Sample Category Title

GBPUSD Maintains Positive Outlook Above 1.30

GBPUSD is pivoting around its 50-day moving average, remaining mostly neutral for now, with risk tilted to the upside.

The corrective move of the uptrend to 1.3656 appears to have stabilized above the key 1.3000 level after the sell-off from September 20 to October 6 has turned into a consolidation phase.

The outlook is positive since the market has held above 1.3000 and has also crossed above its 50-day MA. Prices have broken above what was a key resistance level at the 50% Fibonacci retracement (1.3215) of the upleg from 1.2773 to 1.3656.

GBPUSD is now testing the 38.2% Fibonacci (1.3317). The RSI indicator is neutral for now but above 50 in bullish territory, suggesting a break higher is possible. A daily close above 1.3350 would confirm the short-term bullish phase to target 1.3448 (23.6% Fibonacci) followed by 1.3500. From here prices would target 1.3600 and see a re-test of the 1.3656 peak for a resumption of the medium-term uptrend.

The underlying trend higher is considered to be intact as long as the market remains above 1.3000. However, the sideways range that followed the drop from 1.3656 is expected to continue unless there is a sustained rally through the mid-1.3500 area.

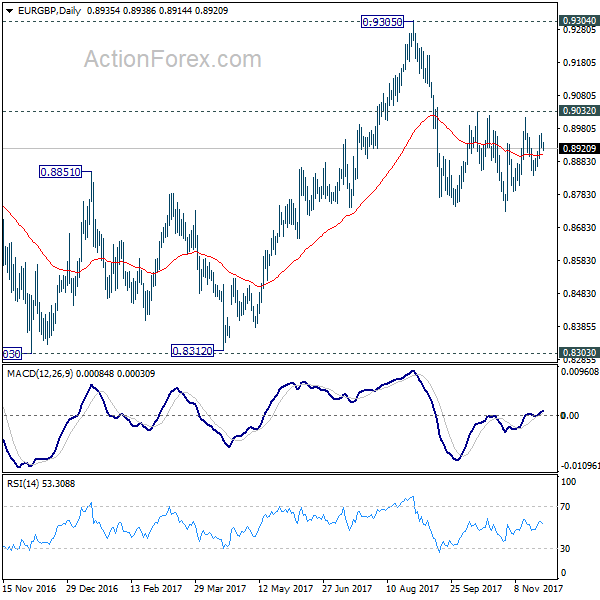

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8915; (P) 0.8941; (R1) 0.8957; More...

EUR/GBP is still bounded in range of 0.8732/9032 and intraday bias remains neutral. With 0.9032 resistance intact, deeper decline is mildly in favor in the cross. Break of 0.8732 will resume the fall from 0.9305 and target 0.8303 key support level. However, on the upside, decisive break of 0.9032 will confirm completion of the decline from 0.9305. In such case, intraday bias will be turned back to the upside for retesting 0.9305 key resistance.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5611; (P) 1.5653; (R1) 1.5692; More....

No change in EUR/AUD's outlook. Intraday bias stays on the upside. Medium term rise from 1.3624 should target 61.8% projection of 1.3624 to 1.5226 from 1.4949 at 1.5939 first. Break will target 100% projection at 1.6551, which is close to 1.6587 key resistance. On the downside, break of 1.5458 support is needed to indicate short term topping. Otherwise, outlook will remains bullish in case of retreat.

In the bigger picture, we're holding on to the view that corrective decline from 1.6587 medium term top (2015 high) has completed at 1.3624. Rise from 1.3624 is expected to extend to retest 1.6587. We'll hold on to this bullish view as long as 1.5226 resistance turned support holds. Firm break of 1.6587 will resume long term rise from 1.1602 (2012 low).

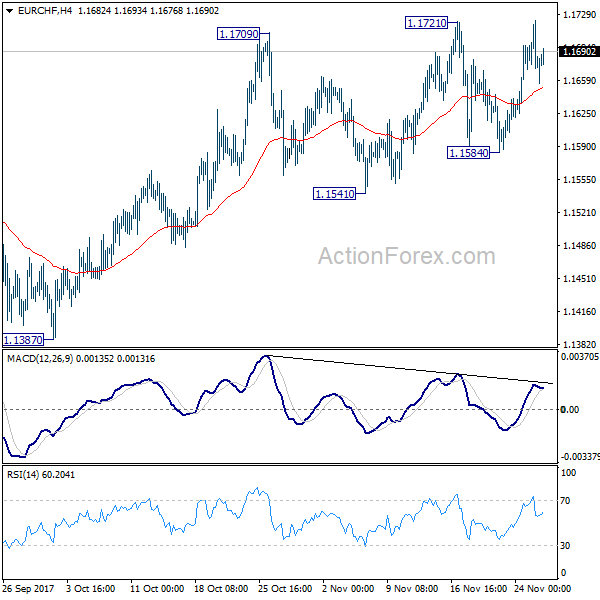

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1661; (P) 1.1691; (R1) 1.1711; More...

Upside momentum in EUR/CHF remains unconvincing with bearish divergence condition in 4 hour MACD. But outlook stays bullish as long as 1.1584 support holds. Medium term rise from 1.0629 should extend to 1.2 key level. However, firm break of 1.1584 will now indicate near term reversal and should bring pull back to 1.1355 support or below.

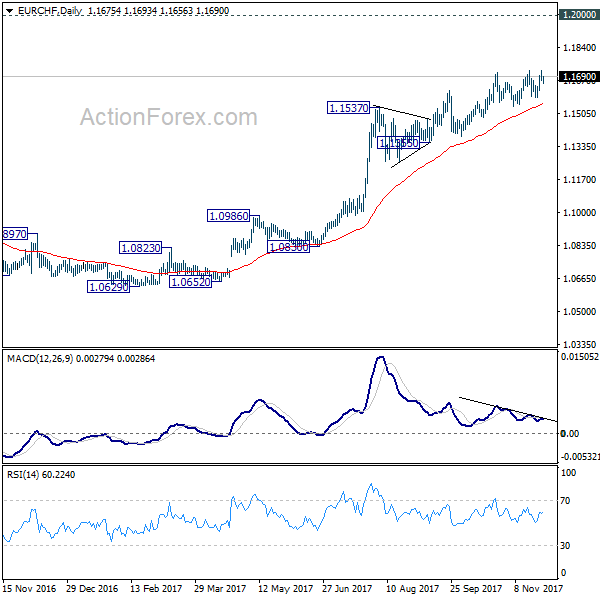

In the bigger picture, long term rise from SNB spike low back in 2015 is still in progress. EUR/CHF should now be heading back to prior SNB imposed floor at 1.2000. For now, this will be the favored case as long as 1.1355 support holds. However, break of 1.1355 will indicate medium term topping. In that case, EUR/CHF should head back to 55 week EMA (now at 1.1142) and possibly below.

Forex: USD Languishes

USD continues to languish at 8-week lows against many of its peers, as the markets are concerned over possible delays to the US Tax Reform Plan. Senator John Cornyn, the Senate Republicans’ whip, said on Monday “Hopefully we will get to the floor on Wednesday.” Asked to clarify if he meant the vote to proceed will be Wednesday, he said yes. The expectation is that Senate Majority Leader McConnell will bring the bill to the house on Tuesday and that will then start a 20-hour debate clock (excluding breaks which are likely from Democrats). It becomes a dynamic process with many votes on amendments and further debates, but the expectation is that it will end this week. Tennessee Republican Senator Corker, who had been a dissenter regarding the deficit burden the plan would cause, has been rumored to have spent the Thanksgiving period on calls with the administration in the hope of moving the bill forward. Corker’s spokesman stated, “While more work remains, all parties are hopeful that the final bill will be good for our country.” Until the markets have a clearer idea as to the timeline, and final amended bill to enact, USD is likely to remain soft.

GBP has benefitted from USD weakness, but concerns have risen as the UK nears an EU summit on Brexit in mid-December, with the markets concerned that GBP will become more vulnerable to political headlines as the date nears. UK Prime Minister Theresa May was given a 10-day “absolute deadline” by the EU to improve her Brexit divorce offer. The improved offer needs to address a resolution on the Northern Ireland border issue or face failure in persuading EU leaders to open trade talks with Britain at the December summit.

EURUSD is little changed overnight, currently trading around 1.1900.

USDJPY is 0.1% higher in early Tuesday trading at around 111.17.

GBPUSD is 0.1% higher in early session trading at around 1.3330.

Gold is unchanged overnight, currently trading around $1,294.25.

WTI is 0.2% lower in early Tuesday trading at around $57.77.

Major data releases for today:

07:00 GMT: Bank of England Bank Stress Test Results will be released. The Bank of England has now set out further details of the UK scenario for the stress tests that the eight major UK banks and building societies will be undertaking this year.

07:30 GMT: Bank of England Governor Mark Carney is scheduled to speak.

14:15 GMT: FOMC Member Jerome Powell is scheduled to speak.

14:15 GMT: New York Federal Reserve President William Dudley is scheduled to speak.

15:15 GMT: FOMC Member Patrick Harper is scheduled to speak.

16:15 GMT: Bank of Canada Governor Stephen Poloz is scheduled to speak.

20:45 GMT: US Treasury Secretary Steven Mnuchin is scheduled to speak.

Stocks Drop, Currencies Range Bound & Bitcoin Eyes $10,000

Most Asian indices edged lower on Tuesday, following a mixed session on Wall Street yesterday. China is becoming a key market to watch, as it is leading the direction for other markets across Asia. Rising bond yields are threatening corporate profit margins for the second largest economy; meanwhile Chinese authorities are helping to drag equities lower, after sending alarming messages about a potential bubble being created in large-cap firms. Given that China continues to focus on quality rather than quantity growth, it’s not surprising to witness action of this nature from the Chinese government in an attempt to mitigate bubbles in asset prices. However, such actions may have a negative impact on sentiments that could spread across other Asian markets.

U.S. equity traders are in a wait-and-see mode. President Trump will meet senators today at their weekly policy lunch, to ensure that Republicans are on the same page regarding the tax system overhaul. I firmly believe that U.S. legislative tax reforms are strongly “priced in”the U.S. markets, thus if significant tax reforms do not pass, I expect a substantial decline in major indices, particularly in small caps. Given that the effective tax rate currently stands at around 27%, taxes should be brought below 25% to be effective. Republican Senator Ron Johnson said he would vote against the bill unless his concerns about the legislation are resolved. Given that other Republican Senatorsshare Johnson’s worries on deficit implications, passing the bill does not seem to be a done deal yet.

Currency markets were trading in narrow ranges early Tuesday, as investors brace for U.K. bank stress test results, BoE’s Carney Speech and the Fed speech, including Powell’s Congressional address. On the data front,the U.S. Goods Trade Balance, and the Housing Price Index are likely to have minimal impact on the USD.

At the time of writing, Bitcoin scored a new record high of $9,886 in an attempt to break above the critical $10,000 threshold. Bitcoin has become a very hot topic and many fund managers have raised the price target for the cryptocurrency. Yesterday, former Fortress hedge fund manager Michael Novogratz commented on CNBC, that bitcoin could be at $40,000 by the end of 2018 and he expects that total market capitalization could reach $2 trillion, from $309 billion currently. I think that we will hear more skyrocket predictions, but few will provide an economic metric that supports their valuations. It will be interesting to see how the market reacts when Bitcoin breaks above $10,000.

Interest Rate Cuts By The Central Bank Could Hurt The Economy

Market movers today

Another quiet day. US Fed chair nominee Jerome P owell's confirmation hearing in t he Senate Banking Commit tee begins today. We expect his approval to be plain sailing despite him not being an economist . Powell is expected to cont inue the Fed's current monetary policy strategy with gradual hikes.

In the US, we have t ier-2 data releases with trade data, house prices and Conference Board consumer confidence indicator due for release.

In the euro area, we get M3 money supply and lending data today.

In Sweden, we get retail sales in October, which may shed light on how the Swedes have reacted to the recent development in the housing market .

Selected market news

Last night , Jerome Powell's prepared text for his confirmat ion hearing was published, see Federal Reserve, which support s t he view that Powell is going to stick to the Fed's current monetary policy strategy with gradual hikes and a cont inuation of Quantitative Tightening. Given that many Republicans want a more rule-based approach to monetary policy, it is interest ing that Powell says that the Fed ‘must retain the flexibility to adjust our policies in response to economic developments'. The nomination of Powell suggests the Trump administration does not want big changes to the current Fed framework. Also noticeable, Powell says that ‘we will continue to consider appropriate ways to ease regulatory burdens while preserving core reform'. Besides his own remarks, the most interest ing thing about the hearing is the Q&A session and his answers if there are any important quest ions.

Yesterday, the flattening of the US yield curve cont inued, with little news on the data front, amid new home sales surging in the US to the highest level in 10 years. Overnight New York Federal Reserve President William Dudley said in a speech that the US economy is running close to full employment and growth is expanding at an above trend pace.

Today, Bank of Japan (BoJ) Governor Haruhiko Karudo said that a ‘reversal rate', i.e. the level where interest rate cuts by the central bank could hurt the economy, helps BoJ to understand the appropriate shape of the yield curve. That said, Kuroda added that he did not see any signs that t he BoJ's ultra-loose policy was causing serious damage to Japan's banking system.

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD attempted to push higher yesterday topped at 1.1961 but closed lower at 1.1898. The bias is neutral in nearest term but as long as stay inside the bullish channel (see my H1 chart below )and above 1.1800, price is still in a bullish phase targeting 1.2000 – 1.2090 region. Immediate support is seen around 1.1850. A clear break below that area could trigger further bearish pressure testing 1.1800 and the lower line of the bullish channel. Overall I am neutral on this pair.

GBPUSD

The GBPUSD attempted to push higher yesterday topped at 1.3382 but whipsawed to the downside and closed lower back below 1.3330 key resistance, printed a bearish pin bar as you can see on my daily chart below. The bias is bearish in nearest term testing 1.3230 support area. Immediate resistance is seen around 1.3360. A clear break above that area could lead price to neutral zone in nearest term testing 1.3400 or higher. Overall, as long as stay above 1.3000 I remain bullish.

USDJPY

The USDJPY had a bearish momentum yesterday bottomed at 110.84. The bias remains bearish in nearest term testing 110.65 area as a part of the bearish pin bar scenario as you can see on my daily chart below. Immediate resistance is seen around 111.30. A clear break above that area could lead price to neutral zone in nearest term testing 111.65 – 112.00 region. On the downside, a clear break and daily close below 110.65 would expose 110.00 – 109.50 region. Overall I remain neutral.

USDCHF

The USDCHF had a moderate bullish momentum yesterday topped at 0.9819. The bias is neutral in nearest term probably with a little bullish bias testing 0.9835. A clear break above that area could trigger further bullish pressure testing 0.9875 area which is a good place to sell with a tight stop loss. Immediate support is seen around 0.9778. A clear break and daily close below that area would expose 0.9700 region. Overall I remain neutral.

Gold Price Poised To Break $1300 Vs US Dollar

Key Highlights

- Gold price remains in a major uptrend and is currently well above the $1280 support against the US Dollar.

- There is a key rising channel forming with support at $1282 on the 4-hours chart of XAU/USD.

- The US New Home Sales in Oct 2017 increased 6.2% (MoM), which was opposite to the -6.3% forecast.

- Today, the US Housing Price Index for Sep 2017 will be released, which is forecasted to increase by 0.6% (MoM).

Gold Price Technical Analysis

Gold price remains in an uptrend above the $1280 support area against the US Dollar. The price is currently approaching a major resistance zone near $1300-1302.

Looking at the 4-hours chart of XAU/USD, there is a key rising channel forming with support at $1282. The channel support at $1280-1282 is close to the 100 simple moving average (red, 4-hour). Therefore, the $1280-1282 support region can be considered as a major buy zone in the near term.

Only a daily close below $1280 would negate the current bullish bias. On the upside, the last swing high at $1296.93 is a short term resistance. Above the mentioned $1296.93, the price might test the next major resistance around the 1.236 Fib extension of the last drop from the $1296.93 high to $1274.61 low at $1302.20.

On the downside, an initial support is at $1288, followed by $1285 and then the most important at $1280-1282.

US New Home Sales

Recently in the US, the New Home Sales report for Oct 2017 was released by the US Census Bureau. The forecast was slated for a decline of 6.3% in sales in Oct 2017 compared with the previous month.

The actual result was on encouraging, as the New Home Sales increased 6.2% at a seasonally adjusted annual rate of 685,000. However, the last increase was revised down from 18.9% to 14.2%.

The report added:

The median sales price of new houses sold in October 2017 was $312,800. The average sales price was $400,200. The seasonally-adjusted estimate of new houses for sale at the end of October was 282,000. This represents a supply of 4.9 months at the current sales rate.

Gold price declined after the release, but remains well supported above the $1290 and $1282 levels.

Economic Releases to Watch Today

Germany’s GfK Consumer Confidence for Dec 2017 – Forecast 10.8, versus 10.7 previous.

Euro Zone Private loans (YoY) Oct 2017 – Forecast +2.8%, versus +2.7% previous.

US House Price Index for Sep 2017 (MoM) – Forecast +0.6%, versus +0.7% previous.

Market Update – Asian Session: Data Falsification Issue Spreads To Japan’s Toray

General Trend/Theme: Continued weakness in chip-related and China/Hong Kong equities amid dearth of economic data

China/Hong Kong

Markets opened lower following declines on Monday: Shanghai Composite opened -0.3%, Hang Seng opened -0.3%

Hang Seng Materials Index -1.1%, Financials Index -0.8%, Property Index -0.7%, Information Technology Index -0.7% (Tencent -1%)

(CN) China said to ban certain funds from selling stocks on a large scale – Chinese Press

(CN) China govt reportedly to make punishment harsher for banks' law violations - China press

(CN) China should be ‘vigilant' of risk from loan company closures – Chinese Press

(CN) China said to target adoption of e-commerce law in 2018 – Chinese Press

(HK)) China PBoC renews CNY400B currency swaps agreement for another 3 years with Hong Kong Monetary Authority (HKMA)

(CN) PBoC sets yuan reference rate at 6.5944 v 6.5874 prior

(HK) Hong Kong Oct Trade Balance (HKD): -44.B v -41.9Be; Exports Y/Y: 6.7% v 10.1%e

(CN) PBoC OMO: Injects CNY250B in 7, 14-day, 63-day reverse repos v CNY140B injected in 7,14 and 63-day reverse repos prior; Net: nil v nil prior

(CN) China Development Bank (CDB) sells 1, 3, 5 and 7-year bonds (**Note: On Nov 24th, there was speculation that China Development Bank might not sell the usual 10-year bonds in its weekly bond sale)

Australia:

ASX200 opened -0.1%; closed flat

ASX 200 Financials Index -0.3%; REIT Index +0.9%, Utilities Index +0.8%

Telstra -2% (block trade)

(AU) Australia sells A$150M in Nov 2027 Indexed Bonds, avg yield 0.6407%, bid to cover 4.83x

Japan

Nikkei 225 opened -0.1%; Closed flat

TOPIX Textiles & Apparels Index -1.4%

Chip-related stocks remain weaker following Monday's declines: Tokyo Electron -2.5% Toshiba -2%, SUMCO -1.5%

Index component Toray (chemicals/Plastics & Rubber) -3.4%: Data falsification issue spreads to the company

Toyota +0.3%: Names new CFO

Softbank said to offer to buy Uber shares at a $48B valuation, 30% below Uber's current valuation – US financial press (in line with valuation reported in early Aug)

BoJ Gov Kuroda: Reiterates global economy continues to recover; Asia's economy will be at core of global growth; Asia is more resilient against economic shocks.

JP) BOJ's Suzuki: Reiterates view that must maintain powerful monetary easing; yield Control changes is possible when CPI is near 2% level - financial press

(JP) BOJ's Kataoka: should strive to reach the 2% inflation target by FY18

Japan PM Abe: Reiterates don't think necessary to make changes on accord with BoJ

Japan govt reportedly considering tax cuts for companies that have cybersecurity plans - Japanese press

Japan MoF sells ¥500B v ¥500B in 0.90% 40-yr bonds; bid to cover 3.00x v 3.24x prior

South Korea

Kospi opened +0.2% (declined 1.4% prior session)

Samsung Elections +0.3% (declined over 5% prior session)

South Korea sells 30-year bonds at 2.52%

South Korea Dec Business Manufacturing Survey: 82 v 84 prior; Non-Manufacturing Survey: 80 v 79 prior

Channel News Asia reporter: Japanese govt is detecting signals that North Korea may be prepping ballistic missile launch (report is from US morning on Monday)

Other Asia

Malaysia

Ringgit (MYR) -0.2%

Malaysia Central Bank (Bank Negara) Deputy Gov Singh said to resign, effective immediately – Malaysian Press; The official is said to have chosen to retire early, says the report

Europe:

(IE) Ireland opposition Justice spokesperson: unless deputy PM resigns, will force Ireland into new election

(IE) Ireland Foreign Minister: Relationship with UK is ‘tense', last thing we need right now is an election in the middle of Brexit talks

(DE) Germany Econ Min Zypries: we're prepared to take countermeasures if US imposes new tariffs on steel

Unilever: Board to delay decision related to choice of headquarters – financial press

M&A: IAG.UK: Confirms acquisition of Monarch Airlines' Gatwick landing slots

Constantin Medien [EV4.DE]: Highlight Communications makes takeover offer to the shareholders of Constantin Medien AG to acquire no-par value ordinary bearer shares

North America

US equity markets end mixed: Dow Jones +0.1%, S&P500 flat, Nasdaq -0.2%, Russell 2000 -0.4%; Energy Sector -1%, Materials -0.6%

The US National Retail Federation (NRF) expected to release its Black Friday and Cyber Monday sales data on Tuesday, Nov 28th.

(US) Adobe: Confirms data shows Cyber Monday is largest online sales day in history with $6.59B in sales, +16.8% y/y as of 10:00 pm ET

Fed Speak: (US) Fed's Dudley (FOMC voter): Not particularly concerned that inflation is 'a little bit' below a Fed target; Reiterates we are gradually raising US interest rates; FOMC is 'very united' on appropriate policy path; Surprised 'how relaxed' markets are about government borrowing outlook

(US) Fed Chair-designate Powell: Expects interest rates will rise somewhat further from here; pledges to respond decisively to any new economic threats - prepared congressional testimony

(US) Fed's Kashkari (dove, voter): Reiterates sees no reason to 'tap the breaks' on the economy, no reason to raise rates when inflation continues to run low

(US) Fed's Kaplan (moderate, voter): backs rate hike in near future; remains mindful of Fed getting behind the curve

Tax Reform: (US) Senator Corker (R-TN): Could vote no on tax bill in committee if ‘trigger' not done; Wants the tax bill to have 'trigger' to raise revenues if economic growth expectations are not met; Says 'no vote' is not a threat, Republicans are working to resolve the issue. (** INSIGHT: The Senate Budget Committee has 12 Republicans and 11 Democrats. One vote switching could halt the bill's progress to the floor. Sen. Corker (R-TN) is also on the Budget Committee)

(US) Sen Johnson (R-WI): will vote against tax bill in Budget Committee on Tues unless my issues are resolved

(US) Sen Rand Paul (R-KY): will vote in favor of Senate tax bill

(US) Aides to Sen Daines (R-MT): Senator is currently a no on tax bill; however is optimistic about changes

(US) Sen Cornyn (R-TX): Senate will vote Weds on motion to proceed to tax bill; confirms that senators are considering a deficit trigger and

changes to pass-throughs

US) Sen Lankford (R-OK): working on different options for deficit 'backstop' if growth projections in tax bill do not pan out as expected

(US) White House: President Trump to meet with Congressional leadership on Tuesday

Fed's Dudley: Favors tax simplification and base-broadening; Opposes US tax stimulus at current time because the economy does not really need it; Tax stimulus may be worth the price to get reform.

Fed's Kashkari: If Congress passes a tax bill, Fed will update economic models, which may change path of interest rates

Goldman: Sees outcome of OPEC meeting more uncertain than usual, sees risks to oil as skewed to the downside this week

Saudi Arabia Energy Minster Falih: When asked how long oil output cuts will be extended, he replied that we will see when we get to Vienna

M&A: Roark said to agree to raise bid for Buffalo Wild Wings to ~$157/share or $2.4B in cash – US financial press

Levels as of 01:00ET

Hang Seng -0.8%; Shanghai Composite -0.3%; Kospi +0.3%

Equity Futures: S&P500 -0.1%; Nasdaq100 -0.2%, Dax -0.1%; FTSE100 flat

EUR 1.1892-1.1909 ; JPY 110.93-111.32 ; AUD 0.7601-0.7614 ;NZD 0.6910-0.6938

Dec Gold flat at $1,293/oz; Jan Crude Oil -0.6% at $57.77/brl; Dec Copper -0.3% at $3.124/lb