Sample Category Title

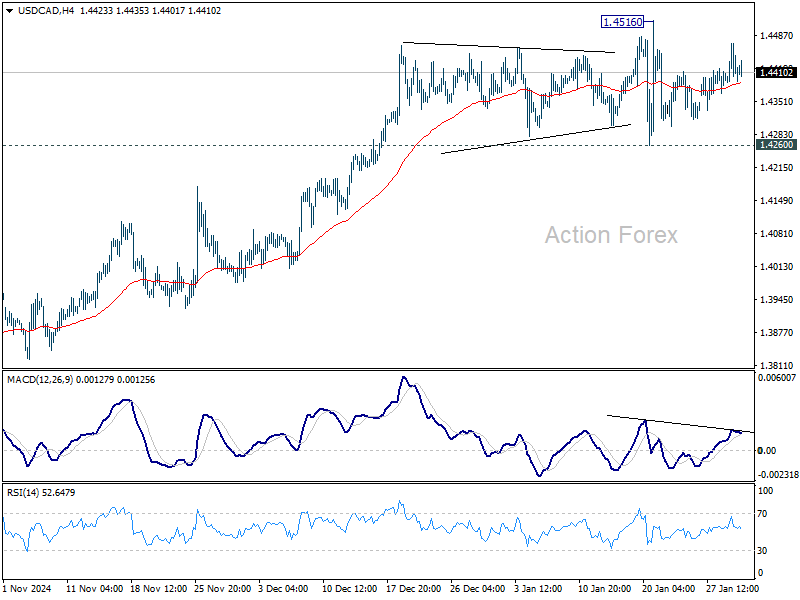

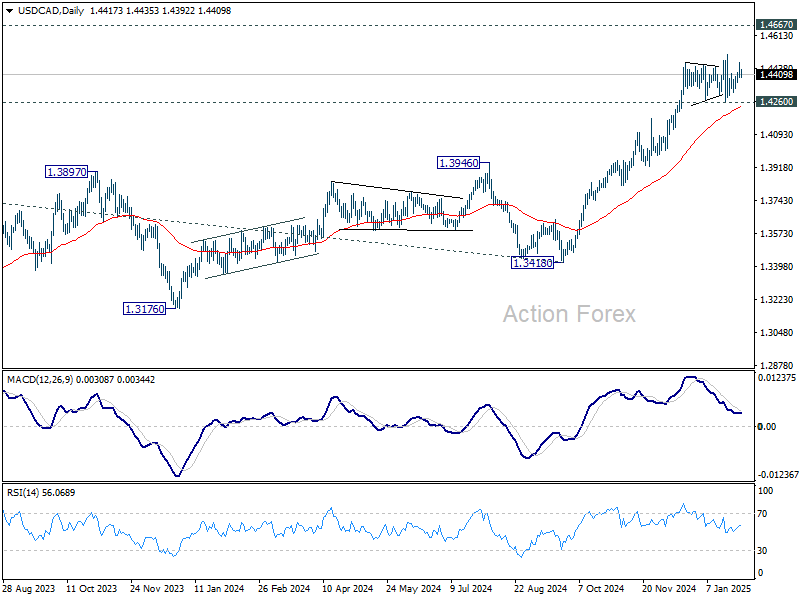

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4383; (P) 1.4427; (R1) 1.4465; More...

USD/CAD is still bounded in range trading below 1.4516 and intraday bias stays neutral. More consolidations would be seen, but further rally is expected as long as 1.4260 support holds. On the upside, firm break of 1.4516 will resume larger up trend to 1.4667/89 key resistance zone. Nevertheless, firm break of 1.4260 will turn bias to the downside for deeper pullback through 55 D EMA (now at 1.4241).

In the bigger picture, up trend from 1.2005 (2021) is in progress for retesting 1.4667/89 key resistance zone (2020/2015 highs). Decisive break there will confirm long term up trend resumption. Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. Medium term outlook will remain bullish as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.

ECB Rate Cut Takes Center Stage, as FOMC Hold Triggers Minimal Reaction

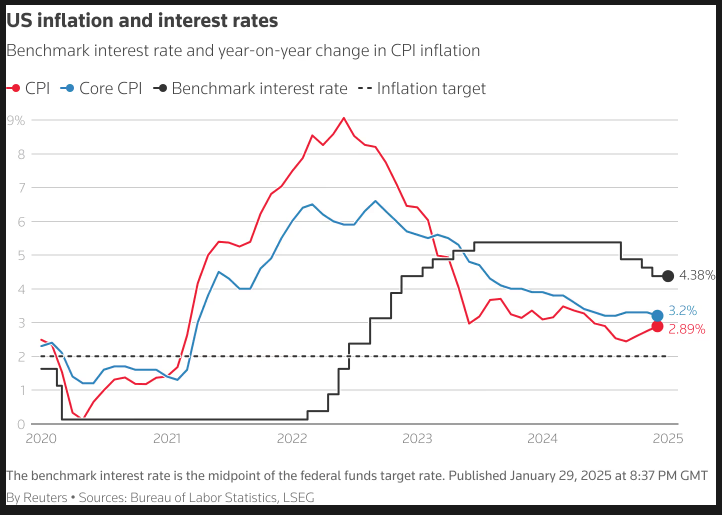

FOMC rate decision and press conference yesterday proved to be a non-event. Dollar remained firm following the decision to keep interest rates unchanged at 4.25–4.50%. Fed Chair Jerome Powell reinforced a patient approach to policy adjustments, stating, "we do not need to be in a hurry to adjust our policy stance." He also emphasized the risks of premature easing, warning that "reducing policy restraint too fast or too much could hinder progress on inflation." His remarks reaffirmed expectations that Fed is unlikely to cut rates in the near term, with market pricing now assigning an 82% probability of another hold in March, up from 73% last week.

Meanwhile, US President Donald Trump renewed his criticism of Fed, accusing it of failing to manage inflation and misjudging bank regulations. Trump demanded last week that "interest rates drop immediately". However, markets largely ignored his remarks, as Powell’s measured tone continues to shape expectations for a prolonged hold on interest rates.

Attention now turns to ECB as it concludes this week’s round of major central bank meetings. ECB is widely expected to continue its "regular, gradual" easing path by cutting the deposit rate by 25bps to 2.75%, moving closer to the estimated neutral range of 1.75–2.25%.

Market pricing suggests a terminal rate of around 2.00% by late spring or early summer, but ECB President Christine Lagarde is unlikely to provide a clear roadmap just yet. With uncertainty surrounding US trade policy and potential tariff escalations, Lagarde is expected to maintain a data-dependent stance rather than commit to a specific easing path.

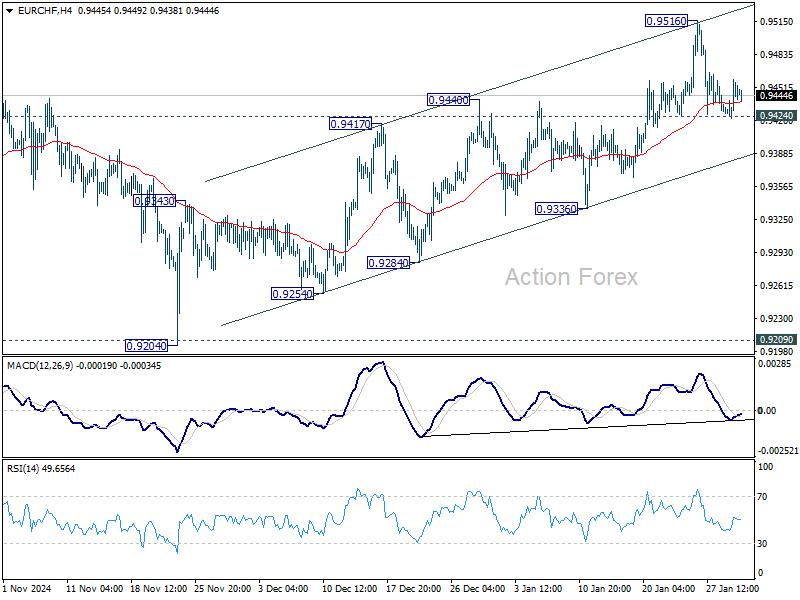

Technically, while EUR/CHF's choppy rebound from 0.9204 extended last week, momentum continue to be unconvincing. It's still more likely that not that this rebound is merely a corrective move. Firm break of 0.9242 support will be an early sign that this correction bounce has completed, and bring deeper fall to channel support (now at 0.9398) for more evidence.

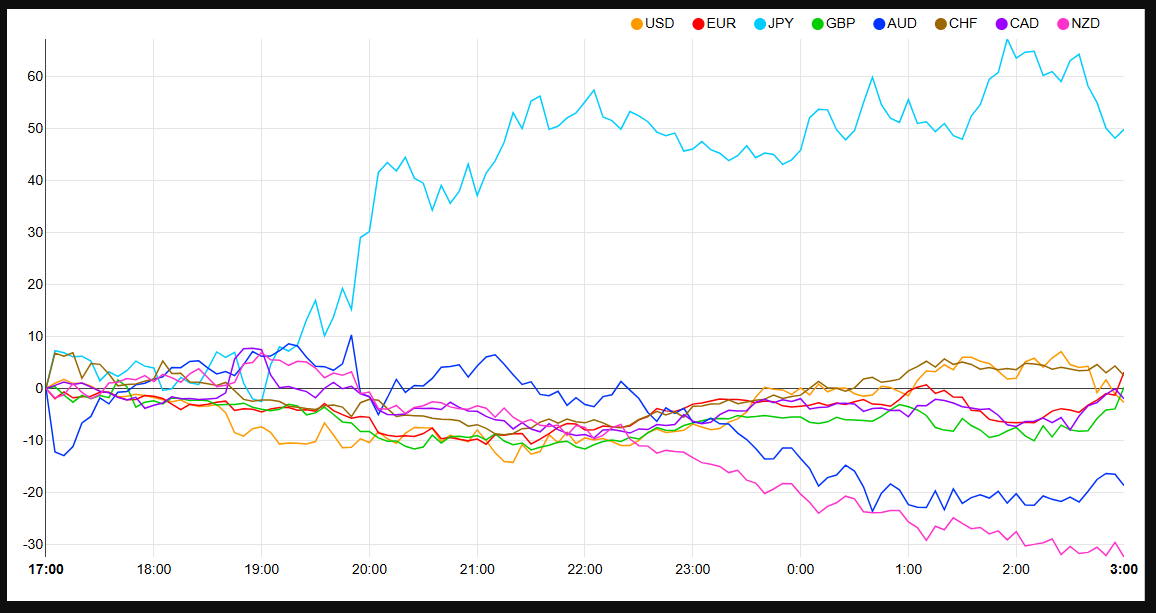

Overall for the week so far, Yen is still the strongest, followed by Dollar, and then Swiss Franc. Aussie is staying at the bottom, followed by Kiwi, and then Loonie. Euro and Sterling are stuck in the middle.

Swiss KOF rises to 101.6, led by manufacturing and services

Switzerland’s KOF Economic Barometer climbed to 101.6 in January, up from 99.6 and surpassing market expectations of 100.5. This data suggests modest pickup in economic momentum, particularly in production-side sectors.

According to KOF, "the majority of the production-side indicator bundles included in the KOF Economic Barometer show positive developments."

The strongest contributions came from manufacturing, financial and insurance services, hospitality, and other service industries, signaling resilience in key sectors of the Swiss economy.

However, the outlook remains uneven. While production indicators strengthened, demand-side indicators showed signs of weakness. KOF noted that both "the indicator bundles for foreign demand as well as for private consumption indicate a downward tendency," highlighting subdued consumer activity and external trade concerns.

BoJ’s Himino reiterates further hike possible if economic forecasts hold

BoJ Deputy Governor Ryozo Himino reinforced expectations that the central bank could raise interest rates further if its economic and price projections are met.

Speaking today, Himino stated, "If our economic and price forecasts are achieved, we will raise our policy rate accordingly and adjust the degree of monetary support."

Himino also highlighted concerns about Japan’s prolonged period of negative real interest rates, describing the situation as "not normal."

He explained that an ideal economic scenario for Japan would involve rising wages and corporate profits, fueling stronger consumption and investment, which would then support moderate and stable inflation. In such a case, Japan could see real interest rates turn positive.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4383; (P) 1.4427; (R1) 1.4465; More...

USD/CAD is still bounded in range trading below 1.4516 and intraday bias stays neutral. More consolidations would be seen, but further rally is expected as long as 1.4260 support holds. On the upside, firm break of 1.4516 will resume larger up trend to 1.4667/89 key resistance zone. Nevertheless, firm break of 1.4260 will turn bias to the downside for deeper pullback through 55 D EMA (now at 1.4241).

In the bigger picture, up trend from 1.2005 (2021) is in progress for retesting 1.4667/89 key resistance zone (2020/2015 highs). Decisive break there will confirm long term up trend resumption. Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. Medium term outlook will remain bullish as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.

US Dollar Index (DXY) Analysis: Hawkish FOMC Pause, Trump’s Fed Criticism, and Technical Outlook

- The Federal Reserve held interest rates steady and signaled a “wait and see” approach as uncertainties remain.

- US Commerce Secretary Nominee Lutnick expressed support for sweeping tariffs, claiming they don’t impact inflation.

- President Trump blamed the Fed for inflation, escalating tension between him and the central bank.

- The US Dollar Index (DXY) experienced volatility following the FOMC, but struggles at key resistance level.

The FOMC meeting has officially passed and let me start by saying that there were no real surprises. Looking at Fed Chair Powell’s press conference, the Fed Chair delivered a very balanced statement, keeping all market participants interested in the Central Bank’s next moves.

Fed Chair Powell said that there would be no rush to cut rates again until inflation and jobs data made it more appropriate. No surprises here, as I have been saying in many articles of late there are too many uncertainties around the US economy moving forward. Most of this comes down to how markets will react to the implementation of tariffs as well as their potential effect.

Yesterday we heard some interesting comments from US Commerce Secretary Nominee Lutnick who is the frontrunner for the position. Lutnick stated that is in favor of sweeping tariffs saying it does not impact inflation. Lutnick was also hawkish on China which does not bode well for markets moving forward.

All of these uncertainties are the main reasons the Fed needed to adopt a more balanced and an almost ‘wait and see’ approach moving forward.

Currency Strength Chart: Strongest JPY, EUR, CHF, GBP, CAD, USD, AUD, NZD – Weakest

Source: FinancialJuice (click to enlarge)

President Trump and Fed on a Collision Course?

President Trump has never been the biggest fan of the Federal Reserve and has not directly called for lower rates yet as he promised but did blame inflation on the Fed. Yesterday the President said that If the Fed had spent less time on DEI, gender ideology, “green” energy, and fake climate change, inflation would never have been a problem.

Whether or not you agree with President Trump, there does appear to be some friction which may come to a head in the coming months. When asked yesterday about President Trump, Federal Reserve Chair Jerome Powell did not comment but said he had not been in touch with the President.

This will come to a head at some stage and is worth keeping an eye on as well over the coming weeks and months.

Key Comments from Chair Powell

A quick summary of some of the key comments from Fed Chair Powell yesterday.

- Economy has made “significant progress toward goals”

- Inflation has moved much closer to goal remains somewhat elevated

- Labor market is not a source of inflationary pressures

- Fed does “not need to be in a hurry to adjust policy”

- Fed to continue meeting-by-meeting approach

- Fed’s 2% long-term inflation goal will not change

The inflation conundrum is also something the Fed needs to consider given the recent uptick has come ahead of any proposed tariffs being implemented.

Source: LSEG (click to enlarge)

The Fed will now get a peak at their preferred inflation gauge, the PCE data due for release tomorrow. Markets are expecting consumer spending MoM to have ticked up to 0.5% from a previous 0.4% with the YoY print forecast to rise to 2.6% from a previous 2.4%.

Technical Analysis and DXY Reaction

US Dollar Index (DXY)

The US Dollar index rose briefly after the Powell presser yesterday but struggled to push on.

The US Dollar has been on a rollercoaster of late, with tariff chatter either supporting the US Dollar or dragging it lower.

This is likely to continue over the coming days until more clarity on the tariff picture is given. President Trump remains on course to implement 25% tariffs on Mexico and Canada on February 1, such a move could aid the US Dollar and provide support. However, any retaliatory tariffs may then see the Dollar face some weakness.

Looking at the DXY chart below and as you can see, the 108.00 handle has stood firm over the past two days, with yesterdays wick to the upside a sign of selling pressure. The daily candle closed as an inverted hammer which usually hints at further upside. However, the fact that the inverted hammer was printed at a resistance level means that further upside may not materialize.

Immediate resistance rests at 108.00 before the 108.49 comes into focus.

Support rests at 107.00 before the 106.13 and 105.63 handles come into focus.

US Dollar Index (DXY) Daily Chart, January 30, 2025

Source: TradingView.com (click to enlarge)

Support

- 107.00

- 106.13

- 105.63

Resistance

- 108.49

- 109.52

- 110.00

Nasdaq 100 Hovering Near Weekly Highs in a Volatile Week

As shown on the 4-hour chart of the Nasdaq 100 (US Tech 100 mini on FXOpen), the index stood around the 21,600 level this morning, near the weekly high that formed at Monday’s open.

This suggests that the tech-stock index has almost fully recovered from the decline triggered by the launch of AI from the Chinese startup DeepSeek. According to media reports:

→ Experts have pointed to signs that the Chinese startup used a technique known as “distillation” – in simple terms, this means that DeepSeek’s model extracted knowledge from more advanced models such as ChatGPT. In other words, this is not about innovation but rather an unfair practice.

→ Nassim Taleb believes that the sharp drop in NVDA shares is only the beginning of a potential market downturn inflated by AI-driven expectations. Further declines could be more significant than what we witnessed on Monday.

Apart from news surrounding DeepSeek, traders were also focused on earnings reports from major corporations (which we will cover in detail in separate articles):

→ Tesla (TSLA) is holding above $400 in pre-market trading today, despite earnings per share falling short of expectations. Meanwhile, company executives believe that Trump’s policies could negatively impact Tesla’s operations.

→ Microsoft (MSFT) shares fell by more than 4%, Meta Platforms (META) surpassed $700 per share in post-market trading for the first time, and IBM surged by approximately 9%.

Additionally, the fundamental backdrop became even more eventful following yesterday’s Fed updates, which, however, contained no surprises:

→ As expected, interest rates remained unchanged.

→ According to The Wall Street Journal, the Fed has entered a “Wait-and-See” phase, showing less confidence that inflation will continue to decline.

The Nasdaq 100 (US Tech 100 mini on FXOpen) chart reveals that the price:

→ Tested a key support line (marked in blue) at the weekly low.

→ Remains within the red descending channel.

From a bullish perspective, the red channel can be seen as a large-scale correction within the broader uptrend on higher timeframes.

From a bearish perspective, the bearish gap that formed at Monday’s open may act as resistance. Whether bulls will be able to overcome this barrier in the near term will depend, among other factors, on the next batch of earnings reports from major tech companies.

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Dollar Slightly Strengthened after the Fed Meeting

Yesterday’s Fed meeting proceeded in line with expert forecasts. The base interest rate remained at 4.50%. Jerome Powell, who spoke after the Fed’s decision was announced, did not clarify the future direction of monetary policy. The head of the US regulator, in particular, noted that the Fed would not rush to cut rates and that, in order to change the course of monetary policy, real progress in reducing inflation needed to be seen.

GBP/USD

The GBP/USD currency pair tested key support at 1.2400 yesterday. At the moment, the price is holding above this level, and if positive news for the pound emerges, the pair could rise towards recent highs at 1.2530–1.2500.

If GBP/USD buyers manage to consolidate the price above 1.2570 in the coming trading sessions, the pair may continue to rise towards 1.2660–1.2610. A break below the 1.2400 support level could trigger a renewed decline towards 1.2320–1.2260.

Key events that could influence GBP/USD movements:

- Today at 12:30 (GMT+2): Bank of England consumer credit data

- Today at 16:30 (GMT+2): US GDP

- Today at 16:30 (GMT+2): US initial jobless claims

- Tomorrow at 16:30 (GMT+2): US core personal consumption expenditure price index

EUR/USD

The EUR/USD currency pair fell below 1.0400 yesterday following the Fed’s rate decision. However, euro buyers managed to push the price back up to 1.0440. Today is another important day for EUR/USD in terms of fundamentals. Analysts predict that the ECB may lower the base interest rate from 3.15% to 2.90%. Comments from Christine Lagarde on the regulator’s future monetary policy will also be significant.

If incoming data is perceived as positive for EUR/USD, the price could once again test key resistance at 1.0540–1.0500. A break below yesterday’s low could trigger a renewed decline towards 1.0300–1.0240.

Key events that could influence EUR/USD pricing:

- Today at 12:00 (GMT+2): Germany GDP

- Today at 16:15 (GMT+2): ECB interest rate decision

- Today at 16:45 (GMT+2): ECB press conference

- Tomorrow at 16:00 (GMT+2): Germany consumer price index (CPI)

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Swiss KOF rises to 101.6, led by manufacturing and services

Switzerland’s KOF Economic Barometer climbed to 101.6 in January, up from 99.6 and surpassing market expectations of 100.5. This data suggests modest pickup in economic momentum, particularly in production-side sectors.

According to KOF, "the majority of the production-side indicator bundles included in the KOF Economic Barometer show positive developments."

The strongest contributions came from manufacturing, financial and insurance services, hospitality, and other service industries, signaling resilience in key sectors of the Swiss economy.

However, the outlook remains uneven. While production indicators strengthened, demand-side indicators showed signs of weakness. KOF noted that both "the indicator bundles for foreign demand as well as for private consumption indicate a downward tendency," highlighting subdued consumer activity and external trade concerns.

BoJ’s Himino reiterates further hike possible if economic forecasts hold

BoJ Deputy Governor Ryozo Himino reinforced expectations that the central bank could raise interest rates further if its economic and price projections are met.

Speaking today, Himino stated, "If our economic and price forecasts are achieved, we will raise our policy rate accordingly and adjust the degree of monetary support."

Himino also highlighted concerns about Japan’s prolonged period of negative real interest rates, describing the situation as "not normal."

He explained that an ideal economic scenario for Japan would involve rising wages and corporate profits, fueling stronger consumption and investment, which would then support moderate and stable inflation. In such a case, Japan could see real interest rates turn positive.

Fed Policy Meeting a Non-Event

Markets

Yesterday’s Fed policy meeting was a non-event. The US central bank kept rates steady at 4.25-4.5% and suggested they would remain there for some time. A hawkist twist in the statement that left out the part saying inflation has made progress was dismissed by chair Powell as being part of a “cleaning-up exercise”. He nonetheless noted the Fed wants to see “serial [CPI] readings” that suggested things were headed in the right way. Add “We need to let those [Trump’s] policies be articulated before we can even begin to make a plausible assessment of what their implications for the economy will be” and you sense the central bank just installed a long pause that could last through June. US markets reacted accordingly. The small spike shortly after the updated statement was released, evaporated quickly, leading to marginal net daily changes varying between +1.9 (2-yr) to -0.6 bps (30-yr). Bunds slightly underperformed (+2.4 bps in the 30-yr). The dollar held a minor upper hand against most global peers. Sterling appreciated towards EUR/GBP 0.837 as UK Chancellor Reeves sought to convince investors of her growth-reviving plans in her first high-profile appearance yesterday since delivering the October budget. The Japanese yen outperformed yesterday and does so again this morning. USD/JPY eases to 154.5.

US Q4 GDP figures today should comfort the Fed in taking a long breather and keep both US yields and the dollar at least steady. Economic activity is seen to have expanded at a solid 2.6% q/q annualized pace following Q3’s 3.1%. Private consumption remains the key engine. Q4 PCE price deflators may have picked up to 2.5%. Euro area GDP growth contrasts with a meagre 0.1% q/q. France’s numbers released this morning suggest, if any, minor downside risks. From a market point of view, though, a lot of pessimism has been priced in already. Attention is likely to shift to the ECB meeting pretty quickly. Another 25 bps rate cut to 2.75% is all but certain. But the path forward is getting less and less predictable with the central bank nearing (the upper bound of) the neutral rate. President Lagarde will face but will probably walk around any related questions. Last week’s PMI’s in any case offered light at the end of the tunnel for the economy while flagging rising price pressures. We assume one more cut in March to 2.5% before the debate opens up and paves the way for a pause in the cycle. Since this is the market’s base case too, risks for the euro (and yields) are for Lagarde to keep the door ajar for cuts in April and June as well.

News & Views

The Brazilian central bank (BCB) raised its policy rate as flagged by new governor Galipolo by 100 bps to 13.25% and sticks to its commitment to implement another 100 bps rate hike at the next, March 19, policy meeting which will take the key Selic rate above its previous peak level of 13.75% (Aug 2022 – July 2023). Beyond the next meeting, the BCB reinforces that the total magnitude of the tightening cycle will be determined by the firm commitment of reaching the inflation target and will depend on inflation dynamics, on the output gap, and on the balance of risks. Domestic economic activity and the labour market remain strong while inflation remains above the 3% target and is rising again. A significant increase in inflation expectations adds to upside inflation risks together with resilient services inflation and a persistently more depreciated currency both because of internal (fiscal) policy and the external environment (Fed: higher for longer). Inflation forecasts show headline inflation declining from 5.2% Y/Y to 4% Y/Y by Q3 2026 (current policy horizon), assuming a 15% peak policy rate through year-end.

The Bank of Canada (BoC) reduced its policy rate by 25 bps to 3% yesterday. The central bank acknowledged that the cumulative reduction in the policy rate since last June is substantial (200 bps). Lower interest rates are boosting household spending and the economy is expected to strengthen gradually (from 1.4% in 2024 to 1.8% in 2025 & 2026) and inflation to stay close to the 2% target. Risks around the outlook are reasonably balanced. Dovish twists include the labelling of the labour market as being “soft” and the warning that if broad-based and significant tariffs were imposed by the US, the resilience of Canada’s economy would be tested. Canadian money markets are split on the outcome of the next, March 12, policy meeting. All else equal we’re inclined to think of a pause awaiting new updates at the April meeting. The BoC yesterday also announced its plan to end quantitative tightening. The Bank will restart asset purchases (regular term repo programme followed by treasury bill purchases) in early March, beginning gradually so that its balance sheet stabilizes and then grows modestly, in line with growth in the economy. The Canadian dollar remains weak at USD/CAD 1.4430 (1.45-1.47 resistance).

ECB Takes the Stage After Trio Yesterday

In focus today

At the ECB meeting today at 14:15 CET, another 25bp cut bringing the policy rate to 2.75% is unanimously expected among analysts and markets. Markets anticipate 100bp in rate cuts this year. While we expect the ECB to cut further, we see the risk of a repeat hawkish market reaction in December if Lagarde does not commit to the end point of this cutting cycle.

Multiple euro area prints are on the agenda today including the first estimate of euro area GDP for Q4 2024, which we expect to show continued weak growth at 0.1% q/q. Previously released data indicated that Spain remained the primary growth driver with GDP rising 0.8% q/q. Ahead of the euro area, we receive Q4 GDP figures from France and Germany, where we anticipate a slightly negative growth rate. Additionally, the euro area unemployment rate for December will be released. With survey indicators suggesting a softening of the labour market in recent months, not yet visible in the hard data, it will be interesting to see the print. Focus will also be on Spanish inflation for January.

In the US, we expect Q4 Flash GDP growth to land at 2.4% q/q AR, indicating a modest slowdown from the 3.1% pace in Q3. Solid private consumption continues to be the most important driver of growth, although we do pencil in some moderation towards 2025.

In Sweden, we will receive additional data to assess where we stand with regards to the widely expected consumption-driven recovery. At 08.00 CET, retail sales data for December will be out, followed by NIER's confidence indicators at 09:00 CET. The NIER survey will highlight consumer confidence, which has been rising since late 2022 but dipped in December. Corporate sector sentiment and pricing plans will also be examined.

Economic and market news

What happened yesterday

In the US, the Fed kept rates unchanged at 4.25-4.50% as expected. Powell delivered a balanced message avoiding speculation on future trade and fiscal policy effects. He noted the committee's general lack of urgency to adjust policy, but he did not rule out a cut in March. We make no changes to our call for the next cut in March and for quarterly reductions thereafter until the policy rate target reaches 3.00-3.25%. See more in Fed review: As balanced as it gets, 29 January.

In Sweden, the Riksbank cut the policy rate as expected by 25bp to 2.25%, motivated in the press release as "the risk of inflation becoming too high is limited, at the same time as economic activity is weak". In combination with the wording that the Riksbank "is prepared to act if the outlook for inflation and economic activity changes", our interpretation is that the Riksbank keeps the door open to further cuts, and we maintain our view that the Riksbank will cut once more to 2.00% in May. Especially as our inflation forecast is lower than the Riksbank's. See more in Flash Comment: Riksbank January 2025, 29 January. The Swedish GDP indicator for Q4 showed an increase of 0.2% q/q s.a. close to consensus and our expectations of 0.3% q/q. Important to note, that this print belongs in the unofficial, experimental set of SCB data, which has understated actual GDP growth, so it should be taken with a pinch of salt.

In the euro area, the European Commission presented the "Competitiveness Compass", which outlines policy priorities for the next five years aimed at enhancing the European economy's competitiveness. This will be achieved through reforms that promote investment by increasing innovation, risk capital, and reduced regulation. Concrete reforms, based on the Draghi report's recommendations, will be introduced over the next two years. If implemented, these reforms could enhance European and Danish productivity. However, their long-term impact remains uncertain due to the need for approvals and growing scepticism in the European Parliament about increased EU centralisation and integration.

In Spain, the strong GDP growth continued into Q4 rising 0.8% q/q (cons: 0.6%, prior: 0.8%). The Spanish economy has been a clear bright spot of the euro area with GDP rising 3.2% y/y in 2024. This growth has been boosted by strong service activity, relatively lower energy prices, and a large rise in employment.

In Canada, BoC cut policy rate by 25bp bringing it to 3.0% as widely expected. Emphasis was especially on the threat of US tariffs as a major source of uncertainty, though the BoC stressed that its projections do not incorporate these new tariffs threatened by the US.

Equities: Global equities declined yesterday, once again dragged down by the US while Europe was higher. Year to date, European equities are up by 6%, while their US counterparts have increased by only 3%. Yesterday was not influenced by a single factor and the DeepSeek impact faded as anticipated. The combination of monetary policy and earnings dominated the market, with monetary policy aligning closely with expectations, while earnings were strong not only in Europe but also in the US. Most positive earnings news in the US emerged after the close of cash trading, which should positively impact cash trading today. In the US yesterday, the Dow fell by 0.3%, the S&P 500 by 0.5%, the Nasdaq by 0.5%, and the Russell 2000 by 0.3%. Many Asian markets are closed for the Lunar New Year. However, those open for trading are mostly higher. Futures in Europe are mixed this morning, while US futures are higher, led by the Nasdaq.

FI: Yesterday's wait-and-see mode ahead of the FOMC in the evening led to European yields trading in a very tight range. In the afternoon, a surge in natural gas prices due to unplanned supply restrictions sent yields slightly higher though. 10y Bunds ended the day at 2.58%. All three central bank decisions were widely anticipated: Riksbank and the BoC cut by 25bp while the Fed was on hold. That said, BoC also announced its plan to end QT to complete the normalisation of its balance sheet. Starting in early March, BoC will gradually restart its asset purchases to stabilise its balance sheet. At the same time, effective 30 January, the BoC will set the deposit rate at a spread of 5bp below the policy rate. Together with the plan to halt QT, these measures aim to support the functioning of liquidity markets and mitigate upward pressure on the overnight repo rate.

FX: EUR/USD remained largely unchanged following the widely anticipated Fed hold, hovering above 1.04. We continue to see potential for a near-term topside to EUR/USD. CAD remained unfazed as the BoC delivered a widely expected 25bp rate cut, bringing its policy rate to 3.00%. We maintain our near-term bias for a move lower in USD/CAD. Yesterday, the Riksbank cut the policy rate as expected by 25bp to 2.25%. EUR/SEK initially dipped lower, but the cross ended the day close to unchanged. GBP FX has been in for a strong week with Chancellor Reeves speech yesterday not spurring renewed fiscal policy concerns.

AI Race Heats Up

Three of the Magnificent 7 companies – and ASML – released their Q4 earnings yesterday and the numbers were ... mixed. First, ASML announced better-than-expected results and more importantly a strong order book confirming a continued strength in AI business for the coming months. The share price gained more than 5.5% in Europe and regained the levels pre the DeepSeek selloff.

The announcements were less outright great from the three others’. Microsoft reported a significant boost in its AI segment, with an annual revenue increase of 175% year-over-year. However, the growth rate in Azure and other cloud services was 31%, slightly below 31.8% expected by analysts. Note that the company faces challenges in meeting the rising AI demand due to data center capacity constraints – the reason why they plan to invest around $80bn in AI this year. But investors were not enchanted by the cocktail of high spending and slowing growth, and sent the stock price more than 4.50% in the afterhours trading.

Meta exceeded both revenue and earnings expectations, but its current quarter forecast disappointed. More importantly, the company doubled down on its planned $60-65bn AI investment this year – defying the DeepSeek-triggered skepticism about AI costs – and Zuckerberg said that 2025 will make Meta’s AI accessible to over a billion users. There you go – you can’t have such ambitions and buy less than Nvidia’s most premium chips. The stock price first fell on disappointing current-quarter forecast then rebounded more than 2% in the afterhours. If Meta pulls off this AI story successfully, they have an incredible potential to grow as they have so much data in their hand! Meta's AI ambitions are as convincing as its metaverse bet was unconvincing.

And oh, Alibaba stepped out of the darkness saying that it’s AI model is the greatest of the world and is performing better than Meta and DeepSeek. A giant like Alibaba should be taken as a bigger threat than DeepSeek as the company can back it up with real-world applications and wide adoption. Enthusiasm from investors remains surprisingly underwhelming. Alibaba is a solid candidate for Chinese AI bets.

Overall, the AI race is intensifying, with strong demand and limitless potential. While competition might drive prices down, the sector is definitely on track for another impressive year of growth.

Last but not least: Tesla missed both earnings and revenue expectations last quarter, but... the company said that it will launch the robotaxi and pilot production of the Optimus as early as this year. Musk said that ‘Teslas will be in the wild with no one in them in Austin in June’. It was a rollercoaster ride in the afterhours trading. The stock price first fell nearly 4%, then rebounded to print a more than 4% jump. I should all admit that Musk is impressive encouraging price rallies with lower-than-expected results. But be careful, his implication in politics is a risk.

Apple is due to report earnings today.

Keeping up with the central banks

Zooming out, the US equity markets were down yesterday, but the futures are up this morning. The Federal Reserve’s (Fed) decision went according to the plan. Fed members decided to maintain the rates where they are but there was some confusion about the inflation outlook. The statement cited that inflation remains ‘somehow elevated’ bit removed a reference regarding the progress toward the 2% goal. The latter immediately got investors’ attention as a significant hawkish shift and sent stock prices lower. But then, Powell said that the language tweak was only to shorten the sentence and wasn’t meant to send a signal. So the Fed removed a big chunk of the most important information to markets from a sentence to shorten the sentence (?!) and investors partially bought into the rectification...

Overall, the fact that ‘inflation remains elevated’ and the fact that it does not necessarily trend toward the 2% target, combined with the healthy US jobs market and robust growth/earnings, topped with Trump’s tariff threats led to an unsurprisingly hawkish Fed announcement. The probability of a no cut in May rose to around 55%. And the first rate cut from the Fed is now expected for June – the earliest. But the data could change that.

Beyond the borders, the Bank of Canada (BoC) cut its rate by 25bp BUT refrained from giving any guidance due to Trump uncertainties. The USDCAD remains under the pressure of Trump risks to the Canadian growth that could need the BoC’s help to navigate the agitated waters, and the European Central Bank (ECB) will certainly announce a 25bp cut today, and repeat that if the data allows, there will be further support. The EURUSD is under pressure and is inclined to extend losses.