Sample Category Title

Bitcoin (BTC/USD) Rises Above $105k as US States Ponder Bitcoin Strategic Reserve

- Bitcoin’s price surges past $105k, driven by a weaker US dollar and growing institutional interest.

- Several US states are considering adopting Bitcoin reserves, further enhancing Bitcoin’s appeal.

- Grayscale launches a Bitcoin Miners ETF.

- On-chain analysis suggests potential for further price appreciation.

Bitcoin has regained momentum after a four-day decline, bolstered by a weaker US Dollar. The cryptocurrency’s recovery has also been fueled by discussions in several US states about adopting Bitcoin reserves, reflecting growing institutional interest. Additionally, the overall sentiment toward cryptocurrencies remains strong, a trend that has persisted since the start of the Trump administration.

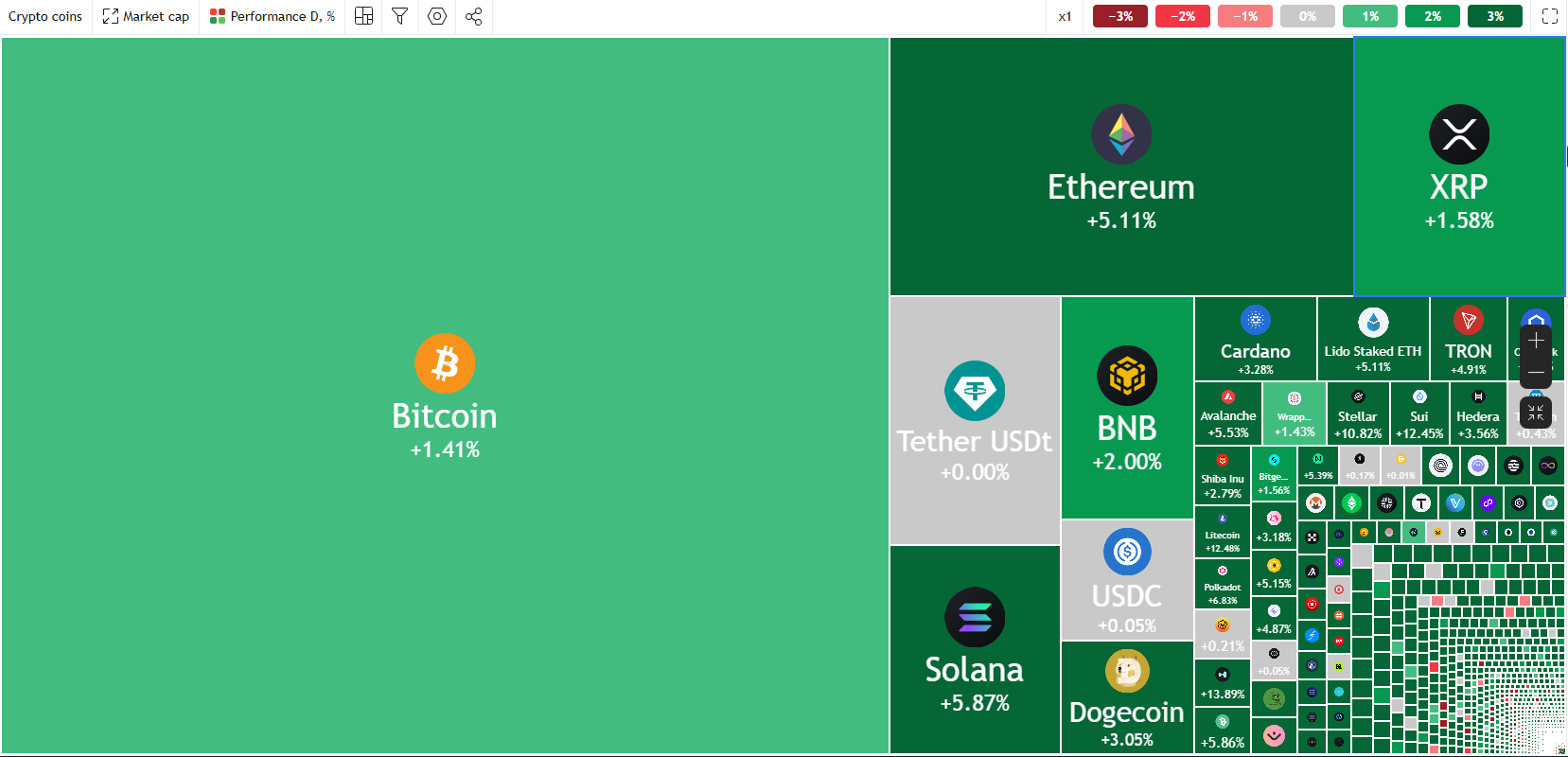

Crypto Heatmap, January 30, 2025

Source: TradingView (click to enlarge)

US States Eye Bitcoin Reserve

Following the inauguration of President Trump crypto market sentiment has remained bullish. The appointment of an interim SEO Chair who is known to be a proponent of crypto and who is developing a framework for crypto has been lauded by crypto enthusiasts.

This week however, various US States are considering a Bitcoin reserve, something which will further enhance the appeal of the Worlds Largest Crypto and could help support prices. Yesterday Utah became the second US state after Arizona to clear the Strategic Bitcoin Reserve Bill. There is hope that if the Bill is approved it may see other States follow suit.

An estimated 11 US states are exploring the inclusion of Bitcoin in their strategic reserves, with many considering a standard allocation of 10% of their total funds. This highlights the growing recognition of Bitcoin as a viable asset in government portfolios.

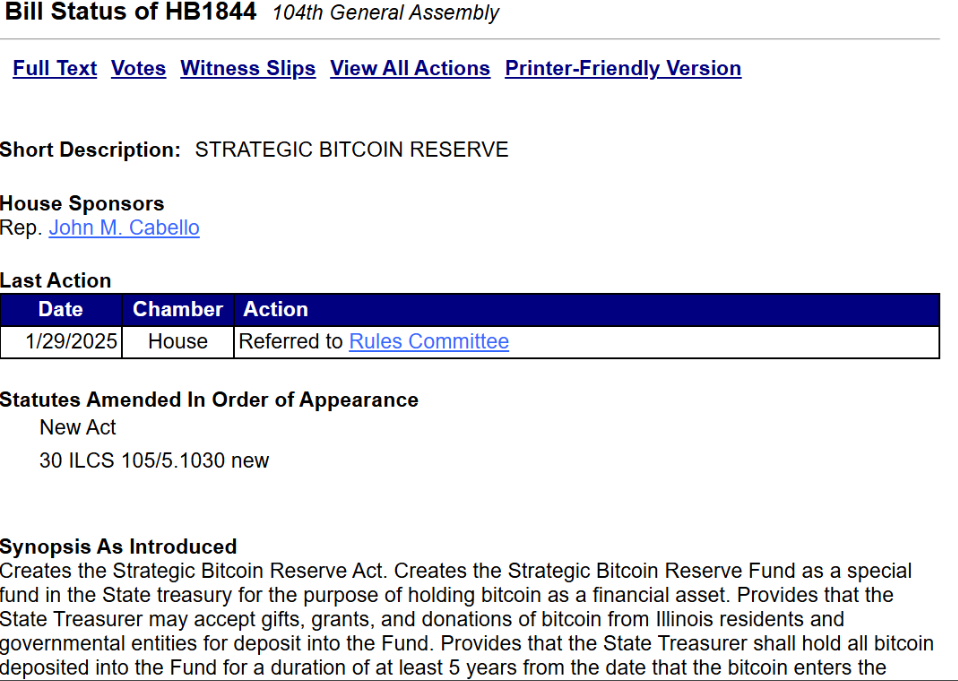

Joining the list of states to advance a Strategic Bitcoin Reserve Bill is Illinois who are eyeing a 5-year ‘HODL’ strategy. The bill was submitted to the Rules Committee on January 29 to finalize regulatory details, marking a critical step before it advances for full approval by lawmakers.

Source: Ilga.gov (click to enlarge)

GrayScale Launches Bitcoin Miners ETF

Grayscale has introduced a new crypto investment product, emphasizing the vital role of Bitcoin miners in supporting the Bitcoin network. The company stated that miners play a crucial part in ensuring the network’s security, integrity, and overall operation.

Grayscale has launched the Bitcoin Miners ETF, giving investors a simple way to gain exposure to Bitcoin miners and the global mining industry. David LaValle, Grayscale’s global ETF head, explained that Bitcoin miners are key to the network and are expected to grow significantly as Bitcoin becomes more widely adopted, making the ETF an attractive choice for many investors.

Bitcoin mining stocks struggled in 2024 to replicate the gains of Bitcoin, which recorded gains of around 112% for the year. This is backed up by data from Hashrate Index and Google Finance shows that most publicly traded Bitcoin mining companies ended 2024 with major losses, with some seeing their value drop by as much as 84%.

It will be interesting to see what the demand and flows are like for miners’ ETF, i for one will be keeping an eye on how this develops.

ETF Flows Remain Positive

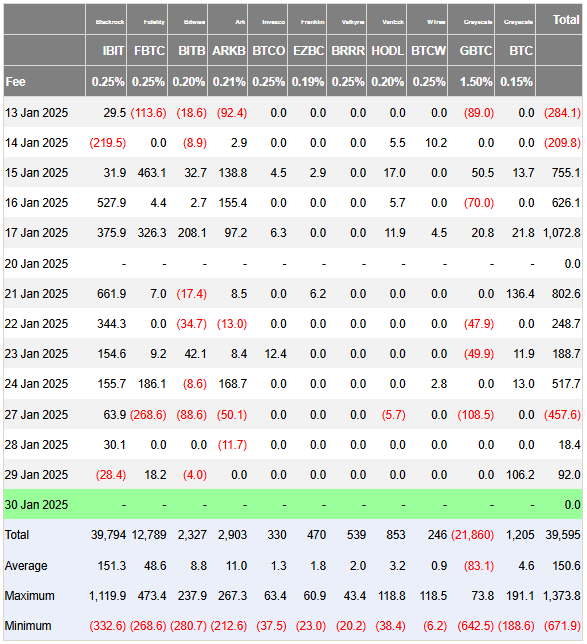

Bitcoin ETF flows have struggled this week following on from massive inflows last week even though it was a four-day week with the President’s inauguration.

This week however, saw massive outflows on Monday of around $457.6m before two days of positive inflows. However the amounts on Tuesday and Wednesday were quite small at $18.4 and $92m respectively. The smaller inflows could have had something to do with the FOMC meeting as well as the threat of the market’s reaction to proposed tariffs from February 1.

Source: Farside Investors (click to enlarge)

I am still positive on the overall Bitcoin picture from a fundamental perspective. The US being on a drive to build Bitcoin Strategic Reserves is a good thing as it will further enhance the Cryptos standing.

Another reason why I remain relatively optimistic is the recent on chain analysis by Glassnode. In the Executive Summary, Glassnode explained Cyclical Market Growth: Their take is that the rate of Bitcoin price appreciation has declined cycle by cycle, reflecting a path into market maturity. The drawdown profile of this cycle thus far closely resembles that of the 2015–2017 cycle. Prior cycles also hint at a potential acceleration phase in the bull market, which tends to occur around this time (relative to the cycle low).

This is just another reason that we could be due for another period of gains and potentially fresh all-time highs for BTC/USD.

Technical Analysis BTC/USD

Bitcoin (BTC/USD) from a technical standpoint printed a bullish engulfing candlestick yesterday with follow through today.

However, in order to convince bulls and myself that we could go on and achieve fresh all-time highs, i would like to see a daily candle close above the 106.200. This would be the highest daily close for Bitcoin and may embolden bulls to join the rally.

Bitcoin (BTC/USD) Daily Chart, January 30, 2025

Source: TradingView.com (click to enlarge)

Dropping down to a H2 chart and this could come to fruition after price broke out of the descending channel in play.

Price is currently pulling back with a possibility of a deeper pullback toward the 100-day MA resting just around the key support level at 103500.

This may present an excellent risk to reward opportunity for potential bulls with further support being found at the 102650 handle, where we have both the 50 and 200-day MAs restings.

Looking at potential barriers on the upside lie at 107140 before the 108000 109350 handles come into play.

Bitcoin (BTC/USD) Two-Hour (H2) Chart, January 23, 2024

Source: TradingView.com (click to enlarge)

Support

- 103500

- 102650

- 100000

Resistance

- 107140

- 108000

- 109350

ECB Review – A 25bp Rate Cut – Looking Towards the Spring

- The ECB's policy decision to cut 25bp was unanimously expected by markets and analysts, and furthermore there were no new policy signals.

- Incoming information since the December meeting supported the economic and inflation assessment in the ECB's December baseline, with an unchanged risk assessment. Hence, today's press conference will not be remembered as a key one. However, in the current environment, boring is good.

- Markets traded in a tight range through the press conference, and following the pre-meeting rally, markets are now discounting another 71bp of rate cuts this year. Markets rallied somewhat again after the end of the press conference.

No change in the macroeconomic assessment

The ECB's characterisation of the economy was a stagnating one that is set to remain weak in the near term as manufacturing continues to contract while services are expanding. The near-term weakness was noted due to fragile consumer confidence and households not getting sufficient encouragement from rising real rates, albeit with a robust yet softening labour market there are reasons to expect a recovery later this year, provided that trade tensions do not escalate. Also, rising real incomes and the gradually fading effects of restrictive monetary policy should support a pick-up in demand over time. Overall, risks to growth remains tilted to the downside, with the risk assessment wording essentially unchanged. On inflation, the ECB stated that 'Most measures of underlying inflation suggest that inflation will settle at around the target on a sustained basis. Domestic inflation remains high, mostly because wages and prices in certain sectors are still adjusting to the past inflation surge with a substantial delay'.

Direction is clear - end point unknown

During the press conference Lagarde said that today's decision to cut 25bp was a unanimous decision that all rallied behind. Looking ahead, the ECB is on route to deliver another rate cut at the March meeting, yet when asked the important question on where the cutting cycle will end, Lagarde didn't give any signals. However she did say that next week, on 7 February, ECB staff will publish a revision of r* estimates. For now, the ECB's monetary policy stance remains restrictive, and they are not at neutral - an acknowledgment from Lagarde as well. It is an 'entirely premature' debate according to Lagarde.

G10 Central Banks Start the Year in a Dovish Overall Mood

Summary

- It was a busy week for foreign central banks, with several institutions offering their first monetary policy assessment of 2025. The European Central Bank lowered its policy rate 25 bps to 2.75%, while repeating that inflation should converge to 2% by late this year and that growth remains weak. We expect 25 bps rate cuts in March, April, June and September, for a terminal policy rate of 1.75%.

- The Bank of Canada cut its policy rate 25 bps to 3.00%, but did not offer any future policy guidance amid tariff-related uncertainty. We would not interpret that as a hawkish signal, however, and indeed the central bank's modeling suggested higher tariffs would have a relatively rapid and substantial impact on economic growth, and a somewhat more gradual impact in boosting inflation. Our view remains for 25 bps rate cuts in March, April and June, which would see the policy rate reach a low of 2.25%.

- Sweden's Riksbank cut its policy rate 25 bps to 2.25%, while its accompanying statement was mildly dovish in tone. We think an accumulation of benign inflation and subdued activity data will see the central bank deliver a final 25 bps rate cut by May. In Australia, the latest inflation figures slowed more than forecast and pointed to an easing in domestic price pressures. We now expect the Reserve Bank of Australia to start its easing cycle with a 25 bps rate cut in February, and look for a cumulative 100 bps of policy rate cuts this year, to a low of 3.35%.

European Central Bank Continues Its Rate Cut Cycle

The European Central Bank (ECB) lowered its Deposit Rate by 25 bps to 2.75% at its first monetary policy announcement of 2025 and delivered an accompanying statement that, while not overtly dovish, is in our view consistent with further easing at upcoming meetings. Among the key points, the ECB said:

- The disinflation process is well on track, and that most measures of underlying inflation suggest that inflation will settle around the 2% target on a sustained basis.

- Domestic inflation remains high, but wage growth is moderating as expected and profits are partially buffering the impact on inflation.

- Monetary policy remains restrictive and the economy is still facing headwinds. On a more encouraging note, rising real incomes and the gradually fading effects of restrictive monetary policy should support a pick-up in demand over time.

With respect to policy guidance, the ECB said it will follow a data-dependent and meeting-by-meeting approach to its monetary policy decisions, and that it is not pre-committing to a particular rate path.

Comments from ECB President Lagarde at the post-meeting press conference did not deviate significantly from the initial ECB announcement. Lagarde said there were both upside and downside risks to inflation, but that risks to the growth outlook were tilted to the downside. Lagarde said the ECB would publish a report on the neutral policy interest rate in early February, while also adding that discussing where to stop interest rate cuts is premature—the latter an indication that further interest rate cuts should be forthcoming.

Overall, we don't see anything in today's announcement and post-meeting press conference that would prompt us to change our outlook for ECB monetary policy. Eurozone growth remains very sluggish, as evidenced by the flat quarter-over-quarter outcome for Q4 GDP, along with small quarterly declines for German and French Q4 GDP. Our view remains for further 25 bps rate cuts at the March, April, June and September meetings, which would see the Deposit Rate reach 1.75% by September, though the later rate cuts in particular would require a further deceleration in wages, services inflation and core inflation in the months ahead. Our view is more aggressive than currently expected by market participants, which anticipates a Deposit Rate of around 2.00% by September.

Bank of Canada Eases Monetary Policy Further Amid Increasing Uncertainty

The Bank of Canada (BoC) began 2025 by delivering a 25 bps policy rate cut to 3.00% at its January meeting, but did not offer any guidance on future monetary policy given the increasingly uncertain outlook amid the threat of higher tariffs from the United States. Also on the policy front, the BoC announced an end to quantitative tightening, saying that it would begin asset purchases in March, such that its balance sheet stabilizes and then grows modestly.

The BoC said that with inflation around 2% and the economy in excess supply, it decided to reduced interest rates further. The central bank described the cumulative 200 bps of rate reductions since last June as “substantial”, which could support some strengthening in consumption and housing activity, even as population growth slows given reduced immigration targets. The outlook for business investment remains weak. This overall outlook, notably, is based on economic projections which the Bank of Canada explicitly based on the absence of new tariffs and their economic impact. Those updated economic projections, based on unchanged tariffs, forecast:

- GDP growth of 1.8% in 2025 and 2026, weaker than the prior projections in October, but still stronger than an estimated 1.3% GDP growth in 2024.

- Slightly higher CPI inflation than previously, at 2.3% in 2025 and 2.1% in 2026. Those inflation forecasts are still close to the central bank's target, however. Moreover, the core CPI forecasts of 2.1% for end-2025 and end-2026, we largely unchanged, and also close to the central bank's target.

The BoC said that “setting aside threatened US tariffs, the upside and downside risks around the outlook are reasonably balanced.” But the central bank also said a protracted trade conflict would most likely lead to weaker GDP growth and higher prices, and would test the resilience of Canada's economy. Indeed, the BoC offered some insight into how higher U.S tariffs on Canada (a 25% rate) and an equivalent Canadian tariff retaliation (also a 25% rate) would affect the economic outlook. In this hypothetical scenario, the central bank's benchmark calibration or estimates:

- Envisaged a 2.5 percentage point hit to GDP growth in year one, a 1.5 percentage point hit to GDP growth in year two, and little impact on growth by year three.

- Envisaged a very modest boost to CPI inflation in year one, around a 0.5 percentage point boost to inflation in year two, and around a 1.0 percentage point boost to inflation in year three.

Overall, the Bank of Canada views the impact of tariffs in this scenario as having a relatively rapid and substantial impact on economic growth, and a somewhat more gradual impact in boosting inflation. Accordingly, we would not view the central bank's absence of future policy guidance as a hawkish signal, but simply an unusual lack of certainty about the outlook. Even if higher tariffs do transpire, we believe the BoC would be inclined to continue with its easing cycle. In that context, our view remains for 25 bps rate cuts at the March, April and June meetings, which would bring the BoC's policy rate to a low of 2.25%. The risks around that outlook are tilted toward a slightly more truncated easing cycle, with a June rate cut potentially the most at risk.

Riksbank Keeps Rate Cut Door Slightly Ajar

Sweden's central bank, the Riksbank, kicked off 2025 by lowering its policy rate 25 bps to 2.25%, and also offered a mildly dovish accompanying statement. The Riksbank said that inflation pressures are broadly consistent with the 2% target and that economic projections from December essentially still hold, forecasts that anticipated just one rate reduction in the first half of this year.

Still, the Riksbank said the risk of inflation becoming too high is limited at the same time that economic activity is weak (the Q4 GDP indicator rose 0.2% quarter-over-quarter, a bit less than the consensus forecast). The central bank said it “is prepared to act if the outlook for inflation and economic activity changes” and cited an uncertain global environment and geopolitical tensions. Given the mildly dovish statement, we believe an accumulation of evidence will eventually see the Riksbank cut rates further. If inflation remains benign and if economic activity shows a renewed softening, we expect a final 25 bps policy rate cut to 2.00% at the Riksbank's May meeting. That said, if economic trends are especially weak, there is a risk that rate cut could come earlier, at the March announcement.

Benign Inflation To Quicken Reserve Bank of Australia Easing

While Australia was not among the central banks to announce a policy decision this week, there was nonetheless some significant and relevant news for the monetary policy outlook. Australia's Q4 and December CPI outcomes were benign, in our view, indicating that the Reserve Bank of Australia (RBA) is on course to return inflation to its medium-term 2%-3% target range. With respect to the more closely followed quarterly CPI readings, headline inflation slowed more than expected to 2.4%. Core inflation measures also slowed more than forecast, with trimmed mean inflation printing at 3.2% and weighted median inflation printing at 3.4%. While the annual increase in the core inflation measures are still above the top of the target range, the small quarterly increase in both measures suggests that on a shorter timeframe, underlying inflation may already be trending in line with target.

The December monthly CPI readings are also consistent with overall ongoing deceleration. While December headline inflation did tick higher to 2.5% year-over-year, trimmed mean inflation slowed further to 2.7%—inside the target range. This week's inflation data comes after December employment jumped by 56,300, although that report also revealed a drop in full-time jobs and a slight rise in the jobless rate. However, we think the benign CPI outcome will tip the RBA toward easing monetary policy earlier than we had previously forecast. We now expect the RBA to lower its policy rate by 25 bps in February, with 25 bps rate cuts also seen in May, August and November, which would see the RBA's policy rate reach a low of 3.35% by the end of this year.

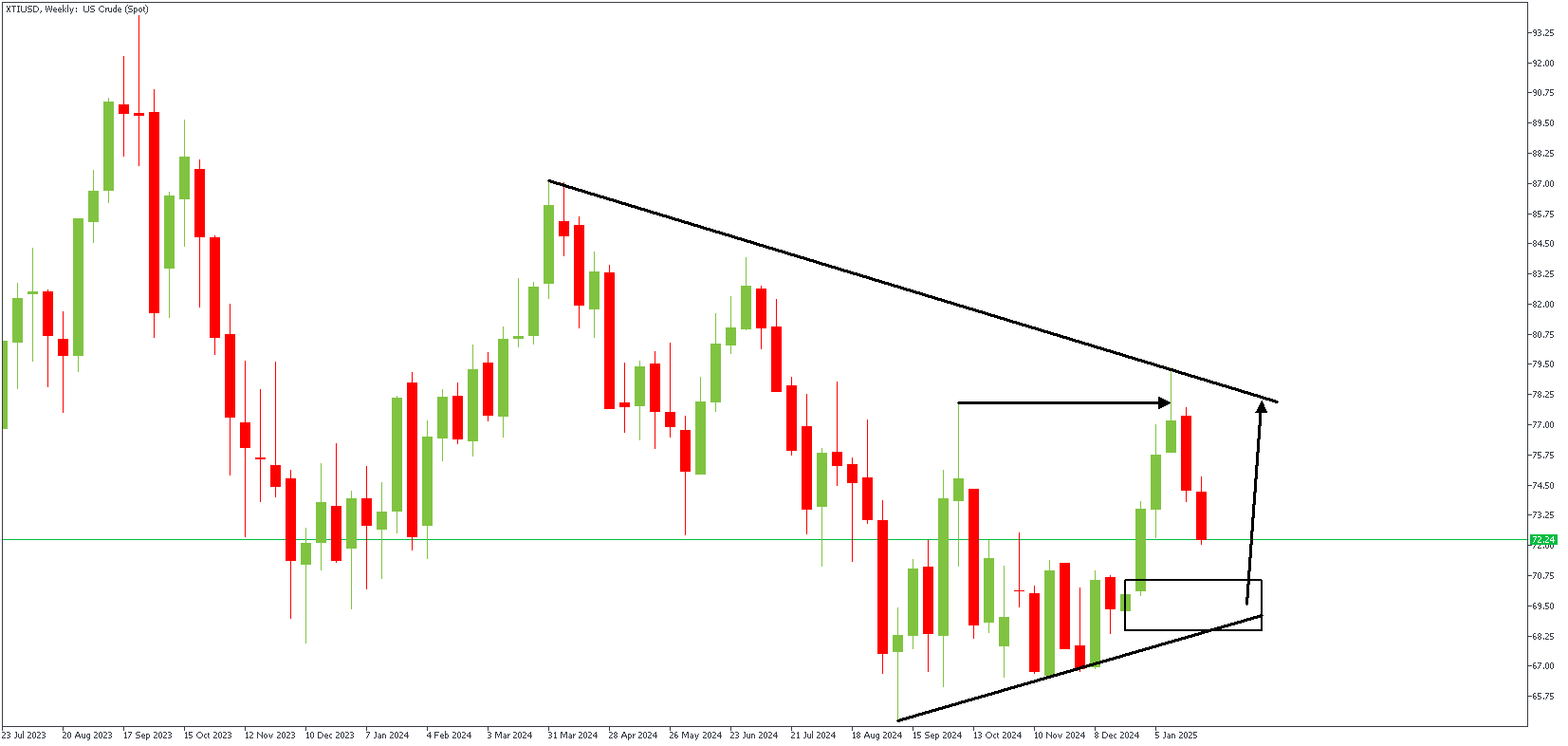

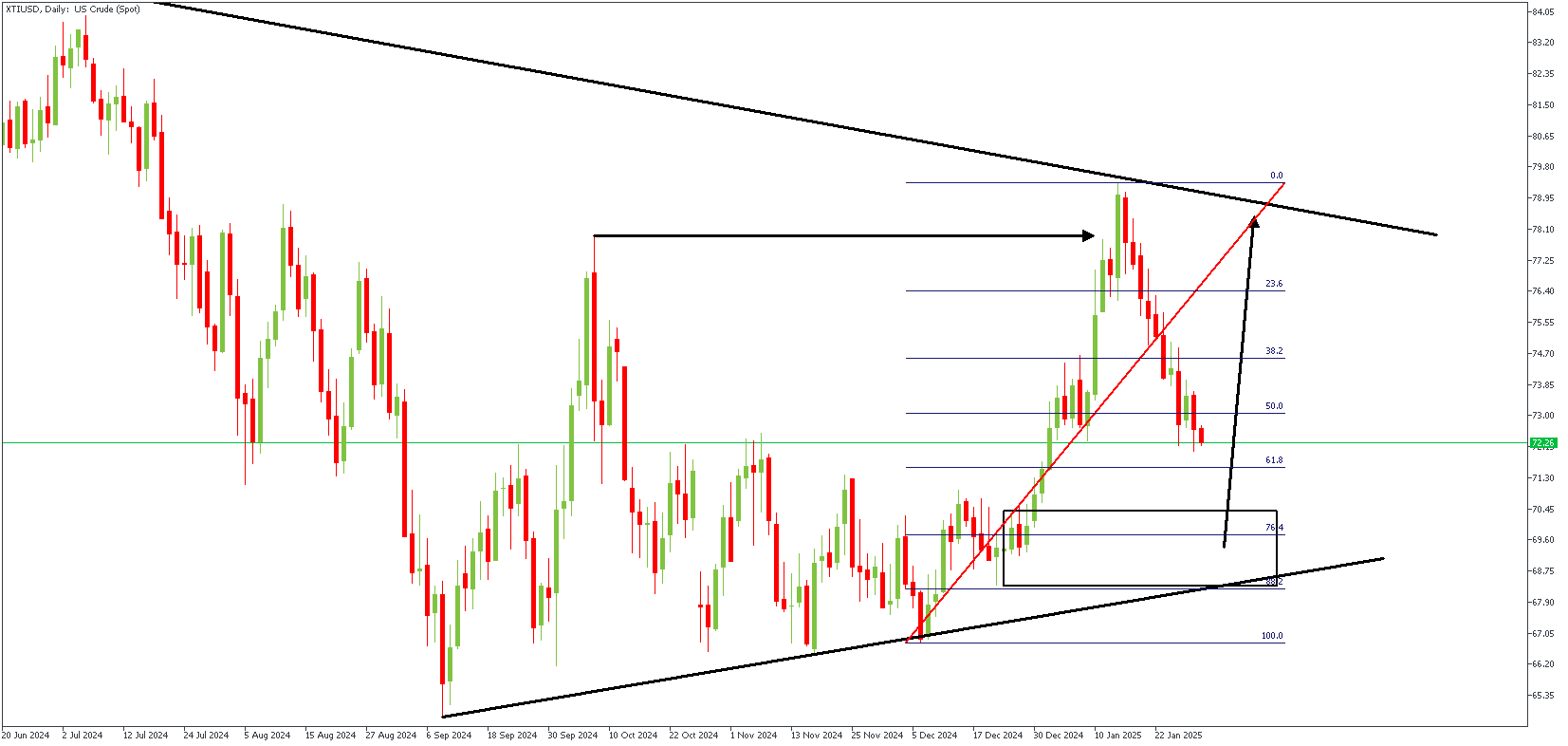

XTIUSD Price Action Breakdown

Oil and natural gas prices remain unstable as traders react to global tensions and trade uncertainties. Crude oil prices stayed steady as markets evaluated how new tariff measures might affect significant energy suppliers. Meanwhile, U.S. oil stockpiles grew by 3.46 million barrels, likely due to lower demand after recent weather disruptions.

Oil (XTIUSD) is trading at $72.51, down 0.61%, struggling to rise above the key level of $73.49. If prices break above this point, they could climb toward $74.93 or even $75.95, but if they fail to do so, oil may drop to $72.32 or $71.25.

XTIUSD – W1 Timeframe

The weekly timeframe chart of XTIUSD shows a recent break above the previous high. The price is currently trading near the FVG (Fair Value Gap) created by the impulse move. The highlighted zone is the expected area of interest to watch for a bullish confirmation. The lower timeframe lends clarity to the area.

XTIUSD – D1 Timeframe

On the daily timeframe chart of XTIUSD, we see the price sliding towards the drop-base-rally demand zone at the origin of the impulse move. The demand zone also features an SBR (Sweep-Break-Retest) pattern and overlaps the 76% Fibonacci retracement level – powerful confluences favoring the bullish sentiment.

Analyst’s Expectations:

- Direction: Bullish

- Target: 77.94

- Invalidation: 66.50

Sunset Market Commentary

Markets

The ECB lowered the key policy rate by 25 bps to 2.75%. The fifth reduction was unanimous, widely expected and came with some minor tweaks to the statement. While inflation is converging to the 2% target, the ECB scratched the notion that domestic inflation is edging lower. Instead it now only states that it remains high, mostly due to strong (but moderating) wage growth. Just as the Riksbank and Bank of Canada earlier this week, the ECB highlights how its recent rate cuts are now gradually filtering through. Lagarde during the presser explicitly mentioned the cumulative amount (125 bps), leaving a short moment of silence afterwards. This can be seen an early indication that back-to-back cuts make room for a more cautious easing pace. Gradually fading effects of restrictive monetary policy along with rising real incomes continues to underpin hopes for a demand-led recovery. Growth risks remain tilted to the downside. Among the risk factors, president Lagarde mentioned greater friction in global trade. The introductory statement does not say what such a scenario would mean for inflation though, only that it makes the outlook more uncertain. When asked, Lagarde, just as Powell yesterday, said it is too early to draw any conclusions from what has been announced (by the Trump administration) so far. The central bank still sticks to a data-dependent and meeting-by-meeting approach without pre-coming to a particular rate path. The first question from the audience was nevertheless about the way forward, referring amongst others to Board Member Schnabel who said the ECB is now nearing the neutral rate. Lagarde deflected by referring to the March meeting as one with updated forecasts that will substantiate the decision then without looking beyond that. She did flag an upcoming staff publication, Feb 7, on the revision of the natural interest rate. The timing, ahead of the March 6 meeting when another rate cut brings the deposit rate to the upper bound of the/Schnabel’s neutral rate estimates, is not a coincidence. Euro area yields slip 7/9 bps today but that’s mostly the result of disappointing GDP numbers in France and Germany. The euro tried to gain against the dollar (1.042) but the move lacked traction. Strong US GDP figures (2.3% Q/Qa) also muddied the market reaction. A strong consumer performance (4.2% Q/Q, from Q3’s 3.7%) made up for the growth deceleration compared to Q3 or the slight expectations miss (2.6%). It alone carried the US economy in Q4, contributing 2.8% to the print. Inventory depletion (-0.93 ppts) was the main drag. Net exports were flat while the government contributed 0.4 ppts. Combined with low weekly jobless claims it showcases ongoing strength of world’s number 1 economy. The headline price deflator picked up from 1.9% to 2.2% over Q4, less than the 2.5% expected. The core gauge matched the 2.5% estimate (from 2.2%). US yields ease less than 2 bps.

News & Views

The Belgian Statistical Office (Statbel) today reported that inflation in the country accelerated to 1.39% M/M and 4.08% (0.4% and 3.16% in December). The biggest contributions came from electricity, domestic services, milk products and natural gas. Prices for mobile telephony, hotel rooms and travels decreased. Core inflation accelerated to 3.14%Y/Y from 2.91%. Energy inflation (15.89% Y/Y from 7.4%) was an important driver of upward headline price pressures. Compared to last month, natural gas prices increased by 2.7% and those for electricity by 8.8%. The high recent (energy) inflation is due base effects. This will continue to have an upward impact on inflation up to February 2025. Inflation for services increased to 4.13% from 3.94%. Inflation for rents has decreased to 3.41% from 4.22%. Food inflation now stands at 2.54% compared to 1.85% last month. The first inflation estimate according to the European harmonised index of consumer prices (HICP flash estimate) for Belgium amounts to 4.4% in January 2025.

Hungarian GDP rebounded 0.5% Q/Q in Q4 compared to the previous quarter. This means that the economy left a technical recession after negative figures in Q3 (-0.6% Q/Q) and Q2 (-0.2%). Activity in Q4 last year was 0.2% higher Y/Y. For the whole of 2024, activity growth was a very modest 0.6% Y/Y. Statistics Poland also released a preliminary estimate of 2024 growth. Activity in the country last year increased 2.9% compared to the whole of 2024. Total consumption expenditure increased by 4.0% compared with the previous year, with household consumption increasing 3.1%. Gross fixed capital formation rose by 1.3%. Looking at gross value added, the economy grew 2.1% in 2024. Gross value added in the industry increased 1.0%. Valued added in construction decreased by 6.7% and increased in trade and repair (2.3%).

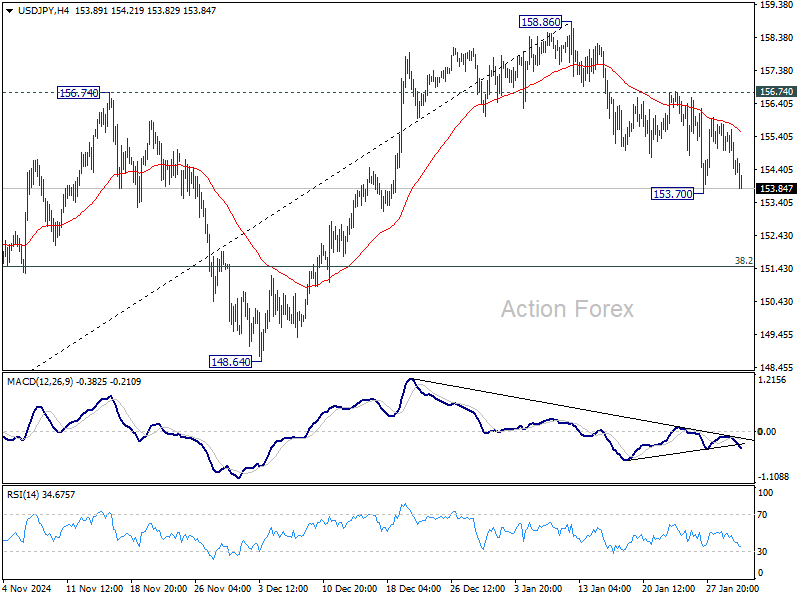

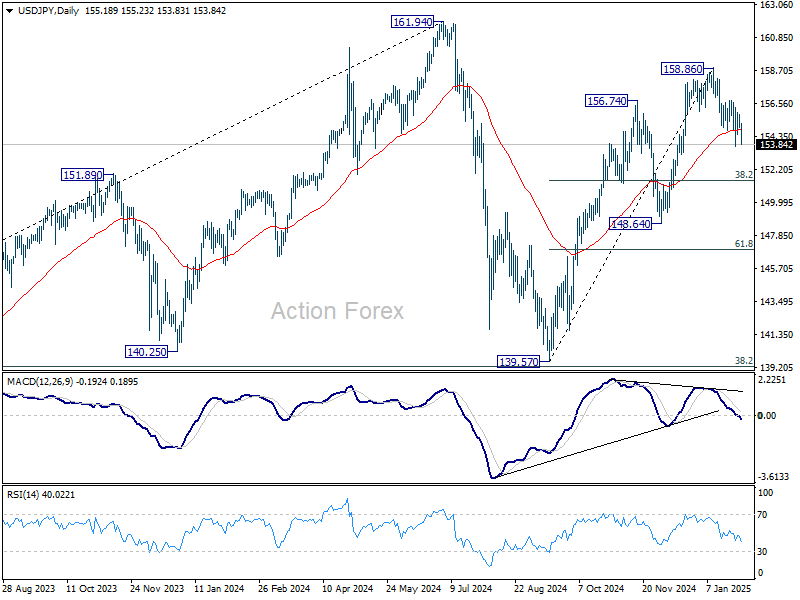

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 154.86; (P) 155.33; (R1) 155.71; More...

USD/JPY dipped notably today but stays above 153.70 temporary low and intraday bias remains neutral. On the downside, firm break of 153.70 will resume the fall from 158.86 to 38.2% retracement of 139.57 to 158.86 at 151.49. Nevertheless, break of 156.74 resistance will indicate that fall from 158.86 has completed as a correction. Intraday bias will be back on the upside for 158.86 and above to resume the whole rally from 138.57.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

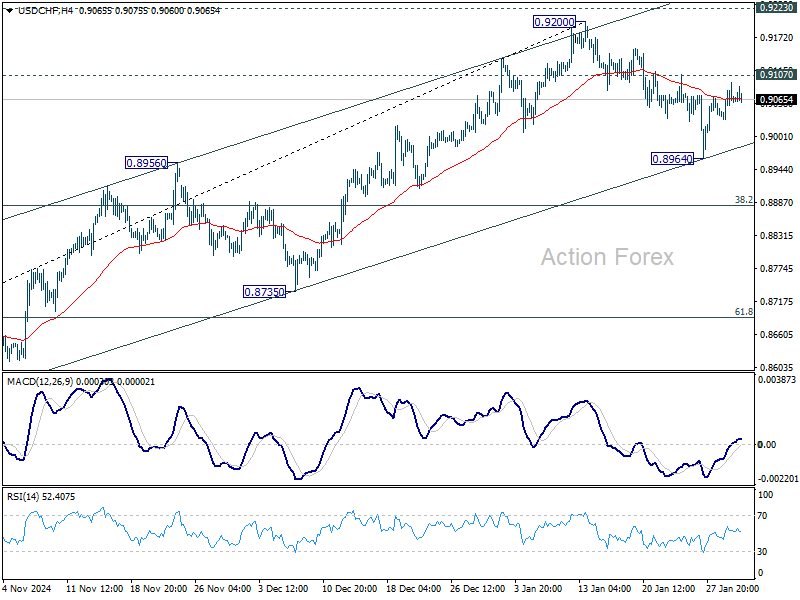

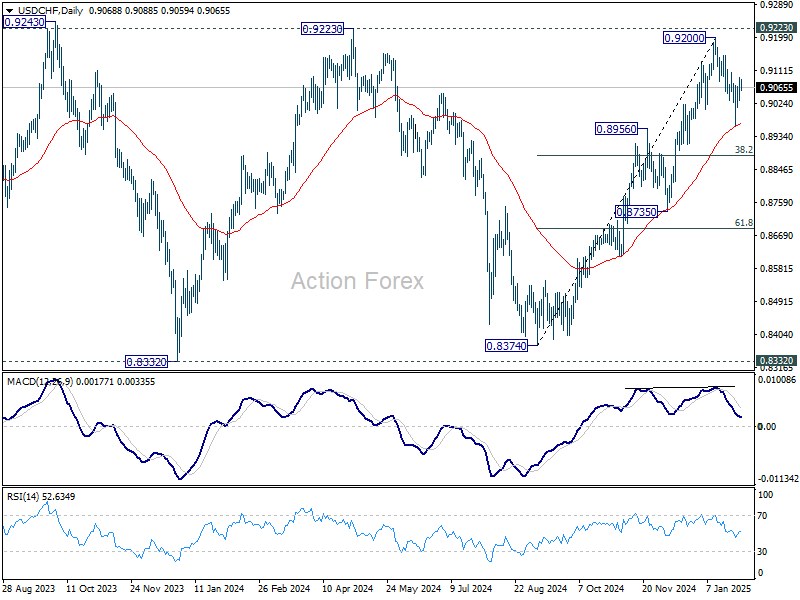

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9036; (P) 0.9065; (R1) 0.9099; More…

USD/CHF is hovering around 55 4H EMA as recovery from 0.8964 stalled. Intraday bias remains neutral for the moment. Overall, rise from 0.9374 stays intact with strong support seen from near term rising channel. On the upside, break of 0.9107 will target 0.9200 and 0.9223 key resistance. On the downside, however, break of 0.8964 will resume the fall from 0.9200 to 38.2% retracement of 0.8374 to 0.9200 at 0.8884 next.

In the bigger picture, as long as 0.9223 resistance holds, price actions from 0.8332 (2023 low) are seen as a medium term corrective pattern. That is, long term down trend is in favor to resume through 0.8332 at a later stage. However, sustained break of 0.9223 will be an important sign of bullish trend reversal.

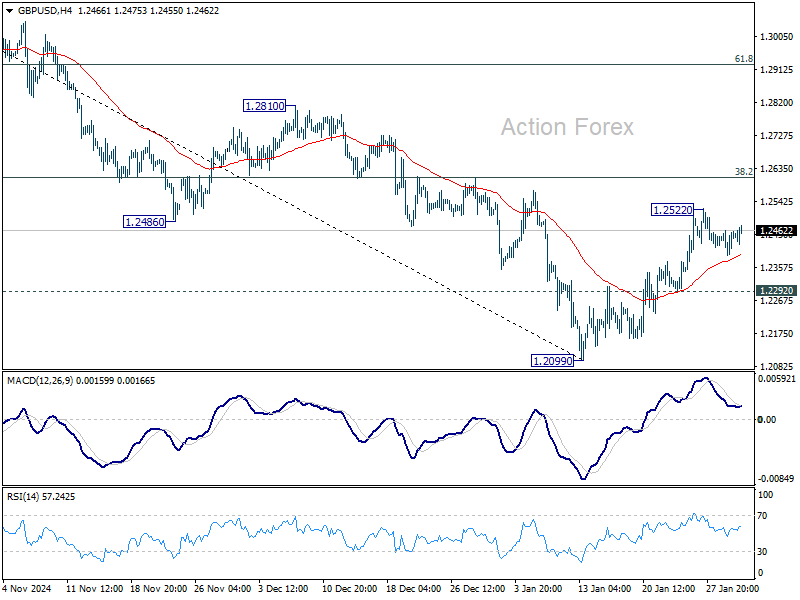

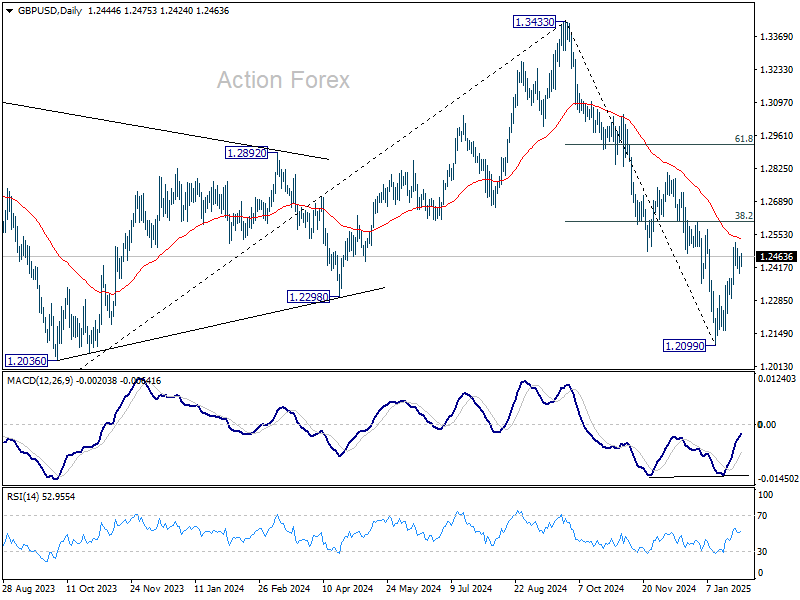

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2409; (P) 1.2436; (R1) 1.2480; More...

GBP/USD is still bounded in established range below 1.2522 and intraday bias remains neutral for the moment. Outlook is unchanged that rebound from 1.2099 is seen as a corrective move. While another rise cannot be ruled out, strong resistance could be seen 38.2% retracement of 1.3433 to 1.2099 at 1.2609 to limit upside. On the downside, below 1.2292 minor support will bring retest of 1.2099 low. However, sustained trading above 1.2609 will raise the chance of reversal and target 61.8% retracement at 1.2923.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

U.S. Economic Growth Eased But Remained Healthy at the End of 2024

The U.S. economy expanded by 2.3% quarter-on-quarter (q/q, annualized) in the fourth quarter, a touch lower than the consensus forecast of 2.6%. Growth for 2024 as a whole was 2.8%, showing little slowing from 2023's 2.9% pace.

Consumer spending defied expectations for a slowdown, accelerating to 4.2% q/q from 3.7% in the previous quarter. The gain was driven by goods spending (+6.6% q/q), and more specifically a 12% gain in durable goods outlays. Spending on services grew by a healthy 3.1%, up from 2.8% in Q3.

Gross private domestic investment was a drag, falling 5.6% q/q. Looking at the details, non-residential investment was down 2.2% – largely on the back of a 7.8% decline in equipment spending, which came after two solid quarters of growth. Structures also fell 1.1%, while investment in intellectual property products grew 2.6%. On the other hand, residential investment improved after two quarters of contraction, rising 5.3% q/q.

Government spending provided a boost, growing at 2.5% q/q, even as this marked a deceleration from the 5.1% pace in the previous quarter. State & local government spending eased to 2% from 2.9% previously.

On international trade, both imports and exports retreated by 0.8 q/q. The end result was a wash, with net trade leading to a miniscule positive fillip for GDP.

Final domestic demand was up a healthy 3.1% q/q, a deceleration from Q3's gain of 3.7%. Headline GDP growth was held back by weaker inventory investment, which subtracted 0.9 percentage points from the overall tally last quarter.

Core PCE inflation – the Fed's preferred inflation gauge – rose to 2.5% q/q (annualized), a mild acceleration from Q3's 2.2% pace.

Key Implications

The U.S. economy notched another solid quarter at the end of 2024, even as growth eased a touch from the stronger pace experienced in the third quarter. Non-residential investment and inventories weighed on growth, but the consumer helped save the day, powering growth with another outsized gain in goods spending. A meaningful improvement in residential investment also helped provide some support. The fact that the economy basically sustained 2023's pace into 2024 is an impressive accomplishment in the face of what is still an elevated interest rate environment.

While there's still plenty of uncertainty with changes coming out of Washington, we anticipate a more trend-like pace of growth of around 2% for the year ahead. This as the economic cycle matures, and some of the positive growth impulses from policies such as deregulation are offset by more restrictive policies on trade and immigration. Additionally, efforts to rein in government spending suggest that the fiscal growth-dividend that helped boost growth in previous years – such as in 2018-19 thanks to the Tax Cuts and Jobs Act (TCJA) – may not be there to prop up this economy this time around, reinforcing the case for a more trend-like pace of growth

EUR/USD Stable as the Market Absorbs Fed Decision and Awaits ECB Meeting

The EUR/USD pair is consolidating around 1.0426 on Thursday as investors digest the Federal Reserve’s latest policy decision and shift their focus to the upcoming European Central Bank (ECB) meeting.

Key market influences

As widely expected, the Federal Reserve held its interest rate steady at 4.5% per annum. In its commentary, the central bank reaffirmed its commitment to reducing its balance sheet at a pace of 25 billion USD per month. Fed Chair Jerome Powell stated that inflation does not necessarily need to fall to 2% before considering rate cuts. He also supported banks' provision of crypto services, a move that signals openness to financial innovation.

Notably, Powell indicated that the Fed is in no rush to lower interest rates. The central bank monitors stock market valuations closely, expressing concerns that some assets may be significantly overvalued. Interestingly, Powell avoided commenting on US President Donald Trump’s repeated calls for immediate rate cuts.

Earlier reports suggested that Trump may push for a policy allowing US presidents to have a say in setting interest rates. While the Fed remains independent for now, the issue could resurface in political discussions.

Technical analysis of EUR/USD

On the H4 chart, EUR/USD moved downward to 1.0382, forming a corrective wave towards 1.0437. After completing this correction, the pair is likely to resume its decline, with an initial target at 1.0345. A brief correction to 1.0437 may follow before the downtrend extends towards 1.0050. The MACD indicator supports this outlook, with its signal line positioned above zero but trending downwards, indicating bearish momentum.

On the H1 chart, the pair consolidated around 1.0437 before breaking lower to reach a local target at 1.0382. A corrective move towards 1.0437 is now likely before the pair resumes its decline towards 1.0345, with a potential continuation to 1.0160. The Stochastic oscillator confirms this scenario, with its signal line above 80 but pointing downward towards 20, signalling the likelihood of further losses.

Conclusion

The EUR/USD pair remains stable following the Fed’s policy announcement, with attention shifting to the ECB’s upcoming meeting. The Fed’s cautious stance on rate cuts supports the USD, while uncertainty surrounding Trump’s potential influence over monetary policy adds another layer of complexity. Technical indicators point to further downside potential for EUR/USD, with key targets at 1.0345 and 1.0160. The next major moves depend on the ECB’s policy outlook and broader market sentiment.