Sample Category Title

GBPUSD Intraday Analysis

GBPUSD (1.3097): The British pound broke past the support level at 1.3236 as price continued to push lower. Even the minor support level at 1.3161 was also breached. This signals a continued downside momentum. GBPUSD will be seen testing the lower support at 1.2980 region. Any short term retracements are likely to be limited to the recently breached support level at 1.3236. Establishing resistance here could confirm the downside in the GBPUSD.

EURUSD Intraday Analysis

EURUSD (1.1702): The common currency weakened yesterday as price action was seen giving up the gains from the previous days. Support at 1.1688 is relatively close and could be tested in the short term. EURUSD continues to consolidate inside the descending wedge pattern as long as price remains supported above or close to 1.1688. A breakdown below this support could signal further declines invalidating the potential bullish outlook. To the upside, a breakout could result in EURUSD testing the resistance level at 1.1822 where resistance is most likely to be formed.

Dollar Gains Momentum On Trade Deficit And Tax Reform Progress. NFP In Focus

The U.S. dollar managed to maintain its bullish momentum on Thursday after economic data released showed that the trade deficit narrowed to $42.2 billion in the month of August. This marked the lowest levels since a year. Orders for capital goods excluding non-defense rose 1.1% in August beating estimates of 0.9%. The U.S. House of Representatives approved the fiscal 2018 budget draft which is expected to pave way for the government to go ahead with the tax reforms.

Elsewhere, the ECB's meeting minutes revealed that the central bank is on path to tapering QE but that it could happen at a gradual pace.

Looking ahead, the September payrolls report will be released today. According to the estimates, the U.S. economy is expected to add 82k jobs for the month of September which is below the average trend. On the upside, wages are expected to grow 0.3% on the month while the unemployment rate is expected to remain steady at 4.4%. Canada will also be releasing its jobs report today and the Canadian unemployment rate is expected to tick higher to 6.3% from 6.2% in the previous month.

Forex: Data Reflects A Strong US Labour Market – Eyes Turn To NFP

On Thursday, the US Department of Labour released Initial Jobless Claims for the week ending September 29th. Surprisingly, the number Americans filing for unemployment benefits fell more than expected to 260K. The market forecast was for 265K from the previous release of 272K. The figures do not, however, factor in the impacts of the recent Hurricanes – which has impacted labour market data collection.

Also on Thursday, the Bureau of Economic Analysis and the U.S. Census Bureau, released Trade Balance data for August. The US trade deficit narrowed to $-42.4B from the previous reading $-43.6B. The narrowing of the deficit underscores the current strength in the US economy. August exports of services & goods rose to a 30-month high, with core capital goods being stronger than previously reported.

Sterling came under downward pressure on Thursday, following Prime Minister Theresa Mays’ keynote address at her Party’s Political Conference that was seen by many as a disaster. A coughing bout, a prankster, signage falling off the stage and her somewhat nervous demeanor has led to many of her own party suggesting her time as Leader is up. According to a National UK Newspaper, there are over 30 Conservative Lawmakers who are prepared to sign a letter calling for her resignation. Whilst Theresa May is obviously “wounded”, it is highly unlikely that she will resign at a time when the UK needs consistency as they negotiate their divorce from the EU.

EURUSD is trending lower in early Friday trading. Currently, EURUSD is trading around 1.1690.

USDJPY is nearly 0.2% higher to currently trade around 113.00 – Friday’s early high for the pair.

GBPUSD remains under pressure, down 0.3% in early Friday trading. Currently, GBPUSD is trading around 1.3080.

Gold is little changed overnight, currently trading around $1,268.

WTI is down 0.2% overnight to currently trade around $50.90pb.

Major economic data releases for today:

At 13:30 BST, the US Department of Labor will release NFP for September, per market consensus, it is expected to come in at a meagre 88,000 due to the impact of the recent Hurricanes. However, with the knowledge that NFP has been negatively impacted by Harvey and Irma, the markets will have “priced-in” a potentially poor data release. The markets will be also closely watching the Average Hourly Earnings release at the same time. The markets are hoping to see an improvement on the previous readings. The previous release of 0.1% was the lowest increase since March. The consensus is calling for a robust increase in September’s release to 0.3%. With higher average earnings, consumer spending should increase, which will then help create inflationary pressure – helping underscore the Federal Reserve’s plans to hike rates before the end of the year. Closing out the slew of Department of Labour data releases will be US Unemployment. Consensus calls for an unchanged rate of 4.4%.

At 13:30 BST, Statistics Canada will release Canadian Unemployment Rate and Net Change in Employment for September. Net change is expected to be +14.5K and the Unemployment rate is expected to rise from 6.2% to 6.3%.

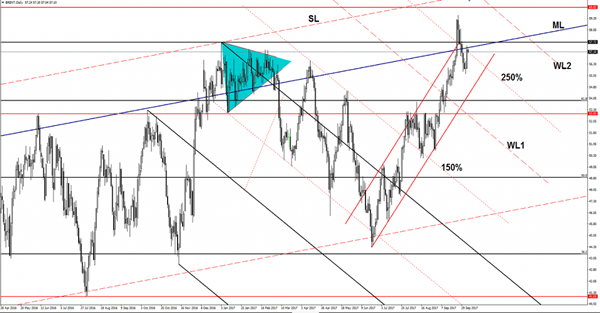

Brent Oil Poised For Further Drop

Brent Oil rallied in the yesterday’s session, but failed to close above the median line (ML) of the major ascending pitchfork. Price is trading in the red right now and tries to stabilize below the 250% Fibonacci line (descending dotted line). I’ve said in the previous days that a retest of the ML followed by a minor drop will confirm a larger drop in the upcoming period. Only a valid breakout above the ML and above the 57.72 will validate an increase at least till will reach the 59.50.

GBP/USD Accelerates The Sell-Off

GBP/USD drops further on the short term and seems too heavy to be stopped. Price has broken through the confluence area formed at the intersection between the 250% Fibonacci line of the ascending pitchfork with the median line (ml) of the descending pitchfork. The pair is almost to hit the 1.3046 static support, where he could find temporary support. The breakdown below the 250% line and below the median line (ml) still needs confirmation. I’ve said in the previous reports that a valid breakdown will conform a larger drop.

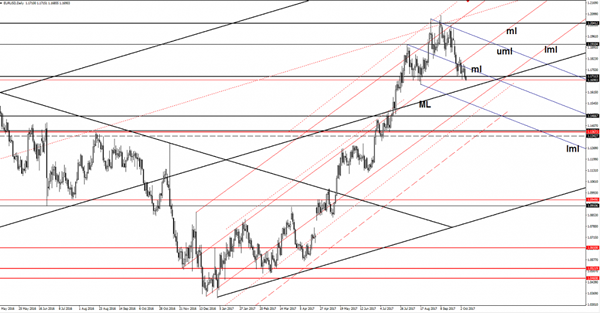

EUR/USD Targeting New Lows

Price dropped and resumed the yesterday's bearish candle. The dollar has taken the lead on the short term again as the dollar index has managed to close much above the 93.81 horizontal resistance. USDX has jumped above the 94.00 psychological level and tries to reach new highs. A further USDX's increase forces the USD to dominate the currency market on the short term.

Personally, I'm still waiting for a retest of the 93.81 broken resistance before will climb much higher. I've said in the last weeks that only a valid breakout above the 93.81 obstacle will announce a larger rebound and a potential reversal. Is premature to talk about a reversal on the dollar index because is still trapped below some important resistance levels.

You should know that the rate will be driven by the fundamental factors in the afternoon, the US is to release the Unemployment Rate, Average Hourly Earnings, and the NFP.

Price drops after the retest of the median line (ml) of the descending pitchfork. EUR/USD has finally managed to close below the 1.1711 horizontal support and now moves towards the median line (ML) of the major ascending pitchfork. Technically, it is expected to drop further and to ignore the ML, but we'll see what impact will have the US data in the afternoon because a disappointment will send the pair higher again on the short term.

Technically, we may still have a Head and Shoulders pattern on the Daily chart, which could confirm a larger drop.

Currencies: Payrolls To Support Further USD Gains?

Sunrise Market Commentary

- Rates: Can payrolls pave the way for full retracement?

The Fed indicated that Q3 eco data might be distorted by the impact from hurricanes. Therefore, we don't expect US Treasuries to strongly profit from disappointing payrolls. If, on the other hand, payrolls are strong, it should pave the way for a full retracement in the US note future towards 124-14+. - Currencies: Payrolls to support further USD gains?

The dollar received support from higher US yields and a new record race of US equities yesterday. Today's US payrolls will probably distorted by the impact of the hurricanes. Still, a decent report might support further USD gains. Rising uncertainty on the political fate of UK PM May kick-started a new down-leg of sterling

The Sunrise Headlines

- The S&P 500 (+0.5%) closed at its sixth consecutive record, its longest streak of highs since 1997. Asian stock markets trade with more or less similar gains this morning with China still closed.

- The second-largest bank based in Catalonia, Banco de Sabadell, has decided to move its legal headquarters out of the region as Catalan separatists and the Spanish authorities hurtle towards a showdown over independence.

- Theresa May faces rebellion among Tories. Grant Shapps, who served as Tory chairman, said he has a list of colleagues who want a new leader and prime minister. The plotters aren't yet numerous enough to push her out.

- Congressional Republicans moved to hasten an overhaul of the US tax code, while Federal Reserve officials warned in rare public remarks that President Trump's tax plan could lead to inflation and unsustainable federal debt.

- The global economy is enjoying its best growth spurt since the start of the decade, IMF Lagarde said, as she urged governments and companies not to “let a good recovery go to waste”.

- The US Senate approved Randal Quarles for a key banking oversight post on the Federal Reserve Board, marking President Donald Trump's first imprint on the central bank and his first full-time appointment of a banking regulator.

- The focus of today's agenda is on the US payrolls report. Average hourly earnings and unemployment rate will also be closely monitored. A number of European and US central bankers is scheduled to speak

Currencies: Payrolls To Support Further USD Gains?

Dollar profits from renewed reflation trade.

Initially, there was again no clear story to guide USD trading, yesterday. There were only second tier eco data in the US and Europe. Tensions on the Spanish markets eased, but it didn't support the euro. Later, the dollar was supported by some ‘hawkish' Fed comments. The US reflation trade also regained momentum with major US stock indices setting new record levels and interest rate differentials slightly widening in favour of the dollar. EUR/USD finished the day at 1.1711 (from 1.1759). USD/JPY closed session at 112.82 (from 112.76)

Overnight, Asian markets profited from positive spill-over effects from WS record race. Even so, the gains in USD/JPY are modest. The pair continues struggling to overcome the 113.00/26 resistance. Uncertainty on the outcome of the Japanese parliamentary elections might play a role. Overall USD strength finally pushed EUR/USD for the test of the recent lows below 1.17. The decline of the Aussie dollar accelerates after RBA-member Harper indicated that the economy isn't out of the woods and as he suggested that an additional rate cut isn't ruled out.

Today, the US September payrolls will be published. The tropical hurricanes likely impacted the payrolls negatively. How much is difficult to say. The consensus stands at a modest 80K net job growth. It compares to a trend growth of about 200K. Also other key metrics of the report like the unemployment rate (expected 4.4%) and the average hours earnings (expected 0.3% M/M and 2.5% Y/Y) might be distorted too.

We see an asymmetrical risk. If payrolls are indeed weak, markets may discard them as unreliable. Better than expected job growth and, maybe even more important, a positive surprise in wage growth will be seen as confirming recent strong US data. It might reinforce the reflation trade, including the rise of the dollar. A weak figure might have only a modest negative impact on the dollar. The central bank parade continues today with Fed governors Dudley, Kaplan and Bullard and ECB governor de Galhau. Uncertainty on Spain/Catalonia remains a wild card for the euro, but currently we don't see a big impact on the single currency.

From a technical point of view EUR/USD hovered in a consolidation pattern between 1.1823 and 1.2070, but broke below last week. There was some hesitation in the USD rebound, but the pair holds below the 1.1823 previous range bottom. Higher US yields are needed to support additional USD gains. Next support in EUR/USD comes in at 1.1662, while 1.1423 marks the 38% retracement from the 2017 rally. EUR/USD is captured in a sell-on-upticks pattern. The USD/JPY momentum was constructive of late, but for an important part due to yen weakness. USD sentiment recently also improved though. USD/JPY regained 110.67/95 (previous resistance), a short-term positive. The 114.49 correction top is the next important resistance. The rally lost momentum this week and underperformance the overall USD rebound. So a break beyond 144.49 probably is not evident.

EUR/USD: nears 1.1662 support. Will the payrolls force the break?

EUR/GBP

Sterling sell-off accelerates

Yesterday, sterling came under more pressure after the failed key note speech of UK PM May. The ‘event' brought additional uncertainty on the political support for PM May and weighed on sterling. The EUR/GBP short-squeeze accelerated as the pair broke the 0.8900/07 resistance area. BoE ‘s McCafferty, as expected, spoke hawkish. He expects economic slack to disappear quickly and saw CPI persistently overshooting the target. His view iss well-know and was ignored. EUR/GBP closed the session at 0.8927. Cable finished the day at 1.3119, a substantial additional loss from Wednesday's close (1.3248).

Today, UK Halifax House prices and the Q2 unit labour costs will be published. However, the focus for sterling trading will be on the internal political developments. According to rumours, up to 30 lawmakers already support a campaign to replace May as prime minister. The risk of a political vacuum causes further sterling losses this morning. The pound will probably remain vulnerable as long as this topic dominates to financial and political headlines. Sterling again looks like a falling knife, especially the decline of cable is becoming quite impressive…

EUR/GBP made an strong uptrend since April to set a top at 0.9307 late August. UK price data amended the dynamics and hawkish BoE comments reinforced a sterling rebound. Medium term, we maintain a EUR/GBP buy-on-dips approach as we expect the mix of euro strength and sterling softness to persist. The prospect of (limited) withdrawal of BOE stimulus triggered a good sterling countermove. However, this rebound has apparently run its course. EUR/GBP supports at 0.8743 and 0.8652 are probably difficult to break. We look to buy EUR/GBP on dips. Yesterday's rebound above the 0.89 area improved the ST technical picture of EUR/GBP.0.9026 is 50% retracement of the recent countermove.

EUR/GBP: clears 0.89 resistance area

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7765; (P) 0.7815; (R1) 0.7844; More...

AUD/USD's strong break of 0.7807 support indicates that rise from 0.7328 has completed at 0.8124. More importantly, whole medium term rise from 0.6826 is possibly completed too. Intraday bias is now on the downside for 382% retracement of 0.6826 to 0.8124 at 0.7628 first. Decisive break there will target 0.7328 key cluster support (61.8% retracement at 0.7322) next. On the upside, break of 0.7874 minor resistance is need to indicate completion of the decline. Otherwise, outlook will now be cautiously bearish.

In the bigger picture, rise from 0.6826 medium term bottom is seen as corrective pattern. In case of further rally, strong resistance should be seen at 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside. Meanwhile, firm break of 0.7807 is the first signal that such correction is focused. Break of 0.7328 will bring retest of 0.6826 low.

Dollar Boosted by Tax Plan Hope, Non-Farm Payroll Watched

Dollar traders broadly higher today and remains as the strongest major currency for the week. The greenback is boosted by news that US President Donald Trump's administration is finally moving a procedural step on the tax plan. Optimism was also seen in the stocks markets as DOW, S&P 500 and NASDAQ all extended the record runs. Elsewhere, Sterling remains the weakest one for the week as troubled by political uncertainties in UK, and weak economic data. Nonetheless, Australian Dollar is sold off sharply in Asian session after RBA board member Ian Harper said he won't rule out a rate cut.

Trump's tax plan moved a procedural step

The Republican controlled House approved a fiscal 2018 spending blueprint yesterday, by 219-206 vote. It's a procedural step forward for US President Donald Trump's tax plan. With the blueprint, Republicans can now pass the tax bill by a simple majority vote in the Senate. As there are 52 out of 100 Republicans there, the Democrats could be bypassed. The move is seen by the markets that Trump's administration is finally taking the job of tax cut (or reform) seriously.

Fed Williams criticized the tax plan

However, there are still a loud voice of opposition of Trump's tax plan. San Francisco Fed President John Williams criticized that slashing tax rates could only boost short-lived growth. He pointed to analysis of Trump's proposals and said they "mostly boost demand and tend to have relatively small" impacts on labour supply and productivity.

Without targeting to raise productivity and growth potential, the tax cut could only promote "unsustainable" growth. And, such unsustainable could be easily undone by asset price bubbles, inflation and even recessions. He emphasized that "having policies that don't kind of maintain this sustainable path, stable inflation, will just end up, we know from history, creating potential recessions or high inflation or other problems and that doesn't benefit anybody."

Fed officials support another hike this year

Regarding monetary policy Williams said that "favorable employment numbers, combined with the findings on inflation and the steady pace of growth, are all behind my confidence that rates will need to rise to their new normal levels." Meanwhile, he noted that "conventional monetary policy has less room to stimulate the economy during an economic downturn." And, in those cases, Fed could need to "lean more heavily" on unconventional tools.

Kansas City Fed President Esther George said that it is "appropriate" to move interest rate "cautiously" at "this stage of expansion". She added that "moving interest rates at a gradual pace toward a level consistent with longer-run growth is the best step to help promote a continuation of the economic expansion." And there, "further gradual rate adjustments will be needed."

Philadelphia Fed President Patrick Harker said that US GDP growth will be "slightly above" 2%. And "until we see some other changes on the fiscal side of the house, we're not going to move that growth rate too much." Meanwhile, he is still supporting another rate hike this year and three more for next. Though he added that policymakers will "have to see how the inflation dynamics play out".

Upside risks for NFP, downside risks for wage

Non-farm payroll report is the main feature for today. NFP is expected to show 77k growth in the job market in September. That would be less than half of August's 156k, mainly due to the impact of hurricanes. Unemployment rate is expected to be unchanged at 4.4%. Expectation on wage growth is high as average hourly earnings could grow 0.3% mom.

The 77k expectation could have overestimated the impact of the hurricanes. After all, ADP report showed 135k private job growth, which wasn't too bad. Employment component of ISM manufacturing rose to 60.3, up from 59.9. Employment component of ISM non-manufacturing rose slightly to 56.8. Both are rather respectable numbers. 4-week average of initial claims rose 18k to 268k, still a very low number historically. Continuing claims was relatively unchanged at around 1.94m.

There are rooms for an upside surprise in today's NFP. Meanwhile, the biggest downside risk is on wage growth.

Elsewhere

Japan labour cash earnings rose 0.9% yoy in August. Leading indicator rose to 106.8 in August. German factory orders rose 3.6% mom in August. Swiss foreign currency reserve will be released in European session. Later today, in addition to US NFP, Canada will also release job data and Ivy PMI.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7765; (P) 0.7815; (R1) 0.7844; More...

AUD/USD's strong break of 0.7807 support indicates that rise from 0.7328 has completed at 0.8124. More importantly, whole medium term rise from 0.6826 is possibly completed too. Intraday bias is now on the downside for 382% retracement of 0.6826 to 0.8124 at 0.7628 first. Decisive break there will target 0.7328 key cluster support (61.8% retracement at 0.7322) next. On the upside, break of 0.7874 minor resistance is need to indicate completion of the decline. Otherwise, outlook will now be cautiously bearish.

In the bigger picture, rise from 0.6826 medium term bottom is seen as corrective pattern. In case of further rally, strong resistance should be seen at 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside. Meanwhile, firm break of 0.7807 is the first signal that such correction is focused. Break of 0.7328 will bring retest of 0.6826 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:00 | JPY | Labor Cash Earnings Y/Y Aug | 0.90% | 0.50% | -0.30% | -0.60% |

| 5:00 | JPY | Leading Index Aug P | 106.8 | 107.2 | 105.2 | |

| 6:00 | EUR | German Factory Orders M/M Aug | 3.60% | 0.70% | -0.70% | -0.40% |

| 7:00 | CHF | Foreign Currency Reserves (CHF) Sep | 724B | 717B | ||

| 12:30 | CAD | Net Change in Employment Sep | 14.0K | 22.2K | ||

| 12:30 | CAD | Unemployment Rate Sep | 6.30% | 6.20% | ||

| 12:30 | USD | Change in Non-farm Payrolls Sep | 77K | 156K | ||

| 12:30 | USD | Unemployment Rate Sep | 4.40% | 4.40% | ||

| 12:30 | USD | Average Hourly Earnings M/M Sep | 0.30% | 0.10% | ||

| 14:00 | CAD | Ivey PMI Sep | 57.2 | 56.3 | ||

| 14:00 | USD | Wholesale Inventories Aug F | 1.00% | 1.00% |