Sample Category Title

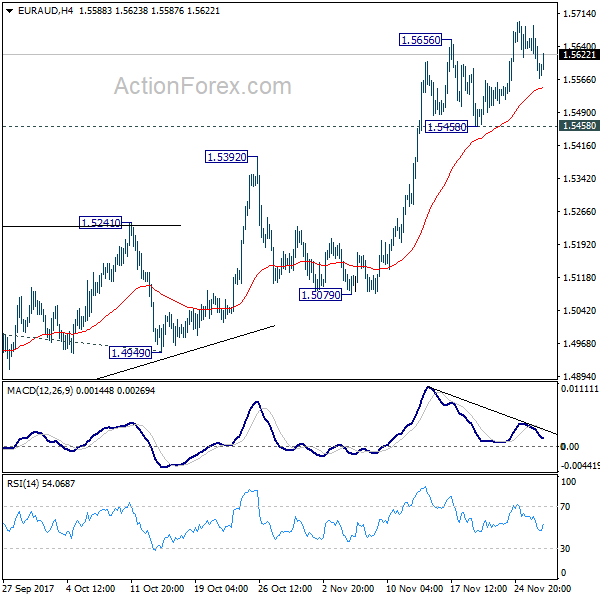

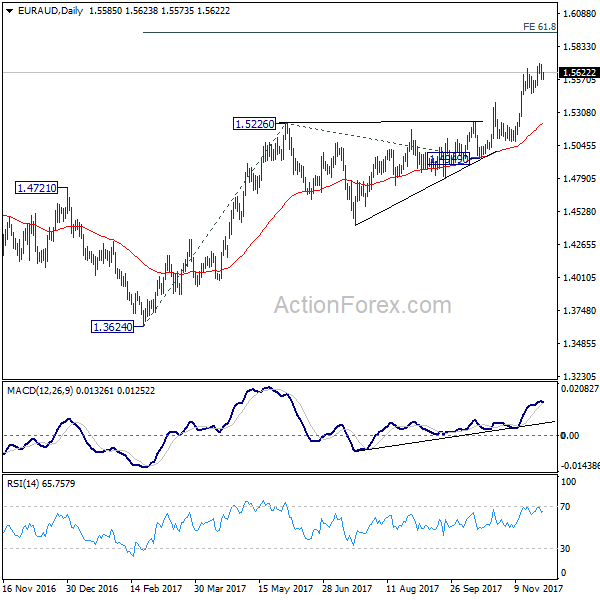

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5543; (P) 1.5616; (R1) 1.5663; More....

Near term outlook in EUR/AUD will remain bullish as long as 1.5458 support holds. Medium term rise from 1.3624 should target 61.8% projection of 1.3624 to 1.5226 from 1.4949 at 1.5939 first. Break will target 100% projection at 1.6551, which is close to 1.6587 key resistance. However, firm break of 1.5458 will now indicate near term topping and should bring pull back towards 55 day EMA (now at 1.5232).

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top (2015 high) has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. We'll hold on to this bullish view as long as 1.5226 resistance turned support holds. Firm break of 1.6587 will resume long term rise from 1.1602 (2012 low).

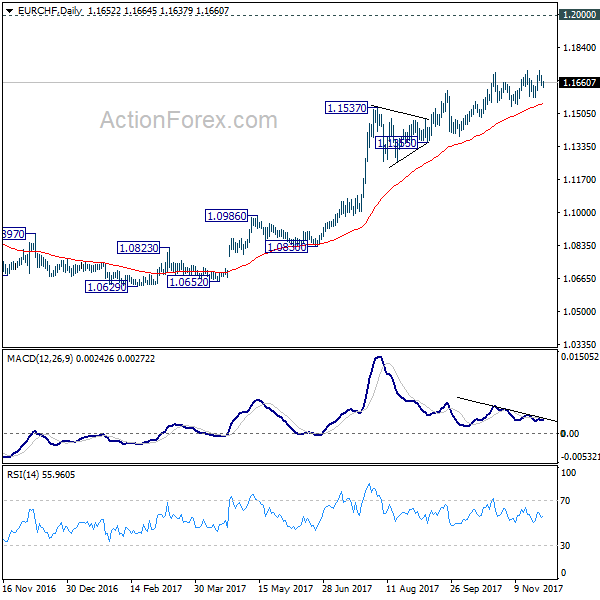

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1630; (P) 1.1665; (R1) 1.1684; More...

Near term outlook in EUR/CHF stays bullish as long as 1.1584 support holds. Current medium term rise from 1.0629 would extend to 1.2 key level. However, considering bearish divergence condition in 4 hour MACD, firm break of 1.1584 will now indicate near term reversal and should bring pull back to 1.1355 support or below.

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1355 support holds. However, break of 1.1355 will indicate medium term topping. In that case, EUR/CHF should head back to 55 week EMA (now at 1.1142) and possibly below.

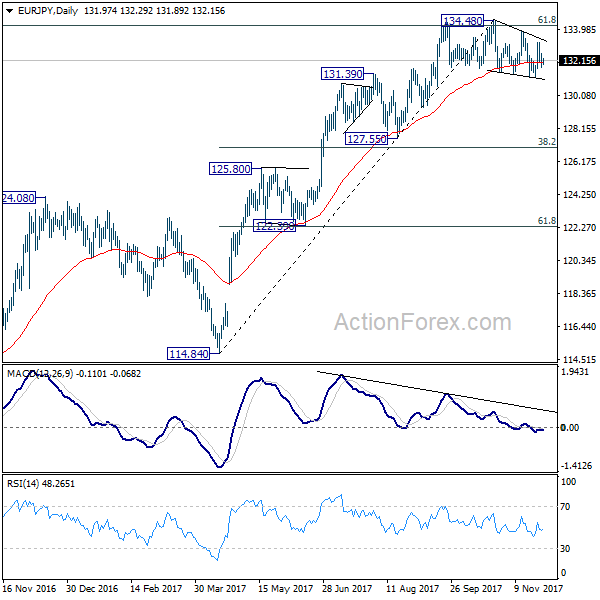

EUR/JPY Daily Outlook

Daily Pivots: (S1) 131.63; (P) 132.09; (R1) 132.47; More....

Intraday bias in EUR/JPY remains neutral corrective pattern from 134.48 is still unfolding. As long as 134.48 key resistance holds, risk remains on the downside for deeper pull back. Break of 131.16 will target 38.2% retracement of 114.84 to 134.48 at 126.97, which is close to 127.55 support. We'll look for support from there to bring rebound on first attempt.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). 61.8% retracement of 149.76 to 109.03 at 134.20 is already met. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. However, break of 127.55 support will argue that the medium term trend has reversed and will turn outlook bearish for deeper fall back to 114.84/124.08 support zone at least.

Market Morning Briefing: Euro Has Seen A Hold Of The Resistance At 1.19

STOCKS

Dow (23836.71, +1.09%) has risen sharply finally trading above our target levels of 23800. Resistance is visible near current levels which if holds, may push the index back towards 23500; else a break above 23850 if seen could take it higher towards 24000, opening up further upside for the near to medium term. Note that although immediate resistance is visible on the candle charts, the 3-day line charts indicates an upside room towards 24000-24500 which would be our next target on a break above 23850/900 levels.

Dax (13059.53, +0.46%) is trading within the 13200-12900 region and this may continue for a few more sessions. The current sideways consolidation may be a temporary base building phase which could possibly lead to a sharp break above 13200 in the medium term. While above 12900, Dax remains bullish for the medium term.

Nikkei (22576.86, +0.40%) is stable as usual below 22760 and could trade in the 22760-22250 region for some time. A break on either side is necessary to have more clarity on further direction. For now Nikkei is likely to remain range-bound. Near term resistance near 112.00-111.65 if holds and pushes back Dollar Yen towards 111-110 in the medium term could possibly lead to a fall in Nikkei too. But for now that remains unclear.

Shanghai (3314.51, -0.57%) recovered a bit yesterday to close above 3320 but is again attempting lower levels today. Looking at the downside momentum, a fall towards 3300 and lower is more likely in the near term.

Nifty (10370.25, -0.28%) could be stable within 10450-10300 region for a few sessions. A corrective fall towards 10300-10200 is preferred while below 10500. Only on a break above 10500, we would focus on further upside.

Sensex (33618.59, -0.31%) however looks more bullish than Nifty just now. A break above 33750 could take it higher towards 34000 in the near term.

COMMODITIES

Gold (1295.60) has room on the upside and could rise towards 1320 in the near term while Silver (16.86) has broken below immediate support and could move down to 16.75-16.60 in the near term.

Brent (63.24) is trading at slightly lower levels today and could test 62.50-62.00 before again bouncing back. Overall long term looks bullish towards 65.

WTI (57.67) has immediate support at 57 and could possible see a bounce from there back to levels near 59-60. Failure to sustain above 57 would take it lower towards 56-55 before producing an upmove.

Copper (3.1080) could be moving lower on weak Chinese stocks but is trading at support levels just now. A rise from 3.10-3.08 is needed to take it higher again towards 3.15-3.20. Near to medium term looks bullish. Only on a break below 3.05, our lower target of 2.95 would come into picture.

FOREX

Dollar-Index (93.221) seems to have had a definitive bounce from support near 92.50-92.70 with three days of continuous rise in levels. The markets have thus shrugged off the possibility of further immediate dollar weakness and we could see the index trading between a range of 92.25 to 93.75 in the next two weeks. A more concrete view on whether Dollar will see a sustained phase of strength or weakness would depend on the index breaching resistance around 93.5 or support around 92.25-92.50 respectively in the next week or two.

Euro (1.1851) has seen a hold of the resistance at 1.19 on the weekly line charts and is now likely to move further down in the near term towards support near 1.1825 on the daily candles, a break of which could further pull it down to test support near 1.1775 on the weekly candle chart. However, it would be prudent to wait and watch if Euro goes below 1.1775 or rebounds above 1.19, before commenting on the sustainability of its weakness or strength.

Dollar-Yen (111.42) has also moved up with the weakening of dollar seeing a halt. As predicted in our briefing on Monday, this slight rebound of the Yen has created a new support for it on the daily candles at 111.25. It could well oscillate between resistance around 111.75-112.00 and support at 111.25 in the next few sessions, before a more concrete market view on dollar strength moves it above or below that range.

Pound (1.3368) contrary to our expectations has breached resistance on daily charts at around 1.335 and now seems to be poised for an upmove towards 1.34-1.3415 levels, from where there could be a slight corrective dip.

Dollar Rupee (64.4150) is likely to find support in the 64.40/30 region from where a bounce back to levels near 64.50/60 is possible. Some strength in the US Dollar could possible keep Rupee stable today with an intra-day high of 64.30.

INTEREST RATES

After moving up slightly to 0.72% the day before, the US 30-5 Yr Spread (0.69%) has dipped again a bit, but remains above the crucial channel Support which could push it up towards 0.75%, if not higher.

There has not been much movement in US Yields yesterday, but the chances of a rise remain valid while the 5Yr (2.07%), 10Yr (2.33%) and 30Yr (2.76%) remain above Supports seen near current levels.

In comparison, the German 2Yr (-0.71%) and 5Yr (0.34%) could be reasserting their overall downtrend. The German-US 10Yr Spread (-1.99%) has also started dipping a bit and may try to test -2.03% over the next week or two.

The long-term trend Resistance on the Japan 10Yr (0.03%) has held, pushing the yield lower from levels of 0.039% and 0.036% seen earlier this week. If it falls further, it could end up weakening the Yen.

As we mentioned yesterday, it will be interesting to see if the US Q3 GDP will come in near/ higher/ lower than the market expectation of 3.30% tomorrow.

As expected, the Indian 10Yr GOI (7.03%) has come off a bit from just below 7.10% and may get into a sideways range of 6.90-7.10% for some days.

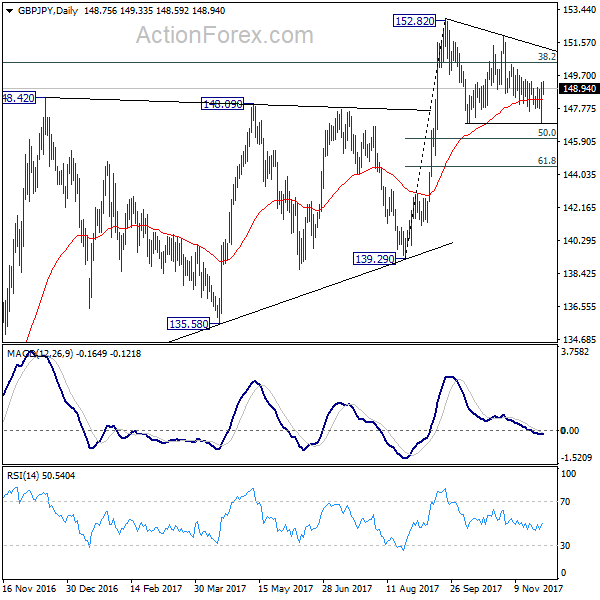

GBP/JPY Daily Outlook

Daily Pivots: (S1) 147.35; (P) 148.31; (R1) 149.65; More...

Outlook in GBP/JPY is unchanged that price actions from 152.82 are forming a corrective pattern. On the upside, above 149.45 will turn bias to the upside for 151.92 resistance first. Break there will likely resume rise from 139.29 through 152.82 high. On the downside, below 146.96 will bring deeper fall. But now, we'd expect downside to be contained by 50% retracement of 139.29 to 152.82 at 146.05 to bring up trend resumption eventually.

In the bigger picture, medium term rebound from 122.36 is still expected to resume after corrective pull back from 152.82 completes. Firm break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. However, break of 139.29 will indicate rejection from 150.43 key fibonacci level. And the three wave corrective structure of rebound from 122.36 will argue that larger down trend is resuming for a new low below 122.26.

US Stocks Surged to Records as Tax Plan Moved Another Step, Sterling Boosted by Reports of Brexit Bill

US equities staged a strong rally overnight. Investors were happy that another step was taken with the Republican's tax plan. Senate version was approved by the Budget Committee, paving the way for a floor vote on Thursday. Also, Fed chair nominee Jerome Powell commented that current banking regulations are "tough enough". And there could even be some easing also lifted sentiments. DOW closed up 255.93 pts or 1.09% at 23826.71. S&P 500 gained 25.62 pts or 0.98% at 2627.04. NASDAQ also rose 33.84 pts or 0.49% to 6912.36. All three indices closed at record highs. Dollar rebounded broadly but was overwhelmed by Sterling. The Pound was given a strong boost on reports that UK and EU have agreed on the divorce bill.

Fed Powell: Banking regulations tough enough already

Fed Chair nominee Jerome Powell's confirmation hearing brought little new to the markets. Basically, Powell indicated that "the case for raising interest rates at our next meeting is coming together." He didn't sound too concerned with slow inflation in the US and expected inflation to rise as the economy nears full employment. Regarding banking regulations, Powell indicated they are "tough enough" for now. And he expressed the intention to "consider appropriate ways to ease regulatory burdens while preserving core reforms".

Minneapolis Fed President Neel Kashkari sounded cautious again in his speech yesterday. He said that "because inflation is low, I am seeing no reason to tap the brakes on the economy." He added that "my perspective is, let's allow the job market to continue to strengthen, allow more Americans to go back to work, allow wages to strengthen, and then, if we start to see inflation creep back up to our 2-percent target, we can tap the brakes then." Kashkari dissented both of Fed's hikes this year. His comments suggested that he's going to dissent again in December.

Sterling jumped as UK and EU agreed on divorce bill

Sterling rebounds broadly and stays firm on multiple reports that an agreement was reached between UK and EU on the divorce bill, clearing an important hurdle to move on to trade talks. The Daily Telegraph reported that EU's request for EUR 60b was agreed in principle. There would be further detailed interpretations and the final amount could range between EUR 45b and EUR 55b. The Financial Times reported that EU liabilities could sum up to EUR 100b but net payments over the decades could add up to half the amount. UK's Brexit Ministry just said that there were "intensive talks" and both sides were finding ways to "build on recent momentum". European Commission declined to comment. But the news raised hope that there would finally be "sufficient progress" made before EU summit on December 14/15 to move on to trade negotiations.

BoC Poloz named housing as big risks

Bank of Canada Governor Stephen Poloz said that "our financial system continues to be resilient, and is being bolstered by stronger growth and job creation". But he also emphasized the need to "continue to watch financial vulnerabilities closely." The central bank pointed out, in the latest financial system review, risks of historic levels of household debts. And, more than 80% of the debts is on mortgages and home equities credit lines. Poloz warned that "these vulnerabilities continue to be elevated and it will take a long time for them to return to more sustainable levels."

RBNZ to unwind home loan restrictions

RBNZ indicates today that it would to unwind some restrictions on home loans. The loan-to-value ratio restrictions could be modestly eased starting January 1 next year. Governor Grant Spencer said that "over the past six months, pressures in the housing market have continued to moderate due to the tightening of LVR restrictions in October 2016." And, "the market has been coming off really since mid-last year and so we have been considering it particularly as Auckland was flattening out and indeed going negative." Also, "housing market policies announced by the government are also expected to have a dampening effect on the housing market."

North Korea close to striking anywhere in US mainland

North Korea launched an intercontinental ballistic missile which flew for 53 minutes over 960km and reached an altitude of more than 4000km. US Secretary of Defense James Mattis said that it's the highest reaching missile ever. And it's believed that North Korea is now close to being able to strike anywhere in the mainland US. South Korea President Moon Jae-in called for dialogue and urged to "prevent a situation where North Korea threatens us with its nuclear arsenal based on misjudgment or the US. considers a preemptive strike." The news was shrugged off by the markets though.

On the data front

Japan retail sales rose 0.8% yoy in October. UK BRC shop price dropped -0.1% yoy in November. Germany CPI will be the main feature in European session. Eurozone will release confidence indicators and French GDP. UK will release mortgage approvals and M4. Swiss will release UBS consumption indicators. Later in the day, US will release Q2 GDP revisions, pending home sales and Fed's Beige Book. Fed Chair Janet Yellen will also have her last Congressional testimony.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 147.35; (P) 148.31; (R1) 149.65; More...

Outlook in GBP/JPY is unchanged that price actions from 152.82 are forming a corrective pattern. On the upside, above 149.45 will turn bias to the upside for 151.92 resistance first. Break there will likely resume rise from 139.29 through 152.82 high. On the downside, below 146.96 will bring deeper fall. But now, we'd expect downside to be contained by 50% retracement of 139.29 to 152.82 at 146.05 to bring up trend resumption eventually.

In the bigger picture, medium term rebound from 122.36 is still expected to resume after corrective pull back from 152.82 completes. Firm break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. However, break of 139.29 will indicate rejection from 150.43 key fibonacci level. And the three wave corrective structure of rebound from 122.36 will argue that larger down trend is resuming for a new low below 122.26.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Retail Trade Y/Y Oct | 0.80% | 0.00% | 2.20% | |

| 00:01 | GBP | BRC Shop Price Index Y/Y Nov | -0.10% | -0.10% | ||

| 07:00 | CHF | UBS Consumption Indicator Oct | 1.56 | |||

| 07:45 | EUR | French GDP Q/Q Q3 P | 0.50% | 0.50% | ||

| 09:30 | GBP | Mortgage Approvals Oct | 65K | 66K | ||

| 09:30 | GBP | M4 Money Supply M/M Oct | 0.30% | -0.20% | ||

| 10:00 | EUR | Eurozone Business Climate Indicator Nov | 1.51 | 1.44 | ||

| 10:00 | EUR | Eurozone Economic Confidence Nov | 114.6 | 114 | ||

| 10:00 | EUR | Eurozone Industrial Confidence Nov | 8.6 | 7.9 | ||

| 10:00 | EUR | Eurozone Services Confidence Nov | 16.7 | 16.2 | ||

| 10:00 | EUR | Eurozone Consumer Confidence Nov F | 0.1 | 0.1 | ||

| 13:00 | EUR | German CPI M/M Nov P | 0.30% | 0.00% | ||

| 13:00 | EUR | German CPI Y/Y Nov P | 1.70% | 1.60% | ||

| 13:30 | USD | GDP Annualized Q/Q Q3 S | 3.20% | 3.00% | ||

| 13:30 | USD | GDP Price Index Q3 S | 2.20% | 2.20% | ||

| 15:00 | USD | Pending Home Sales M/M Oct | 1.20% | 0.00% | ||

| 15:30 | USD | Crude Oil Inventories | -1.9M | |||

| 19:00 | USD | Federal Reserve Beige Book |

Indecision Candle At AUD/NZD Daily Support

With Monday's AUD/USD and yesterday's USD/CAD setups playing out nicely, I wanted to speak about the AUD/NZD short setup that we had previously featured. A level that didn't hold and the setup was blown out of the water by a fundamental news spike.

Take a look at the chart below in comparison to September's blog. The zone broke to the upside pretty convincingly, but as you can now see, price is back retesting it again from the other side.

AUD/NZD Daily:

It's not just the level that's interesting, but it's the price action inside it. The last daily candle that's low touches the bottom of the marked zone is a pretty juicy indecision candle. The fact that it's inside the support zone and the bottom touched the exact bottom gives it more stead in my opinion.

Now zoom into an intraday chart and take a look at the price action on for example the 15 minute chart such as below.

AUD/NZD 15 Minute:

You can really see the buyers coming in at the bottom of the zone with that huge wick late in the trading session.

Let's see if it can break and hold back above it now. Remember that for now, it's just a daily indecision candle rather than a reversal.

Won Heck of a Story Unfolding in Asia FX

After a relatively uninspiring Asia session yesterday, equity markets returned to recent form overnight after the Senate Budget Committees stamped their approval on the Senates tax plan.

Also Financial's hit a high note during Jerome Powell's testimony to the Senate Banking Committee when his comments regarding "easing regulatory burdens while preserving core reforms." put a huge smile on Wall Street Bankers faces and an even broader one on their shareholders.

Initially, the dollar moved higher lifted by higher US yields after Senate Budget Committee signed off the bill to move to the Senate floor for a final vote. But with Powell towing the current Fed's dovish narrative of gradual rate hikes in his earlier Senate confirmation the dollar edge dulled quickly against most G-10, but USDJPY remained buoyant on improving risk sentiment.

The festivities were briefly interrupted after the US Pentagon confirmed that an NK missile launch was "probable," made around 13:30 EST. But unlike the previous North Korea missile tests, investors haven't sounded any alarm bells and in fact, quickly faded the initial knee-jerk.

The British Pound

Sterling is being lashed around on the latest Brexit headlines. The Pound ripped higher after a deal over the soi-disant 'Brexit bill' which includes a purported EUR60bn financial settlement according to sources on both sides was agreed on balance. This headline is fantastically positive news for the beleaguered pound which was sold early in the day after Bank of England governor Mark Carney's depressing warning of potential Brexit fallout. While Carney candid talks my hold true, the financial settlement should pave the way to possible breakthrough in negotiations in December overcoming investors biggest fears, a hard Brexit

The New Zealand Dollar

The Kiwi moved higher in early trade on an unexpected decision from the RBNZ to ease its LVR restrictions. The move proved to be short-lived and was quickly sold given the tacitly backed stronger USD dollar narrative this morning

The Euro

The Euro failed to break convincingly higher on Monday or Tuesday, and that alone would have caused traders to unwind some overextend long EUR positioning. But the single currency got caught up in headline wash after Brixit positive news caused EURGBP to crater, and then Ireland's deputy PM Frances Fitzgerald is reported facing calls to resign over a controversy involving a police whistleblower. Mind you, the Irish edition of EU political risk should be inconsequential to the Euro as have all the other politically inspired moves. But last nights sell-off is as much about Traders getting nervous about the crowded trade mentality in less than ideal liquidity conditions and cutting quickly when the trade set up goes sideways.

The Japanese Yen

Its been a real chop feast this week as the market digests noise about BoJ normalisation, US Tax Reform, month-end rebalancing and of course, the North Korea threat. It makes for difficult trading conditions, however, buying the USDJPY dip still looks attractive on the positive risk outcome from US tax reform.

The Australian Dollar

In listless trade, the Aussie dollar is slightly lower as the currency remains range bound amidst the market's competing priorities.

Indeed all the talk about China destabilising markets into year end is not helping sentiment as the Aussie would be the go-to G-10 hedge against China market fallout.

The Chinese Yuan before the Fix

Month end and year end USD demands are creeping into the picture keeping a floor under the USDCNH. Not much early action despite the moves other regional pairs so I suspect the latest equity market bobble and bond market sell-off is too fresh in traders minds to take on more Yuan risk.

Energy Market

Oil traders remain incredibly jittery ahead of Thursday's OPEC meeting. And while we can never be sure what's evolving behind closed doors, market whispers suggest Saudi Arabia and Russia are not yet fully coordinated which indicates the balance of risks remain skewed lower.

The Korean Won

The market woke up when London walked in eager to buy Asia FX. The move was briefly interrupted by news that North Korea has tested another missile.But the KRW reaction is very very telling as USDKRW NDF barley moved from 1082.70 to 1084.50 before USD offers returned as geopolitically risk desensitised investors view little chance of escalation and are using these opportunities to add risk.

On the broader KRW rally that began in earnest in London, some were attributing the move to Yonhap News Agency reports that China has eased the ban on group tour packages bound for South Korea which was put in place after the deployment of the THAAD missile system. But the move has more to do with the grand exit of long USD geopolitical risk hedges ahead of Thursday BoK interest rate decision

Traders will be on the edge of their seat awaiting the BoK rate hike and more specifically what tone the governor will take. There's a high chance for dovish interest hike expressed during the press conference to slow down the pace of the Won appreciation.

The Malaysian Ringgit

The Market continues to express its bullish Asia FX views through the Ringgit which rallied yesterday in tandem with regional peers.

The Yellen-Esq dulcet dovish tones from incoming Fed Chair Jerome Powell portend well for the Ringgit. And while the USD, more so USDJPY, could bounce higher on a favourable tax reform improving global risk sentiment, the bounce in global equity markets should play favourably in the region and offset higher USDJPY

The Indian Rupee

A strong showing for the Rupee yesterday bolstered by investment inflow.The dovish Fed rhetoric play's well for the Ruppe and looks very favourable after breaking through 64.50 level. Sentiment remains a guardedly optimistic on the Rupee in conjunction with other Asain pairs. However, given the Rupee susceptibility to rising oil prices, suspect traders will be less inclined to push USDINR lower until after OPEC clears the airwaves.

Bank of Canada Sees Elevated Risks, But Things are Moving in the Right Direction

The Bank of Canada released the latest edition of its biannual Financial System Review this morning, laying out an updated view of the main risks facing Canada's financial system. Household indebtedness and housing market imbalances once again took center stage. However, robust economic growth and tightened mortgage rules are seen as factors that should mitigate these vulnerabilities over time. The vulnerability of the Canadian financial system to cyber-attacks was also highlighted as a risk.

On the topic of household indebtedness, the Bank noted that credit growth continues to outpace income growth, largely due to mortgage and HELOC activity. Encouragingly, the share of mortgage originations going to highly-indebted, high-ratio borrowers has declined notably, likely due to mortgage stress test rules implemented last year. However, there are signs that risks may have shifted towards low-ratio borrowers. They account for about 9 in 10 new mortgages in Toronto and Vancouver, with the share of both borrowers that are highly indebted and those with amortizations of more than 25 years trending up, pointing to heightened risk.

The newest mortgage underwriting guidelines from OSFI are meant to address this risk, but the Bank of Canada sees uncertainty around the effectiveness, noting that around 17% of outstanding uninsured mortgages are held by credit unions that are not regulated by OSFI and therefore not subject to the new guidelines. As such, there remains the possibility that high risk borrower activity shifts away from the more heavily regulated areas of the financial system. However, the extent of migration may be limited by the relatively smaller lending capacity available. On balance, the new guidelines are seen as broadly supportive of overall credit quality, although the large stock of outstanding debt means it will take some time for the overall vulnerability to be reduced.

On a related note, the Bank highlighted the vulnerability stemming from imbalances in Canadian housing markets. The report notes that as Toronto has undergone an adjustment over the summer months, home price growth elsewhere has remained steady, with healthy growth in Vancouver and nascent signs of a recovery in Alberta. This has served to reduce the differences in regional home price growth. Policy measures, including changes to underwriting standards are expected to continue to reduce demand and thus price growth, particularly in the high growth markets of Toronto and Vancouver. The Bank also noted that some localized measures, such as foreign buyer taxes in specific regions may have only a limited impact, and may be pushing demand to other cities.

Cyber threats have always been a risk to the financial system, but the growing interconnectedness of the system means that the impacts can be more significant, with a successful attack against one institution potentially spreading more widely. The Bank is working with financial institutions to increase resiliency and put recovery plans in place.

Other vulnerabilities discussed include brokered deposits at monoline lenders, with the experience at Home Capital Group earlier this year demonstrating the risk of rapid funding withdrawal. Risk taking, in a general sense, is being incentivized by low interest rates and low market volatility, leading to the use of higher leverage and rising risk profiles among investors. Finally, high corporate indebtedness was noted – corporate debt relative to GDP is at historic highs, although firms appear to have adequate cash buffers at present.

Key Implications

Canada's financial system may be facing a number of key vulnerabilities, but the Bank of Canada sees things moving in the right direction. For both high household indebtedness and housing market imbalances, changes to underwriting standards and rising interest rates are having, or are expected to have, the desired effect. The report noted that past changes to standards for borrowers with low down payments had something of a balloon-squeezing impact, pushing some risk into high down payment lending, but this should be at least partially mitigated by expanded mortgage stress-testing requirements in the new year.

More fundamentally, rising borrowing costs, which impact all sectors of the market, should work to slow activity. The Bank noted that five-year fixed mortgage rates are up 70 basis points since June, bringing them in line with levels seen five years ago. At the same time an improved economic backdrop, including robust employment growth, is seen as also working to reduce vulnerabilities through time.

In light of the sizeable stock of debt outstanding, it will be some time before these factors work their way through the market, with these vulnerabilities not going away any time soon. However, the Bank sees things as moving in the right direction – towards reduced financial sector risk – a scenario consistent with continued gradual tightening of monetary policy in 2018.

BoC Says Financial System Risks Still Elevated But Sees Signs of Improvement

Our Take:

Thanks to a growing economy and changes in housing regulation, the Bank of Canada sounded a bit more sanguine on risks facing the financial system. Today's semi-annual Financial System Review noted that key vulnerabilities related to household debt and housing market imbalances remain elevated, but in contrast to prior reports, haven't necessarily increased over the last six months.

The bank has emphasized that the economy will be more sensitive to higher interest rates than in the past due to elevated household debt levels. Today's report provided little new insight on that interaction, so it's tough to draw implications for monetary policy. But we think it's worth remembering what Governor Poloz said around the time of the June FSR: with the economic backdrop having improved, monetary policy and financial stability goals are less at odds with one another. Higher interest rates will both keep the economy from overheating and help address key vulnerabilities. So while the bank will likely raise rates more gradually than they otherwise would, household indebtedness isn't necessarily an impediment to tightening monetary policy.