Sample Category Title

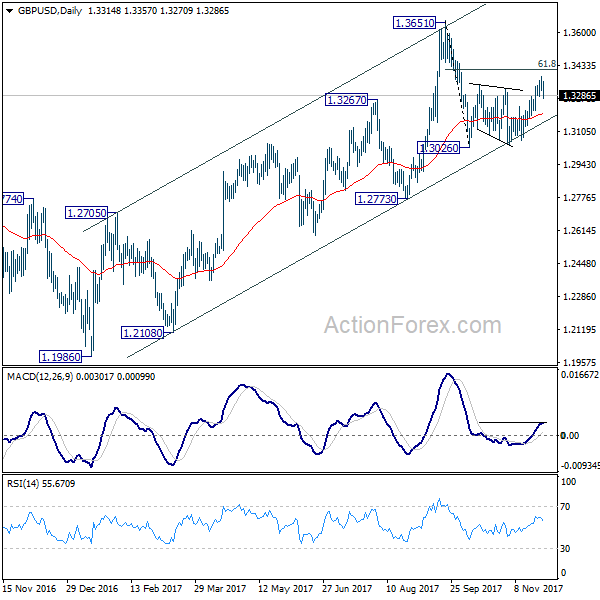

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3290; (P) 1.3336; (R1) 1.3363; More....

GBP/USD's rebound was limited at 1.3382 and weakens sharply. Loss of momentum and break of 1.3278 minor support revive the case that price actions from 1.3026 are merely a correction. Intraday bias is turned back to the downside and sustained trading below 4 hour 55 EMA will pave the way to retest 1.3026 low. Above 1.3382 resistance will target 61.8% retracement of 1.3651 to 1.3026 at 1.3412 instead.

In the bigger picture, as noted before, GBP/USD hit strong resistance from the long term falling trend line. Nonetheless, subsequent fall was contained by 55 week EMA (now at 1.3069). Outlook is a bit mixed. For the moment, as long as 1.3835 support turned resistance holds, medium term rise from 1.1946 are viewed as a corrective pattern. That is, we'd expect another leg in the long term down trend through 1.1946 low. However, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

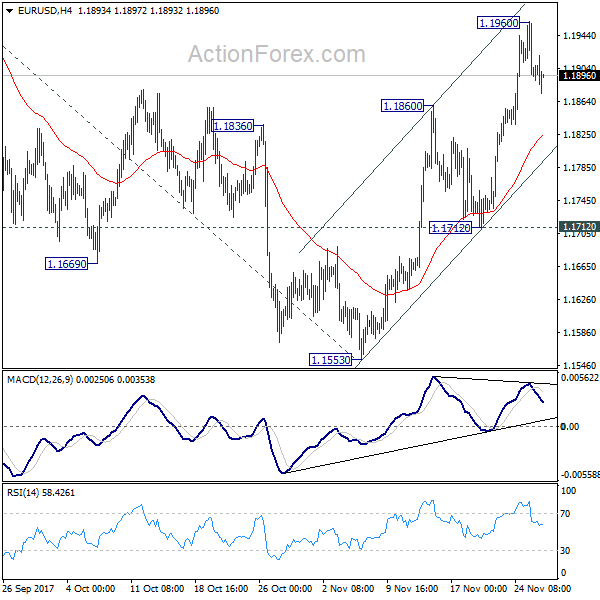

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1875; (P) 1.1918 (R1) 1.1941; More....

A temporary top is in place at 1.1960 and intraday bias in EUR/USD is turned neutral first. As long as 1.1712 support holds, rise from 1.1553 is expected to continue. Above 1.1960 will target 1.2091 high first. Break there will resume medium term up trend from 1.0339 and target 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494, which is close to 1.2516 long term fibonacci level. We'd expect strong resistance from there to bring reversal. On the downside, break of 1.1712 will indicate completion of the rise from 1.1553 and turn near term outlook bearish.

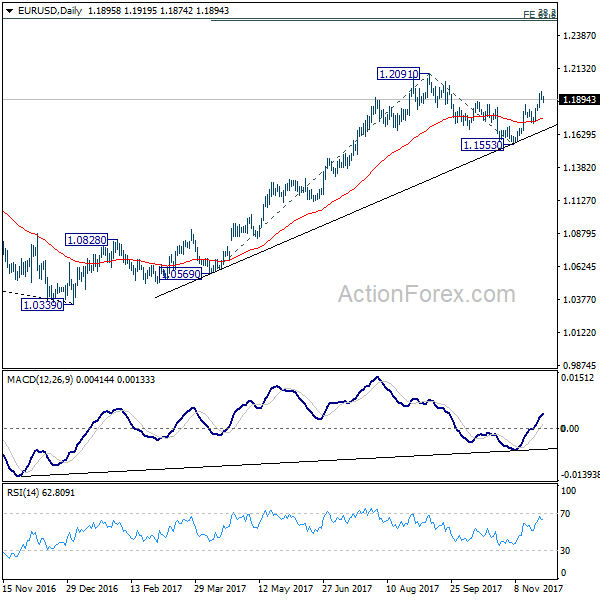

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1393) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.73; (P) 111.20; (R1) 111.57; More...

A temporary low is in place at 110.83 and intraday bias is turned neutral first. As long as 112.71 resistance holds, fall from 114.73 is expected to continue. Below 110.83 will target 61.8% retracement of 107.31 to 114.73 at 110.14. For the moment, we're still favoring the case medium term corrective pattern from 118.65 has completed at 107.31 already. Hence, we'll looking for bottoming below 110.14 to bring another rise. On the upside, break of 112.71 will suggest that the fall from 114.73 is completed and turn bias to the upside for retesting this resistance.

In the bigger picture, as long as 107.31 support holds, medium term rise from 98.97 (2016 low) is not completed yet. And another rise is in favor. Break of 114.73 resistance will target a test on 118.65 high first. However, break of 107.31 will dampen this will and extend the medium term fall back to 98.97 low.

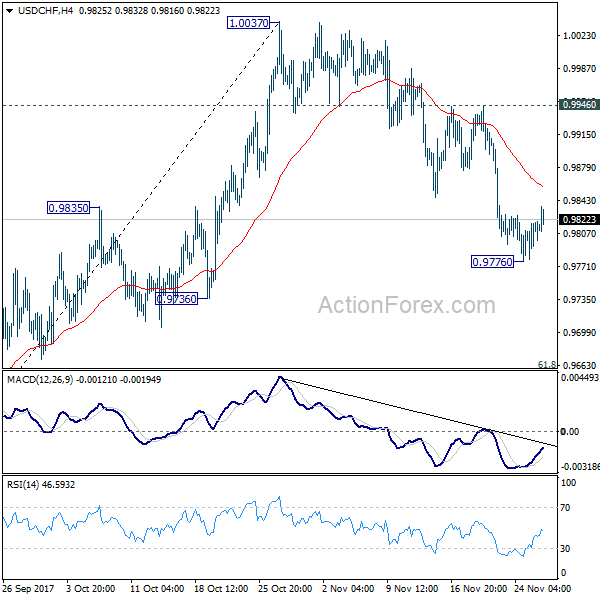

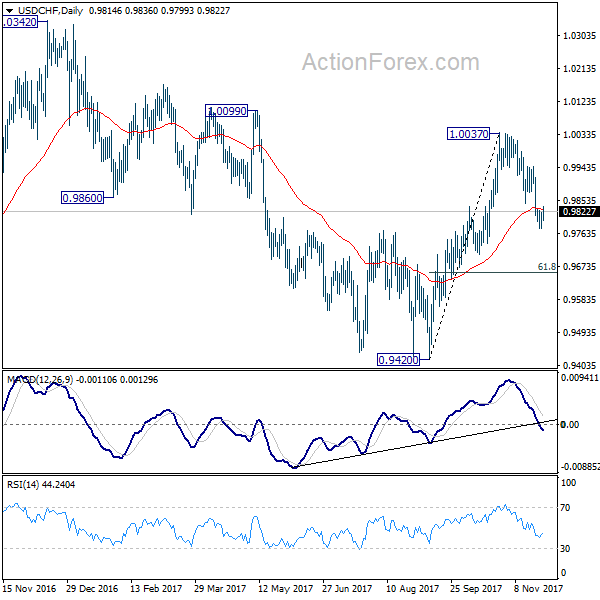

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9788; (P) 0.9804; (R1) 0.9832; More....

Intraday bias in USD/CHF remains neutral as recovery from 0.9776 temporary low continues. As long as 0.9946 resistance holds, another fall is still expected. Below 0.9776 will extend the decline from 1.0037 to 61.8% retracement of 0.9420 to 1.0037 at 0.9656. We'll look for bottoming again below 0.9656 and above 0.9420. On the upside, break of 0.9946 resistance will indicate that the decline from 1.0037 has completed and bring retest of this resistance.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

Dollar Paring Losses, OECD Projects US Growth to Accelerate in 2018, Other Major Economies to Slow

Dollar recovers broadly today as it's digesting recent losses. Also there is some support from OECD report that projects acceleration in US growth next year. Focus will turn to Fed chair nominee Jerome Powell's confirmation hearing. But Powell is generally seen as a safe choice for the job and shouldn't give us surprises. While the greenback recovers, momentum remains unconvincing as trader stays cautious ahead of Senate vote on tax bill later in the week. Elsewhere, Aussie and Kiwi are both trading as the strongest one today while Sterling is back under broad based pressure.

Powell expects interest rates to rise and balance sheet to shrink

Fed chair nominee Jerome Powell released a statement to the Senate Banking Committee before his confirmation hearing today. Powell said in the statement that Fed policy makers "expect interest rates to rise somewhat further and the size of our balance sheet to gradually shrink." Adding to that, he emphasized "while we endeavour to make the path of policy as predictable as possible, the future cannot be known with certainty." So far, Powell sounded like he would like maintain continuity from the Yellen era. But we may read deeper into his mind in the Q&A session today.

OECD projects Eurozone, Japan, UK, China growth to slow in 2018, US in 2019

The Organization for Economic Cooperation and Development published its semi-annual economic outlook report today. OECD projects further acceleration in global growth in 2018, but could slow in 2019. Global economy is forecast to grow 3.6% in 2017, accelerate to 3.7% in 2018, then slow to 3.6% in 2019. But it warned that "evidence continues to build that financial asset prices are inconsistent with expectations for future growth and the policy stance, exacerbating the risks of financial corrections and growth downdrafts." That suggests investors are being too optimistic.

US is projected to grow 2.2% in 2017, accelerates to 2.5% in 2018 and then slow sharply to 2.1% in 2019. Fiscal and business spending could boost wages and then prompt inflation and more Fed tightening. OECD noted that "risks to the outlook remain sizable". In particular "elevated leverage ratios in the corporate sector need careful monitoring and action to ensure that these risks are contained."

Eurozone growth is expected to peak at 2.4% in 2017, then slow to 2.1% in 2018 and 1.9% in 2019. OECD cautioned that ECB tightening too quickly could "weigh on the recovery in countries with high unemployment and large output gaps". Also, while OECD projected inflation to pick up to 1.7% by 2019, it would remain well below ECB's target of at or slightly below 2%.

Japan growth is also projected to peak in 2017 at 1.5%, then slow to 1.2% in 2018 and then 1.0% in 2019. The organization urged that "a rethinking of the monetary policy strategy would, however, be needed if the inflation target is not met for a prolonged time." Also, it criticized that "the BOJ becomes an even more predominant holder and buyer of government bonds and financial intermediation and stability become compromised."

UK Growth is projected to slow to 1.5% in 2017 and continued the downward path, to 1.2% in 2018, then 1.1% in 2019. The growth slowdown would be due to "continuing uncertainty over the outcome of negotiations around the decision to leave the European Union and the impact of higher inflation on household purchasing power." Nonetheless, "the upward revision of 0.2 percentage points for 2018 in part reflects the slower pace of fiscal consolidation announced in the Budget, and also partly reflects our revised technical assumption on the exit from the EU."

While China remains one of the global economic driver, growth is also to peak in 2017 at 6.8%, then moderate to 6.6% in 2018 and then 6.4% in 2019. Instead, India might suffer a blip with grow to slowing to 6.7% in 2017. India growth is projected to pick up pace again to 7.0% in 2018 and 7.4% in 2019. Brazil is expected to come out of contraction and grow 0.7% in 2017, accelerate to 1.9% in 2018 and then 2.3% in 2019.

BoE: UK banks could manage disorderly Brexit

BoE's latest stress test results show that "the U.K. banking system could continue to support the real economy through a disorderly Brexit." BoE Governor Mark Carney said in a press conference that "let's be clear, this is a big call … Because we will be here in March 2019 in the unlikely event that we end up in a situation without a transition deal or without an agreement. So we are putting our money where our mouth is." Meanwhile, five of the seven biggest banks tested passed the healthcheck Barclays Pls and Royal Bank of Scotland group fell below their systemic reference point. But actions were taken by both since 2016 year end and no further action is needed.

A Spanish candidate could fill ECB Vice next year

ECB Vice President Vitor Constancio will step down next year. It's reported that the position would probably go to a Spanish candidate. After Jose Manuel Gonzalez Paramo, Spain has not had an ECB Executive Board member since 2012. Spanish Economy Minister Luis de Guindos told newspaper El Economista that "I'm convinced that the position will go to Spain." Meanwhile, de Guindos rubbished the rumor that he will replace Jeroen Dijsselbloem as Eurogroup head.

BoJ Katakoa pushes for additional easing again

BoJ board member Goushi Katakoa was a new comer to the board, and the sole dissenter to last months' decision to stand pat. He called for more easing as "our near-term challenge is to think about how we can achieve our 2 percent inflation target, and whether current steps are enough." He added that "if the global economy is hit by a big shock, there's a risk things won't proceed as projected. Before that happens, we need to ensure we return to a position where have room to take policy action when needed." Also, "we need to avoid a situation where we're forced to continue current monetary policy as inflation fails to reach 2 percent, and gradually hurt Japan's financial system,"

Separately, BoJ Governor Haruhiko Kuroda said that a "reversal rate", the level where central bank rate cuts could hurt the economy, could help BoJ understand the appropriate yield curve shape. This comes in a time where policy makers are considering reform of monetary policies.

On the data front

US trade deficit widened to USD -68.3b in October. Wholesale inventories dropped -0.4% mom in October. Canada RMPI rose 3.8% mom in October while IPPI rose 1.0% mom. German Gfk consumer sentiment was unchanged at 10.7. Import price rose 0.6% mom in October. Eurozone M3 rose 5.0% yoy in October.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9788; (P) 0.9804; (R1) 0.9832; More....

Intraday bias in USD/CHF remains neutral as recovery from 0.9776 temporary low continues. As long as 0.9946 resistance holds, another fall is still expected. Below 0.9776 will extend the decline from 1.0037 to 61.8% retracement of 0.9420 to 1.0037 at 0.9656. We'll look for bottoming again below 0.9656 and above 0.9420. On the upside, break of 0.9946 resistance will indicate that the decline from 1.0037 has completed and bring retest of this resistance.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 07:00 | EUR | German Import Price Index M/M Oct | 0.60% | 0.40% | 0.90% | |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Oct | 5.00% | 5.10% | 5.10% | 5.20% |

| 12:00 | EUR | German GfK Consumer Confidence Dec | 10.7 | 10.7 | 10.7 | |

| 13:30 | USD | Advance Goods Trade Balance Oct | -68.3B | -65.0B | -64.1B | |

| 13:30 | USD | Wholesale Inventories M/M Oct P | -0.40% | 0.40% | 0.30% | 0.10% |

| 13:30 | CAD | Industrial Product Price M/M Oct | 1.00% | 0.50% | -0.30% | |

| 13:30 | CAD | Raw Materials Price Index M/M Oct | 3.80% | 2.00% | -0.10% | -0.20% |

| 14:00 | USD | House Price Index M/M Sep | 0.50% | 0.70% | ||

| 14:00 | USD | S&P/Case-Shiller Composite-20 Y/Y Sep | 6.00% | 5.92% | ||

| 15:00 | USD | Consumer Confidence Index Nov | 124 | 125.9 |

Canadian Dollar Ticks Higher Ahead of Inflation Reports

The Canadian dollar has posted slight gains in the Tuesday session. Currently, USD/CAD is trading at 1.2794, up 0.19% on the day. On the release front, Canada releases two inflation reports, and BoC Governor Stephen Poloz holds a press conference about the Financial System Review. The US will release CB Consumer Confidence, with an estimate of 123.9 points. Fed Chair Designate Jerome Powell will testify at his confirmation hearing before the Senate Banking Committee. On Wednesday, the US publishes Preliminary GDP and Pending Home Sales and Janet Yellen will testify before a congressional committee.

The spotlight is on Jerome Powell, who is replacing Janet Yellen at the helm of the Federal Reserve. Investors will learn a bit more about Powell, who testifies before the Senate Banking Committee on Tuesday for his confirmation hearing. Powell is widely expected to maintain Janet Yellen's cautious monetary stance, which has been marked by small, incremental rate hikes. Powell inherits an economy that is in excellent shape, but persistently low inflation remains a nagging problem. Fed policymakers have differing views on what to do about inflation, with some members proposing that the Fed drop its 2 percent target, in favor of a "gradually rising path" for prices. The Fed remains confounded by low inflation and wage growth, despite a labor market that is at full capacity. Still, the Fed will likely pull the rate trigger next month, and could raise rates up to 3 more times in 2018 if the economy continues to expand at its current pace.

The Canadian dollar remains under pressure, as oil prices have dipped lower. As well, weak retail sales reports for September missed their estimates and this continues to weigh on the currency. Core Retail Sales improved to 0.3%, but this was well off the forecast of 0.9%. Retail Sales came in at 0.1%, compared to an estimate of 0.9%. Investors will be keenly following the Bank of Canada, which releases its semi-annual Financial System Review.

CAC Rebounds as German Political Crisis Eases

The CAC has bounced back after starting the week with losses. In the Tuesday session, the CAC is at 5387.25 up 0.51% on the day. On the release front, there are no major eurozone events on the calendar. Later in the day, Fed Chair Designate Jerome Powell will testify at his confirmation hearing before the Senate Banking Committee. On Wednesday, France releases Consumer Spending and Preliminary GDP. The US will also publish Preliminary GDP and Janet Yellen will testify before a congressional committee.

European stock markets are in green territory on Tuesday, as German coalition talks have been revived, after collapsing last week. The SPD (socialist democrats), a junior partner in the last government, have agreed to hold coalition talks with Angela Merkel's CDU. The SPD is expected to demand a bigger role in a new government if it agrees to a "grand" coalition. Talks between the CDU, the Greens and the Free Democrats imploded when the Free Democrats bolted, saying there was not enough common ground to continue talks. Merkel is reluctant to run a weak minority government, and if talks with the SPD don't make progress, the likely result would be another election. For its part SPD lawmakers are split on whether to join up with the CDU, but Merkel may choose to make her former coalition partner an offer it can't refuse, such as the powerful finance ministry.

All eyes will be on Jerome Powell, who testifies before the Senate Banking Committee on Tuesday for his confirmation hearing. Will Powell be a clone of outgoing chair Janet Yellen? Powell inherits an economy that is in excellent shape, but persistently low inflation remains a nagging problem. Fed policymakers have differing views on what to do about inflation, with some members proposing that the Fed drop its 2 percent target, in favor of a "gradually rising path" for prices. The Fed remains confounded by low inflation and wage growth, despite a labor market that is at full capacity. Still, the Fed will likely pull the rate trigger next month, and could raise rates up to 3 more times in 2018 if the economy continues to expand at its current pace.

USDJPY Turning Bullish Above 111.34 Level

The U.S dollar is starting to recover upside momentum against the Japanese yen, as the U.S dollar index bounces from its recent trading lows. Despite the risk-off trading sentiment continuing through Asia the USDJPY pair is starting to attack the 111.34 resistance level once more. Traders now look to a key-note speech from incoming Federal Reserve Chair Jerome Powell, and U.S Consumer Confidence data for the month of November.

Should price action hold above the 111.34 technical level, intraday buyers may look to test the 111.72 level again, with a possible deeper retrace towards 112.20 level..

If USDJPY buyers fail to hold the 111.34 level again, a continuation of the down-move towards 110.90 and 110.60 seems most likely.

GBPUSD Turning Bearish Below 1.3307

The British pound has fallen against the U.S dollar, hitting 1.3290, after BOE Governor Mark Carney warned of the possible shocks the UK economy faces after leaving the European Union. GBPUSD still remains below the key 1.3307 level, with price-action currently holding slightly above the 1.3300 level and hourly momentum pointing down. The pair is likely to remain volatile heading into the U.S trading session, as we see the release of high-impact data from the U.S economy, and a host of Federal Reserve members speaking.

The GBPUSD pair remains intraday bearish while trading below the key 1.3307 level. Further downside towards the 1.3268 level appears likely, with extended weekly support found at 1.3230.

Should price-action on the GBPUSD pair start to move back above 1.3307 technical level, buyers will likely push the pair towards the 1.3360 resistance level.

Fed’s Powell Speech Eyed, Bitcoin Nears New Milestone

- Powell Testimony Eyed For Fed Direction Clues;

- UK Banks Pass Stress Tests But OECD Revises 2017 Growth Lower;

- Bitcoin Closes in on New Milestone as Frenzy Continues.

US equity markets are expected to open slightly higher on Tuesday following a flat and rather slow start to the week.

Federal Reserve Chair-designate Jerome Powell will testify on his nomination before the Senate Banking Committee on Tuesday and his comments will be monitored closely for clues on the direction he plans to take the central bank under his leadership. Based on the comments released overnight, it would appear Powell intends to send a message of continuity which means rate hikes will proceed, or intend to, as has been laid out already.

The regulatory component of his testimony may be of more interest though, with some seeing his appointment as a push towards looser regulation, something that has been a key feature of Trump’s first year in office and likely a big part of Powell’s nomination. In his prepared remarks Powell referenced a desire to consider ways of easing regulatory burdens although, likely in a bid to appease those concerned, he also stressed the need to preserve core reforms. I imagine he will be questioned heavily on these views. William Dudley and Patrick Harker will also appear today.

A rare piece of good news for the UK this morning as the Bank of England announced that all banks passed its stress tests for the first time since the financial crisis. While the tests didn’t test for Brexit scenarios specifically, they did suggest that banks are equipped to deal with a disorderly exit due to severity of the scenarios that were tested, which encompassed a range associated with it.

The OECD did add a small dose of negativity to the mix though, revising its growth forecast for the UK to 1.5% this year, down from 1.6%, although that was accompanied by a revision higher for 2018, to 1.2% from 1%. While the net revision may be positive, it’s hard to ignore the fact that this still means we’re headed for a period of slowing growth at a time when other countries prospects are looking much brighter, which was also reflected in the OECD’s latest forecasts.

The Bitcoin frenzy continues on Tuesday, with the cryptocurrency set to reach yet another milestone as it closes in on $10,000. While you can’t ignore the fundamental factors supporting the rise of Bitcoin – the latest being CME Group’s decision to launch Bitcoin futures – a 900% increase since the start of the year and the frenzy that’s formed around it does suggest there’s a large speculative force at play here.

While there’s no reason that can’t continue, nor anything to suggest it is overvalued in the long term, I do worry that it is vulnerable to further sharp and painful corrections, possibly more severe than anything we’ve seen since the start of the year. It will be very interesting to see how Bitcoin traders respond the closer we get to $10,000. Any severe corrections that may come in the future will also be a major test of speculators continued desire for such risk.