bank will not taper stimulus before inflation moves closer to the BoJ's target of around 2 percent.

Elliott Wave analysis: USDMXN and NZDUSD Update

Good day traders.

USDMXN is trading in a clear bearish impulse, with recent bullish reversal being part of wave 4). This wave 4) can look for resistance near the Fibonacci ratio of 38.2 and 50.0 and near former swing high of one minor degree wave four and there make a new drop lower.

USDMXN, 1H

NZDUSD is recovering, now seen in wave 5 of A) which is approaching the upper line of an EW channel and some Fib. resistance level that can limit current bullish leg. We know that after every five waves market turns, so traders should be prepared on a three wave set-back, lower into wave B).

NZDUSD, 1H