Sample Category Title

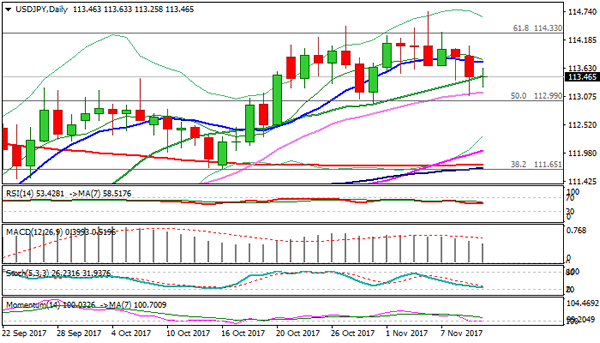

Technical Outlook: USDJPY Bounces From Thursday’s Low But Risk Remains On Downside

The pair is recovery mode on Friday and reversed some of previous day's losses, but near-term action remains biased lower.

Red daily candles in past two days weigh on near term action, as the pair is stuck around 20SMA (113.48) which was broken on Thursday's dip to 113.09, but bears failed to close below it.

Firm break below 20SMA and 112.95 (31 Oct trough) is needed to confirm reversal and trigger bearish extension towards 111.90 target (Fibo 38.2% of 107.31/114.73 ascend).

Meanwhile, extended recovery attempts are expected to be capped by 10SMA (113.75) also Fibo 38.2% of 114.73/113.09 downleg).

Res: 113.63, 113.75, 114.06, 114.34

Sup: 113.19, 113.09, 112.95, 112.50

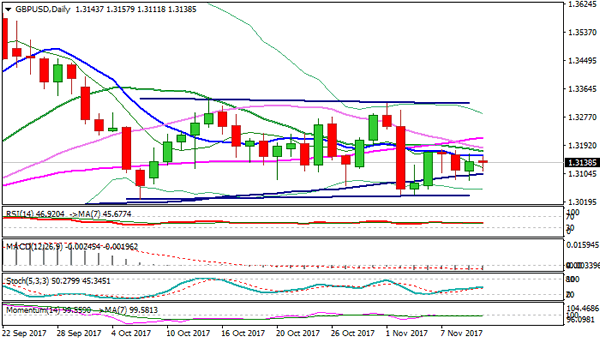

Technical Outlook: GBPUSD Trades In Extended Directionless Mode, Waiting For Direction Signals

Cable remains in holding mode on Friday, entrenched between 100SMA (1.3104) and 10SMA (1.3160). Bearish setup of 10 / 20 / 30 SMA's and daily cloud above the price weigh on near-term bias, while neutral momentum studies and converged daily Tenkan-sen/Kijun-sen show lack of signal, confirming mixed picture on daily studies. Initial direction signals will be generated on break through 100SMA at the downside or 10SMA at the upside. Loss of 100SMA support would expose double-bottom at 1.3038/26 and psychological 1.3000 support. Conversely, lift above 10 and 20SMA's (1.3160/1.3173) would risk attack at daily cloud base (1.3214) and generate stronger bullish signal on break. UK data (Manufacturing production/trade balance) and US tax plans/Brexit talks are in focus for fresh signals.

Res: 1.3160, 1.3173, 1.3182, 1.3214

Sup: 1.3104, 1.3085, 1.3057, 1.3038

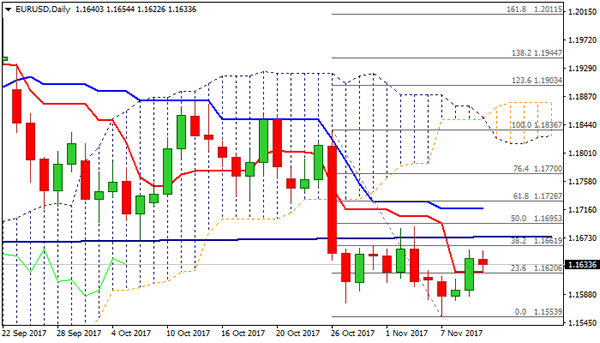

Technical Outlook: EURUSD In Tight Range As Fibo Barrier At 1.1661 Caps Recovery

The Euro is holding within tight range (1.1622/54) on Friday, following strong advance the previous day.

Close above 10SMA (1.1624) which now acts as initial support, was bullish signal, but recovery is for now limited under pivotal barrier at 1.1661 (Fibo 38.2% of 1.1836/1.1553 downleg) and weighed by thick 4-hr cloud (spanned between 1.1643 and 1.1705).

Further upside requires sustained lift above 1.1661 Fibo barrier to expose key 1.1700 resistance zone, break of which would spark stronger recovery.

However, bearishly aligned daily techs suggest limited upside action (ideally to be capped 1.1661 barrier) and keep focus at 1.1510 target (Fibo 38.2% of 1.0570/1.2092 ascend).

Res: 1.1661, 1.1674, 1.1690, 1.1705

Sup: 1.1622, 1.1585, 1.1553, 1.1510

Dollar Weakens As Senate Delays Tax-Cuts, Aussie Slips After RBA Cuts Inflation Forecasts

US tax legislation was the main headline during today's Asian session after the US Senate flagged a delay in corporate tax cuts on Thursday, pushing the dollar lower against its counterparts. Meanwhile, the aussie posted moderate losses after the RBA downgraded its forecasts on inflation.

While the US President continues his trip in Asia, his team back in the US faces increasing obstacles to turn the promised massive tax cuts – that could be Trump's first major legislative achievement since he took the presidential role in January – into law. Late on Thursday, the tax plans submitted by the Senate and the House of Representatives agreed to reduce corporate taxes to 20% from the current 35%, but disagreements were observed in key areas, including the time of implementation. The Senate version signalled that it would like to put its plan forward in 2019, contradicting the House bill (due to be voted next week) which plans to implement the legislation a year earlier. Moreover, the Senate increased the value of exemption of estate taxes, which mostly has to do with wealthy individuals and removed the deductibility of state and local taxes, something that could raise opposition among House lawmakers.

The dollar index retreated to a one week low of 94.41 on Thursday during US trading hours before edging up to 94.53 on Friday. Dollar/yen touched a ten-day low of 113.08 and continued fluctuating around that level in Asia. Dollar-denominated gold hit a three-week high of $1,288.38 per ounce.

In Australia, the RBA revised down its GDP growth and core inflation outlook in its quarterly statement on monetary policy released early today. According to the statement, the RBA policymakers expect core inflation to reach the low band of the 2-3% target in early 2019 as they consider that wage growth might rise only gradually despite a tightening labour market, hinting that a rate hike might take longer to emerge. Last August, the central bank predicted that inflation would reach 2% in the second semester of this year. Furthermore, the central bank reduced its growth forecasts to 2.75% in the mid-2018 from an earlier prediction of 3.0%. Regarding, household spending, it is expected to grow at a slower pace than before the 2008 financial crisis as consumers' incomes suffer from overloaded debt obligations.

The aussie posted short-lived losses following the release of the RBA statement, rebounding immediately on the back of a broadly weaker dollar. Aussie/dollar was last at $0.7678 (0.03% down on the day).

The kiwi went down by 0.17% to $0.6936, pressured by remarks delivered on Friday by New Zealand's Finance Minister, Grant Robertson. Robertson claimed that the successor of the central bank's governor must agree on the new government's plan to target employment and any opposition on this would put his role in question. The current RBNZ Governor, Grant Spencer, will be stepping down in March.

In the UK, Prime Minister Theresa May announced her determination to set an official date and time for the nation's departure from the EU at 2300GMT on 29 March 2019. According to the Brexit Secretary, David Davis this would weep confusion on what an “exit date means”. The piece of legislation has passed to the committee stage which will start next week. Pound/dollar was mainly flat around $1.3138 during the session.

The euro was moving sideways around $1.1632.

Next on the day, traders will focus on the industrial production figures out of the UK and on the Michigan consumer sentiment readings out of the US.

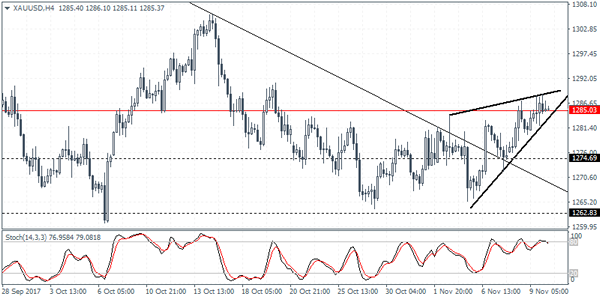

XAUUSD Intraday Analysis

XAUUSD (1285.37): Gold prices managed to rally back to the 1285 level of resistance yesterday. The subdued price action within 1285 resistance and 1262 support could be seen breaking out in the near term. However, the price needs to close above 1285 in order to maintain the bullish bias towards the 1320 level of resistance. Given the strong consolidation at the 1285 handle, we expect the possibility of a fake break out near this level which could potentially trap weak long positions. The minor rising wedge pattern near the resistance level indicates a possible decline back to 1274.70 where price could retest the breakout level from the trend line.

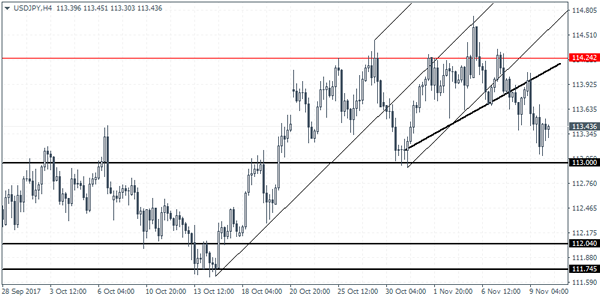

USDJPY Intraday Analysis

USDJPY (113.43): The USDJPY was seen breaking past the minor trendline. On the daily chart, the breakout from the rising wedge pattern potentially indicates the downside decline in prices. Support at 113.00 is likely to be tested in the near term. A break down below 113.00 support could, however, push USDJPY lower towards the next support level at 112.04 - 111.74 area of support. A short-term bounce to the upside could see prices rising back to the breakout level, but the bias remains poised to the downside. The bearish outlook changes only on a close above 114.24.

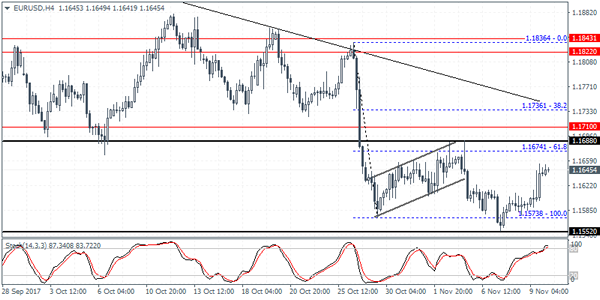

EURUSD Intraday Analysis

EURUSD (1.1645): The EURUSD maintained its bullish gains yesterday marking a second consecutive day of gains. Price action rallied to a four-day high yesterday but remained well below the 1.1674 resistance level. The bearish flag pattern breakout level is being retested, but the strong bounce off the previous low suggests that the bearish pattern might be weakening. On the 4-hour chart, however, we see some bearish signs with the Stochastics oscillator posting a hidden bearish divergence. This could possibly suggest another leg to the downside if EURUSD posts a reversal at the current levels. Overall, the ranging price action between 1.1688 - 1.1574 is most likely to be maintained.

Dollar Sentiment Hurt On Delays To Tax Reforms

The lack of any clear macroeconomic drivers has kept the markets broadly subdued. Investors sold off the US dollar as the proposed tax reforms were rumored to be delayed. The US Senate Republican plan for delaying the corporate tax cuts to 2019 saw even the equities falling back.

On the economic front, the EU commission's economic forecasts were upbeat on the GDP as the commission said that GDP would rise at the fastest pace in nearly a decade. The Euro managed to recover on the back of the positive assessment. The RBA lowered its inflation forecasts noting that inflation might not reach the lower end of the 2% band until 2019.

Looking ahead, the UK's manufacturing, construction, and industrial production numbers will be coming out today. The economic calendar is light. Later in the afternoon, the UoM's consumer sentiment and inflation expectations data will be released.

Delay In Corporate Tax Cuts Pulls Equities And The Dollar

President Donald Trump and corporate America may not be satisfied with the revised Senate Republican tax plan. The dollar and global equities received a hit on news that Republican senators are likely to delay the introduction of corporate tax cuts until 2019. The reaction in markets wasn't a surprise, given that investors have been pricing in a lot of good news and further pullback may continue for a couple of days or weeks, as many stocks look overbought at the moment.

The Senate wants to maintain the seven tax brackets, rather than the four proposed by the house. They also want to tax foreign profits held by offshore U.S. companies at a different rate. However, the timing of the corporate tax cuts will likely determine how markets move for the remainder of 2017.

The dollar traded in very tight ranges early Friday after falling on Thursday. While the delay in tax cuts isn't good news for the U.S. currency, the rise in U.S. Treasury yields prevented the dollar from falling further. The U.S. economic calendar is light today with only November's Michigan Consumer Sentiment Index due for release, so I don't expect much action unless the Senate reveals a detailed tax reform plan.

Sterling is the only currency in play, with manufacturing and industrial production, trade balance, and NIESR GDP estimates, due for release later today. Brexit negotiations also resumed on Thursday, but according to officials there was no major breakthroughs. If talks in Brussels end in a similar way to previous negotiations, expect Sterling gains to remain capped.

Oil prices were also moving in narrow ranges after rallying sharply at the beginning of the week. High demand, falling inventories, and confidence that OPEC will extend production cuts, will likely keep the prices elevated in the short run, but the geopolitical risk premium due to tensions in the Middle East, has undoubtedly been responsible for a large portion of the recent surge in prices. I still believe that current fundamentals aren't sufficient to keep Brent above $60-$62, however geopolitical tensions will continue to be the main driver in the days and weeks to come.

Currencies: USD In The Defensive As Tax Bill Might Undershoot Expectations

Sunrise Market Commentary

- Rates: Unusual correlation between stocks/bonds unlikely to persist

Tension on Asian stock markets eased overnight, but we think that the equity correction has further to go from a technical point of view. If so, it remains a strange combination to see both core bonds and stocks sell-off simultaneously. The end of the refinancing operation, doubts on US tax reforms and the weekend ahead generally favour some cautiousness as well. - Currencies: USD in the defensive as tax bill might undershoot expectations

Yesterday, there were some strange correlations on global markets, including the FX market. For new, we assume that the overall context is slightly negative for the dollar. A risk-off decline of USD/JPY might be less pronounced than is usually the case. The euro might remain relatively well supported. Brexit headlines might remain slightly GBP-negative

The Sunrise Headlines

- US stock markets corrected around 0.5% lower yesterday. They tried to erase opening weakness which spread from Asia/Europe, but failed on headlines that the US Senate aims to delay tax reforms. Asian markets are mixed overnight with Japan underperforming and China outperforming.

- Senate Republicans' proposal to rewrite the tax code breaks significantly with the one crafted by the House GOP confronting party leaders with dozens of differences to reconcile and little time before the year-end deadline.

- The House Ways and Means Committee approved revisions to the GOP tax legislation that trimmed the bill's cost while providing more tax relief to owners of partnerships, limited liability companies and other so-called pass-throughs.

- The EU is demanding Britain accept that Northern Ireland may need to remain inside the European customs union and single market after Brexit in order to avoid “a hard border on the island of Ireland”.

- Australia's central bank has sliced its forecasts for core inflation which is seen lurking under its long-term target band for another two years, a strong signal that interest rates won't rise for a long time to come.

- The ECB can tighten monetary policy more decisively once inflation is on a clear path towards the target, leaving behind its gradualist approach, Governing Council member Lane told German business newspaper Boersen-Zeitung.

- Today's eco calendar contains UK industrial production and University of Michigan consumer confidence. Barnier and Davis hold a press conference on Brexit talks. ECB Mersch is scheduled to speak

Currencies: USD In The Defensive As Tax Bill Might Undershoot Expectations

Dollar ceded slightly ground on US tax plan

Global markets were spooked by an unexpected uptick of volatility on equity markets yesterday. At the same time, Bunds and, to a lesser extent Treasuries, came under pressure. The dollar and the euro both received interest rate support, despite the equity correction. This prevented a meaningful gain of the usual safe havens (Japanese yen, Swiss franc). Later in the session, the dollar ceded ground as more details on the Senate tax plan were aired. EUR/USD finished the session at 1.1642 (from 1.1595). USD/JPY finished the session at 113.47.

Overnight, most Asian equity indices show modest losses. China outperforms. Japan underperforms again. The yen maintains yesterday's gains, but the Japanese currency doesn't profit from the additional equity losses overnight. EUR/USD holds near yesterday's closing levels in the 1.1650 area. So, the US currency remains slightly in the defensive. The RBA expects underlying inflation to remain below its inflation target band till early 2019. This suggest that a policy rate hike isn't on the cards anytime soon. AUD/USD (currently 0.7685 area) trades within reach of the recent lows, but there are few additional losses.

Today's eco calendar remains uninspiring with only University of Michigan consumer confidence for November. Consensus expects a small increase in both the headline, from 100.7 to 100.9, and expectations, from 90.5 to 91, components of the report. Both indices trade near/at decade-highs. ECB Mersch is scheduled to speak, but probably won't touch on monetary policy.

Global markets (including FX) showed some unusual links yesterday. The global risk-off sentiment/rise in volatility coincided with a rise in core (especially German) yields. This rise in German (and to a lesser extent in US yields) supported the euro and the dollar against the usual FX safe havens. Uncertainty, on the tax bill was a negative for the dollar. Today, the Michigan consumer confidence might be slightly supportive for the dollar. However, the focus of markets is elsewhere. Yesterday's price action suggests that the developments in core interest rate markets are currently more important for trading in the major FX cross rates rather than global risk sentiment. Regarding the latter, it isn't sure that the sell-off will continue, but we assume that equity enthusiasm has cooled a bit short-term. This will probably remain a negative for USD/JPY even as the pace of the decline might be less pronounced than is usually the case. The absolute low level of German/European interest rates makes that the euro will probably receive interest rate support in case of a risk-off correction. Uncertainty on the US tax plan might be slightly USD negative, too

In this context we change our day-to-day bias for EUR/USD from negative to neutral. For now, there are also no indications of selling pressure on EUR/JPY due to the global risk-off sentiment.

From a technical point of view, EUR/USD dropped below 1.1670/62 support, the subsequent follow-through price action occurred very slow. Still the pair dropped to a new post-ECB low on Tuesday. A sustained break would confirm that the recent EUR/USD uptrend is broken. EUR/USD 1.1423 (38% retracement of 2017 rise) is the next downside target on the charts. USD/JPY's momentum was positive in past months. The pair regained 110.67/95 resistance and tested the 114.49 MT range top, but the attempt failed. A sustained break would improve the technicals. We remain cautious to preposition for further USD/JPY gains. This week's price action remains unconvincing.

EUR/USD: euro rebounds on higher EMU yields, despite risk-off

EUR/GBP

Brexit continues to dominate GBP trading

Sterling felt additional selling pressure yesterday. There were no important eco data in the UK. Investors kept a close eye on the next round of official Brexit negotiations that started in Brussels. EU negotiators were said to maintain a very cautious approach as they tried to ponder the consequences of the political turmoil in the UK. The overall risk-off context is usually a negative for sterling, too. EUR/GBP closed the session at 0.8856 (from 0.8840). Cable finished the session at 1.3145. The pair received some support from overall USD weakness.

The UK September production data, the trade balance and the NIESR GDP estimate will be published today. Production is expected to rise at a modest pace (0.3% M/M). The trade deficit is expect to narrow after a bad figure the previous month. We don't expect the data to bring additional negative news for sterling. Markets will be more focused on the Brexit negotiations in Brussels. Press headlines suggest that the negotiations on the border between Ireland and Northern Ireland are more difficult than previously expected. This might be a slightly additional negative for sterling. A risk-off context also doesn't help sterling. So, we maintain an cautious upward bias for EUR/GBP.

MT technical: Sterling rebounded in September as the BoE prepared markets for a rate hike. This rebound ran into resistance as markets anticipated that any rate hikes would be very gradual and limited. This view was confirmed at last week's BoE policy meeting. EUR/GBP currently trades in a 0.8733/0.9033 consolidation range. A downside test of this range was rejected last week. We maintain the view that the 0.8733 -0.8652 support area will be tough to break in a sustainable way. A EUR/GBP buy-on-dips approach is favoured. EUR/GBP 0.9023/33 is the first important resistance

EUR/GBP: off recent low, but no sustained rebound, yet