Sample Category Title

Euro Trading Higher In The Morning Session

For the 24 hours to 23:00 GMT, the EUR declined 0.42% against the USD and closed at 1.1607 on Friday.

The US Dollar recovered from its initial losses against its major peers, following better than expected data on the US ISM non-manufacturing PMI.

The ISM non-manufacturing PMI unexpectedly rose to 60.1, against market expectations of a fall to a level of 58.5. In the prior month, the non-manufacturing PMI had registered a level of 59.8. However, the final Markit services PMI remained flat at 55.3 in October from last month, against market expectations of an advance to a level of 55.9. The preliminary figures had indicated an advance to 55.9.

US jobs market report showed a mixed picture about the economy. US non-farm payrolls advanced by 261.0K in October, compared to a revised advance of 18.0K in the prior month. Market expectation was for non-farm payrolls to increase by 313.0K. Meanwhile, the nation’s unemployment rate unexpectedly declined to 4.1% in the last month, from a rate of 4.2% in the previous month. Additionally, US average hourly earnings rose 2.4% YoY in October, missing market expectations for an advance of 2.7%. In the last month, average hourly earnings had climbed by a revised 2.8%.

Separately, US trade deficit expanded to $43.5 billion in September, compared to a revised trade deficit of $42.8 billion in the previous month. Market expectation was for the nation to register a trade deficit of $43.2 billion. Moreover, the final durable goods orders rose 2.0% in September, at par with market expectations. Durable goods orders had registered a similar rise in the prior month. Meanwhile, US factory orders registered a rise of 1.4% on a monthly basis in September, compared to a rise of 1.2% in the prior month. Markets were also expecting factory orders to advance 1.2%.

In the Asian session, at GMT0400, the pair is trading at 1.1614, with the EUR trading 0.06% higher from Friday’s close.

The pair is expected to find support at 1.1577, and a fall through could take it to the next support level of 1.1541. The pair is expected to find its first resistance at 1.167, and a rise through could take it to the next resistance level of 1.1727.

Moving ahead, Eurozone’s services PMI for October along with the Sentix investor confidence index for the region in November, both due to release today, would grab significant market attention. Also, Germany’s factory orders for September and services PMI data for October, scheduled today, would be closely assessed by investors. In the US, Fed Chairwoman, Janet Yellen’s speech, due later in the day, would be eyed by traders.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

UK’s Services Sector Expanded At Its Fastest Rate In Six Months In October

For the 24 hours to 23:00 GMT, the GBP rose 0.16% against the USD and closed at 1.3074 on Friday, following robust UK Markit services PMI data.

Data showed that Britain's services sector unexpectedly rose to 55.6 in October, compared to a reading of 53.6 reported in the previous month. Markets were expecting the index to fall to a level of 53.3. The growth in UK's dominant sector was led by an advance in order books and strong client demand.

In the Asian session, at GMT0400, the pair is trading at 1.3077, with the GBP trading marginally higher from Friday's close.

The pair is expected to find support at 1.3034, and a fall through could take it to the next support level of 1.2991. The pair is expected to find its first resistance at 1.3126, and a rise through could take it to the next resistance level of 1.3175.

Amid a lack of major economic releases in the UK today, trading trends in the currency pair would be determined by global economic factors.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

BoJ Governor Remains Confident About Japan’s Economy And Inflation Outlook

For the 24 hours to 23:00 GMT, the USD rose 0.06% against the JPY and closed at 114.12 on Friday.

Minutes of the Bank of Japan's (BoJ) September policy meeting, which were released overnight, revealed that Japan's economy continued to proceed at an acceptable pace. However, the policy members cited downside risks to growth amid uncertainty in US economic policies and Brexit outcome. Also, most of the board members believed that the BoJ's current policy was adequate to achieve 2.0% inflation in the long term.

In other news, Japan's services PMI climbed to more than two-year high of 53.4 in October due to a sharp increase in new orders, from a reading of 51.0 recorded in the previous month.

In the Asian session, at GMT0400, the pair is trading at 114.34, with the USD trading 0.19% higher from Friday's close.

Earlier this morning, the BoJ Governor, Haruhiko Kuroda, expressed his confidence in Japan's economy by stating that the nation's economic growth is gathering momentum and there is a growing possibility of inflation hitting the 2.0% target, thus strengthening expectations that no additional stimulus is forthcoming.

He also stated that there is no need to alter the pace of its ETF purchases under its stimulus programme for the time being.

The pair is expected to find support at 113.74, and a fall through could take it to the next support level of 113.15. The pair is expected to find its first resistance at 114.83, and a rise through could take it to the next resistance level of 115.33.

With no additional economic release in Japan today, traders will look forward to global macroeconomic data for further direction.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Swiss Franc Trading Slightly Higher, Ahead Of Consumer Price Index Data

For the 24 hours to 23:00 GMT, the USD rose 0.13% against the CHF and closed at 1.0008 on Friday.

In the Asian session, at GMT0400, the pair is trading at 1.0005, with the USD trading marginally lower from Friday’s close.

The pair is expected to find support at 0.9962, and a fall through could take it to the next support level of 0.992. The pair is expected to find its first resistance at 1.0036, and a rise through could take it to the next resistance level of 1.0068.

Investors will now look forward to Switzerland’s inflation figures for October, set to release in a few hours, for further cues.

The currency pair is trading between its 20 Hr and 50 Hr moving averages.

Canada’s Trade Deficit Remained Steady, Unemployment Rate Surprisingly Rose

For the 24 hours to 23:00 GMT, the USD declined 0.36% against the CAD and closed at 1.2766 on Friday.

Macroeconomic data showed that Canada reported international merchandise trade deficit of C$3.18 billion in September, from a revised international merchandise trade deficit of C$3.18 billion in the prior month. Market had anticipated the nation to report a trade deficit of C$3.0 billion. Meanwhile, the unemployment rate in Canada unexpectedly rose to 6.3% in October, compared to market expectations of an unchanged reading. In the prior month, the unemployment rate stood at 6.2%.

In the Asian session, at GMT0400, the pair is trading at 1.2768, with the USD trading a tad higher from Friday's close.

The pair is expected to find support at 1.271, and a fall through could take it to the next support level of 1.2652. The pair is expected to find its first resistance at 1.2831, and a rise through could take it to the next resistance level of 1.2894.

Later in the day, traders will await the release of Canada's Ivey PMI data for October.

The currency pair is trading below its 20 Hr and 50 Hr moving averages.

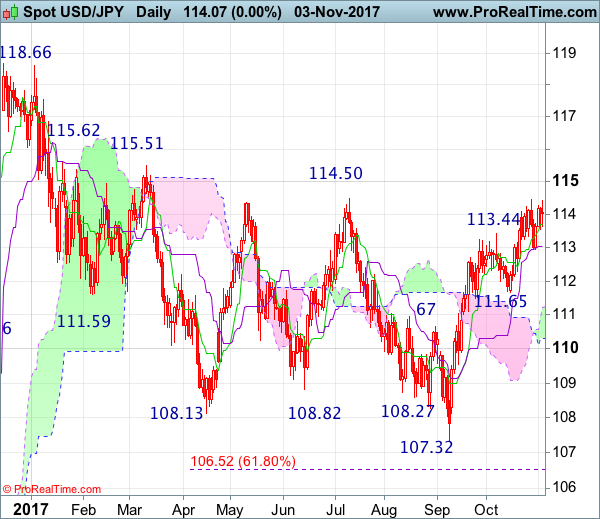

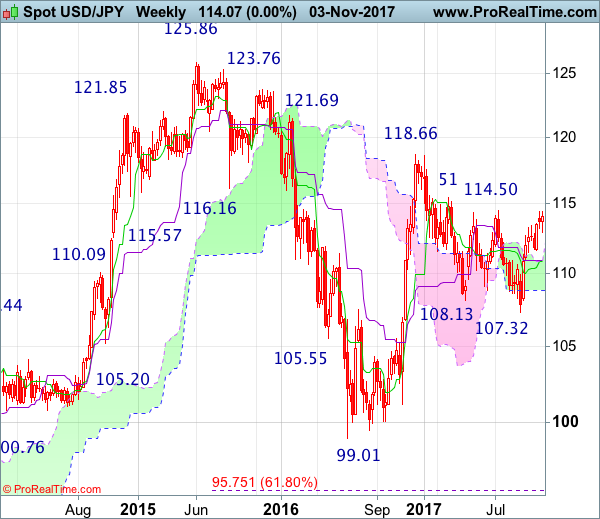

USD/JPY Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Dark cloud cover

• Time of formation: 10 Jul 2017

• Trend bias: Down

Daily

• Last Candlesticks pattern: Evening doji

• Time of formation: 7 Aug 2017

• Trend bias: Down

USD/JPY – 114.32

Dollar’s breach of previous resistance at 114.45-50 adds credence to the view that the fall from 118.66 has ended and upside bias remains for the rise from 107.32 to extend further gain to 115.00, then towards previous resistance at 115.51-62, however, loss of momentum should prevent sharp move beyond 116.00-10 and reckon 116.50-60 would hold from here, risk from there is seen for another retreat later.

On the downside, whilst initial pullback to 113.60-65 is likely, reckon the Kijun-Sen (now at 113.20) would contain downside and bring another rise later to aforesaid upside targets. Below support at 112.96 would defer and suggest a temporary top is formed instead, risk correction to 112.30 but still reckon downside would be limited to 112.00 and previous support at 111.65 should remain intact, bring rebound later.

Recommendation : Buy at 113.40 for 115.40 with stop below 112.40.

On the weekly chart, as the single currency has risen again after finding renewed buying interest at 112.96 last week and broke above indicated previous resistance at 114.45-50, suggesting the rise from 107.32 is still in progress, this also signal early erratic decline from 118.66 has ended at 107.32, hence consolidation with upside bias remains for further gain to 115.51-62 resistance, break there would extend gain towards 116.50-60 first, having said that, near term overbought condition should limit upside to 117.00-10, risk from there is seen for another retreat later.

On the downside, expect pullback to be limited to 113.40-50 and said support at 112.96 should remain intact, bring another rise later. A drop below 112.96 support would defer and suggest a temporary top is possibly formed instead, bring pullback to 112.30, then 112.00, however, previous support at 111.65 should hold. Only a break below this level would signal the rise from 107.32 low has ended, bring deeper correction to the Kijun-Sen (now at 111.03) which is likely to hold from here.

Market Update – Asian Session: BOJ Gov Kuroda Affirms Easing Stance, Weakens Yen

Asia Summary

Asian equity markets opened the session mixed. The Nikkei 225 resumed trade slightly higher, following Friday's holiday.

However, Japanese tech name, Furukawa Electric, has traded lower by over 16%, following disappointing earnings.

Softbank has declined by over 2%, amid reports that T-Mobile and Sprint would end their merger talks. Following this news, Softbank also announced that it was planning to raise its stake in Sprint to less than 85%. The Japanese company owned an ~83% stake as of June 5th, according to Sprint's proxy statement.

In other tech M&A news, it was reported on Friday that Broadcom was said to consider an ~$103B cash and stock bid for Qualcomm.

Nasdaq Futures are currently lower by over -0.1%. Supplier Foxconn is said to have been asked by Apple to accelerate its production of the iPhone X amid strong sales, said a Taiwanese press report. Samsung and Hynix have declined by over 0.4%, in South Korea.

SK Telecom has declined by over 2%, as Q3 operating profits missed expectations.

South Korean consumer discretionary companies, including Lotte Shopping, are gaining amid speculation that China tourist numbers may rise in 2018. Fast Retailing has gained over 1.5%, as the company reported a 8.9% rise in its Oct domestic SSS. Cathay Pacific has declined over 3%, as Qatar Airways will acquire a 9.6% stake in the company from Kingboard Chemical.

Air China, which owns an over 29.9% stake in Cathay, has declined by over 2%. The overall Hang Seng China Enterprise index has declined by over 1% on the session amid weakness in the property sector. Real estate sales firm Sunac China has dropped over 6%.

Financials in China have also declined, as China's 10-year bond yield has declined on the session. HNA Holdings Group has declined over 3%. On Friday's session, China's NDRC (state planner) announced that it had issued draft guidelines on overseas investment by Chinese companies.

Australia's Westpac has traded lower by over 2%, as FY earnings missed market expectations. Shares of DBS in Singapore are lower by over 0.5%. The company's Q3 profit missed market expectations, amid a rise in the allowance for credit losses related to the oil/gas sector. Japanese mega banks are trading lower, as Mitsubishi UFJ and Mizuho have declined by over 0.5%. Both companies are due to report earnings on Monday, November 13th.

In the auto sector, Honda, which reported its earnings last week (Nov 1st) has gained over 1.5%. Shares of Toyota, which is due to report results on Tuesday, are higher by over 0.3%. Isuzu Motor has gained over 2% amid speculation that H1 operating profits may rise by 7%. Meanwhile, Mazda has declined by more than 3% as its quarterly earnings missed expectations. Subaru has dropped over 2%, after cutting its FY forecast.

Japan steelmakers are trading generally lower. Nippon Steel has declined by over 1.5%. Kobe Steel, which gained over 10% last week, is lower by over 2%. There has been speculation on today's session that certain executives at the steel company could seek to resign amid the recent data falsification issue.

Australian commercial blasting systems manufacturing Orica has declined by over 8% after reporting a drop in FY profits.

Energy companies in Australia are trading generally higher. Santos has gained over 2%, while shares of Woodside Petroleum are up over 1.5%. Brent Crude prices have risen on the session to trade at highs not seen since July 2015.

Over the weekend, it was reported that Saudi Arabia's Crown Prince ordered the arrest of individuals including members of the royal family, ministers and investors. On Sunday, it was also reported that a Saudi-led coalition intercepted a ballistic missile that was fired towards Saudi Arabia. The Saudi coalition has called the incident a 'direct Iran military aggression' and said it would temporarily close all Yemeni crossings.

USD/JPY has risen by over 0.4% to trade at highs not seen since March. Speaking from Japan, US President Trump, who has started his 12-day trip to Asia, said currently trade with Japan is not fair as he noted the US' trade deficit with Japan. Bank of Japan (BoJ) Gov Kuroda reiterated that the central bank will continue with its ‘powerful easing' and it is crucial that people actually experience inflation above 2%.

US Long Bond Futures are lower by over 0.1%. NY Fed President Dudley (FOMC voter) is expected to retire before his term expires in Jan 2019, according to a US financial press report.

Looking ahead, the Reserve Bank of Australia (RBA) is expected to hold its monetary policy meeting on Tuesday's session. Wednesday is the tentative release date for China's Oct Trade Balance. The Reserve Bank of New Zealand (RBNZ) is due to meet on Thursday's session, while's the RBA's Quarterly

Monetary Policy Statement and economic forecasts are due to be released on Friday.

Key economic data

(JP) Japan Oct PMI Composite: 53.4 v 51.7 prior (5-month high); Services:53.4 v 51.0 prior (26-month high)

(NZ) NEW ZEALAND Q4 2-YR INFLATION EXPECTATION: 2.0% V 3.2%E

(NZ) New Zealand Oct ANZ Commodity Price m/m: -0.3% v 0.8% prior

(JP) Bank of Japan (BOJ) Sept 20-21st Policy Meeting Minutes: momentum towards price goal is being maintained

Speakers and Press

Japan

(JP) Bank of Japan (BOJ) Gov Kuroda: Reiterates BOJ will continue with powerful easing; Price moves weak compared with improvement in the economy

Korea

(KR) South Korea, US and Australia to conduct joint naval drills near Jeju

Australia

(AU) Fitch: Australia major banks will face earnings pressure in FY18

China/Hong Kong

(CN) PBOC Gov Zhou: The market should play a "decisive role" in allocating financial resources, but also needs to be stronger regulation and Communist Party leadership in guiding financial reform - Chinese press

(CN) Moody's Report: Property developers in China face record bond maturities in 2018

Outside Asia

(JP) During President Trump's visit to the country, Japan to tell US it will strengthen sanctions against North Korea - Japanese Press

(US) NY Fed President Dudley (FOMC voter) to retire before term expires in Jan 2019; could leave as soon as the Spring of 2018 – financial press

(SA) Saudi-coalition calls weekend missile incident a 'direct Iran military aggression'; to temporarily close all Yemeni crossings

(SA) Saudi Arabia's Crown Prince ordered the arrest of individuals including members of the royal family, ministers and investors – financial press

Asian Equity Indices/Futures (23:00ET)

Nikkei -0.0%, Hang Seng -1.0%; Shanghai Composite -0.1%; ASX200 -0.1%, Kospi -0.8%

Equity Futures: S&P500 -0.2%; Nasdaq100 -0.2%, Dax -0.1%; FTSE100 -0.2%

FX ranges/Commodities/Fixed Income (23:00ET)

EUR 1.624-1.1596; JPY 114.74-113.96; AUD 0.7659-0.7638;NZD 0.6914-0.6887

Dec Gold +0.1% at $1,269/oz; Dec Crude Oil +0.2% at $55.76/brl; Dec Copper +0.8% at $3.14/lb

(AU) Australia buys back A$400M in Oct 2018, 2019 bonds

(AU) Australia sells A$400M in 2037 bonds; avg yield 3.0580%; bid-to-cover 2.54x

(CN) PBoC OMO: Skips OMO v skipped prior (3rd consecutive skip); Net drains CNY160B

USD/CNY *(CN) PBOC SETS YUAN REFERENCE RATE AT 6.6247 V 6.6072 PRIOR

(KR) Bank of Korea (BoK) sells KRW270B in 6-month monetary stabilization bonds at 1.55% v 1.59% prior

Equities notable movers

Australia/New Zealand

WBC.AU Reports FY17 (A$) Cash Earnings A$8.06B, +3% y/y; Net A$7.99B v A$7.45B y/y; Rev A$21.8B, +3.9% y/y; -2.4%

ORI.AU Reports FY17 (A$) Net profit 386.2M, -0.7% y/y; EBIT A$635M, -1% y/y; Rev 5.04B, -1% y/y; -8.1%

MEA.AU Guides FY18 EBITDA not likely to reach A$16.6M (below expectations); initial plan is to cut expenses by A$5M/year; -14%

Japan

2371.JP Reports H1 Net profit ¥7.14B v ¥6.98B y/y, Op profit ¥10.5B v ¥10.1B y/y, Rev ¥21.7B v ¥20.8B y/y; +7.6%

5801.JP Reports H1 Net ¥21.7B v ¥6.7B y/y, Op ¥21.8B v ¥13.3B y/y; Rev ¥457.5B v ¥397.6B y/y; -16.5%

US

S Announces strategic MVNO agreement with Altice USA; financial terms not disclosed

TMUS T-Mobile and Sprint End Merger Discussions

S Softbank announces its intention to raise stake through open market transactions or otherwise, subject to market conditions and other factors

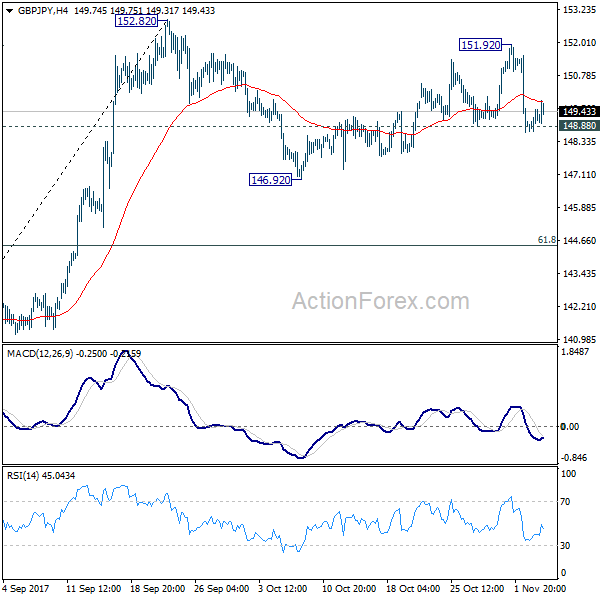

GBP/JPY Daily Outlook

Daily Pivots: (S1) 148.68; (P) 149.10; (R1) 149.52; More

Intraday bias GBP/JPY remains mildly on the downside for the moment. As noted before, corrective recovery from 146.92 has completed at 151.92. Further fall should be seen to 146.92. Break will resume the decline from 152.82. At this point, we'd expect strong support from 61.8% retracement of 139.29 to 152.82 at 144.45 to contain downside and bring rebound. On the upside, above 151.92 will retest 152.82 high instead.

In the bigger picture, medium term rebound from 122.36 is still expected to resume after corrective pull back from 152.82 completes. Firm break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. However, break of 139.29 will indicate rejection from 150.43 key fibonacci level. And the three wave corrective structure of rebound from 122.36 will argue that larger down trend is resuming for a new low below 122.26.

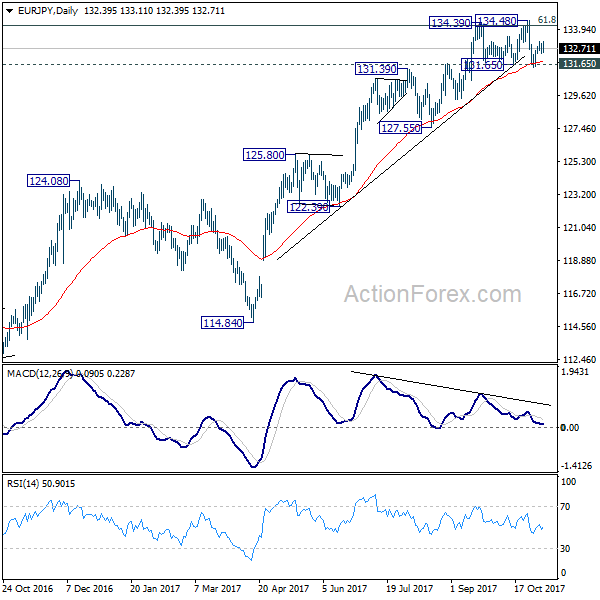

EUR/JPY Daily Outlook

Daily Pivots: (S1) 132.19; (P) 132.60; (R1) 132.80; More....

Intraday bias in EUR/JPY remains neutral for the moment. As noted before, decisive break of 134.39/48 resistance zone is needed to confirm up trend resumption. Otherwise, even in case of rebound, near term outlook is neutral at best. On the downside, decisive break of 131.65 will confirm rejection from 134.20 fibonacci level and confirm near term reversal. And, in such case, intraday bias will be turned to the downside for 127.55 key support level.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). 61.8% retracement of 149.76 to 109.03 at 134.20 is already met. Sustained break there will pave the way to key long term resistance zone at 141.04/149.76. However, break of 127.55 support will argue that the medium term trend has reversed and will turn outlook bearish for deeper fall back to 114.84/124.08 support zone at least.

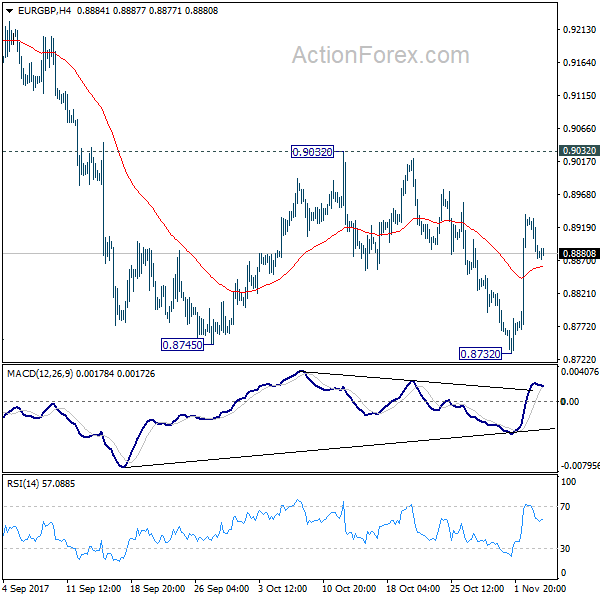

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8854; (P) 0.8894; (R1) 0.8915; More...

At this point, intraday bias in EUR/GBP remains neutral first. On the upside, decisive break of 0.9032 will confirm completion of the decline from 0.9305. In such case, intraday bias will be turned back to the upside for retesting 0.9305 key resistance. On the on the downside, break of 0.8732 will resume the fall and target 0.8303 key support level instead.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.