Sample Category Title

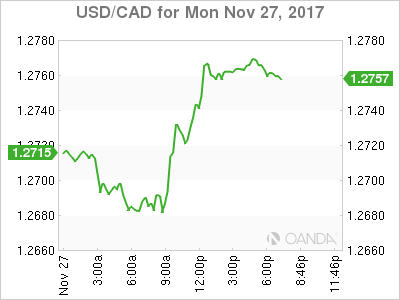

Canadian Dollar Lower as Oil Price Falters

The Canadian dollar depreciated on Monday after oil prices fell more than 1 percent at the start of the week. Higher supply in North America and concerns about Russia's commitment to the OPEC production cut agreement have lowered energy prices after touching two year highs. The fall in energy prices affected the loonie as the correlation between the two is resurfacing.

The Bank of Canada will release its Financial System Review on Tuesday, November 28 at 10:30 am EST. US Federal Reserve members will also feature heavily this week, with Chair nominee Jerome Powell due to testify before the US Senate at 10:00 am EST on Tuesday.

BMO released a report on the impact of NAFTA ending with the impact to Canada about 1 percent of GDP. Inflation would rise given the potential weak loonie and pricier imports which could put pressure on the BoC to raise rates. After the fifth round of talks ended in Mexico City there was a sense that little progress has been made. The end of the year is fast approaching and with the new year will come Presidential elections in Mexico and the US primaries adding more uncertainty to an already dicey negotiation. The next round of talks will happen in Washington on December 11.

The USD/CAD gained 0.52 percent on Monday. The currency pair is trading at 1.2769 as the US dollar managed to get a leg up after a short holiday week had the greenback on the backfoot. The negative impact on the US tax reforms issues remains when talking about the JPY but against all the other majors the USD appreciated. Friday, December 1 will be a busy week for CAD traders. Statistics Canada will release the monthly GDP figures as well as the employment report both at 8:30 am EST. GDP is expected to have shrunk by 0.1 percent and there is some anxiety on the job front as the first ADP job report for Canada showed a loss of 5,700 in October.

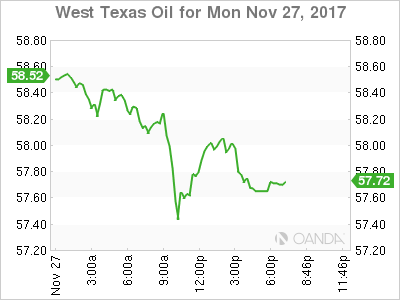

Oil prices fell at the beginning of the week. The price of West Texas Intermediate is trading at $57.65 after the Keystone pipeline will restart operations on Tuesday and doubts about Russia's willingness to extend the OPEC production cut agreement, put pressure on crude prices.

Oil ministers will meet in Vienna on Thursday a year after a deal was reached to reduced crude production to stabilize prices by the Organization of the Petroleum Exporting Countries (OPEC). Russia and other major producers joined the agreement in December, and have already extended the deal until March of 2018, but the likely outcome from the meeting in Vienna is a second extension. The main topic of debate is for how long as different timelines have been discussed. Russia has taken the leadership position in a time when Saudi Arabia is opening too many fronts in the diplomatic arena.

The mercurial nature of OPEC members has already resulted in failed summits in the past, but it appears that Russia is seen as a conciliatory third party that could push through an extension. The main issue now is by how much will the new head of the energy class want to extend the production cut agreement. Russia was slow to comply with the cuts, and might not be as willing to go for a full 9 month extension this time around.

Market events to watch this week:

Tuesday, November 28

- 2:00am GBP Bank Stress Test Results

- 10:00am USD CB Consumer Confidence

- 11:15am CAD BOC Gov Poloz Speaks

- 3:00pm NZD RBNZ Financial Stability Report

Wednesday, November 29

- All Day All OPEC Meetings

- 8:30am USD Prelim GDP q/q

- 10:30am USD Crude Oil Inventories

- 7:00pm NZD ANZ Business Confidence

- 7:30pm AUD Private Capital Expenditure q/q

Thursday, November 30

- 8:30am USD Unemployment Claims

Friday, December 1

- 4:30am GBP Manufacturing PMI

- 8:30am CAD Employment Change

- 8:30am CAD GDP m/m

- 10:00am USD ISM Manufacturing PMI

*All times EDT

British Pound Looking for Footing

The British pound moved higher on Monday, but has given up these gains. In North American trade, GBP/USD is trading at 1.3332, up 0.02% on the day. On the release front, there are no UK events on the schedule. In the US, New Home Sales surged to 687 thousand, well above the estimate of 627 thousand. On Tuesday, the focus will be on the Bank of England which publishes the results of its bank stress tests, as well as the semi-annual Financial Stability report. The US releases CB Consumer Confidence, with an estimate of 123.9 points. As well, Federal Reserve Chair Designate Jerome Powell will testify before a Congressional committee.

There may be signs that the British economy is slowing down, but CBI retail sales and manufacturing reports looked sharp last week. Retail sales jumped in November, as CBI Realized Sales rebounded with a strong reading of 26 points. The release was all the more impressive, as the indicator came in at -36 points in October. CBI Industrial Order Expectations, an important barometer of activity in the manufacturing sector, also impressed. The indicator surged to 17 points in October, rebounding from the September release of -2 points. Manufacturing indicators continue to point upwards, boosted by strong global demand and a weak British pound. Export order books are at their highest levels since 1995, and the markets are predicting that the export and manufacturing sectors will continue to shine in the fourth quarter.

All eyes will be on Jerome Powell, who testifies before the Senate Banking Committee on Tuesday for his confirmation hearing. Will Powell be a clone of outgoing chair Janet Yellen? Powell inherits an economy that is in excellent shape, but persistently low inflation remains a nagging problem. Fed policymakers have differing views on what to do about inflation, with some members proposing that the Fed drop its 2 percent target, in favor of a "gradually rising path" for prices. The Fed remains confounded by low inflation and wage growth, despite a labor market that is at full capacity. Still, the Fed will likely pull the rate trigger next month, and could raise rates up to 3 more times in 2018 if the economy continues to expand at its current pace.

Gold Pushes Higher as Dollar Sags

Gold has jumped on the bandwagon, as the US dollar is broadly lower in the Monday session. In North American trading, the spot price for an ounce of gold is $1295.12, up 0.52% on the day. Gold pushed above the $1299 line earlier in the day, its highest level since October 16. On the release front, New Home Sales surged to 687 thousand, well above the estimate of 627 thousand. On Tuesday, the US releases CB Consumer Confidence, with an estimate of 123.9 points. As well, Federal Reserve Chair Designate Jerome Powell will testify before a Congressional committee.

Federal Reserve policymakers remain upbeat about the U.S economy, according to the minutes of the most recent policy meeting. The minutes indicated that policymakers expected the U.S economy to continue showing strong growth, and predicted that interest rates will be raised in the "near term". The members discussed the vexing question of why inflation has been persistently low (no quick-fix solution was provided), with most agreeing that a tight labor market should lead to higher inflation levels. Although policymakers did not provide further hints about the timetable of a rate hike, the markets remain convinced that additional rates are imminent. The odds of a rate hike in December are 93%, and the odds of a January raise are at 91%.

All eyes will be on Jerome Powell, who testifies before the Senate Banking Committee on Tuesday for his confirmation hearing. Will Powell be a clone of outgoing chair Janet Yellen? Powell inherits an economy that is in excellent shape, but persistently low inflation remains a nagging problem. Fed policymakers have differing views on what to do about inflation, with some members proposing that the Fed drop its 2 percent target, in favor of a "gradually rising path" for prices. The Fed remains confounded by low inflation and wage growth, despite a labor market that is at full capacity. Still, the Fed will likely pull the rate trigger next month, and could raise rates up to 3 more times in 2018 if the economy continues to expand at its current pace.

Dollar Broadly Weaker; Sterling Rises Despite Brexit Uncertainty; Oil Retreats

With US new home sales being the day's major release during today's session, upcoming developments, such as US tax reform deliberations and Brexit negotiations, were in forex market participants' minds during today's European session. Meanwhile, the yen was advancing on some softness in Asian and European equity markets.

At 1523 GMT, the dollar index, which measures the greenback against the currencies of six major US trading partners, was 0.1% down at 92.74. The gauge finished lower in the three preceding weeks, while today it touched a three-month low of 92.50. The US currency was deeper in losses earlier in the day but managed to reverse some of its losses later in the session.

Jerome Powell, President Trump's nominee to lead the Fed once Janet Yellen's term expires in February, will be having his confirmation hearing in Washington on Tuesday (1500 GMT) with senators having the opportunity to question him on key issues. Any comments on monetary policy, deregulation and the economy overall have the capacity to act as market movers.

The US Senate will be resuming deliberations on tax reform this week following last week's Thanksgiving break. Donald Trump is scheduled to meet Senate Republicans on Tuesday to discuss continuing efforts to pass the tax plan legislation. Developments on this front are also likely to act as catalysts for dollar positioning.

In today's main release, October new home sales rose by 6.2% m/m to reach 685k units, contrasting expectations for a decline by 6.0% after September's surge by 14.2% (downwardly revised from 18.9%). Sales in October constitute a decade high as well as the third straight monthly increase and reflect strong demand across the US. The dollar managed to erase some of its losses relative to major rivals following the release at 1500 GMT.

Dollar/yen was last 0.3% lower, trading above the 111 mark, a level violated on the downside earlier in the day as the pair hit a two-month low of 110.87. Euro/dollar was flat after advancing in the three preceding days. At its highest, it recorded a two-month peak of 1.1960. Upbeat data in recent days and political uncertainty withering out in Germany on the back of rising prospects for a coalition between Social Democrats and Merkel's Christian Democrats, have been supportive of a stronger euro.

Eurozone's common currency was losing ground relative to the yen during today's trading though. Euro/yen was 0.4% down at 132.63. Still, the pair held most of the gains from Friday's advance, a day on which it rose by 1.1%. The yen's capacity as a funding currency appears to have supported it today as there was a pullback of some sorts in non-US equity markets. Pound/yen was also lower (by 0.2%) at 148.42.

Sterling was last stronger versus both the dollar and the euro despite the Irish border issue – a key consideration in Brexit negotiations – getting more complicated ahead of political uncertainty in Ireland, with elections potentially being put on the table for December; this will become clearer by tomorrow. Pound/dollar was 0.1% up after tracking a two-month high of 1.3382 earlier in the day. Euro/pound was 0.1% lower at 0.8935 after previously rising to an 11-day high of 0.8966.

UK PM Theresa May was given a deadline up to December 4 by EU counterparts to improve its position on key pending Brexit issues in order for leaders from the bloc to approve the commencement of talks on trade relations during the summit scheduled for December 14-15.

Dollar/loonie was 0.1% higher at 1.2726, reversing earlier losses. Meanwhile, the aussie was flat relative to the greenback at $0.7611 and the kiwi was up by 0.5% versus its US counterpart at $0.6913. At their highest, they both touched two-week peaks versus the greenback.

In notable movements within the emerging markets spectrum, the South Africa rand was making up on some of its losses from previous days relative to the dollar after credit rating agency Moody's decided to place South Africa on review for a downgrade rather than proceed with an outright credit cut as was the case with Standard & Poor's which now rates the nation's credit ability within the "junk" category. There is some relief in the markets, as should Moody's had gone ahead with a downgrade, then South African bonds would had been removed from numerous key global bond indexes. Dollar/rand was last 0.9% down at 13.7435.

In commodities, gold was 0.5% up at $1,294.40 per ounce. Its highest on the day, which also constituted a more than one-month peak, was $1,299.13. The precious metal is on a positive footing on the back of dollar weakness, but it also benefitted on cautiousness in stock markets during today's trading. WTI and Brent crude traded lower by 2.15% and 1.1%, at $57.68 and $63.26 a barrel respectively. Despite the sell-off, both benchmarks remained relatively close to recently-hit more than two-year high levels.

USDCAD Bounces from Dangerous Zone on Upbeat US Data

The pair accelerated sharply higher as the greenback was strongly boosted by upbeat US data.

US new home sales unexpectedly rose in October (6.2% / 685K vs -6.0% / 625K forecast) hitting the highest level since October 2007.

Fresh rally moves away from dangerous zone at 1.2665/70 (lows of 10 Nov / 23 Nov) which mark the breakpoint for bears from 1.2916 (27 Oct high).

Higher base is forming here but break above next strong barriers at 1.2750 zone (4-hr cloud base / converging 10/20SMA's) is needed to confirm and open way for further recovery.

Further recovery would then open next pivot at 1.2783 (4-hr cloud top).

Lower oil prices would be also supportive for further weakness of the loonie.

Conversely, recovery rejection under 10/20SMA's would signal extended consolidation and keep the downside at risk.

Res: 1.2750; 1.2761; 1.2791; 1.2820

Sup: 1.2680; 1.2665; 1.2628; 1.2598

UK100 Index Enters Ichimoku Cloud; Neutral Bias Intact

UK100 paused its recent downtrend at a six-week low of 7349.80 on November 20 and has been trading flat around that level since then, painting a neutral picture in the short-term. In the medium-term, the index is also in a consolidation phase.

The index is currently located inside the Ichimoku cloud, retracing the 50% Fibonacci level of the upleg from 7194.70 to 7588.66 (September 15 – November 7) at 7391.04. In the short-term, the bias is likely to remain neutral as the RSI is moving sideways slightly below 50, while the oscillator is also flat in the four-hour and the one-hour chart. The Kijun-sen and the Tenkan-sen lines, which posted a bearish cross on November 17 have also flattened out, supporting this view.

In case downside pressure emerges, the index is likely to find support around the 61.8% Fibonacci at 7344.94, where the 200-day exponential moving average is also placed. However, any violation of this point would extend the downleg started from a six-month high of 7588.60 on November 7, turning the short-term bias from neutral to bearish. Then from here, steeper declines would also target the 78.6% Fibonacci at 7278.03.

To the upside, the 38.2% Fibonacci of 7437.15 could represent strong resistance as the 50-day EMA is also laying in that area. Further increases would meet additional resistance levels at the 23.6% Fibonacci of 7495.01 and at the previous top of 7588.66.

To sum up, in the medium-term, the outlook is neutral as long as UK100 moves between 7194.70 and 7588.66.

USD Selling Remains the ‘By Default’ FX Trade, For Now?

- European equities traded choppy in this week's opening trading session. At the time of writing, they lose around 0.25%. US stock markets opened narrowly mixed.

- Germany's political stalemate showed signs of easing as the Social Democrats started haggling over terms of a renewed coalition with Chancellor Merkel's conservative bloc rather than outright blocking an alliance between Germany's two biggest parties.

- EU authorities have approved Ireland's plans to pay off the last of its crisis-era bailout loans from the IMF early, in a move the government claims will save it around €150m in debt servicing costs. Ireland will repay the remaining €4.5bn from €22.5bn in IMF rescue cash and another €1bn in bilateral loans from Sweden and Denmark.

- The Senate tax bill is headed for a marathon debate this week with the aim to hold a floor vote as early as Thursday. Should it pass, Republican leaders will have to hammer out a compromise between different provisions in the House and Senate bills.

Rates

Core bonds marginally higher in uneventful session

The Bund opened the session unchanged and traded a bit erratic throughout the European session, but overall with a positive bias. The changes are minimal and technically insignificant. The eco calendar was thin and ignored. Equities and oil prices traded range-bound. In this context, the moves of core bonds were range-bound too, but with a slightly upward bias. The US curve flattening was modest, but resumed its trend after a 2-day pause. The German curve was marginally affected. The sole EMU eco releases, Italian economic and consumer confidence, were weaker than expected, but didn't play a role on trading. Later today, the US new home sales will be released and the Treasury sells 2- and 5-yr. Treasury Notes. We don't expect these to fundamentally change the course of core bonds.

At the time of writing, the German yield curve bull flattens slightly with yields up to 1.8 bps (30-yr) lower. The US yield curve flattens too with yields up to 0.8 bps higher at the shorter end (2-yr) and up to 1.7 bps lower at the very long end. On intra-EMU bond markets, yield spreads are virtually unchanged.

Currencies

USD selling remains the 'by default' FX trade, for now?

There was little economic news in the US or in EMU today. Risk sentiment turned a bit more cautious, even as European losses remain modest. Softer equity sentiment was a good enough reason to keep the dollar in the defensive. USD/JPY dropped below the 111 big figure. EUR/USD set a minor new correction top north of 1.1950. Dollar selling remains the preferred FX trade as long as there is no high profile eco or other news.

Overnight, sentiment on Asian markets gradually tuned negative. China and South Korea took the lead in the correction. Japanese equities reversed an opening gain into a small losses. USD/JPY more or less copied the intraday price action on Japanese equity markets. An initial up-tick was reversed. USD/JPY returned to the 111.40 area. EUR/USD traded little changed near 1.1925.

European equities opened slightly lower, but tried to decouple from the correction in Asia. The tentative European equity rebound temporary slowed the dollar's decline, but the US currency never gave the impression that even a modest rebound was imminent. Changes in interest rate differentials were negligible and no driver for FX trading. There were further indications that the SPD and the CDU/CSU are moving to real coalition talks for a German government. This might have been a slightly supportive for the euro. However, dollar softness was the dominant FX trend.

This trend continued in US dealings as risk sentiment dwindled. EUR/USD touched a now correction top in the 1.1960 area. USD/JPY also set a new correction low as the pair dropped below the 111 big figure. Dollar selling remains the way of least resistance. EUR/USD trades currently in the 1.1955 area. USD/JPY is changing hands around 110.90. The dollar is still desperately looking for good news.

Cable breaks beyond intermediate resistance

There were no eco data in the UK today. EU and UK negotiators still try to engineer behind closed doors a proposal that might convince EU leaders at the mid-December summit to give the green light for negotiations on the further relationship between the UK and the EU. For now, there are no signs that big progress has been made. Even so, in technical traded, sterling (re)gained a few ticks against the euro and the dollar. EUR/GBP trades in the 0.8935 area. Cable broke above the 1.3348 intermediate resistance and trades in the 1.3375 area. This move is mostly due to USD weakness rather than GBP strength.

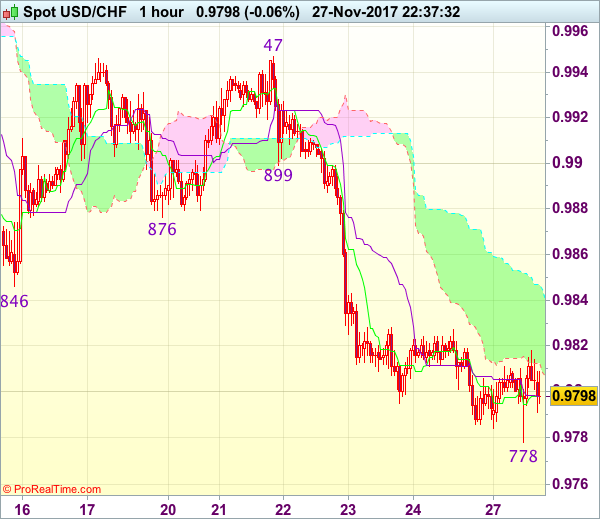

Trade Idea Wrap-up: USD/CHF – Sell at 0.9845

USD/CHF - 0.9810

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 0.9798

Kijun-Sen level : 0.9798

Ichimoku cloud top : 0.9845

Ichimoku cloud bottom : 0.9809

Original strategy :

Sell at 0.9835, Target: 0.9735, Stop: 0.9870

Position : -

Target : -

Stop : -

New strategy :

Sell at 0.9845, Target: 0.9735, Stop: 0.9880

Position : -

Target : -

Stop : -

As dollar has remained under pressure after last week’s selloff, adding credence to our bearish view that top has been formed at 1.1038 and bearishness remains for the decline from there to extend weakness to 0.9730-37 support area, however, near term oversold condition should limit downside and reckon support at 0.9705 would hold from here, bring rebound later.

In view of this, we are looking to sell dollar again on recovery as previous support at 0.9846 should turn into resistance and limit upside. Only break of 0.9875-80 would defer and signal a temporary low is formed instead, bring test of 0.9899 but price should falter well below resistance at 0.9947.

Trade Idea Wrap-up: GBP/USD – Buy at 1.3280

GBP/USD - 1.3359

Most recent candlesticks pattern : N/A

Trend : Near term up

Tenkan-Sen level : 1.3347

Kijun-Sen level : 1.3347

Ichimoku cloud top : 1.3311

Ichimoku cloud bottom : 1.3265

Original strategy :

Buy at 1.3280, Target: 1.3380, Stop: 1.3245

Position : -

Target : -

Stop : -

New strategy :

Buy at 1.3280, Target: 1.3380, Stop: 1.3245

Position : -

Target : -

Stop : -

As cable has maintained a firm undertone after breaking above previous resistance at 1.3338, adding credence to our view that the erratic rise from 1.3027 low is still in progress and bullishness remains for this move to extend gain to 1.3395-00, however, reckon upside would be limited to 1.3417-20 (61.8% Fibonacci retracement of 1.3658-1.3027) would hold from here due to loss of near term upward momentum.

In view of this, we are looking to buy sterling on pullback as 1.3270-80 should limit downside. Below 1.3250 would defer and risk correction to 1.3230 but only break of support at 1.3209-13 would abort and signal a temporary top is formed instead, bring further weakness towards support at 1.3170.

GBPUSD at New Two-Month High; Bulls Eye Target at 1.3415

Cable posted new nearly two-month high at 1.3382 on Monday after fresh bullish acceleration triggered stops above Friday's high at 1.3359.

Immediate focus lies at 1.3401 (02 Oct high) ahead of key target at 1.3415 (Fibo 61.8% of 1.3655/1.3026 descend), violation of which would generate another strong bullish signal.

No signs of rally's stall so far, despite overbought slow stochastic on daily chart, but some hesitation on approach to 1.3415 target could be anticipated.

We expect broken trendline which connects former tops at 1.3337 and 1.3320 (1.3305) to limit dips, guarding key n/t support at 1.3276 (daily cloud top).

Res: 1.3401; 1.3415; 1.3455; 1.3506

Sup: 1.3305; 1.3276; 1.3256; 1.3214