Sample Category Title

RBA Slashed Australia’s Growth And Inflation Forecasts

For the 24 hours to 23:00 GMT, the AUD traded flat against the USD and closed at 0.7679.

LME Copper prices declined 0.5% or $35.0/MT to $6777.0/MT. Aluminium prices declined 1.2% or $25.5/MT to $2078.0/MT.

In the Asian session, at GMT0400, the pair is trading at 0.7688, with the AUD trading 0.12% higher against the USD from yesterday's close.

Earlier today, the Reserve Bank of Australia (RBA), in its quarterly statement on monetary policy, slightly lowered Australia's economic growth outlook, while signalling only a gradual rise in headline inflation. The Australian economy is now expected to post an economic growth of 2.75% in mid-2018, from an earlier projection of 3.0%, while inflation is estimated to rise to 2.0% by June 2018 and 2.25% by the end of 2019. The central bank also warned that outlook for household income growth remains a significant uncertainty in its efforts to forecast consumption growth.

The pair is expected to find support at 0.7661, and a fall through could take it to the next support level of 0.7633. The pair is expected to find its first resistance at 0.7705, and a rise through could take it to the next resistance level of 0.7721.

Next week, traders would focus on Australia's unemployment rate, NAB business confidence and Westpac consumer confidence data.

The currency pair is showing convergence with its 20 Hr moving average and trading above its 50 Hr moving average.

Euro-Zone’s Economy To Continue Its Strong Momentum In The Second Half Of 2017: ECB’s Economic Bulletin

For the 24 hours to 23:00 GMT, the EUR rose 0.41% against the USD and closed at 1.1642.

According to the European Central Bank's (ECB) latest economic bulletin, the solid and broad-based economic recovery in the common currency region is likely to continue unabated into the second half of this year, aided by upswing in business investment and robust domestic demand.

Meanwhile, the European Commission, in its Autumn Forecast report, lifted the Euro-zone's 2017 growth forecast, predicting the fastest economic expansion in a decade. The commission now expects the single currency-bloc to grow 2.2% in 2017, up from 1.7% forecasted earlier in May.

Separately, Germany's seasonally adjusted trade surplus widened more-than-expected to €24.1 billion in September, compared to market consensus for a surplus of €22.3 billion. The nation had reported a revised trade surplus of €20.1 billion in the previous month.

The greenback lost ground against its major counterparts, amid lingering uncertainty over US tax reforms after the Senate revealed that its proposed tax plan would push the long-awaited corporate tax cuts to 2019.

On the macro front, first time claims for the US unemployment benefits climbed more-than-anticipated to a level of 239.0K in the week ended 04 November, compared to a level of 229.00 K in the previous week. Markets were anticipating initial jobless claims to rise to a level of 232.00 K. Further, the nation's seasonally adjusted final wholesale inventories advanced 0.3% on a monthly basis in September, confirming the preliminary print. In the previous month, wholesale inventories had registered a revised rise of 0.8%.

In the Asian session, at GMT0400, the pair is trading at 1.1649, with the EUR trading 0.06% higher against the USD from yesterday's close.

The pair is expected to find support at 1.1608, and a fall through could take it to the next support level of 1.1566. The pair is expected to find its first resistance at 1.1673, and a rise through could take it to the next resistance level of 1.1696.

Amid a lack of major macroeconomic releases in the Euro-zone today, investors will look forward to the US flash Michigan consumer sentiment index for November, slated to release later today.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Trade Idea : EUR/USD – Stand aside

EUR/USD - 1.1637

Most recent candlesticks pattern : N/A

Trend : Down

Tenkan-Sen level : 1.1646

Kijun-Sen level : 1.1622

Ichimoku cloud top : 1.1595

Ichimoku cloud bottom : 1.1585

New strategy :

Stand aside

Position : -

Target : -

Stop : -

The single currency rebounded after finding renewed buying interest at 1.1600, suggesting a temporary low has been formed at 1.1554 earlier this week, hence upside risk is seen for retracement of recent decline and gain to 1.1662-65 (38.2% Fibonacci retracement of 1.1837-1.1554) is likely, however, reckon upside would be limited to resistance at 1.691-96 (50% Fibonacci retracement) and bring retreat later.

On the downside, below 1.1600 would suggest an intraday top is formed and revive bearishness for retest of 1.1554, break there would extend recent decline to 1.1520-25, then 1.1500 but oversold condition should prevent sharp fall below latter level and reckon 1.1470-75 would hold. As near term outlook is mixed, would be prudent to stand aside for now.

UK And The European Union Resumed Brexit Negotiations In Brussels

For the 24 hours to 23:00 GMT, the GBP rose 0.22% against the USD and closed at 1.3143.

Yesterday, the sixth round of Brexit negotiations begun in Brussels with little hopes of significant progress.

In the Asian session, at GMT0400, the pair is trading at 1.3147, with the GBP trading slightly higher against the USD from yesterday’s close.

The pair is expected to find support at 1.3099, and a fall through could take it to the next support level of 1.3052. The pair is expected to find its first resistance at 1.3180, and a rise through could take it to the next resistance level of 1.3214.

Going ahead, market participants would keep a close watch on Britain’s industrial and manufacturing production, coupled with the nation’s total trade balance and construction output data, all for September, scheduled for release in a few hours. Later in the day, the release of NIESR GDP estimate for the three months ended October, will garner significant amount of investor attention.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

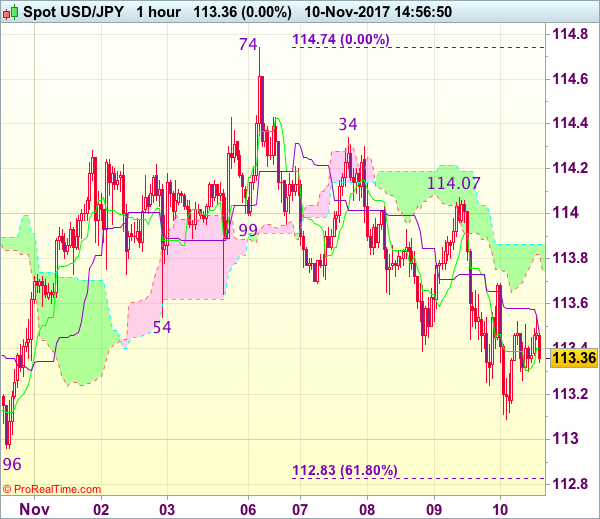

Trade Idea : USD/JPY – Hold short entered at 114.00

USD/JPY - 113.38

Most recent candlesticks pattern : N/A

Trend : Near term down

Tenkan-Sen level : 113.40

Kijun-Sen level : 113.47

Ichimoku cloud top : 113.87

Ichimoku cloud bottom : 113.82

Original strategy :

Sold at 114.00, Target: 113.00, Stop: 114.00

Position : - Short at 114.00

Target : - 113.00

Stop : - 114.00

New strategy :

Hold short entered at 114.00, Target: 113.00, Stop: 113.70

Position : - Short at 114.00

Target : - 113.00

Stop : - 113.70

As the greenback recovered after falling to 113.09 yesterday, suggesting consolidation would be seen, however, reckon upside would be limited to 113.65-70 and bring another decline later, below said support at 113.09 would extend the fall from 114.74 top to previous support at 112.96 but break there is needed to add credence to this view, bring further subsequent selloff to 112.60 but support at 112.30 should hold from here due to near term oversold condition.

In view of this, we are holding on to our short position entered at 114.00. Only above resistance at 114.07 would abort and signal the retreat from 114.74 has ended instead, bring a stronger rebound to 114.34, then retest of this level, above there would revive bullishness and extend recent rise from 107.32 to 115.00.

Japan’s Tertiary Industry Index Further Eased In September

For the 24 hours to 23:00 GMT, the USD declined 0.38% against the JPY and closed at 113.44.

In the Asian session, at GMT0400, the pair is trading at 113.40, with the USD trading a tad lower against the JPY from yesterday's close.

Early morning data showed that Japan's tertiary industry index dropped 0.2% on a monthly basis, in September, more than market expectations for a fall of 0.1%. In the previous month, the index had declined by a revised 0.1%.

The pair is expected to find support at 112.98, and a fall through could take it to the next support level of 112.57. The pair is expected to find its first resistance at 113.92, and a rise through could take it to the next resistance level of 114.45.

Looking forward, investors would closely monitor Japan's flash 3Q GDP numbers, set to release next week, to gauge strength in the Japanese economy.

The currency pair is showing convergence with its 20 Hr moving average and trading below its 50 Hr moving average.

Switzerland’s Unemployment Rate Remained Unchanged In October

For the 24 hours to 23:00 GMT, the USD declined 0.58% against the CHF and closed at 0.9941.

In economic news, Switzerland's seasonally adjusted unemployment rate remained steady at 3.1% in October, in line with market expectations.

In the Asian session, at GMT0400, the pair is trading at 0.9945, with the USD trading marginally higher against the CHF from yesterday's close.

The pair is expected to find support at 0.9905, and a fall through could take it to the next support level of 0.9866. The pair is expected to find its first resistance at 1.0001, and a rise through could take it to the next resistance level of 1.0058.

With no macroeconomic releases in Switzerland today, market participants would focus on global macroeconomic factors for further direction.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

Canada’s New House Price Index Climbed In September

For the 24 hours to 23:00 GMT, the USD declined 0.39% against the CAD and closed at 1.2681.

Macroeconomic data showed that Canada's new house price index rose 0.2% MoM in September, meeting market expectations. The index had registered a gain of 0.1% in the previous month.

In the Asian session, at GMT0400, the pair is trading at 1.2670, with the USD trading 0.09% lower against the CAD from yesterday's close.

The pair is expected to find support at 1.2646, and a fall through could take it to the next support level of 1.2621. The pair is expected to find its first resistance at 1.2716, and a rise through could take it to the next resistance level of 1.2761.

Investors would direct their attention to Canada's crucial inflation figures, set to release later next week.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

UK Data And Brexit Negotiations Key On Friday

- Will Investors Shake Off Thursday's Weakness?

- Brexit Negotiations and UK Data Eyed;

- Quiet Session Expected as US Celebrates Veterans Day;

Financial markets are looking a little flat ahead of the European open on Friday, following a similar session in Asia overnight and as traders try to shake of Thursday's weakness.

The US dollar is recovering a little this morning, coming on the back of moderate losses on Thursday as the Senate proposed delaying the corporate tax cut until 2019, while making other changes to the tax bill in the process. While changes to the bill were expected, those proposed by the Senate will likely not sit well with Donald Trump and I expect further modifications will happen before anything is passed.

The delay in the corporate tax cut may not be one of those that's changed though, with various people including Treasury Secretary Steve Mnuchin appearing not too concerned about it. While markets have responded negatively in the near-term, I don't think this is too big a deal and it's notable that losses in the dollar were not too heavy and while equity markets suffered rare modest losses, the dips were still bought.

This bodes well for a rally that hasn't really been tested of late. Currently, futures suggest both Europe and the US will open flat on Friday which would suggest for now at least that there's no hangover from Thursday's selling. Of course this may change after markets open, although once again today there's very little on the calendar today.

There will be a particular focus on the UK on Friday, with manufacturing and industrial production figures due out this morning and a GDP estimate for the past three months from NIESR this afternoon. Meanwhile, Brexit negotiations will continue as both sides seek to make sufficient progress on the exit bill, citizens' rights and the Northern Ireland border.

That said, given how past negotiations have gone I'm not optimistic that the gap between the two sides will be closed yet. With Theresa May's looking very vulnerable at home and with the EU not wanting a change of leadership at this stage, it's possible that the Prime Ministers weakness may help the negotiations progress in order to give her a domestic boost. That said, the EU isn't going to be overly charitable when it comes to May's cause and so the UK will have to make more effort on the bill before any progress can be made.

It's worth noting that while markets are all open today, it is the Veterans Day bank holiday in the US which is likely to have a significant impact on trading volume and could contribute to quiet trade at the end of the week.

Market Update – Asian Session: Nikkei 225 Remains Volatile Amid Options Settlement

Asia Summary

Following the negative leads from the US session, Asian equity markets opened generally lower. The Nikkei 225 has remained volatile on the session, following the trading action seen on Thursday. November options for the index settled at 22,531.

Large banks in Japan are generally weaker, ahead of their earnings reports which are expected starting next week. The TOPIX Securities brokers index has dropped over 1%.

There has been some weakness in Japanese tech names, after the S&P 500 Technology sector declined by over 0.7% on Thursday.

Shares of Toshiba have declined by over 4%, following reports that the company is considering raising capital. Also, in the tech sector Softbank has declined by over 1.5%. Bucking the trend, semiconductor firm Sumco has gained over 8%, after reporting its financial results and outlook. In Hong Kong, the Hang Seng Information Technology index is higher by over 0.5%.

At the same time, the Hang Seng Energy index has declined by over 0.4%, while Australia’s ASX 200 Energy index has dropped over 1%. In the materials space, BHP has declined by over 2% and the overall ASX 200 Resources index is lower by more than 1.3%.

Key economic data

(AU) RESERVE BANK OF AUSTRALIA (RBA) QUARTERLY STATEMENT ON MONETARY POLICY (SOMP): LOWERS INFLATION FORECASTS THROUGH 2019: GDP GROWTH FORECASTS LITTLE CHANGED; Sees sub 2% core inflation until mid-2019 (**Note: RBA has a 2-3% target range for inflation)

Speakers and Press

China

(CN) China Finance Ministry: To expand corporate tax rate cuts for high tech services firms nationwide

Ford: To export ~$10B in vehicles and auto parts from North America to China

(CN) China to remove foreign ownership limit in domestic banks; raises the foreign stake ceiling in brokerages to 51%; To raise foreign stake ceiling in life insurance companies to 51%; o also, raise the foreign stake ceiling in fund management and futures companies

Other

(JP) Nikkei 225 Nov options settle at 22,531

(NZ) New Zealand Finance Min Robertson: Dual RBNZ mandate may see looser policy in some instances, central bank has role to play in maximizing employment; Expanded RBNZ monetary policy committee won't be a 'circus'; Government committed to 1-3% inflation band; RBNZ's 2% inflation focus could be up for discussion.

(US) Joint Tax Committee: US Senate Tax Proposal is within $1.5T ceiling on deficit expansion

(US) The Senate tax plan is said to just meet the $1.5T budget limit and the plan is expected to cost $1.496T over 10 years, according to a financial press report.; The report adds that the plan would repeal the interest deduction on home equity loans and eliminate deductions for personal exemptions.

Asian Equity Indices/Futures (00:30ET)

Nikkei -0.9%, Hang Seng +0.2%, Shanghai Composite flat, ASX200 -0.3%, Kospi -0.3%

Equity Futures: S&P500 flat ; Nasdaq -0.1% , Dax +0.1% , FTSE100 +0.1%%

FX ranges/Commodities/Fixed Income (00:30ET)

EUR 1.1642-1.1654; JPY 113.26-113.51; AUD 0.7664-0.7689; NZD 0.6920-0.6957

Aug Gold -0.2% at 1,285/oz; Aug Crude Oil -0.2% at $57.05/brl; Sept Copper -0.2% at $3.085/lb

GLD SPDR Gold Trust ETF daily holdings flat at 843.1 metric tons

(CN) PBOC sets yuan reference rate at 6.6282 v 6.6325 prior(CN) PBoC OMO: CNY80B v CNY40B injected in 7, 14 and 63-day reverse repos prior; Net injection CNY50B

(AU) Australia sells A$900M in 2.75% Nov 2027 bonds, avg yield 2.6201%, bid to cover 3.46x

(NZ) New Zealand sells NZ$100M in Sept 2040 inflation-indexed bonds, avg yield 2.1550%, implied bid to cover 3.01x

US markets on close: Dow -0.4%, S&P500 -0.4%, Nasdaq -0.6%, Russell -0.5%

Best Sector in S&P500: Energy +0.3%

Worst Sector in S&P500: Industrials -1.3%

At the close: VIX 10.50 (+0.72pts); Treasuries: 2-yr 1.637% (-1bp), 10-yr 2.338% (flat), 30-yr 2.814% (+2bps)

US Market Summary

US stocks opened under notable pressure as a variety of asset classes exhibited signs of modest liquidation. The VIX bumped up ~15% and bond yields rose as equity markets moved lower. Consternation surrounding Brexit negotiations and a delay in corporate tax cut implementation in the Senate tax bill appeared to be the underlying current, along with an onslaught of corporate debt/equity issuance announcements ahead of year end. The Dollar index fell as the Senate tax bill details circulated, but as the day wore on, markets pared losses a bit following comments from some senators that the final bill could still include an immediate corporate tax cut.

US Afterhours Movers

HTZ Reports Q3 $1.42 v $1.47e, Rev $2.60B v $2.58Be; International car rental rev $728M, +7% y/y; +11.4% afterhours

JWN Reports Q3 $0.67 v $0.63e, Rev $3.63B v $3.60Be; Narrows FY17 $2.85-2.95 v $2.95e, Rev +4%, SSS approx ~0% (prior FY17 $2.85-3.00, Rev +4%, SSS ~0%); -3.2% afterhours