Sample Category Title

Markets Stabilize, But Trade Risks Persist as US Imposes China Tariffs, Beijing Strikes Back

Global markets found some stability after the US agreed to a 30-day delay on tariffs against Mexico and Canada following agreements on fentanyl trafficking and border security measures. However, trade tensions remain elevated as Washington proceeded with the additional 10% tariff on all Chinese imports. In response, China retaliated by imposing a 15% tariff on US coal and LNG, along with a 10% levy on crude oil, farm equipment, and select automobiles, set to take effect on February 10.

Further escalation could be on the horizon, as US President Donald Trump signaled that additional tariff hikes on China remain a possibility unless Beijing takes further steps to curb fentanyl exports. Meanwhile, trade friction with the EU is also building. Trump hinted over the weekend that European imports could be his next target, prompting EU leaders at a summit in Brussels to prepare countermeasures while expressing willingness for negotiations. Developments on both fronts will be closely monitored in the days ahead.

In the currency markets, Canadian Dollar is leading gains for the week so far, rebounding strongly following the tariff delay. Japanese Yen follows as the second-strongest performer, benefiting from risk aversion, while British Pound holds up well. On the weaker side, New Zealand Dollar is underperforming, followed by Euro and Australian Dollar. Dollar has retraced most of its earlier gains and is now trading in the middle of the performance rankings alongside Swiss Franc.

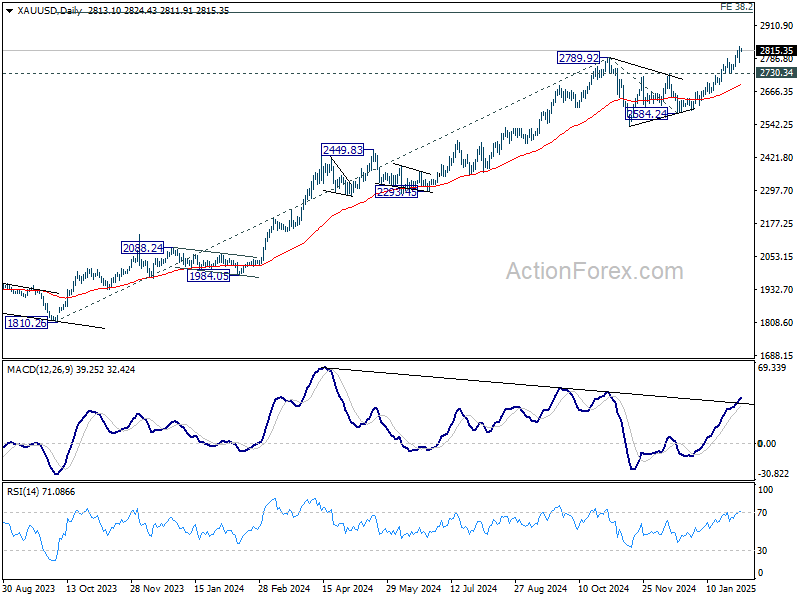

Technically, Gold hit another record high on risk aversion yesterday after initial volatility. For now, outlook will stay bullish as long as 2730.34 support holds. Next target is 38.2% projection of 1810.26 to 2789.92 from 2584.24 at 3074.07, which is close to 3000 psychological. This level will be crucial in determining the underlying momentum of Gold.

In Asia, at the time of writing, Nikkei is up 0.82%. Hong Kong HSI is up 1.76%. China is still on holiday. Singapore Strait Times is down -0.13%. Japan 10-year JGB yield is up 0.0228 at 1.272. Overnight, DOW fell -0.28%. S&P 500 fell -0.76%. NASDAQ fell -1.20%. 10-year yield fell -0.026 to 4.543.

CAD rebounds as US pauses tariffs for 30 days

Canadian Dollar rebounded sharply after US President Donald Trump announced a 30-day pause on planned tariffs against Canadian imports, just hours after implementing a similar delay for Mexico.

The decision came after negotiations between Trump and Canadian Prime Minister Justin Trudeau, who confirmed that Canada would take aggressive new measures to combat fentanyl trafficking, including deploying nearly 10,000 personnel to reinforce border security. Canada also committed to appointing a "Fentanyl Czar", classifying cartels as terrorist organizations, and launching a Canada-US "Joint Strike Force" targeting organized crime and money laundering.

Markets welcomed the de-escalation, as the tariff pause removes immediate downside risks for the Canadian economy. Trump emphasized that the suspension is conditional on further progress in security measures and that an "Economic deal with Canada" may still need to be structured.

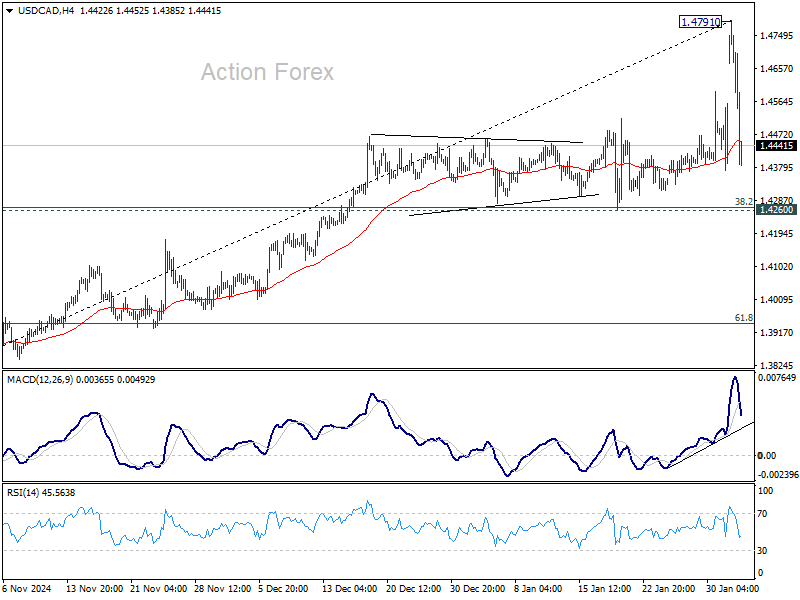

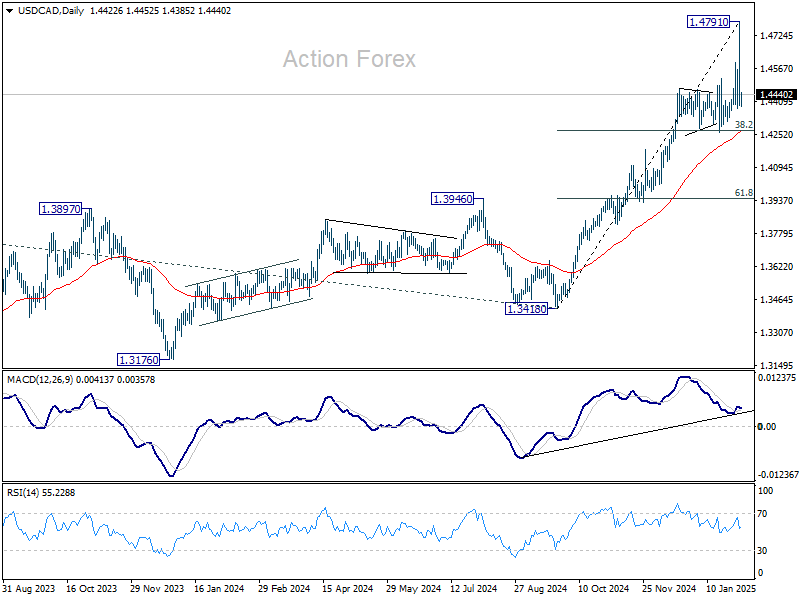

Technically, a short term top is likely formed at 1.4791 in USD/CAD after this week's strong volatility. More sideway trading should now be seen in the near term. However, outlook will continue to stay bullish as long as 1.4260 cluster support holds (38.2% retracement of 1.3418 to 1.4791 at 1.4267), which is also close to 55 D EMA (now at 1.4267). USD/CAD's up trend is still in favor to resume at a later stage when the consolidation completes.

Fed officials stress patience on rate cuts amid tariff uncertainty

A trio of Fed officials cautioned that new broad-based tariffs could add upward pressure to consumer and producer prices, suggesting a slower pace of rate cuts than previously anticipated.

Boston Fed President Susan Collins highlighted yesterday that tariffs on both final and intermediate goods risk inflating costs throughout supply chains, requiring "patient" policy decisions.

"It's really appropriate for policy to be patient, careful, and there's no urgency for making additional adjustments, especially given all of the uncertainty, even though, of course, we're still somewhat restrictive," Collins said.

Chicago Fed President Austan Goolsbee also stressed "a ton of uncertainty," warning that a premature return to lower rates could reignite inflation.

"We've got to be a little more careful and more prudent of how fast rates could come down because there are risks that inflation is about to start kicking back up again," Goolsbee said.

Meanwhile, Atlanta Fed President Raphael Bostic noted that any tariff-related surge in prices or inflation expectations might warrant close monitoring before further easing steps are taken.

BoJ's Ueda prioritizes underlying inflation trends, not short-term volatility

BoJ Governor Kazuo Ueda reiterated the central bank’s commitment to achieving its 2% inflation target on a sustained basis, emphasizing that the focus remains on underlying inflation rather than temporary price fluctuations.

Speaking before parliament, Ueda highlighted that BoJ filters out one-off factors such as fuel and volatile fresh food prices when assessing inflation trends.

However, he acknowledged "that process at times could be difficult", reinforcing the need for careful analysis before making policy adjustments.

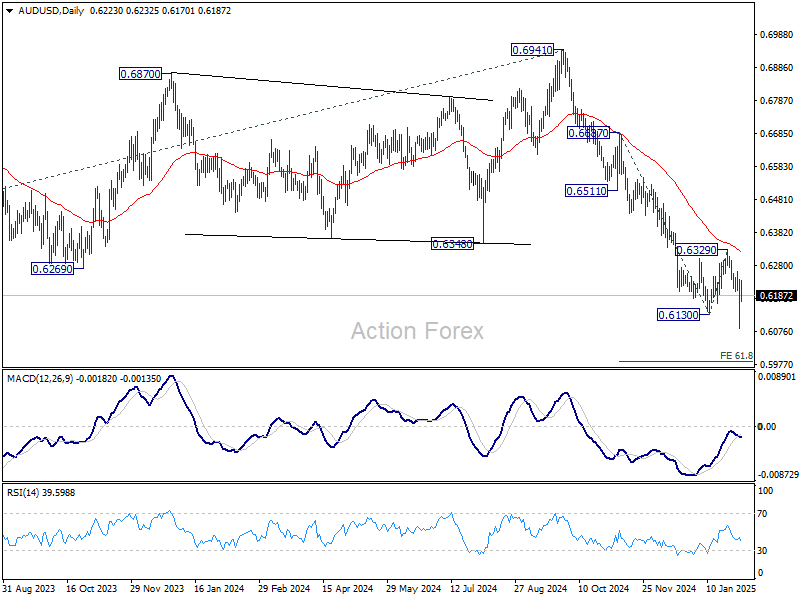

AUD/USD Daily Report

Daily Pivots: (S1) 0.6130; (P) 0.6184; (R1) 0.6279; More...

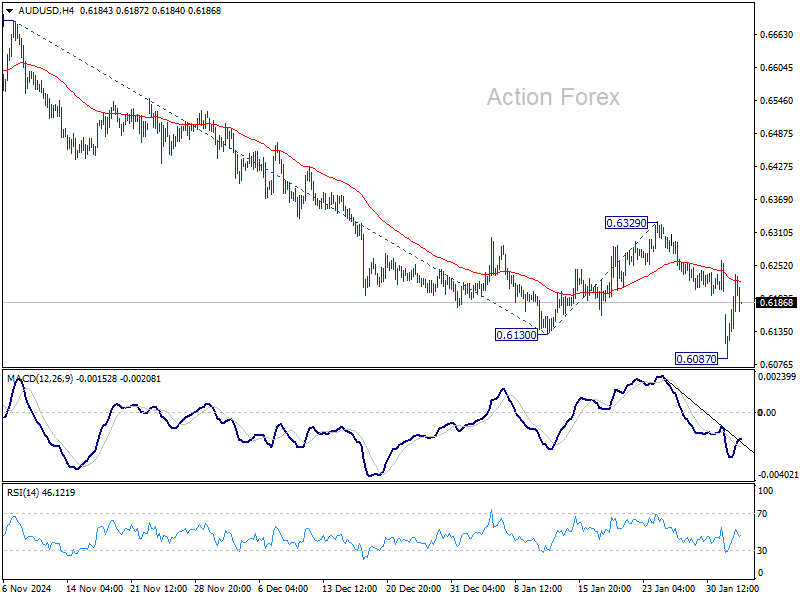

Intraday bias in AUD/USD is turned neutral as it recovered notably after dipping to 0.6087. Some consolidations would be seen first. But outlook will stay bearish as long as 0.6329 resistance holds. Break of 0.6087 will resume larger decline from 0.6941. Next target is 61.8% projection of 0.6687 to 0.6130 from 0.6329 at 0.5985.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6511) holds.

BoJ’s Ueda prioritizes underlying inflation trends, not short-term volatility

BoJ Governor Kazuo Ueda reiterated the central bank’s commitment to achieving its 2% inflation target on a sustained basis, emphasizing that the focus remains on underlying inflation rather than temporary price fluctuations.

Speaking before parliament, Ueda highlighted that BoJ filters out one-off factors such as fuel and volatile fresh food prices when assessing inflation trends.

However, he acknowledged "that process at times could be difficult", reinforcing the need for careful analysis before making policy adjustments.

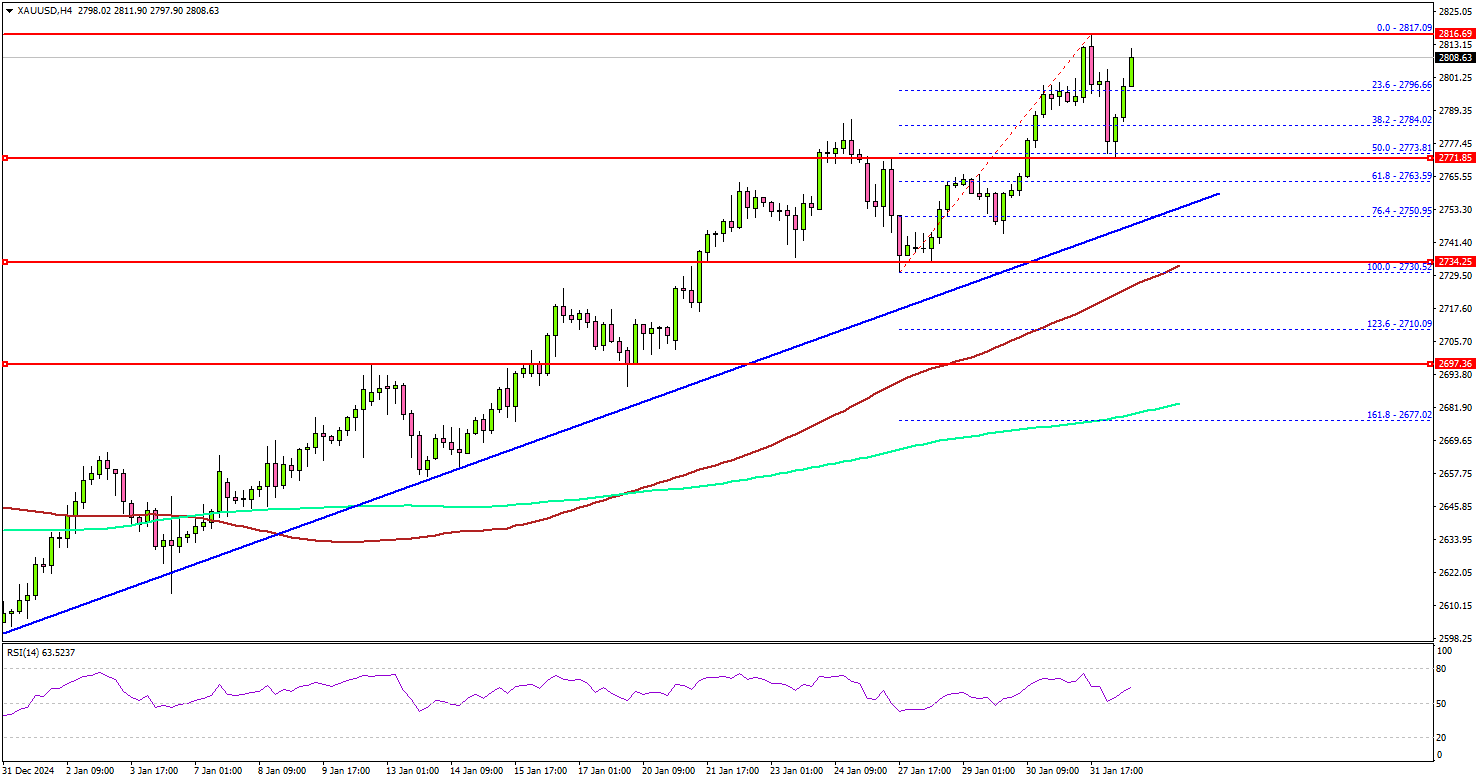

Gold Shines Bright Amid Market Selloff and New US Tariffs

Key Highlights

- Gold started a fresh upward move above the $2,780 resistance.

- A key bullish trend line is forming with support at $2,750 on the 4-hour chart.

- Bitcoin crashed toward $90,000 before the bulls appeared.

- EUR/USD is signaling weakness and might dip toward the 1.0150 support.

Gold Price Technical Analysis

Gold prices started a fresh increase amid Trump’s trade war. The price gained pace and remained in an uptrend above the $2,780 resistance.

The 4-hour chart of XAU/USD indicates that the price was able to clear the $2,800 resistance zone. It settled well above the 100 Simple Moving Average (red, 4 hours) and the 200 Simple Moving Average (green, 4 hours).

The current price action is bullish and indicates chances of more upsides. On the upside, immediate resistance is near the $2,820 level. The next major resistance sits near the $2,832 level.

A clear move above the $2,832 resistance could open the doors for more upsides. The next major resistance could be $2,850, above which the price could rally toward the $2,865 level.

On the downside, initial support is near the $2,795 level. The first key support is near $2,775. The next major support is near the $2,750 level.

There is also a key bullish trend line forming with support at $2,750 on the same chart. The main support is now $2,735. A downside break below the $2,735 support might call for more downsides. The next major support is near the $2,720 level.

Looking at EUR/USD, the pair opened with a gap down and the bears could now aim for more losses below 1.0200.

Economic Releases to Watch Today

- US Factory Orders for Dec 2024 (MoM) - Forecast -0.8%, versus -0.4% previous.

CAD rebounds as US pauses tariffs for 30 days

Canadian Dollar rebounded sharply after US President Donald Trump announced a 30-day pause on planned tariffs against Canadian imports, just hours after implementing a similar delay for Mexico.

The decision came after negotiations between Trump and Canadian Prime Minister Justin Trudeau, who confirmed that Canada would take aggressive new measures to combat fentanyl trafficking, including deploying nearly 10,000 personnel to reinforce border security. Canada also committed to appointing a "Fentanyl Czar", classifying cartels as terrorist organizations, and launching a Canada-US "Joint Strike Force" targeting organized crime and money laundering.

Markets welcomed the de-escalation, as the tariff pause removes immediate downside risks for the Canadian economy. Trump emphasized that the suspension is conditional on further progress in security measures and that an "Economic deal with Canada" may still need to be structured.

Technically, a short term top is likely formed at 1.4791 in USD/CAD after this week's strong volatility. More sideway trading should now be seen in the near term. However, outlook will continue to stay bullish as long as 1.4260 cluster support holds (38.2% retracement of 1.3418 to 1.4791 at 1.4267), which is also close to 55 D EMA (now at 1.4267). USD/CAD's up trend is still in favor to resume at a later stage when the consolidation completes.

Fed officials stress patience on rate cuts amid tariff uncertainty

A trio of Fed officials cautioned that new broad-based tariffs could add upward pressure to consumer and producer prices, suggesting a slower pace of rate cuts than previously anticipated.

Boston Fed President Susan Collins highlighted yesterday that tariffs on both final and intermediate goods risk inflating costs throughout supply chains, requiring "patient" policy decisions.

"It's really appropriate for policy to be patient, careful, and there's no urgency for making additional adjustments, especially given all of the uncertainty, even though, of course, we're still somewhat restrictive," Collins said.

Chicago Fed President Austan Goolsbee also stressed "a ton of uncertainty," warning that a premature return to lower rates could reignite inflation.

"We've got to be a little more careful and more prudent of how fast rates could come down because there are risks that inflation is about to start kicking back up again," Goolsbee said.

Meanwhile, Atlanta Fed President Raphael Bostic noted that any tariff-related surge in prices or inflation expectations might warrant close monitoring before further easing steps are taken.

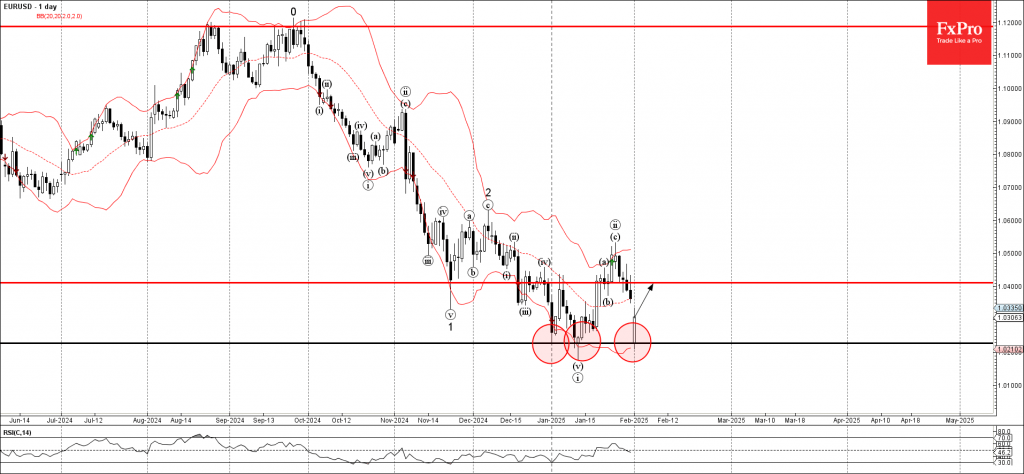

EURUSD Wave Analysis

- EURUSD reversed from pivotal support level 1.0225

- Likely to rise to resistance level 1.0400

EURUSD currency pair recently reversed up from the major pivotal support level 1.0225, which has been steadily reversing the pair from the end of last year, as can be seen from the daily EURUSD chart below.

The support zone near the support level 1.0225 was further strengthened by the lower daily Bollinger Band.

Given the strength of the support level 1.0225 and the bearish US dollar sentiment seen today, the EURUSD currency pair can be expected to rise to the next resistance level 1.0400.

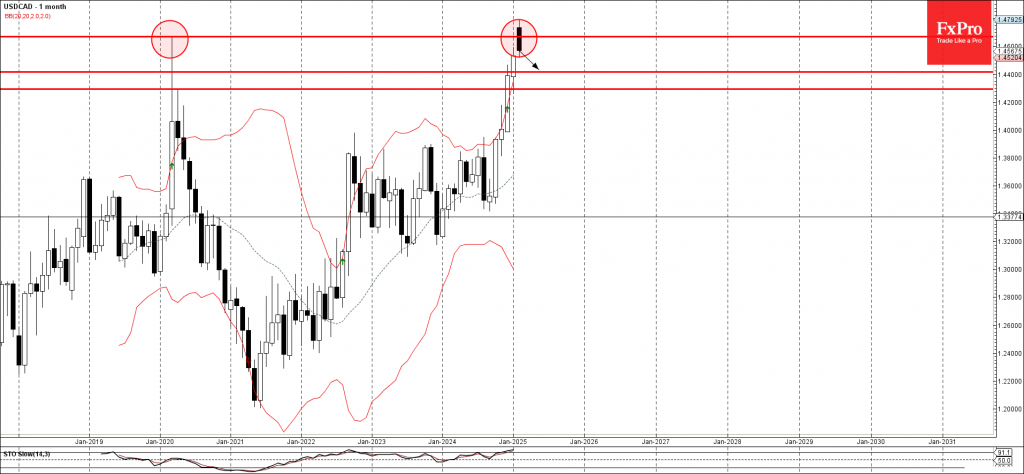

USDCAD Wave Analysis

- USDCAD reversed from the long-term resistance level 1.4670

- Likely to correct to support level 1.4400

USDCAD currency pair recently reversed down from the major long-term resistance level 1.4670, which stopped the previous sharp uptrend at the start of 2020, as can be seen from the weekly USDCAD chart below.

The resistance level was further strengthened by the proximity of the upper daily, weekly and monthly Bollinger Bands.

Given the strength of the resistance level 1.4670, the USDCAD currency pair can be expected to fall to the next support level 1.4400.

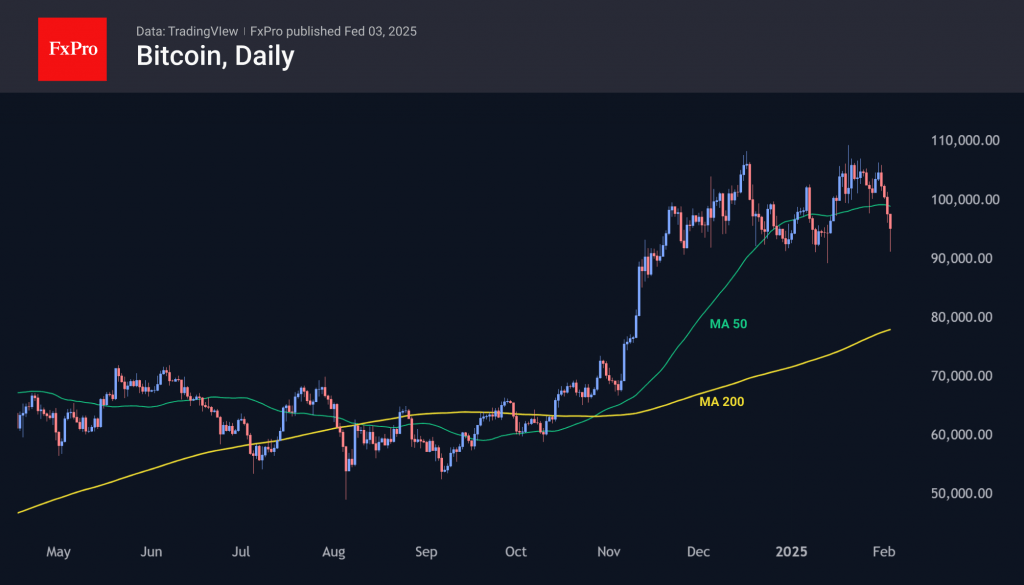

Bitcoin Fell Near Key 90K Support Zone on Tariffs, But Near-Term Outlook May be More Positive Than It Looks

Bitcoin fell below psychological 100K support and hit the lowest in almost three week, to challenge again key 90K support zone, which marks the floor of broader consolidation range.

The leading cryptocurrency remained at the back foot after hitting new record high after President Trump’s inauguration on Jan 20 and accelerated lower on announcement of implementation of trade tariffs over the weekend.

Panic in the markets followed Trump’s decision, prompting traders out of risky assets and pushing the bitcoin sharply lower after it registered the first monthly close above 100K in January.

Renewed pressure on 90K breakpoint made traders more cautious despite the price bouncing strongly after hitting new low on Monday (91054) with the downside expected to remain vulnerable as long as the price stays below 100K, as daily studies are bearishly aligned (daily Tenkan/Kijun-sen bears-cross / negative momentum.

However, growing fears of stronger destabilization of global economy by the trade wars may prompt investors into digital assets, which are not directly connected to traditional markets and can be used as safe haven assets.

In addition, President Trump’s promises on fully focusing on further liberalization of crypto markets, could play a key role, as overall positive sentiment is directly fueled by these signals.

Traders are expected to remain cautious, especially if the price remains below 100K, though mainly betting on limited dips (to be contained at 90K) to provide better buying levels.

Sustained break above 100K is needed to sideline downside risk (break to be confirmed by lift above 20DMA, 102600) and shift near-term focus higher.

Res: 99263; 10000; 101858; 102600

Sup: 96530; 93291; 941054; 89038

Crypto Market Amid US Tariffs

Market Overview

Cryptocurrency market capitalisation fell to $3.0 trillion against a peak of $3.62 trillion on Friday night. The main reason for the fall was the reaction of traditional finance to the duties imposed by the US on goods from Canada, Mexico, and China. A period of low liquidity prior to Asian trading led to a 17% fluctuation when robots and stop-orders dominated the market. Later in the European session, the market stabilised around the $3.11 trillion mark.

Bitcoin has lost more than 14% from last week’s peak, hitting a low near $91,000 at the start of trading on Monday. This collapse could lead to a break of support at the 50-day moving average. So far, bitcoin closed below it on Sunday, which intensified the sell-off. However, the close of trading on Monday will be decisive. A return above the $99,000 level could help accelerate the upside.

Bitcoin ended January up 8.7% at $101,700 and set a record high on the 20th, approaching $110,000. February is historically the best month for Bitcoin: over the past 14 years, it has risen on 11 occasions and declined only three times. The average rise was 27.6%, and the average decline was 20.3%.

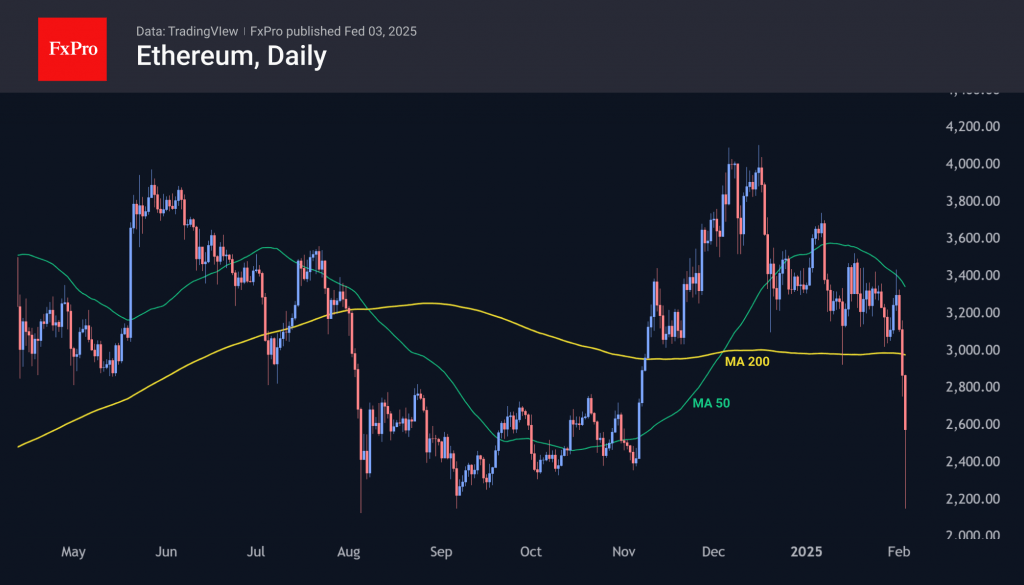

Ethereum plunged to $2,090 at the peak of the decline, its lowest since early 2024. It later stabilised around $2,550, where it stayed for about four months in the second half of last year.

News Background

According to SoSoValue data, net inflows into spot Bitcoin ETFs in the US fell to $559.8 million last week after inflows of $1.76 billion a week earlier. Cumulative inflows since bitcoin-ETFs were approved in January 2024 rose to $40.50bn.

Net outflows from US spot Ethereum-ETFs totalled $45.5m last week after two weeks of inflows. Cumulative net inflows since the ETF’s launch in July fell to $2.76bn.

Glassnode analysts note that the current bitcoin bull market is inferior in strength to previous ones but similar to the 2015-2018 events, leaving room for further gains. They identified a slowing rate of price appreciation with each new cycle, indicating the maturity and depth of the market.

The US SEC has registered a combined bitcoin and Ethereum-based spot exchange-traded fund (ETF) from Bitwise on an ‘expedited basis’. The SEC had previously approved similar instruments from Hashdex and Franklin Templeton.

Tether, the issuer of the USDT stablecoin, reported a record net profit of $13bn for 2024. In the last quarter alone, profits totalled $6bn. The company’s investments in US Treasuries reached a record high of $113bn.

Trading volume on decentralised exchanges (DEX) reached a record $564.56bn in January, hitting highs since last September. In January, the share of Solana-based AMM exchange Raydium exceeded that of Uniswap, the once perennial leader of the segment.