Sample Category Title

Elliott Wave Analysis: AUDUSD and S&P500 Intraday View

USD is rallying on better than expected Jobless Claims. We can see some sharp moves against the AUD and CAD in the last few hours, with Aussie trading close to Oct 03rd low that can be out soon if we consider that flat correction in wave 4 can be finished. There is room for a fifth wave fall to complete red wave 3) near 0.7750/0.7720 region.

AUDUSD, 1H

E-mini S&P500 remains trading at new all-time highs, now still in wave 3 which can be nearing a completion at current 261.8% Fib. level of wave 1 from 2, and with an ending diagonal at the top. Market may also slow down ahead of tomorrows NFP figures, so we think fourth wave set-back may show up in the near-term; in normal circumstances that would be back to 2528.

S&P500, 1H

Canada’s Trade Deficit Unexpectedly Widened to $3.4 Billion in August

Highlights:

- Canada's nominal merchandise trade deficit widened to $3.4 billion in August from $3.0 billion in July.

- Export volumes declined for a third-consecutive month, led for a third-consecutive time by lower non-energy exports.

- Imports continue to outperform, suggesting that domestic demand remains strong.

Our Take:

Exports fell 1.0% in nominal terms and 1.5% controlling for price changes. The August pullback marks a third consecutive monthly export volumes drop with non-energy exports once again leading the way lower. The international trade data is notoriously volatile and much of the recent pullback looks to be just a retracement from four consecutive quarters of gains, culminating in a 10% jump in overall export volumes in Q2 that was clearly not sustainable. We continue to expect that a pickup in trade growth globally in recent quarters and signs of life in the U.S. industrial sector will ultimately support a return to a gradual uptrend in Canadian exports going forward, although attention will also be paid to any signs that the (broadly-based) appreciation in the Canadian dollar since early June is eating into Canada's share of foreign demand. The import data continues to look more encouraging. Import volumes inched up 0.3% in August and were still up 3.1% from a year ago. Imports of industrial equipment - a key indicator of domestic business investment spending - inched lower in volume terms in August but were still up 13% from a year ago and a whopping 18% (annualized rate) Q3 to-date relative to Q2. The relative strength in imports is a negative for the trade balance but argues that domestic demand remains strong.

On balance, today's data adds to the evidence that the outsized outperformance of the economy over the last year is coming to an end. It also, however, does not alter our expectation that growth will still remain at an 'above-potential' pace and - with the economy probably already quite close to capacity limits - that further gradual Bank of Canada interest rate hikes will be warranted.

EUR/USD Drifting Lower in the 1.17 Big Figure

- European equities trade modestly higher in a calm session. Madrid profits from the easing of tensions to outperform (+1.6%). US equities opened slightly higher.

- The ECB policymakers are keen to press ahead with plans to end their bond-buying spree next year, despite some reservations on wage inflation and the strength of the euro. Governing council members were increasingly confident that the recovery would last. Market developments were favourable, while there were "nascent" signs of reflationary forces

- Sterling took a fall, slipping against both the dollar and the euro, after a calamitous speech by PM May boosted political uncertainty. The move brings sterling to a one-month low against the dollar. A critical speech by Mrs May on Wednesday was overshadowed by issues, including a prankster handing the prime minister a P45 redundancy slip.

- Switzerland's return to inflation seems to be taking hold, with the Y/Y pace of price rises reaching 0.7% in September, the highest since March 2011. August's rate was 0.5%. Deflation reached its most severe point in August 2015 when inflation was down 1.4% Y/Y.

- Swedish industrial production fell more than economists expected in August, with July's figures revised down. Industrial production fell 1.7% M/M. The SEK (EUR/SEK 9.52) held on to the big gains of the last three days.

- Saudi Arabia will continue working with Russia to stabilise global oil markets, the country's King said during talks with Russian President Putin in Moscow, where the two leaders discussed the war in Syria and other issues.

- US initial claims dropped a slightly bigger than expected 12K to 260K in the most recent week, gradually unwinding the surge after the passage of the hurricanes. The US trade deficit was marginally lower than expected at $42.3B in August. It was an 11 month low and follows a $43.6B deficit in July. Exports rose 0.4% M/M, imports fell 0.1% M/M. It suggests the global economy is doing well and the US profits from a weaker dollar.

- Philly Fed Harker said he (together with 9 other governors) projects three rate hikes in 2017, suggesting that he will vote for such an increase at the December meeting. He admits there are some issues with inflation but also calls the economy "incredibly resilient."

Rates

Slight outperformance longer end of the German curve

Ahead of the key US payrolls tomorrow, core bonds had an uneventful session. The Bund had a difficult start, but rebounded at a snail's pace from mid-morning onwards. The morning session was devoid of market moving economic reports and comments of ECB's Praet about the need for sufficient convergence before euro adoption had understandably no impact. We saw already a few days a mild tendency to buy German bonds on dips and that might also have been the case today. The Minutes of the last ECB meeting, published in early afternoon, were interesting suggesting that the ECB might recalibrate its purchases by buying less, but compensate by buying for longer. The ECB should also use the forward guidance on rates to keep expectations for a rate hike at bay for longer. Of course, decisions still need to be taken and many details remain unknown. Anyway, the Bund went down for a brief moment after the release, but erased the losses soon.

The US Treasuries kept a sideways trading mode throughout the session, unmoved by the eco releases, which were close to expectations. Philly Fed Harker sees another rate hike this year and Fed Williams said that inflation will rise to 2%, enabling the Fed to raise rates. The remarks of Williams might have triggered some modest (temporary) selling, but not enough to give US Treasuries firm direction. After closure of our report, the factory orders report will be published followed later on by speeches of Fed governors Dudley and Bullard. However, with the payrolls looming, we expect trading to remain quiet and technical uneventful.

At time of writing, German yields are up 0.8/1 bp in the 2-to-5-yr sector and were nearly flat in the 10-30-yr sector. US yields rose up to 2 bps across the curve. On intra-EMU markets, tensions surrounding the Spanish political situation eased a bit, allowing a modest narrowing of the 10-yr yield spreads. Spain and Italy outperformed with a 6 bps narrowing.

The Minutes of the September ECB meeting were interesting and showed that governors were keen to press ahead with plans to end the bond buying programme next year despite some reservations about the (weak) wage inflation and the euro strength. They were increasingly confident the recovery would last and saw "nascent" signs of reflationary forces. The Minutes indicate that the ECB is unlikely to follow the Fed's method of gradually slow the pace of bond purchases. The focus of the debate is on two issues: the degree to which they will slow the pace of purchases and for how long they will keep buying (the recalibration). The benefits from a longer intended purchase horizon combined with a greater reduction in the amount were compared to a shorter period of purchases and larger monthly volumes. The accounts suggest some governors prefer a slower-for longer approach. It also suggest that the council will use the forward guidance on rates to keep monetary policy loose.

Currencies

EUR/USD drifting lower in the 1.17 big figure

Today, there was again no clear story to guide USD trading. There were only second tier eco data in the US and Europe. Tensions on the Spanish markets eased, but didn't cause a sustained euro rebound. In the afternoon, some 'hawkish' Fed comments caused modest dollar gain of the dollar. However, EUR/USD (1.1720 area) and USD/JPY 112.60 area trade still are range-bound.

Overnight, Asian markets showed a mixed picture. Japanese indices were little changed and so was USD/JPY (112.75 area). Australia August retails sales were very weak. AUD/USD declined 0.7865 to the 0.7830 area. EUR/USD held a very tight sideways range in the 1.1760 area.

As was the case yesterday, there was again no clear story to guided trading in EUR/USD or USD/JPY during European trading. The tensions on Spain eased with equities rebounding and Spanish spreads narrowing. EUR/USD tried to go higher early in Europe, but soon settled in a tight sideways range roughly between 1.1750/80. The Minutes of the September ECB meeting suggested that the Bank could reduce bond buying by a substantial amount, but keep the buying for longer. The impact on European bonds or the euro was limited. If anything, the euro felt some modest selling pressure.

The dollar gradually received a better bid as US investors joined trading. Fed's Harker and Fed Williams defended another rate increase in 2017. The comments reinforced the USD bid. EUR/USD trades currently in the 1.1720 area. USD/JPY also rebounded off the intraday lows; but at 112.60 the pair trades in negative territory compared to yesterday's close. In a broader perspective, the dollar is still in consolidation modus, awaiting more higher profile news before starting a new directional trend. Maybe tomorrow's payrolls can do the job.

EUR/GBP squeezed back above 0.89

Sterling came under pressure from the start of trading in Europe. There were no UK eco data releases. In the (financial) press there were extensive analyses of the 'failed' key note speech of UK PM May at the annual meeting of the Conservative congress. The 'event' only raised more questions whether May is the right person to lead the Conservative party and the UK throughout the tumultuous Brexit period. This additional uncertainty on the political support for PM May weighed on sterling. The EUR/GBP short-squeeze accelerated as the pair broke the 0.8900/07 resistance area. After the initial break higher, EUR/GBP settled in a tight range around 0.8925. The currency lost also ground against the dollar. Cable trades currently below the 1.3150 handle. The down-leg in the currency pair even looks like accelerating. Later today ,BoE McCafferty and Chief economist Haldane are still scheduled to speak. If monetary policy issues are addressed, they will probably defend the scenario of a (limited) tightening in the near future.

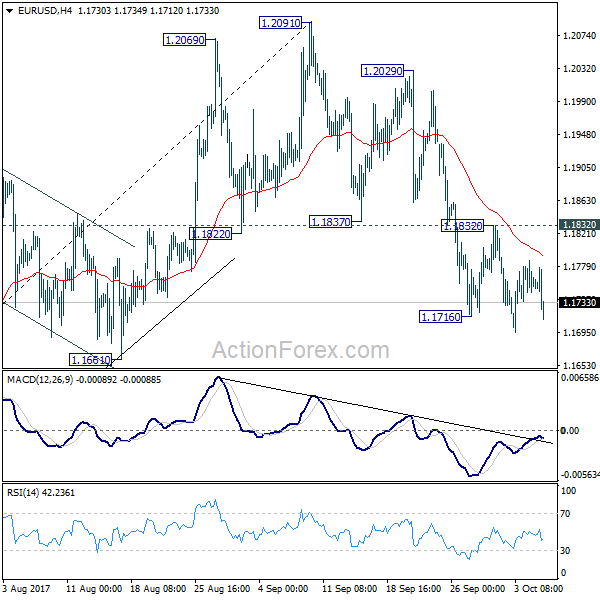

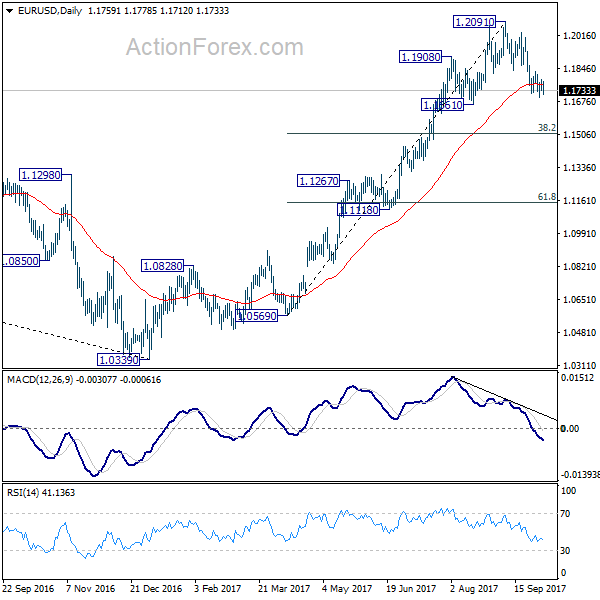

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1702; (P) 1.1738 (R1) 1.1780; More...

As long as 1.1832 resistance holds, fall from 1.2091 is expected to extend lower. Such decline is correcting whole rise from 1.0569. Deeper fall should be seen to 38.2% retracement of 1.0569 to 1.2091 at 1.1510, where we're expecting support to bring rebound. On the upside, break of 1.1832 minor resistance will suggest that the corrective fall is completed and turn bias back to the upside.

In the bigger picture, rise from medium term bottom at 1.0339 is not finished yet. It's expected to continue after pull back from 1.2091 completes. And, next target will be 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. However, it should be noted that there is no confirmation of trend reversal yet. That is, such rebound from 1.0399 could be a correction. And the long term fall from 1.6039 (2008 high) could resume. Hence, we'd be cautious on strong resistance from 1.2516 to limit upside.

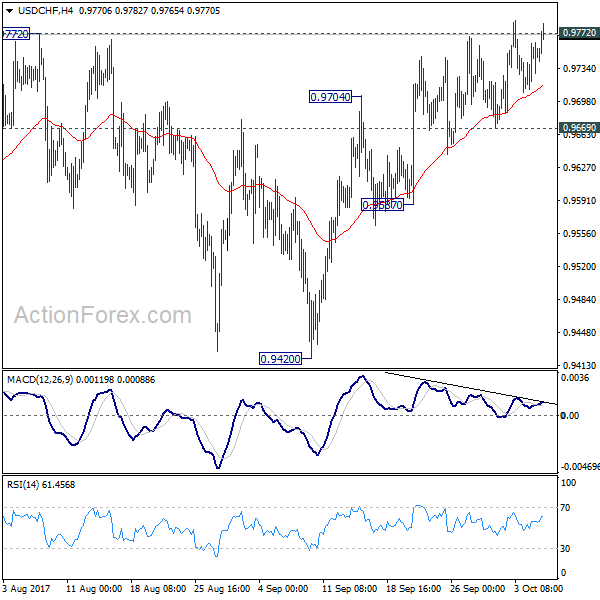

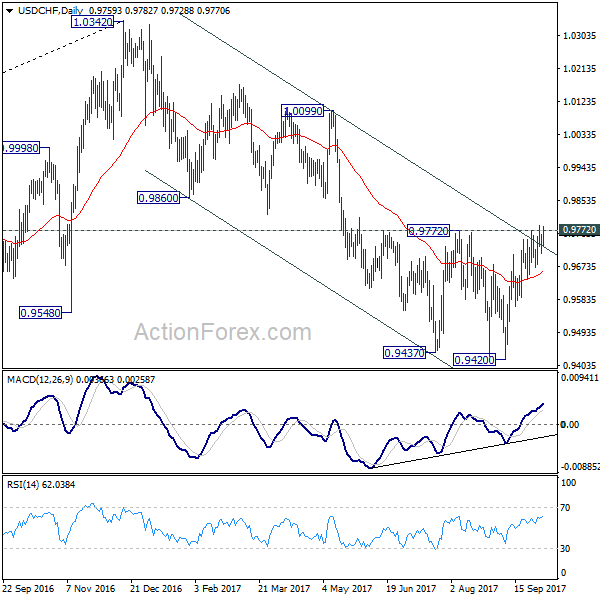

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9714; (P) 0.9749; (R1) 0.9771; More....

USD/CHF is trying to break 0.9772 resistance again and there is not follow through buying yet. Intraday bias remains neutral first. On the upside, decisive break of 0.9772 key resistance will suggest that whole down trend form 1.0342 has completed. In that case, near term outlook will be turned bullish for 0.9860/1.0099 resistance zone. However, break of 09669 minor support will suggest rejection from 09772 and turn bias back to the downside for 0.9587 support. Break will target retesting 0.9420 low.

In the bigger picture, focus remains on whether 0.9443 key support (2016 low) could be taken out firmly as down trend from 1.0342 extends. There are various interpretation of the price actions. But in any case, medium term outlook will stay bearish as long as 0.9772 resistance holds. Current down trend could extend to 38.2% retracement of 0.7065 (2011 low) to 1.0342 (2016 high) at 0.9090. However, break of 0.9772 will indicate that USD/CHF has successfully defended 0.9443 again and turn outlook bullish for 1.0099 resistance.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.40; (P) 112.67; (R1) 113.01; More....

USD/JPY is still bounded tight range below 113.25 and intraday bias remains neutral for the moment. On the upside, sustained break of medium term channel resistance will argue that correction from 118.65 is already completed with three waves down to 107.31. Break of 114.49 will confirm this bullish case and target a test on 118.65 next. On the downside, considering bearish divergence condition in 4 hour MACD, break of 111.46 will suggest rejection from the channel resistance and turn bias back to the downside.

In the bigger picture, rise from 98.97 (2016 low) is seen as the second leg of the corrective pattern from 125.85 (2015 high). It's unclear whether this this second leg has completed at 118.65 or not. But medium term outlook will be mildly bearish as long as 114.49 resistance holds. And, there is prospect of breaking 98.97 ahead. Meanwhile, break of 114.49 will bring retest of 125.85 high. But even in that case, we don't expect a break there on first attempt.

NZDUSD Bearish in Short-Term; Risk Tilted to Downside after Bearish Crossover of Moving Averages

NZDUSD has maintained a bearish phase in the short term since September 20. Risk is clearly tilted to the downside and further weakness in the market could see prices drop another leg lower to extend the bearish phase from the 0.7434 high.

For now, downward momentum has weakened as RSI and MACD are flat on the 4-hour chart. Both indicators in bearish territory which keep the possibility for NZDUSD moving lower again.

Prices declined steadily from the 0.7434 high before steadying around the key psychological level at 0.7200. Then there was a sharp decline from 0.7205 earlier this month. A daily close below 0.7131 (August 31 low) would indicate that the market has moved into a bearish phase with the next target at 0.7055. Breaking below the key 0.7000 area would increase downside pressure and the focus would turn to the next major low at 0.6817.

A rise above 0.7200 would help the market challenge the September 29 high at 0.7243. NZDUSD would need to rise above the 50-period moving average at 0.7290 to see a more sustained reversal in the current trend and give scope to target the September 20 peak at 0.7434.

The September 26 bearish crossover of the 20-period MA with the 50-period MA on the 4-hour chart puts near-term risk squarely on the downside. Only a move back above 0.7200 would ease immediate pressure.

U.S. Trade Deficit Narrows Slightly in August

The U.S. international trade deficit narrowed by $1.2bn to $42.4bn, or a touch lower than market consensus of $42.7bn. The trade deficit for July was little revised, measuring $43.6bn versus $43.5bn previously.

Exports rose 0.4% on a month-on-month (m/m) basis in August. Consumer (+6.4%), capital (+0.9%), and automotive (+0.5%) goods helped to offset declines in food and beverage and industrial supplies exports in the month. Services exports also rose 0.4% in August.

Imports declined for the fourth consecutive month in August, falling 0.1% m/m. Declines in industrial supplies (-1.3%), capital goods (-0.9%), and food and beverages (-0.7%) offset strong rebound in automotive imports (+2.3%). Service imports were largely unchanged in the month.

Excluding the impact of price changes, export volumes fell 0.8% in August, marking two consecutive monthly declines with recent moves implying almost a full reversal of the 1.8% m/m advance from June. Similarly, import volumes declined 0.6% m/m in August.

Key Implications

There are few if any surprises in today's trade report for August. Although the Census Bureau is unable to identify specific Hurricane Harvey related impacts, the contraction in export volumes includes a decline in the volume of petroleum exports of more than 18% m/m, but curiously shows an increase of about 2% in the volume of petroleum imports. This story is consistent with a narrative whereby inbound oil tankers destined for Southeast Texas were diverted to unaffected ports in the U.S. and Mexico.

Next month's trade report will likely help decide how much net trade adds or detracts from third-quarter economic activity. Today's trade report on balance suggests a very small positive impact on third quarter economic growth, particularly as refineries were slowly getting back to pre-Hurricane capacity. Still, a strong uptick in imports in September could easily swing the impact to a small drag. Looking beyond short-term volatility, strong global demand and a weaker U.S. dollar in trade-weighted terms should continue to provide some modest support for exports in the coming months.

Canada’s Trade Deficit Widened in August

Canada's trade deficit widened to $3.4B in August (from $3.0B in July), as exports fell 1% while imports held steady. In real terms, export volumes were down by an even larger 1.9%, while import volumes eked out a slight 0.2% gain.

Exports were down in 5 of 11 industries, led by metal ores and non-metallic minerals (-9.7%), chemical, plastic and rubber products (-5.9%) and consumer goods (-3.8%). Meanwhile, aircraft and other transportation equipment (+3.1%) and electronic equipment (+2.5%) were the top performers during the month.

Imports were unchanged, as declines in aircraft and other transportation equipment (-10.2%) were offset by increases in metal ores and non-metallic minerals (+9.9%) and motor vehicles (+2.5%).

Canada's trade surplus with the U.S. narrowed to $2.3B in August (previously $3.2B), as exports slipped 1.8% while imports were up 0.9%. Canada's trade deficit with the rest of the world narrowed to $5.7B (previously $6.2B), with exports up 1.5% and imports down 1.6% during the month.

Key Implications

August marks the third consecutive month of declines in export volumes, which now sit 6% lower than the peak reached in May. This weak handoff for the third quarter suggests that net trade is likely to detract from overall growth during the quarter. Even with this disappointing report, economic activity remains on track to expand by a solid 2.2% in Q3.

Going forward, a healthy U.S. economy should help to prop up demand for Canadian-made goods, supporting export volumes. However, the appreciation of the loonie since early-September has somewhat reduced the competitiveness of Canadian exporters and could provide some offset. The outcome of the NAFTA re-negotiations also poses some risk, but with negotiations moving slowly, it is unlikely to impact trade this year.

Overall, the Canadian economy is on solid footing, and the Bank of Canada is likely to maintain a tightening bias. Future hikes will be heavily data dependent with recent export performance a weak spot. However, there are a number of key data releases between now and the next Fixed Announcement Date later this month that will influence the Bank's decision.

EUR/JPY Further Correction

The EUR/JPY drops and erases the last day's minor gains. Is trading in the red as the Yen is supported by the Nikkei's minor drop. The pair has developed a Rising Wedge pattern in the last weeks, I've said in the last articles that we may have a broader drop if the pattern will be confirmed. The Euro is losing ground versus the Yen as the bulls weren't strong enough to keep the rate above very important resistance levels. However, we still need a confirmation that will drop further because this could be only temporary.

The European currency drops further even if the Euro-zone Retail PMI increased from 50.8 to 52.3 points, reaching the highest level of the last 3-months. Price is driven lower by the technical factors, a further Nikkei's drop will force the Yen to appreciate versus all its rivals.

Price drops and approaches the downside line of the potential Rising Wedge pattern. It should drop much deeper after the failure to retest the median line (ml) of the black ascending pitchfork and after the failure to stabilize above the sliding line (SL). The Rising Wedge pattern could be confirmed if the Nikkei will slip lower in the upcoming days. Support can be found at the upper median line (UML) of the major ascending pitchfork, but a valid breakdown from the chart pattern will force the rate to take out this support.