Sample Category Title

Canadian Dollar Dives as Trump Confirms Tariffs, Gold Soars to Record High

Canadian Dollar spiked lower after US President Donald Trump confirmed his plan to impose 25% tariffs on imports from Canada and Mexico, set to take effect this Saturday on February 1. Trump justified the decision by citing concerns over migration, drug trafficking, and economic imbalances. However, uncertainty remains regarding whether oil imports will be affected. While the move was not entirely unexpected, the confirmation added pressure to the Loonie as markets assessed the impact on trade, inflation and growth.

In contrast, Trump’s stance on China remains less definitive. While he also mentioned potential tariffs on China due to ongoing fentanyl concerns, he stopped short of detailing any immediate action. This leaves the possibility of further trade disruptions on the horizon, though no concrete measures have been announced yet.

Despite the tariff headlines, Loonie remains middle-of-the-pack in weekly performance. Aussie and Kiwi continue to struggle, along with Euro. Yen leads the market, additionally supported by stronger Tokyo inflation data, followed by the Dollar. British Pound has climbed higher, benefiting from Euro weakness, while Swiss Franc is trading mix.

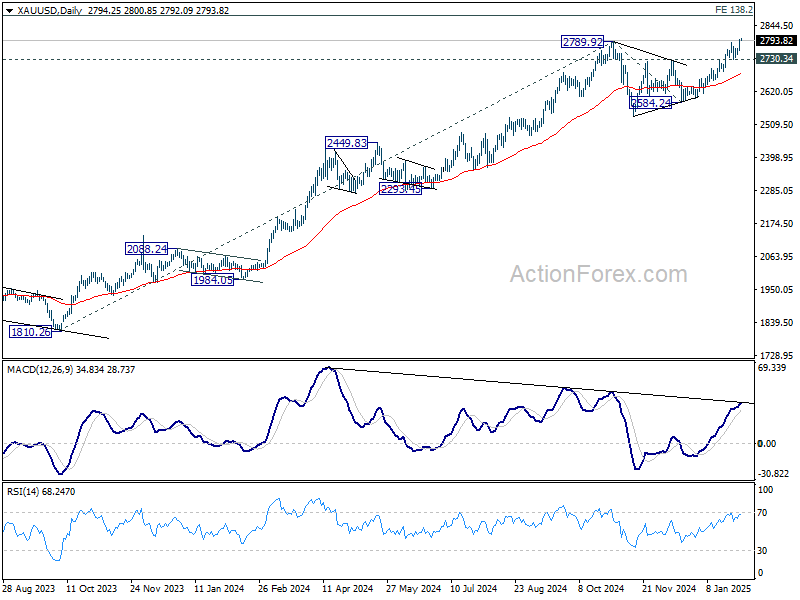

Gold has surged to a new all-time high, reaching 2800 level as investors seek safety amid rising economic uncertainty. The strong rally suggests growing concerns over global stability, particularly with trade tensions escalating.

For now, near term outlook in Gold will stay bullish as long as 2730.34 support holds. Next target is 38.2% projection of 1810.26 to 2789.92 from 2584.24 at 2958.47, or even 3000 psychological level.

Tokyo inflation accelerates, keeping BoJ hikes alive

Japan’s inflationary pressures picked up in January, with Tokyo’s core CPI (excluding fresh food) rising to 2.5% yoy from 2.4%, marking its fastest pace in nearly a year. Core-core measure (excluding food and energy) also edged higher to 1.9% from 1.8%. Meanwhile, headline CPI surged to 3.4% from 3.0%, its highest level in nearly two years, largely driven by rising prices for vegetables and rice.

The data reinforces expectations that inflation in Japan could continue rising toward 3% in the coming months, as persistently weak yen drives up import costs. Some analysts see room for one or two more rate hikes by BoJ this year, particularly if inflation remains sticky and real wage growth improves. However, with Tokyo services inflation slowing to 0.6% yoy from 1.0% yoy, concerns remain about the sustainability of domestic price pressures.

On the production side, industrial output rose 0.3% mom in December, matching forecasts. The Ministry of Economy retained its cautious assessment, stating that production "fluctuates indecisively," though manufacturers expect a 1.0% rise in January and a further 1.2% increase in February.

Retail sales, however, showed resilience, climbing 3.7% yoy, exceeding expectations of 2.9%. This suggests that consumer demand remains strong despite higher living costs.

BoJ’s Ueda reaffirms support for economy while keeping rate hikes on the table

BoJ Governor Kazuo Ueda reiterated the central bank’s is aiming for "gradual pickup" in prices, supported by a "solid increase in wages." He emphasized that maintaining easy monetary conditions remains necessary to "support economic activity" and ensure that underlying inflation continues rising toward the 2% target.

However, he also made it clear that BoJ’s stance remains unchanged, noting that it will "continue raising interest rates" and adjust monetary support if the economy and prices "move in line with our forecasts."

At the same parliamentary session, Prime Minister Shigeru reinforced the government’s priority of achieving sustainable inflation alongside wage growth. He highlighted that while stable price increases are important, "we must aim for wage growth higher than inflation while prices rise stably." He also warned against the perception that falling prices are beneficial, arguing that such views prolonged Japan’s deflationary struggles in the past.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4390; (P) 1.4493; (R1) 1.4593; More...

USD/CAD's break of 1.4516 resistance indicates resumption of larger rally. Intraday bias is back on the upside for 1.4667/89 key resistance zone. Strong resistance might be seen there to limit upside on first attempt. But break of 1.4260 support is needed to confirm short term topping. Otherwise, outlook will stay bullish in case of retreat. Decisive break of 1.4689 will confirm long term up trend resumption.

In the bigger picture, up trend from 1.2005 (2021) is in progress for retesting 1.4667/89 key resistance zone (2020/2015 highs). Decisive break there will confirm long term up trend resumption. Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. Medium term outlook will remain bullish as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.

Tokyo inflation accelerates, keeping BoJ hikes alive

Japan’s inflationary pressures picked up in January, with Tokyo’s core CPI (excluding fresh food) rising to 2.5% yoy from 2.4%, marking its fastest pace in nearly a year. Core-core measure (excluding food and energy) also edged higher to 1.9% from 1.8%. Meanwhile, headline CPI surged to 3.4% from 3.0%, its highest level in nearly two years, largely driven by rising prices for vegetables and rice.

The data reinforces expectations that inflation in Japan could continue rising toward 3% in the coming months, as persistently weak yen drives up import costs. Some analysts see room for one or two more rate hikes by BoJ this year, particularly if inflation remains sticky and real wage growth improves. However, with Tokyo services inflation slowing to 0.6% yoy from 1.0% yoy, concerns remain about the sustainability of domestic price pressures.

On the production side, industrial output rose 0.3% mom in December, matching forecasts. The Ministry of Economy retained its cautious assessment, stating that production "fluctuates indecisively," though manufacturers expect a 1.0% rise in January and a further 1.2% increase in February.

Retail sales, however, showed resilience, climbing 3.7% yoy, exceeding expectations of 2.9%. This suggests that consumer demand remains strong despite higher living costs.

BoJ’s Ueda reaffirms support for economy while keeping rate hikes on the table

BoJ Governor Kazuo Ueda reiterated the central bank’s is aiming for "gradual pickup" in prices, supported by a "solid increase in wages." He emphasized that maintaining easy monetary conditions remains necessary to "support economic activity" and ensure that underlying inflation continues rising toward the 2% target.

However, he also made it clear that BoJ’s stance remains unchanged, noting that it will "continue raising interest rates" and adjust monetary support if the economy and prices "move in line with our forecasts."

At the same parliamentary session, Prime Minister Shigeru reinforced the government’s priority of achieving sustainable inflation alongside wage growth. He highlighted that while stable price increases are important, "we must aim for wage growth higher than inflation while prices rise stably." He also warned against the perception that falling prices are beneficial, arguing that such views prolonged Japan’s deflationary struggles in the past.

After 25 bps Cut in March, Expect ECB to Start Skipping from Time to Time

Markets

The ECB lowered the policy rate to 2.75% (-25 bps) yesterday. While president Lagarde as usual refrained from giving guidance going forward, some subtle statement tweaks and not-so-subtle comments suggest Frankfurt is moving towards a fine-tuning phase. Among the most striking ones was Lagarde explicitly stressing the cumulative amount of cuts the ECB already delivered (purposely followed by a short moment of silence). She also flagged an upcoming staff report about the revision of the neutral rate, due February 7. The timing, ahead of the March 6 meeting when another rate cut brings the deposit rate to the upper bound of the current neutral rate estimates, is not a coincidence. Bloomberg citing officials reported afterwards that the ECB as soon as March may stop labeling its policy stance as “restrictive”. Long story short: after the 25 bps cut in March, we expect the ECB to start skipping meetings from time to time with only one or two additional moves afterwards. German rates eased 6-7 bps but those losses were related to earlier weaker-than-expected GDP readings in France, Germany and, as a result, the euro area (stagnation). US yields finished less than 2 bps lower across the curve. Q4 GDP growth was once again strongly consumer-powered and jobless claims remain low. Q4 PCE deflators missed the bar on a headline level. The dollar ended a tad higher thanks to a late-session sprint after president Trump stuck to his Feb 1 (as in: tomorrow) deadline for tariffs on Mexico and Canada. The Canadian dollar and Mexican peso took a hit intraday. EUR/USD finished sub 1.04. Sterling continues to grind higher. A six-day GBP winning streak brought EUR/GBP from +0.845 to around 0.836. The pound may soon be taking a breather ahead of next week’s (Fed 7) looming Bank of England meeting (including new forecasts) though. Today’s economic calendar features interesting data in the US, including the Q4 Employment Cost Index (expected to pick up from 0.8% to 0.9%) and the December PCE deflators. The latter, however, can be derived from yesterday’s Q4 print. Germany and France release inflation figures for January. The European figure is due on Monday (2.5% y/y). It could trigger some intraday volatility but we don’t expect any huge moves. From a broader perspective, we think both the ECB and Fed have supported the bottom below yields. The dollar could hold the upper hand, especially ahead of a weekend in which we will see whether Trump’s verbal show of force translates into actions as well. We’re particularly interested whether countermeasures will follow swiftly. Canada threatened to cut off oil exports to the US altogether, even as Trump considered excluding this sector from tariffs.

News & Views

CPI inflation (ex-fresh food) in the Tokyo area in January rose 0.3% M/M lifting the Y/Y measure to 2.5% (was 2.4% in December). A such, the Y/Y measure is reaching the highest level in a year’s time. The overall headline CPI even accelerated 0.5% M/M and 3.5% y/y, driven by a sharp rise in food prices (2.1% M/M, 7.7% Y/Y). Core inflation ex fresh food and energy rose slightly further from 1.8% to 1.9%. The Tokyo data are seen as a good pointer for the overall national figures that will be published on Feb 21. The further rise in inflation comes after the BOJ last week raised its policy rate by 25 bps to 0.50%, the highest level since 2008. Today’s data at least support the case for the BOJ to continue policy normalization later this year even as further interest rate hikes are in particular conditional to higher wages supporting domestic demand. In this respect, other Japanese eco data published this morning were mixed. Labour market date suggest ongoing strength with the unemployment rate declining to 2.4% from 2.5% and the job-to-applications ratio holding at 1.25. Preliminary January industrial production was reported at 0.3% M/M and -1.1% Y/Y. Retail sales declined 0.7% in December, but were 3.7% Y/Y. Both series are highly volatile.

The Norwegian government coalition between the Labour Party of Prime Minster Jonas Gahr Store and the Center Party collapsed as both groups failed to reach an agreement on approving a series of new EU energy laws. The euro-skeptic Center party rejected approving new regulation from the EU. The rejection is part of a broader debate in Norway on relationship with the EU with respect to energy, including the impact of the interconnection with the EU in exchanging providing/electricity and its impact on local prices. Parliamentary elections in Norway are scheduled for September 8. Until then, the Labour Party will continue with a minority government.

Gold at Record High

The European Central Bank (ECB) cut the interest rates yesterday for the fifth time, and pulled the facility deposit rate to 2.75%. The euro reacted by giving a positive reaction to the expected move. But enthusiasm didn’t last beyond ECB Chief Christine Lagarde’s presser, where she reminded investors that growth risks remain ‘tilted to the downside’. Other than that, she repeated the concerns regarding lower confidence, rising geopolitical risks, the ongoing impact of the past rate increases. Her speech hinted that the ECB is inclined to pull more rate hikes from its hat, should the inflationary pressures continue to ease. And regarding inflation: Lagarde said that December uptick – caused by higher energy prices – was expected, but that the impact of Trump tariff’s on European inflation was unclear: on one hand, the tariffs and potential retaliation will inevitably rise consumer prices on both sides of the Atlantic Ocean and heat up the inflationary pressures for everyone. But on the other hand, higher tariffs would hit the European businesses, lead to further economic slowdown and tame price pressures. For now, the faltering growth story overweights. Growth in the euro area couldn’t meet the meagre expectation of 0.1% last quarter: it came in at 0%. The yearly figure fell below 1%. German output fell 0.2% and French output fell 0.1% - and political shenanigans in Germany and France point at continued weakness. Funny enough, the European Stoxx 600 couldn’t care less of what the growth data suggests. The index went straight up to a fresh ATH yesterday on rising hope for more ECB support. The EURUSD took the direction of the south following Lagarde’s presser. The pair sank below 1.04 mark and will likely remain under pressure below the 1.0425/1.0460 area, including the 50-DMA and the minor 23.6% Fibonacci retracement on September to January selloff. Even the significant decline in US GDP growth update and the downside revision in Q4 price pressures couldn’t prevent the EURUSD selloff.

Elsewhere, Trump renewed his pledge to impose 25% tariffs on Canada and Mexico, sending the currencies of both countries lower against the US dollar. The USDCAD rallied to 1.46 and is now challenging the highest levels since 2016 and 2020. The risks are tilted to the downside for the Loonie, as heated trade war with the US could significantly hurt Canada’s economic growth, bring in stronger Bank of Canada (BoC) support and weigh on the Canadian dollar.

Gold at fresh high

Good news is that the US tariffs won’t make America Great Again. The bad news is that it will be lose-lose globally – which is probably why gold prices are on the rise again. The price of an ounce hit a fresh ATH yesterday, backed by a swift move to safety due to the Trump's tariff threats, the rising geopolitical tensions, the rising US government debt and the fear of a potential tech rout that could lead to a global risk selloff. And the move is probably amplified by uncertainty regarding the expectations around central bank policies and Trump-dependency, EM central bank gold buying – in case the relations with the US get worse, and shifting market positioning. The latest CFTC data shows increased speculative buying since the beginning of January – partly explained by the worries of Trump, high tech valuations and the chatter of a possible sizeable correction. The question is: could gold get more expensive? Yes, it could. A sizeable risk selloff in global financial markets could drive gold to fresh highs. But the rapid rise in speculative long positions hint that we should see a pullback in gold if the AI worries – triggered by DeepSeek – happen to be unfunded.

DeepSeek blocked by hundreds of companies

And speaking of that, five days into the DeepSeek drama, and ‘hundreds of companies’ – especially those linked to governments – are already limiting access to DeepSeek’s search engine highlighting data security concerns for using a Chinese chat bot that could collect and give information to Chinese authorities. Chip and digital information war between China and the West is entering a new phase and cybersecurity firms will likely see the benefits of it. Crowdstrike, Fortinet and Cloudfare hit fresh ATH levels this week and have potential to attract more capital.

Latest earnings

Speaking of record highs, Meta extended gains to a fresh ATH as well following the announcement of stronger-than-expected earnings on Wednesday, while Apple gained 3% in the afterhours trading after releasing better-than-expected Q4 results and a record high Q4 revenue. But wait, it’s not all rosy for Apple. The company’s Chinese sales was a massive 15% miss and the iPhone sales came in 3% below analyst expectations. Tim Cook highlighted that iPhone 16 sales have been stronger in markets where Apple Intelligence is available hinting that there is potential for growth on AI, and the rise in Mac sales and services revenue are encouraging, but Apple looks expensive at the current valuation, and this week’s DeepSeek push and news of partnership with Starlink are not enough to justify a fresh jump.

ECB Cuts Rate amidst Divergent Euro Area Growth

In focus today

Today, we look out for January inflation data for Germany and France, which we receive ahead of euro area data on Monday. Yesterday, Spain's January inflation was reported at 2.9%. It will be interesting to see what these indicators suggest about euro area inflation and the broader trends for the region.

This afternoon, the US will release December's PCE data on private consumption and inflation. Since yesterday's flash GDP data already included the quarterly data which covers private consumption for December, today's release is unlikely to significantly impact the markets. The Fed will pay more attention to the Q4 employment cost index, which is a key measure of wage pressures.

Economic and market news

What happened overnight

In Japan, January core inflation came in at 2.5% (prior: 2.4%, cons: 2.5%), marking the fastest annual pace in nearly a year. This figure significantly exceeds the BoJ's 2% target, maintaining market expectations for further interest rate hikes.

What happened yesterday

In the euro area, ECB cut policy rate by 25bp to 2.75%, as widely anticipated. Lagarde's assessment of growth and inflation remained unchanged from December, offering no new insights into future policy rates. Looking ahead, the ECB is expected to deliver another rate cut at the March meeting. However, when asked the important question on where the cutting cycle will end, Lagarde did give any signals. See more in Flash: ECB review, 30 January.

Euro area GDP growth for Q4 registered at 0.0% q/q, below expectations of 0.1% q/q. This brings overall GDP growth for 2024 to 0.7% y/y. The Q4 figures highlight continued growth divergence within the euro area, with France and Germany contracting, while Spain and Portugal recorded very strong growth. We anticipate that growth will gradually improve in 2025, driven by rising real incomes and significantly lower policy rates. Private consumption is expected to increase and become the main growth driver. We expect 2025-euro area GDP growth to be 0.9% y/y.

Turning to individual countries, we started the day with France's Q4 GDP, which slightly declined by 0.1% q/q, following a prior increase of 0.4%. Over the last two quarters, GDP growth in France averaged 0.15% q/q, continuing to weight down euro area growth.

In Germany, Q4 GDP fell by 0.2% q/q, mainly due to exports being significantly lower than in Q3, despite increases in household and government final consumption expenditure. The German economy ended in negative territory with GDP overall falling 0.2% in 2024. While we expect quarterly growth to improve gradually throughout 2025, due to statistical underhang, German GDP growth is forecasted to remain flat at 0.0% y/y.

In Spain, higher energy prices drove up inflation rate to 2.9% in January (prior: 2.8%, cons: 2.8%).

In US, Q4 flash GDP came in at 2.3% q/q (prior: 3.1%, cons: 2.6%), marking a weaker than expected end to 2024, a year characterised by the resilience of American consumers. Overall, the economy expanded 2.8% in 2024.

In Denmark, following ECB's rate cut, Nationalbanken cut its key rate by 25bp bringing it to 2.35%.

Equities: Global equities rose yesterday, with European shares once again taking the lead. Perhaps more interestingly, the recent trend is not solely about the US and the MAG 7. Europe has been outperforming the US, and equal-weighted indices have been outperforming the cap-weighted S&P 500. A positive angle is the broadening out of leadership, with all 25 industries in the STOXX 600 advancing yesterday, and defensives performing on par with cyclicals in Europe while outperforming in the US. On a global scale, the only sector that declined yesterday was tech, and this was not a top-down story but more related to earnings in the US. In the US yesterday: Dow +0.4%, S&P 500 +0.5%, Nasdaq +0.3%, Russell 2000 +1.1%. Asian markets are mixed this morning, with South Korea standing out on the negative side. European futures are also mixed this morning, while the US is once again higher, led by the Nasdaq.

FI: European rates ended some 8bp lower in the 2y point and 6bp in the 10y point. Rates generally rallied outside the ECB meeting. Weaker than expected German, French and Italian GDP and positioning ahead of the ECB meeting on risk of a dovish Lagarde led the front-end rally. Markets are pricing another 70bp of rate cuts by year-end. Denmark's central bank mirrored the ECB's rate decision yesterday, thereby keeping the -40bp spread between the policy rates.

FX: EUR/USD was left rather unscathed by yesterday's uneventful 25bp ECB cut. News on tariffs from the Trump administration continues to be taking centre stage with Canada, Mexico and China in focus. AUD has been among the weakest performing G10 currencies this week with Australian Q4 inflation coming in below expectations and underlying inflation now close to pre-pandemic levels for the first time since 2021. European natural gas prices continue to grind higher with the tight supply situation being the main reason, but the flash PMIs last week suggested that economic growth might be on the rise as well.

Cliff Notes: Dealing With Uncertainty

Key insights from the week that was.

In Australia, the Q4 CPI printed modestly to the downside of Westpac’s expectation and the market consensus, headline inflation rising 0.2% (2.4%yr). Cost-of-living measures, most notably the various state and federal government energy rebates, played an important role in suppressing headline inflation, with electricity prices falling –9.9% (–25.2%yr). That said, inflationary pressures are abating broadly across the consumer basket. Most notably in the housing group, including rents and homebuilding costs, but also across fuel, clothing/footwear and household contents/services. Price pressures are still showing persistence in a few sub groups though. While total services inflation ticked down at year-end (4.6%yr in Q3 to 4.3%yr in Q4), downward revisions to childcare costs were at play. The narrower market services inflation measure continues to hover just north of 4.0%yr, with increases in holiday travel and insurance costs primary supports.

Encouragingly though, the RBA’s preferred gauge of underlying inflation, trimmed mean core inflation, eased from 3.6%yr to 3.2%yr Q3 to Q4, and is now tracking a six-month annualised pace of just 2.7%yr, inside the RBA’s 2-3%yr target range. As outlined by Chief Economist Luci Ellis, this update shifts the balance of risks for policy. Although the full suite of economic data is giving mixed signals on the strength and capacity of the economy – consumer spending has disappointed following the Stage 3 tax cuts but we continue to observe a tight labour market and (modest) real income gains – on balance, we believe the inflation trend warrants an imminent start to rate cuts. We have now returned to our earlier view that, starting in February, the RBA will undertake a gradual easing cycle of 25bps per quarter through Q4 to a terminal rate of 3.35%.

Offshore, it was a busy week of central bank meetings and key data.

The FOMC kept rates steady in January having cut by 100bps through late-2024 to a fed funds rate of 4.375%. Meeting communications suggest the Committee remains constructive on the health of the economy and believe the disinflationary trend will persist, with the labour market seen as broadly in balance and an increase in slack judged unnecessary for inflation to continue to decelerate through 2025 as monetary policy remains restrictive.

Of the US data released this week, Q4 GDP stands out. Domestic final demand had another strong quarter, growing 3.0% annualised, in line with the average of the prior three quarters. Household consumption drove this result, backing up Q3's strong 3.7% annualised gain with a 4.2% result in Q4, principally on strength in services consumption though growth in goods consumption was also robust. Government spending meanwhile continued to contribute to GDP at both the Federal and state & local levels, and housing investment rebounded after six months of declines. Business investment was weak however, equipment investment falling at a 7.8% annualised pace (admittedly likely weighed down by industrial disputes) while structures activity declined 1.1% annualised.

The composition of growth matters greatly for the outlook. The labour market and the average US household’s long-term fixed borrowing costs should continue to insulate discretionary consumption. But the sharp rise in long-term yields since last September owing to inflation risks from tariffs and immigration changes and a general expectation of persistence in fiscal expansion casts a long shadow over the housing sector – evincing the risk, pending home sales fell 5.5% in December. While President Trump intends to spark private investment across the US by imposing tariffs and through measures like the AI infrastructure initiative announced last week, this is not necessarily a given, particularly in the near term.

With President Trump today confirming that 25% tariffs will be imposed on imports from Canada and Mexico and that the administration is currently considering actions against China, the coming weeks and months will be a good test of the responsiveness of the US economy to these policies, in particular which way the risks for investment and employment will skew. For the FOMC, the implications of these policies for activity matter as much as for inflation.

For Canada, the balance of risks are certainly one sided, although their scale will depend on whether oil exports to the US escape the 25% tariff. The potential implications of US policy were certainly on the minds of the Bank of Canada as it cut its overnight rate by 25bps to 3.0% and called an end to quantitative tightening, the BoC believing that balance sheet normalisation is largely complete. Arguably the market was more intrigued by the absence of forward guidance for policy, the statement and Governor Macklem’s remarks making clear January’s projections were "subject to more-than-usual uncertainty" given the "rapidly evolving policy landscape". Cumulative rate cuts to date are providing support to Canada’s economy, job growth and household demand are picking up, but with the labour market still soft overall, the announced tariffs put at risk the absorption of excess supply in Canada’s economy anticipated by the BoC over the next two years while also threatening their ability to meet the inflation target, and arguably the ability of monetary policy to provide meaningful additional support to the economy.

The European Central Bank also cut rates by 25bps at their January meeting. The statement and press conference signalled greater concern over the persistence and breadth of the growth upturn, unsurprising given the just released Q4 GDP report suggests activity contracted in Germany and France into year end and stalled across the Euro Area overall – Spain providing an offset, growing 0.8% in Q4. It is also worth noting that the stance of policy and financial conditions were characterised as "restrictive" and "tight" respectively, pointing to additional downside risks for the Euro Area economy in addition to those emanating from US trade policy. To our expectation of two more cuts from here, the market sees downside risk. The policy outlook will depend on the extent to which the easing undertaken to date bolsters confidence amongst households and firms’ resolve to work through the considerable challenges they face.

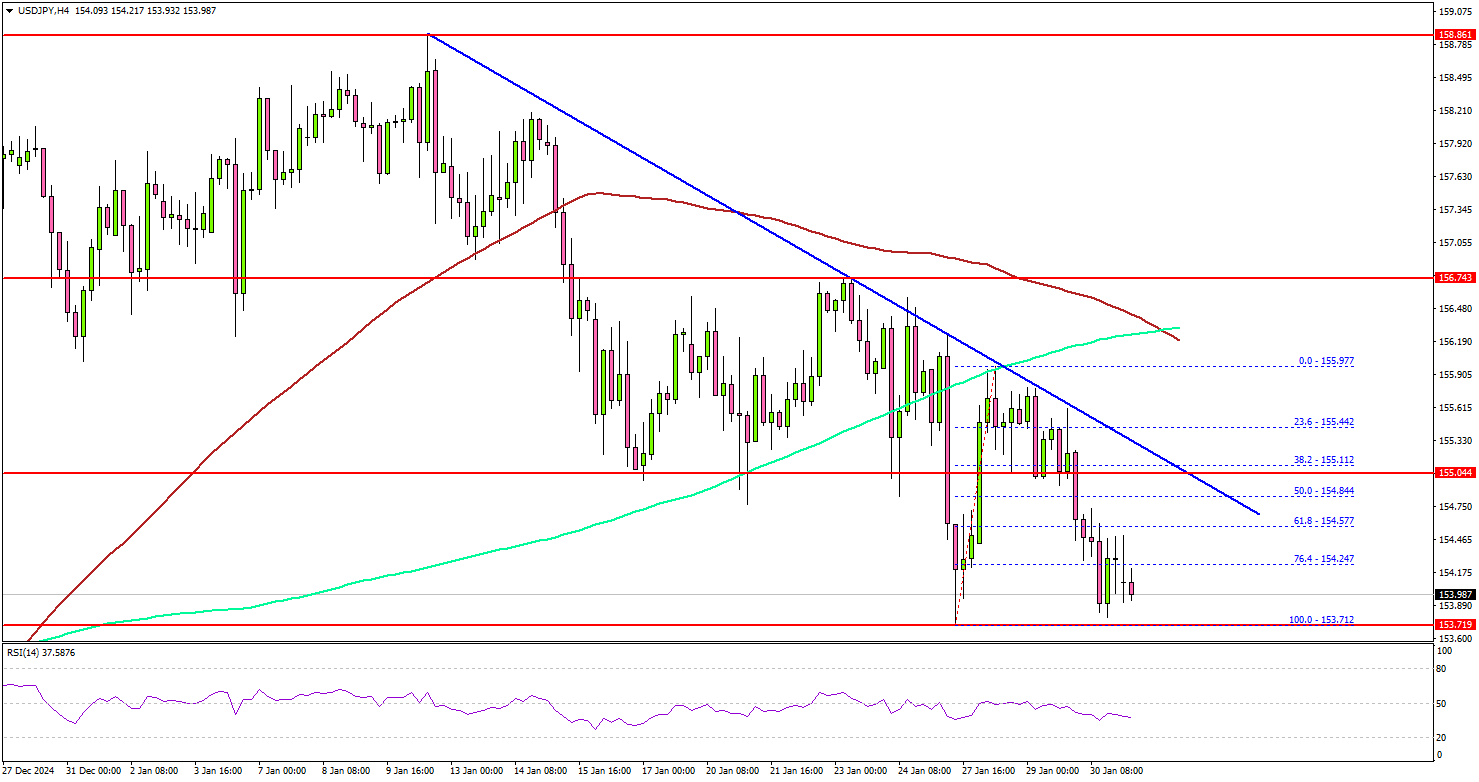

USD/JPY Extends Losses: Bears Tighten Their Grip

Key Highlights

- USD/JPY extended losses below the 155.50 support.

- A major bearish trend line is forming with resistance at 155.10 on the 4-hour chart.

- Gold prices rallied above the $2,770 resistance zone.

- Bitcoin recovered and was able to climb above the $103,500 resistance zone.

USD/JPY Technical Analysis

The US Dollar started a major decline from well above 157.00 against the Japanese Yen. USD/JPY extended losses and traded below the 155.50 support.

Looking at the 4-hour chart, the pair settled below the 155.00 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). The bears seem to be in control and might aim for more losses.

On the downside, immediate support sits near the 153.70 level. The next key support sits near the 153.20 level. Any more losses could send the pair toward the 152.00 level.

On the upside, the pair seems to be facing hurdles near the 154.60 level. The next major resistance is near the 155.00 level. There is also a major bearish trend line forming with resistance at 155.10 on the same chart.

A close above the 155.00 and 155.10 levels could set the tone for another increase. In the stated case, the pair could even clear the 156.50 resistance and the 100 simple moving average (red, 4-hour).

Looking at Gold, the bulls remained in action and they were able to push the price above the $2,770 resistance zone.

Upcoming Economic Events:

- US Personal Income for Dec 2024 (MoM) - Forecast +0.4%, versus +0.3% previous.

- US Core Personal Consumption Expenditure for Dec 2024 (MoM) - Forecast +0.2%, versus +0.1% previous.

Elliott Wave View on Gold (XAUUSD) Impulsive Structure to Resume

Short Term Elliott Wave View in Gold (XAUUSD) suggests that rally from 1.14.2025 low is in progress as an impulse. Up from 1.14.2025 low, wave (i) ended at 2724.74 and wave (ii) ended at 2689.28. Wave (iii) higher ended at 2763.39 and wave (iv) ended at 2735.67. Final leg wave (v) ended at 2785.87 which completed wave ((i)) in higher degree. Pullback in wave ((ii)) unfolded as a zigzag Elliott Wave structure. Down from wave ((i)), wave (a) ended at 2747.07 and wave (b) ended at 2772.04. Wave (c) lower ended at 2730.23 which completed wave ((ii)).

The metal resumes higher in wave ((iii)). Up from wave ((ii)), wave i ended at 2766.3 and wave ii ended at 2744.78. Wave iii higher ended at 2798.55 and wave iv pullback ended at 2788.43. Expect wave v higher to end soon which completes wave (i) in higher degree. Then the metal should pullback in wave (ii) in 3, 7, or 11 swing to correct cycle from 1.28.2025 low before it resumes higher again. Near term, as far as pivot at 2730.23 low stays intact, expect dips to find support in 3, 7, 11 swing for more upside.

Gold (XAUUSD) 1-Hour Elliott Wave Chart From 1.31.2025

GOLD (XAUUSD) Video

https://www.youtube.com/watch?v=SUuEYaVXGTA