Sample Category Title

Canada’s Labour Market Still Gradually Softening Ahead of Looming Tariff Threat

Canada’s labour market likely continued to underperform in January as it has consistently shown a more pronounced deterioration than the U.S. job market.

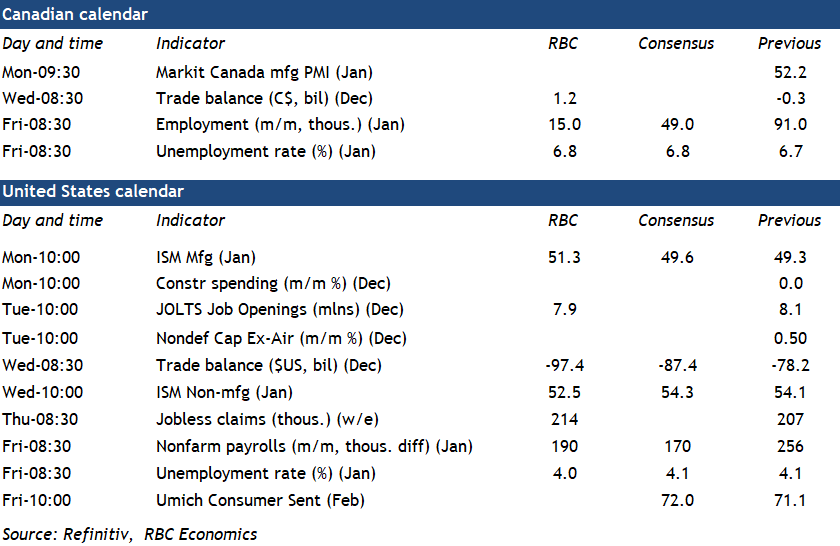

We expect Canada added 15K jobs in January, but with a larger increase in the labour force nudging the unemployment rate higher. We expect it will rise to 6.8%, partially retracing a pullback to 6.7% in November from 6.9% in October but still up more than a percentage point from a year ago. Canadian household spending has shown signs of life, but sentiment among businesses remains lethargic as firms continue to face challenges with spare capacity after a prolonged string of slow demand growth. Companies reported limited hiring intentions for the year ahead in the Q4 Bank of Canada Business Outlook Survey.

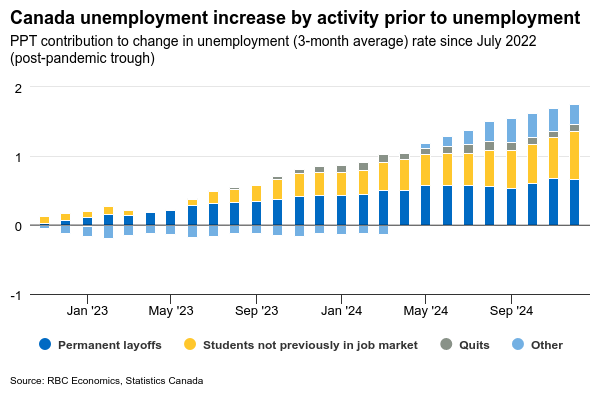

Hiring demand has fallen sharply – job openings were still running 23% below year-ago levels in November. Wage growth has shown signs of slowing and smaller increases in wages in job postings argue for further slowing ahead. The rise in the unemployment rate to-date has been driven more than usual by students and new job seekers, but layoffs have still accounted for almost 40% of the increase in the unemployment rate over the last two and a half years.

Over the past year, job gains have been largely concentrated in the services sector – almost half from public sector education and healthcare jobs. We expect this will continue as the manufacturing sector faces weaker demand and threats of disruption from tariffs. With weaker population growth expected from reduced immigration targets, the pace of job creation is expected to continue to slow throughout 2025.

U.S. labour markets, however, continue to look solid by comparison. We expect January payroll numbers to show the U.S. added 190K jobs on Friday, and for the unemployment rate to tick down to 4.0%. We continue to expect resilience in the U.S. jobs market through 2025 but hiring rates continue to fall, indicating tight conditions have eased. The pace of job creation will be challenged over the medium term by an ageing population and slower population growth (made worse if mass deportations of migrants materializes).

Week ahead data watch

We expect the U.S. trade deficits to widen to $97.4B in December. According to the advance economic indicator report, the goods deficit widened by $18.6B from last month, mainly driven by higher imports and weaker exports.

We expect Canadian exports expanded by 1.9% in December, in line with stronger rail carloading data. We expect imports to dip slightly given motor vehicle shipments weakened.

Week ahead – Nonfarm Payrolls and BoE Decision in the Spotlight

- Dollar continues to be driven by tariff headlines.

- Nonfarm Payrolls to reshape Fed expectations.

- BoE to cut by 25bps; focus to fall on forward guidance.

- Canadian jobs report key for BoC’s next move.

In the mercy of tariffs

The US dollar has staged a recovery this week, corroborating the notion that the latest pullback on news that Trump may adopt a softer stance on tariffs than his pre-inauguration rhetoric suggested, was just a corrective phase.

Tariffs remained the main driver, with Wednesday’s Fed decision adding some extra fuel to the rebound. After Colombia succumbed to Trump’s threats, investors’ concerns were amplified again, with many perhaps thinking that the US President may harden his rhetoric to get what he wants from the rest of the world. And indeed, Trump himself confirmed that view after he rejected reports that US Treasury secretary Scott Bessent is pushing for only 2.5% tariffs that would be gradually lifted to 20%, saying that tariffs would be “much bigger.”

In the shadows of the first imposition of 25% tariffs on Canadian and Mexican imports on February 1, the Fed decided on Wednesday to keep interest rates unchanged. At the press conference following the decision, Fed Chair Powell acknowledged signs of progress in reducing inflation, adding though that “non-market” prices remain stubbornly high and stressing that they are in no hurry to make further adjustments. They will wait for more clarity on the economic front as well as on government policy.

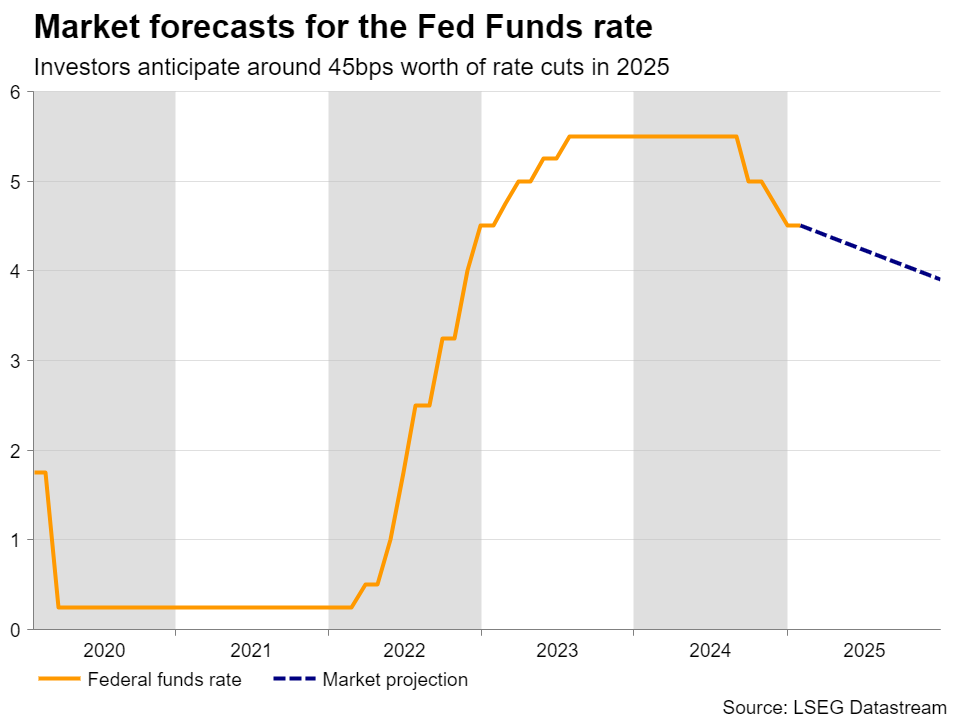

From around 50bps worth of rate reductions for this year, Fed fund futures are now pointing to 45bps as investors lifted only slightly the implied rate path. The next quarter-point reduction is still nearly fully priced in by June.

Nonfarm Payrolls enter the limelight

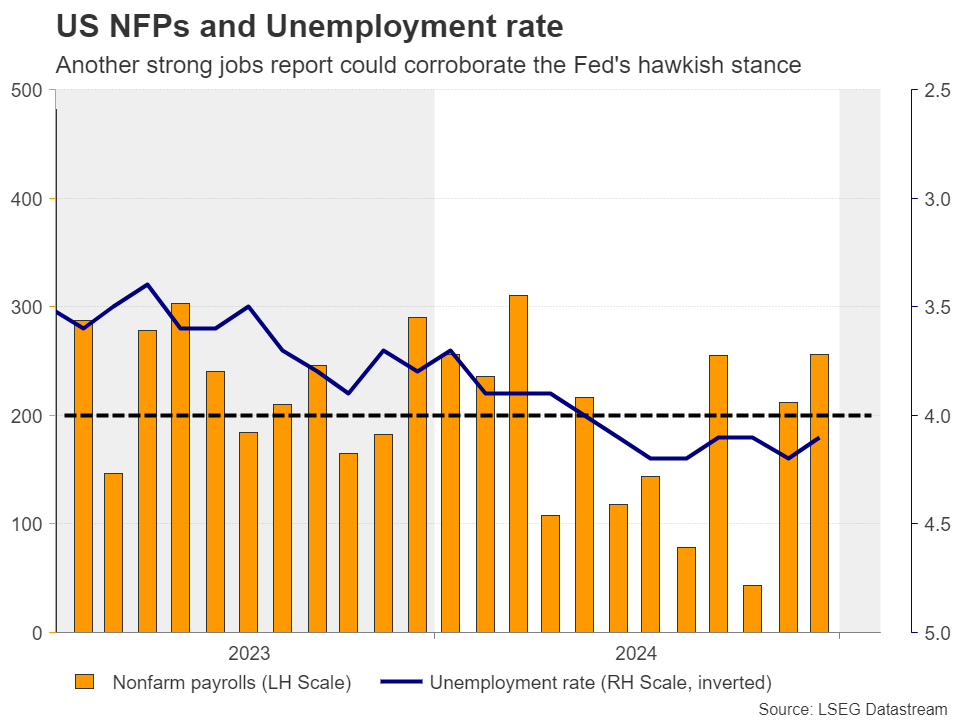

With all that in mind, attention next week is likely to fall on the NFP employment report for January. Powell noted that further labor market weakening is not needed for the inflation target to be met as the path for continued disinflation remains intact. However, he did not mention what will happen in the case of unexpected labor market tightening.

In December, the economy added 256k jobs, with average hourly earnings ticking down, but remaining elevated close to 4.0% y/y. Another round of strong employment and wage growth could intensify concerns about a resurgence of inflation in the months to come, especially if Trump kicks off the tariff game on February 1. Market participants are likely to start doubting again whether two rate cuts will be needed this year, which could allow the US dollar to extend its latest recovery.

The ISM manufacturing and non-manufacturing PMIs on Monday and Wednesday, as well as the ADP private employment report on Wednesday will also be closely monitored ahead of Friday’s NFP data.

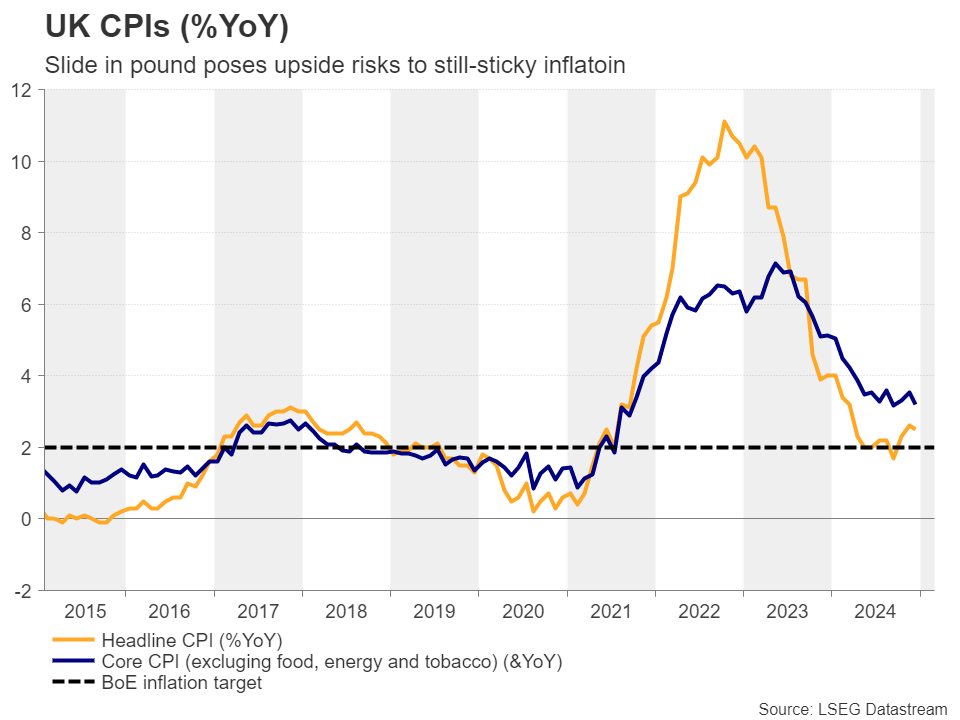

Will the BoE opt for a hawkish cut?

After the BoJ, the Fed, the ECB and the BoC, it will be the BoE’s turn to hold its first policy decision for 2025. Following the concerns over the sustainability of the new government’s fiscal plans, where UK bonds and the pound tumbled on fears of a Truss 2.0 budget crisis, investors became more convinced that a rate cut would be appropriate at this gathering.

Taking also into account the cooler-than-expected CPI numbers for December and the sluggish UK growth, investors are now penciling in around a 90% chance of a quarter-point rate cut at this gathering, while anticipating nearly another two by the end of the year.

That said, both the headline and the core inflation rates remain above the Bank’s objective of 2%, with the latter standing at 3.2% y/y. What’s more, although the surge in bold yields was largely reversed, the pound recovered only a portion of its losses. It is actually the worst performing major currency so far this year, posing upside risks to UK inflation.

Therefore, even if the well-anticipated rate cut is delivered, it may be a hawkish cut, with the Bank revising up its inflation projections, especially with rent inflation remaining stagnant at 7.6% y/y and services inflation still above 4.0% y/y. Officials may signal that they will take their decisions meeting by meeting, avoiding to pre-commit to any future rate cuts. This may disappoint those expecting another two reductions this year and thereby allow the pound to gain some more ground.

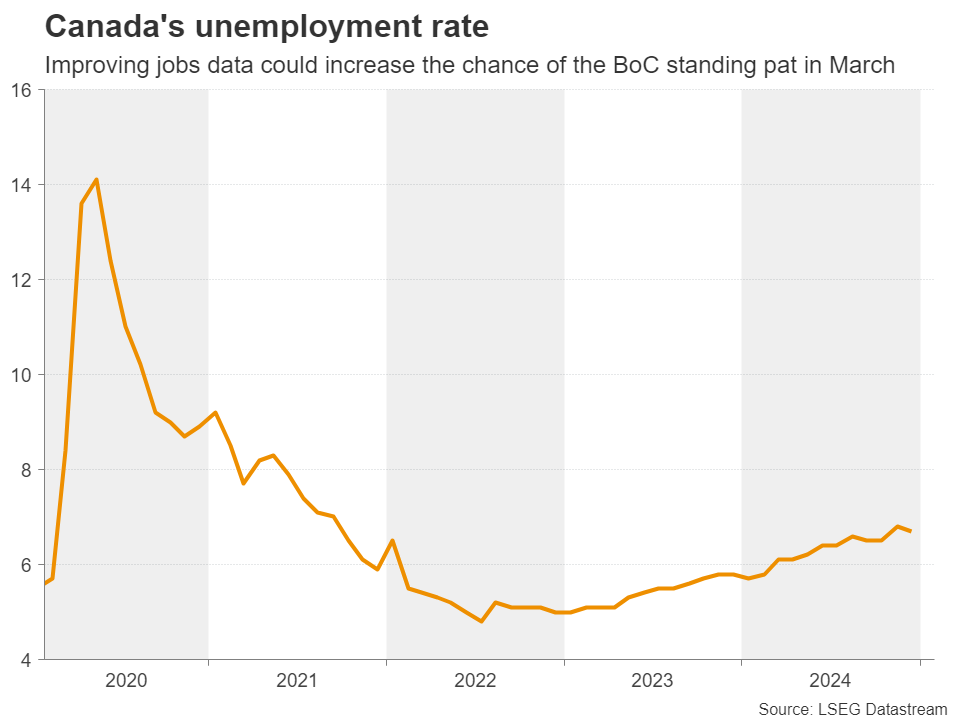

Will the jobs data allow the BoC to take the sidelines?

At the same time with the US jobs data, Canada releases its own employment report for January. This week, the Bank of Canada trimmed interest rates by another 25bps and revised down its growth forecasts, noting that they are concerned about US tariffs.

However, they also added that tariffs could also stoke persistently high inflation, which led market participants to pencil in around a 50% probability for policymakers to take the sidelines at the next policy gathering in March.

In other words, the BoC will find itself between a rock and a hard place and Friday’s jobs report may help tilt the scale towards a pause or another rate cut, depending on whether it will come in strong or soft.

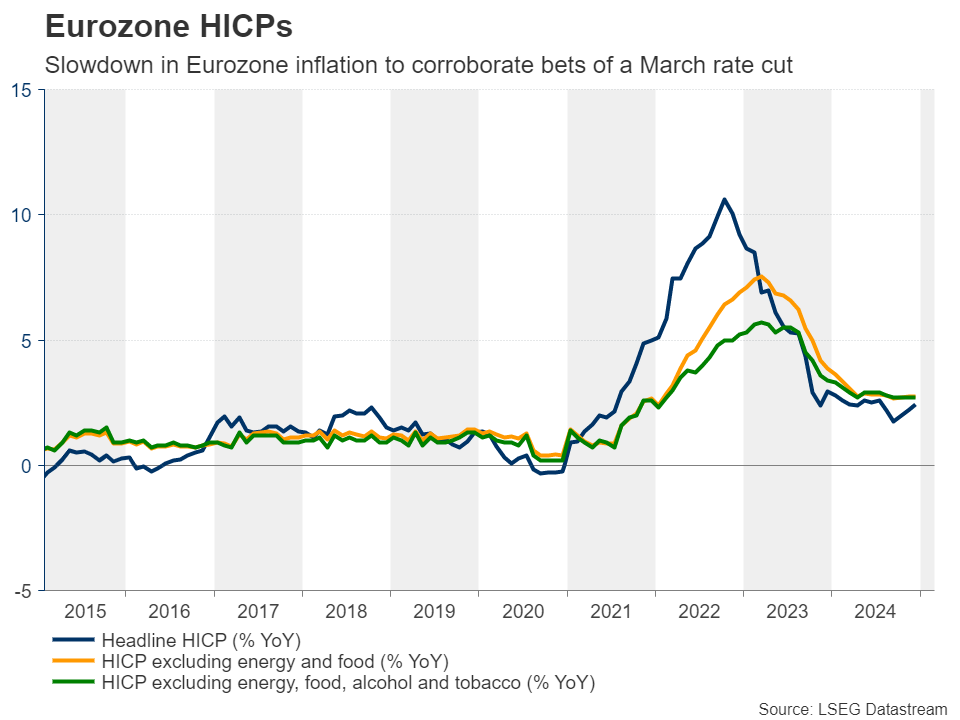

Eurozone CPIs, NZ employment and Japan’s wages

Flying from Canada to the Eurozone, the ECB also decided to reduce interest rates this week, noting that the disinflationary process is well on track and that the economy is still facing headwinds. In the statement, it was noted that the Bank is still not pre-committing to a particular rate path. At the post-decision conference, President Lagarde said that interest rates are still in restrictive territory and that there was no discussion on whether it's time to stop reducing rates.

The market was quick to price in around an 85% chance for another quarter-point cut in March and should Monday’s flash CPI data reveal cooling inflation, that probability could go even higher, thereby weighing on the euro. Eurozone’s retail sales are also on next week’s agenda.

Elsewhere, during Tuesday’s Asian session, New Zealand’s employment report for Q4 could prove crucial on whether the RBNZ will cut by 25 or 50bps, while the following day, Japan’s wage data for December could shape expectations about the BoJ’s next rate increase.

On the earnings front, the tech-related reporting continues with Alphabet and AMD on Tuesday, and Amazon on Thursday.

Weekly Focus – Uneventful Cut, Uneventful Keep

Soft US and euro area data weighed slightly on rates, which largely did not move much through the week, at least until German inflation unexpectedly declined significantly in several of the big Bundesländer, which drove 2Y Bund yields 10bpslower. This puts the spotlight on the euro area total released Monday. January is always a special month setting the stage for the year, because many prices are adjusted only at new year.

After a long period of some serious zigzagging the dollar has been steadier this week. The fallout of US tariff plans will continue to be a key driver of volatility in FX markets, though. European equities outperformed US in a week when the Chinese AI start-up DeepSeek took the spotlight as it poses a challenge to US AI developers to compete without relying on the most advanced chips.

The ECB cut its key interest rates by 25bp in a unanimous decision as widely expected. Despite several attempts from journalists, we did not get much colour on the final destination for this cutting cycle.

The decision followed data showing that the euro area stalled in Q4 with shrinking French and German economies still weighing down. The new year has started off a bit stronger as the current situation index from the IFO data supported the better-than-expected German PMI data for January. Expectations declined further to the lowest level in a year though, and we continue to expect the economy to stagnate in the first half of this year.

The FOMC meeting was as uneventful as the one in Frankfurt. The Fed kept rates unchanged, and Powell delivered a balanced message to markets while steering clear of toxic political questions. He noted that the committee is in no hurry to adjust the policy stance. Data out of the US ticked in a bit weaker than expected, with q/q Q4 GDP growth of 0.6%, slightly below expectations and softer vibes from the labour market with the "jobs plentiful"-index declining to the lowest level since September.

The calendar is packed with interesting highlights next week. Besides inflation data, on Monday French lawmakers will discuss the 2025 budget, and likely adopt it without a majority. Later in the week, we will see if PM Bayrou survives a no-confidence vote. On Friday, the ECB publishes a new paper on the neutral rate of interest, which might give us some further insight into where we should expect the cutting cycle to end up.

In the US, the first tariffs should take effect over the weekend. On the data front, we have a packed schedule with ISM data, JOLTs and jobs report as the key highlights. After a long period of solid job market data, it will be interesting to see if it continues. We expect nonfarm payrolls growth to slow down to +150k. We expect the Bank of England to cut the policy rate by 25bp to 4.50% on Thursday. We expect a cautious message, focusing on a gradual cutting cycle.

Sunset Market Commentary

Markets

Disappointing EMU Q4 growth yesterday triggered a bull steepening on EMU yield’s markets. Today, softer than expected domestic price data continued this dynamic. French HICP inflation declined 0.2% M/M, slowing the Y/Y measure from 1.9% to 1.8% (1.9% expected). German Länder data published throughout the morning also suggested a downside CPI surprise. The domestic measure indeed declined (-0.2% M/M and 2.3% Y/Y vs 2.6% expected). Core inflation excluding food and energy after the December uptick fell back to 2.9% from 3.3%. It was especially goods inflation easing (0.9%). Services inflation remained elevated (4.0%). Still, due to a different statistical set-up, the harmonized measure printed as expected (-0.2 M/M and 2.8% Y/Y, unchanged from December). Yesterday, at the post-meeting ECB press conference, Chair Lagarde indicated the bank is confident inflation will return to target, most likely resulting in an additional 25 bps cut at the March meeting. At the same, cumulative ECB easing has become substantial and policy is becoming ever less restrictive. This will trigger a debate on what is a neutral policy rate and whether the ECB should move below this level from March on. Whatever the outcome of this debate, German yields today again are ceding between 7.0 bps (2-y) and 3.0 bps (30-y). After this week’s setback, EMU money markets again embrace the scenario of the ECB lowering its policy rate to 2.0% by the end of this year. The jury is still out, but for this to happen inflation will probably will have to follow an almost perfect trajectory. US yields today again hold to the established ranges with yields change less than 1 bp aligning with the Fed’s wait-and-see stance. US December income (0.4%) and especially spending (0.7%) were solid as indicated in yesterday’s GDP report. The monthly core PCE deflator was unchanged at 2.8% Y/Y, supporting the Fed assessment that ‘inflation remains somewhat elevated’. US and EMU equities again are trading in positive territory (EuroStoxx 50 +0.3%, S&P 500 +0.5%) as solid earnings outweigh geopolitical uncertainty (the threat of tariffs in particular). In this respect, investors keep a eye on the White House, awaiting more concrete news regarding potential tariffs on Canada, Mexico and China this weekend. Brent oil trades little changed near $77 p/b.

In line with the market reaction function of late, uncertainty on tariffs again results in by default USD strength. DXY again holds north of 108(35). EUR/USD is also ceding ground (1.037), but losses could have been more outspoken given the sharp decline in EMU yields yesterday and today. Sterling marginally outperforms the euro (EUR/GBP 0.8365) as markets look forward to next week’s BoE policy meeting. The Canadian dollar (USD/CAD 1.4530) is trading near the ‘panic levels’ briefly touched at the peak of the corona sell-off early 2020.

News & Views

The ECB in a regular survey found that Euro area manufacturers are more worried about cheaper imports from China than tariffs from the US. Only half of the manufacturers contacted believed US levies would impact their business, with many of them noting they were already producing “local for local”. Some also said they are only exporting highly sophisticated goods which are difficult to substitute. Instead, though, they are more concerned about trade flows redirecting in case of disruptions to the US-Sino trade relationship. "In the absence of protective EU measures, this led more contacts to expect a negative effect on prices in their sector in the euro area than a positive one," the survey reported, adding that "In the event of protective measures and retaliation leading to a more generalised tariff war, it was much more likely that costs and prices would rise."

UK’s Nationwide reported house prices rising marginally at the start of the new year. House prices in January inched 0.1% m/m higher compared to the 0.3% analyst estimate. The yearly print slowed from 4.7% to 4.1% as a result. Nationwide’s chief economist Gardner said the market nevertheless continues to show resilience despite ongoing affordability pressures. While there has been an improvement in affordability over the last year, they remain stretched by historic standards. Monthly mortgage payments currently equal about 36% of an average UK net income, which is well above the long-run average of 30%. House prices remain high relative to average earnings too, posing high hurdles for the initial deposit households need to cover upfront. “This is a challenge that has been made worse by the record increase in rents in recent years, which, together with the cost-of-living crisis more generally, has hampered the ability of many in the private rented sector to save.”, Gardner said.

Canada’s GDP Declines, Canadian Dollar Lower

The Canadian dollar is steady on Friday. In the North American session, USD/CAD is trading at 1.4523, up 0.23% on the day.

The week wrapped up with Canada’s GDP, a report card on the strength of the economy. The November reading of -0.2% was a disappointment. This marked the first contraction of the year. There was better news in December, with an initial estimate of a 0.2% gain.

Will Trump impose 25% tariffs on Feb. 1?

US President Trump has barely warmed the chair in the Oval Office but he has managed to disrupt financial markets with his threat of tariffs against US trading partners. There was some relief in the market when Trump did not announce tariffs on his first day in office but he has reiterated that he will slap Canada and Mexico with 25% tariffs on Feb. 1. Canada and Mexico are the two largest trade partners of the US and a trade war would be damaging for all sides.

Canada would be particularly hit hard by US tariffs, as some 76% of Canada’s exports are sent to its southern neighbor. Bank of Canada Governor Macklem called the trade threat a “major new uncertainty” in December, even before Trump took office and Canada is bracing for a new, nasty reality if Trump makes good on his tariff threats.

The prospect of a trading war between Canada and the US is weighing on the Canadian dollar, which has plunged around 7% since October 1. The Bank of Canada lowered rates by a quarter point on Wednesday while the Federal Reserve maintained rates on the same day. With the BOC expected to make more cuts than the Fed this year, the US/Canada rate differential would widen even further and that could push the Canadian dollar lower.

USD/CAD Technical

- USD/CAD is testing resistance at 1.4493. Above, there is resistance at 1.4593

- There is support at 1.4390 and 1.4290

U.S. Consumer Spending Growth Ended 2024 on a High Note, Outpacing Income Growth

Personal income continued to grow robustly in December, rising by 0.4% month-over-month. Real disposable income, which excludes the impact of taxes and inflation, also edged higher, rising by 0.1% m/m.

Income gains continued to support consumer spending. Coming on the heeds of solid gains in the prior two months, nominal spending increased 0.7% in December. Stripping out inflation, the volume of spending also rose, increasing by 0.4% on the month and 3.1% from the year ago.

December marked another strong month of spending on goods (+0.7% m/m), led by durables (+1.1% m/m). The gain in services spending was more modest (+0.3%).

Inflationary pressures were little changed in December. The Fed's preferred inflation metric, the core PCE price deflator, rose 0.2% m/m, up slightly from the 0.1% increase seen in November. In year-over-year terms, core PCE inflation remained unchanged at 2.8%.

With spending outpacing income growth, the personal savings rate edged lower in December, declining to 3.8% down from 4.1% in November.

Key Implications

It appears that U.S. consumers were off to the races at the end of last year. Yesterday's GDP report had already telegraphed that consumer spending ended 2024 with bang, rising by 4.2% (annualized) in the fourth quarter. However, today's release provided additional color, showing that spending outpaced income growth yet again in December. In fact, this was the case in 9 out of 12 months of last year, coming at the expense consumers' ability to set money aside for the rainy day. As a result, personal saving rate declined from 5.5% at the start of 2024 to 3.8% last month.

Last year's strong consumer spending is even more impressive given that it happened alongside high interest rates and a cooler labor market. Some of the recent strength in spending on durable goods could be due to post-hurricanes replacement demand, and consumers racing to buy electric vehicles ahead of incentives being cancelled. We are still expecting real consumer spending to moderate closer to 2% this year, although the recent performance makes us wonder if U.S. consumers will once again surprise to the upside, helped by large stockpile of wealth they've accumulated since the pandemic.

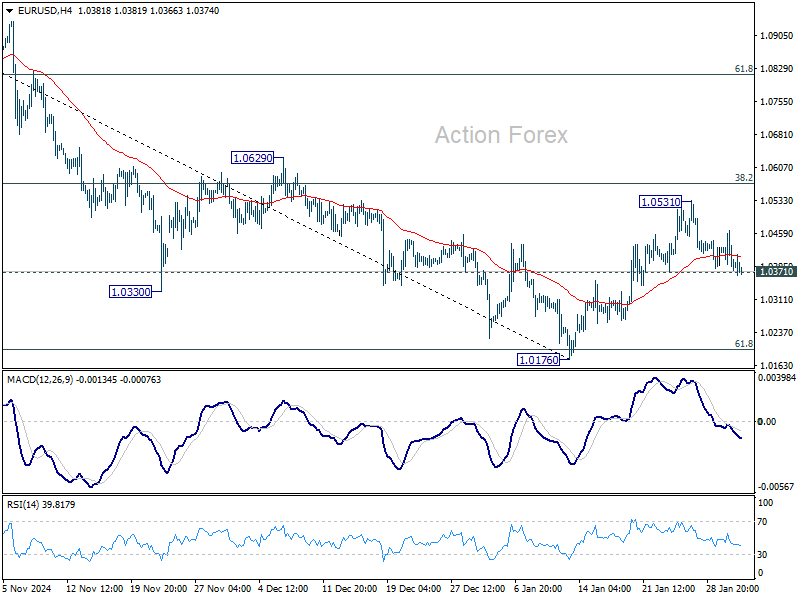

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0363; (P) 1.0415; (R1) 1.0445; More...

No change in EUR/USD's outlook and intraday bias stays neutral at this point. On the downside, break of 1.0371 support will indicate rejection by 38.2% retracement of 1.1213 to 1.0176 at 1.0572 and retain near term bearishness. Retest of 1.0176 low should be seen next. On the upside, though, decisive break of 1.0572 will raise the chance of bullish reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, outlook is mixed as fall from 1.1274 (2023 high) could either be the second leg of the corrective pattern from 0.9534 (2022 low), or another down leg of the long term down trend. Strong support from 61.8 retracement of 0.9534 to 1.1274 at 1.0199 will favor the former case, and sustained break of 55 W EMA (now at 1.0722) will argue that the third leg might have started. However, sustained trading below 1.0199 will favor the latter case and bring retest of 0.9534 low.

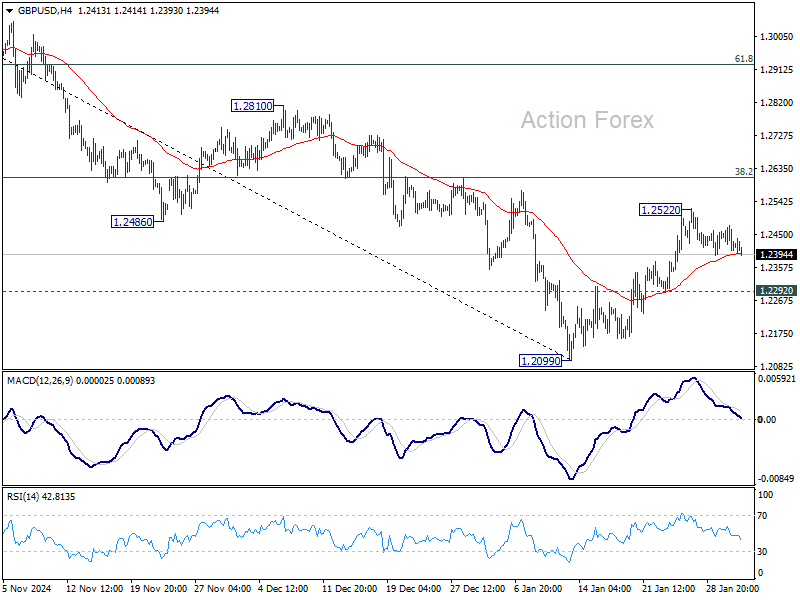

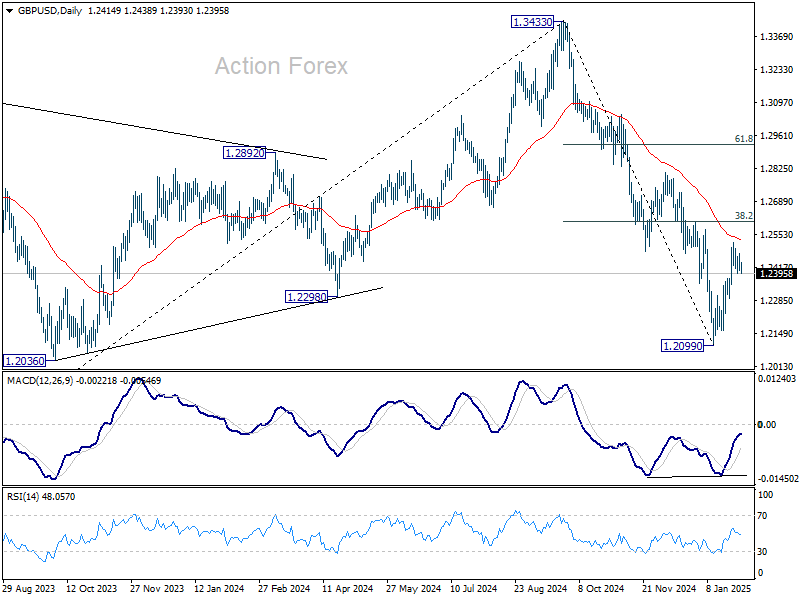

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2391; (P) 1.2434; (R1) 1.2459; More...

Intraday bias in GBP/USD remains neutral for the moment. Rebound from 1.2099 is seen as a corrective move. While another rise cannot be ruled out, strong resistance could be seen 38.2% retracement of 1.3433 to 1.2099 at 1.2609 to limit upside. On the downside, below 1.2292 minor support will bring retest of 1.2099 low. However, sustained trading above 1.2609 will raise the chance of reversal and target 61.8% retracement at 1.2923.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

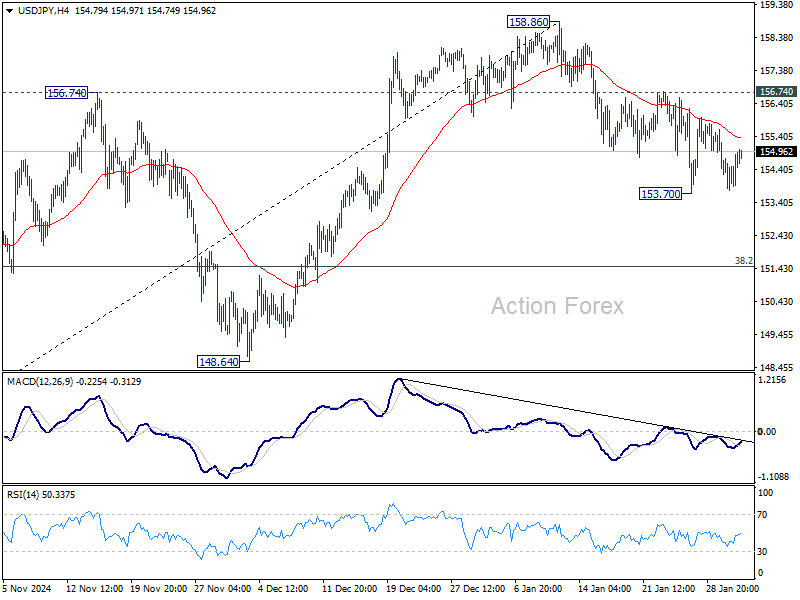

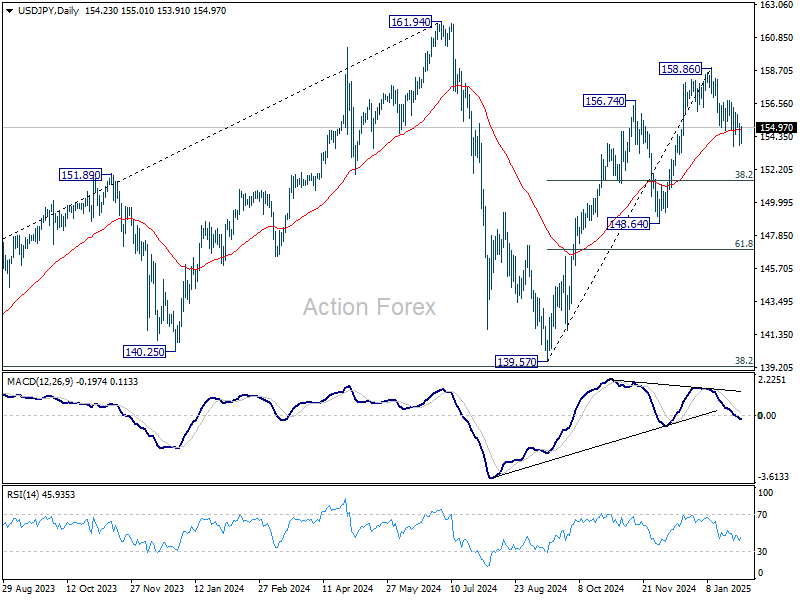

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 153.59; (P) 154.48; (R1) 155.16; More...

USD/JPY is staying in range above 153.70 and intraday bias remains neutral. On the downside, firm break of 153.70 will resume the fall from 158.86 to 38.2% retracement of 139.57 to 158.86 at 151.49. Nevertheless, break of 156.74 resistance will indicate that fall from 158.86 has completed as a correction. Intraday bias will be back on the upside for 158.86 and above to resume the whole rally from 138.57.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Canada’s Economy Pulls Back in November, But December Lift is in the Cards

Canadian economic growth took a step back in November, falling 0.2% month-on-month (m/m). This was a tick below Statistics Canada's advanced guidance and consensus expectations. Early estimates from Statistics Canada point to a 0.2% m/m rebound for December GDP growth, due in part to increases in retail trade, manufacturing, and construction activity.

November's reading was broad-based, with output contracting in 13 of 20 industries. The goods sector fell by 0.6% m/m, while the services sector saw a more modest decline of -0.1% m/m.

A 3.4% m/m decline in oil sands dragged down the mining/quarrying/oil & gas sector. Meanwhile, utilities fell by a hefty 3.6% m/m. The construction sector buffered some of the goods-side shortfall, expanding for a fourth consecutive month (0.7% m/m).

On the services side, the Canada Post strike weighed on the transportation & warehousing sector (-1.3% m/m). Elsewhere, the finance & insurance sector slipped for a second consecutive month (-0.4% m/m). A decent lift in accommodation and food services (1.4% m/m) countered some of the services-sector downside.

Key Implications

It's steady as she goes for domestic growth developments, as recent data comes in more or less in line with expectations. With November GDP data and December guidance, growth in the fourth quarter is tracking on point with the Bank of Canada's (BoC) most recent projections (1.8% q/q annualized). This would mark a decent acceleration from Q3's more meager gain of just 1% and provides a decent handoff into 2025, especially given looming uncertainties.

The BoC has its work cut out for them. After slashing interest rates this week, they will now wait for further details about Trump's tariff implementation plan, which will come as early as tomorrow. The Bank acknowledged that past interest rate cuts are starting to boost the economy while inflation is expected to be stable at 2%. However, future policy setting is subject to higher-than-usual uncertainties. While we think the Bank will step to the sidelines at their March meeting, expedited rate cuts may be in the cards should a worst-case trade war ensue.