Sample Category Title

Daily Technical Analysis: EURUSD, GBPUSD, USDJPY, USDCHF

EURUSD

The EURUSD had a bearish momentum yesterday bottomed at 1.1699. The bias remains bearish in nearest term testing 1.1600 region. Immediate resistance is seen around 1.1780. A clear break above that area could lead price to neutral zone in nearest term but only a clear break above 1.1900/35 key resistance could potentially end the current bearish correction phase. On the downside, a clear break and daily/weekly close below 1.1600 would expose 1.1450 region next week.

GBPUSD

The GBPUSD continued to trade lower yesterday, broke below 1.3150 support area, bottomed at 1.3107. The bias remains bearish in nearest term testing 1.3030. A clear break and daily/weekly close below that area could trigger further bearish pressure testing the daily EMA 200 and the trend line support as you can see on my daily chart below, located around 1.2980/50 area. Immediate resistance is seen around 1.3150. A clear break above that area could lead price to neutral zone in nearest term but as long as stay below 1.3400 price is still in a bearish correction phase.

USDJPY

The USDJPY had another indecisive movement yesterday. There are no changes in my technical outlook. The bias remains neutral in nearest term. My H1 chart bias remains bullish, but we need a clear break above 113.20 key resistance to continue the bullish phase targeting 114.50 region. Immediate support is seen around 112.32. A clear break below that area could trigger further bearish pressure testing 111.65 key support. Overall I remain neutral.

USDCHF

The USDCHF had a bullish momentum yesterday topped at 0.9795. The bias is bullish in nearest term but note that price is inside my key resistance zone as you can see on my daily chart below which is a good place to sell with a tight stop loss above 0.9807. Immediate support is seen around 0.9765. A clear break below that area could lead price to neutral zone in nearest term testing 0.9700 area. On the upside, a clear break and daily/weekly close above 0.9807 would activate my bullish mode targeting 0.9950 region next week.

Elliott Wave View: EURUSD

EURUSD Intra-Day Elliott Wave view suggests the decline from 9/8 peak remains in progress as an expanded Flat Elliott Wave structure. Down from 9/8 high (1.2094), pair ended Intermediate wave (A) at 1.837. Bounce to 1.2034 ended Intermediate wave (B). Intermediate wave (C) remains in progress and unfolding as 5 waves impulse where Minor wave 1 of (C) ended at 1.186, and Minor wave 2 of (C) ended at 1.2. Down from there, Minor wave 3 of (C) ended at 1.1716 and bounce to 1.1832 ended Minor wave 4 of (C).

While EURUSD stays below 1.1789, it has scope to extend lower in Minor wave 5 of (C) and reach 1.1586 – 1.1633 area. The move lower will also end cycle from 9/8 peak and complete Primary wave ((W)). Afterwards, Pair should bounce in Primary wave ((X)) to correct cycle from 9/8 peak in 3, 7, or 11 swing at least. If pair breaks above 1.17899 from here without making a new low, pair may have ended Primary wave ((W)) already.

EURUSD 1 Hour Elliott Wave Chart

Expanded Flat is a 3 waves corrective pattern, and the inner subdivision is labeled as A,B,C with 3,3,5 structure. That means waves A and B are always corrective structures i.e. could be WXY, WXYXZ, Zigzag or any 3 waves corrective pattern. Wave C is either 5 waves impulse or ending diagonal pattern. In the graphic below, we can see what Expanded Flat structure looks like. Inner structure has ABC labeling, where wave B can complete below or above the starting point of wave A. Wave C should complete below the end point of wave A (usually at 1.236-1.618 fibonacci extension A related to B).

Market Morning Briefing: Dollar-Yen Has Been Consolidating Below 113.00-50

STOCKS

Dow (22775.39, +0.50%) has broken above all immediate resistances and looks strongly under the control of the bulls now. While the upward momentum stays intact, we could see a rise towards 23000-23250 levels soon.

Dax (12968.05, -0.02%) is almost stable today but is poised for another upside shot targeting the crucial resistance near 13000-13050 levels from where a sharp corrective dip is likely. The index could close the week on a positive note. By the end of next week, we could possibly get to see some initial signs of correction while below 13050.

Nikkei (20679.18, +0.25%) is trading just below important resistance zone of 20700-20745 and while that holds, scope of further upside looks limited. The index could remain stable and possibly enter into a sideways consolidation if not see a sharp fall towards 20600-20500 levels in the near term.

Resistance near 9970-9950 continues to hold for now. Nifty (9888.70, -0.26%) could trade within 9950-9850 for a few sessions before coming down towards 9800.

Shanghai is closed this week. Fresh movement expected on Monday after the weeklong holiday.

COMMODITIES

Gold (1268.45) is stuck within the 1285-1260 region and could trade sideways for some sessions. Silver (16.61) is also sideways but could possibly come off towards 16.50-16.25 levels in the near term.

Gold-Silver ratio (76.298) could test support near 75.80 and while that holds, we could see a bounce back to 77 in the next 2-3 sessions.

Brent (56.91) has bounced from above support levels of 54.80-55.00 as seen on the 3-day candles. While the immediate support holds, the price could move up to levels near 57-58 soon.

WTI (50.73) seems to have enough room on the downside just now and has potential to move down towards 49.00-48.50 before attempting to rise again in the longer run.

Copper (3.0475) rose sharply and is trading above 3.00 just now. While above 3, the price could start moving up again towards 3.10 in the near term. View is bullish for the coming sessions.

FOREX

We may be wrong, but it appears that with Dollar Index at 93.94 and Euro at 1.1710, the market is going in Long Dollars into the US NFP tonight. Caution is advised as we see Resistance at 94.50 on the Dollar Index and Support in the 1.1665-00 region on the Euro.

Note that the German-US 2Yr Spread (-2.19%) may have Support at -2.23% while the German-US 10Yr Spread (-1.90%) may have Support near -1.94%, limiting the downside in the Euro.

Dollar-Yen (112.85) has been consolidating below 113.00-50 for the last few days but might attempt to rise to 113.50-114.00 in the short term as the US-Japan 10Yr Spread continues to rise.

Not covering the Pound, Aussie today. Apologies.

Dollar-Rupee (65.14) might move up to 65.25-30 today.

INTEREST RATES

There may be some more room on the upside for US yields, but limited to 3.00% on the 30Yr (2.89%), 2.50% on the 10Yr (2.35%) and 2.20% on the 5Yr (1.95%). If all these levels are tested, the US Yield Curve will flatten.

Market expectation is a low 88K from the US NFP tonight. A higher number can well be a trigger for a rise in US yields.

See Forex section above for views on German-US and US-Japan yield spreads.

10Yr GOI (6.7286%) is breaking above 6.70%, the level that we expected to hold as resistance earlier. Needs to be watched carefully.

The Running Of The Dollar Bulls ?

The Running of the Dollar Bulls?

Not quite the running of the bulls as yet but indeed unambiguous signals are building to support the firm USD view. While the markets remain cemented within recent trading ranges, the pendulum is soundly swinging in favour of the dollar as the stars continue to align in support of this view.

Heading into NFP, market forecasts are stunted given the likelihood of the hurricanes distorting the data. None the less, it has been difficult to overlook this week’s stellar US economic data as both ADP data, and weekly initial jobless claims have been surprisingly buoyant. But perhaps the most astounding signals are generating from this week’s ISM PMI’s that clocked in at 12-year highs. One can only assume that more positive economic data surprises are just around the corner.

Fed Williams took to the wires overnight and was unquestionably hawkish in his view not only supporting the 2017 December rate hike but lobbying for three more nudges in 2018. But it was his mention that the risk for asset price bubbles that was especially hawkish as it supports the view that the Feds are no longer single-mindedly focused on inflation for policy guidance.

With the markets woefully underpriced the Fed dot plots, a more aggressive lean from the FOMC would offer up a smorgasbord of opportunities for the dollar bulls who would most certainly have sights set on AUD, EUR and GBP, the current weak links.

Inter-party GOP squabbling has subsided as the US House has taken essential steps setting the stage to roll out a determined tax-overhaul bill which should pass without Democratic backing. Of course with this greater confidence comes a more significant fall but the level of GOP impudence this time around suggests a done deal.

Non-Farm Payroll

Since some hurricane impact is anticipated on the data any blemish on payrolls will most certainly be sidestepped. The tail risk, however, may come from a better than expected wages reading. Make no mistake AHE tends to give FX traders the clearest signal on NFP and this pattern should hold true even more so today. Since the wages reading has been exceptionally soft, any upside surprise will likely generate an outsized move on the USD.

Balance of Risks

Euro

The single currency remains weighted down by the “Pain in Spain” driven by Catalan consternations. But let’s not overlook the above-trend amplification of the US economy which has contrarians coming out of the woodwork now thinking FED -ECB policy divergence as opposed to convergence. US Treasury yields continue firming, and the inflationary expectations from the US tax reform are expected to provoke a further rise. While EURUSD should remain under pressure given this scenario, the EURO bulls are unlikely to give up the plot preferring to hold on for the October ECB

Australian Dollar

The buoyant US dollar along with the acutest declines in domestic retail sales in the past four years has the Aussie trading below the fundamental .7800 level in early APAC trade. On the US side of the equation Fed repricing, supportive US economic outlook and a budget resolution paving the way for tax reform has US dollar bulls champing at the bit.

Japanese Yen

Despite election jitters, the rise in US yields and the firming USD should remain the aggressive driver for this trade. While a top side breakout appears imminent its hard to overlook the election poll risk as we near election day.

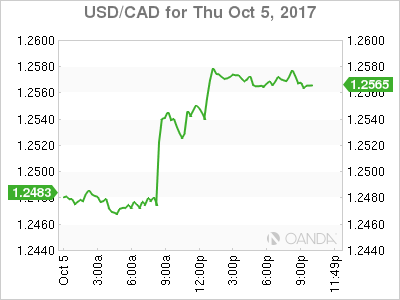

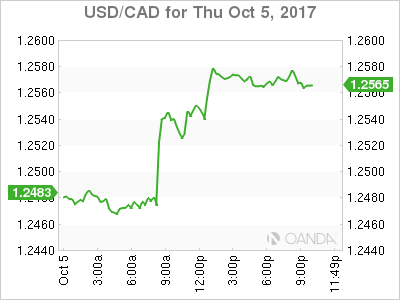

USD/CAD Canadian Dollar Lower Ahead Of US And Canada Jobs Report

The Canadian dollar is lower on Thursday after trade data in Canada showed a larger deficit. Exports continue a downward trend and as many economists have predicted the Canadian economy is losing momentum. The story was different for the US trade balance, that showed a rise in exports and boosted the USD to multi week highs.

The USD/CAD gained 0.74 percent in the last 24 hours. The currency pair is trading at 1.25688 after trade data in the US surprised to the upside with rising exports while a different story played out in Canadian figures. The Canadian trade deficit widened in August with exports falling for a third month in a row.

Economists have warned that the Canadian economy is cooling down after an impressive first half of 2017. Two rate hikes and impressive growth took the loonie to appreciate versus a struggling USD. A third rate hike is losing ground in the eyes of the market. The Bank of Canada (BoC) cut rates by 50 basis points in 2015 and it wasn’t until their assessment of the economy improved in 2017 that they have hiked twice to leave the benchmark rate at 1.00 percent.

Tomorrow’s job releases in Canada and the US will be telling on how the two economies are acting in tandem or breaking apart. The tropical storms in the US could obfuscate the jobs situation in the US while in Canada there are growing concerns about the rate of full time job losses. The headline number in Canada has been steady, but thanks to part time positions. Jobs in Canada are expected to have gained 13,900 positions in September.

The US dollar is trading near seven week highs as economic data has been solid, the central bank is still pushing for a third rate hike and the tax reform proposal is moving forward. Leading manufacturing and non manufacturing indicators have improved and rising exports have shrunk the trade deficit to a yearly low but questions remain on the effect the tropical storms will have on the biggest economic indicator in the market.

The U.S. Bureau of Labor Statistics will release the non farm payrolls (NFP) report on Friday, October 6 at 8:30 am EDT. The economy is forecasted to have added 82,000 positions in September. The impact of hurricanes Harvey and Irma is to blame for the underperformance but given the resilience of the economy the possibility of the final figure beating expectations is not far fetched.

The ADP private payrolls report came in close to the forecast with 135,000 jobs and unemployment claims rose by 260,000 when a 266,000 gain was anticipated. Fed FOMC voting members were in full force this week and today’s comments from Philadelphia Fed chief Patrick Harker that while the 2 percent inflation target will remain untouched he still believes there should be another rate hike. The CME FedWatch tool shows a 86.7 percent probability of the interest rate moving higher to a 125 to 150 basis points range.

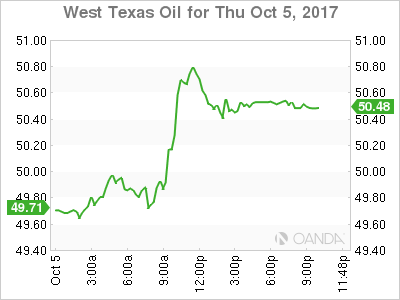

Oil rose 2 percent on Thursday. West Texas Intermediate is trading at $50.55 after Russia and Saudi Arabia sent signals to the market about a potential extension to the production cut agreement between the Organization of the Petroleum Exporting Countries (OPEC) and other major producers. The two nations have acted as representatives of the two groups and limiting output could force prices higher with the biggest question mark being how are the non-pact producers going to react and if their production increases can offset the output curbs.

Uncertainty about the Iran nuclear deal is also pushing prices higher. President Trump could introduce another embargo to Iranian exports, energy included, reducing global supply.

Market events to watch this week:

Friday, October 6

8:30 am CAD Employment Change

8:30 am CAD Unemployment Rate

8:30 am USD Average Hourly Earnings m/m

8:30 am USD Non-Farm Employment Change

8:30 am USD Unemployment Rate

Dollar Climbs Ahead Of Jobs Report

Strong data, Fed comments pushing USD higher

The US dollar is trading near seven week highs as economic data has been solid, the central bank is still pushing for a third rate hike and the tax reform proposal is moving forward. Leading manufacturing and non manufacturing indicators have improved and rising exports have shrunk the trade deficit to a yearly low but questions remain on the effect the tropical storms will have on the biggest economic indicator in the market.

The U.S. Bureau of Labor Statistics will release the non farm payrolls (NFP) report on Friday, October 6 at 8:30 am EDT. The economy is forecasted to have added 82,000 positions in September. The impact of hurricanes Harvey and Irma is to blame for the underperformance but given the resilience of the economy the possibility of the final figure beating expectations is not far fetched.

The ADP private payrolls report came in close to the forecast with 135,000 jobs and unemployment claims rose by 260,000 when a 266,000 gain was anticipated. Fed FOMC voting members were in full force this week and today’s comments from Philadelphia Fed chief Patrick Harker that while the 2 percent inflation target will remain untouched he still believes there should be another rate hike. The CME FedWatch tool shows a 86.7 percent probability of the interest rate moving higher to a 125 to 150 basis points range.

The EUR/USD fell 0.45 percent on Thursday. The single currency is trading at 1.17050 in a tight range awaiting the release of the September U.S. non farm payrolls (NFP) report. The US dollar has traded higher versus the euro as the US economy has shown resilience after two hurricanes.

The release of the European Central Bank (ECB) monetary policy meeting minutes showed there is still an ongoing debate on how exactly to pull back stimulus. Fearing a taper tantrum ECB policy makers are still discussing the size of the taper and a mix of extending the duration. There is even the possibility of changing the name of the process to recalibration to avoid the negative connotation of a tapering.

The situation in Catalonia is far from resolved and Separatists will meet on Monday defying a Spanish court order, but the market has been alerted that they will not declare independence.

The USD/CAD gained 0.74 percent in the last 24 hours. The currency pair is trading at 1.25688 after trade data in the US surprised to the upside with rising exports while a different story played out in Canadian figures. The Canadian trade deficit widened in August with exports falling for a third month in a row.

Economists have warned that the Canadian economy is cooling down after an impressive first half of 2017. Two rate hikes and impressive growth took the loonie to appreciate versus a struggling USD. A third rate hike is losing ground in the eyes of the market. The Bank of Canada (BoC) cut rates by 50 basis points in 2015 and it wasn’t until their assessment of the economy improved in 2017 that they have hiked twice to leave the benchmark rate at 1.00 percent.

Tomorrow’s job releases in Canada and the US will be telling on how the two economies are acting in tandem or breaking apart. The tropical storms in the US could obfuscate the jobs situation in the US while in Canada there are growing concerns about the rate of full time job losses. The headline number in Canada has been steady, but thanks to part time positions. Jobs in Canada are expected to have gained 13,900 positions in September.

Market events to watch this week:

Friday, October 6

8:30 am CAD Employment Change

8:30 am CAD Unemployment Rate

8:30 am USD Average Hourly Earnings m/m

8:30 am USD Non-Farm Employment Change

8:30 am USD Unemployment Rate

Spanish Crisis Keeps Euro Under Pressure

The main issue for the European markets remains the political situation in Spain where we may see an announcement regarding Catalonia's independence come through on Monday. A vote for independence may see the euro continue to lose ground against its major trading partners. On the other hand, after the release of the ECB monetary policy meeting minutes it has become clear that the reduction of stimulus measures in the Eurozone in 2018 is highly likely. Positive news from the Eurozone's retail PMI growth in September to 52.3 against 50.8 in August was not able to offset the negative effects from Spain. Some support for the US dollar came from positive data on the trade balance deficit in the US that in August was only 42.4 billion - this is 0.3 better than forecasted. At the same time, factory orders in the US increased by 1.2% in August against the 1.0% increase expected. Investors are waiting for tomorrow's labor market data in the US that is likely to result in increased volatility. Strong numbers on non-farm payrolls and unemployment are likely to increase confidence in another rate hike by the Fed in December.

The sterling remains in the bearish trend amid uncertainty linked with the Brexit talks. Statistics on the decline in the number of registered autos by 9.3% to 426,170 in September also strengthened concerns about the prospects of British economic growth.

The WTI price demonstrated positive dynamics following the news about crude oil inventories reduction in the US by 6.0 million barrels compared to an expected decline of only 0.5 million barrels. This news however, didn't help the Canadian dollar that felt the pinch due to the trade deficit increase in August to 3.4 billion, which is 0.8 billion worse than the average prediction.

EUR/USD

The EUR/USD price resumed declining after some consolidation above 1.1750 and in case of passing through the support at 1.1700, the next targets will be 1.1620 and 1.1550. In order to resume positive dynamics, it will be necessary to overcome the 1.1800-1.1825 range and in this case the next goals will be 1.1925 and 1.2000. The RSI on the 15-minute chart is near the oversold zone, which points to an increased chance of upward correction.

GBP/USD

The GBP/USD has shown a sharp descending movement and approached the lower limit of the descending channel. Breaking through the support at 1.3150 may become the basis for continued price drops to the 1.3000-1.3050 range. We do not exclude an upward rebound to 1.3250 as the RSI on the 15-minute chart is signalling that the pair is oversold.

USD/CAD

The USD/CAD is growing confidently after a long consolidation near 1.2470. Currently the quotes reached resistance at 1.2550 and gaining a foothold above it may be a reason for further increases with immediate goals at 1.2665 and 1.2800. On the other hand, the trend may change to negative in the case of the price fixing below 1.2450.

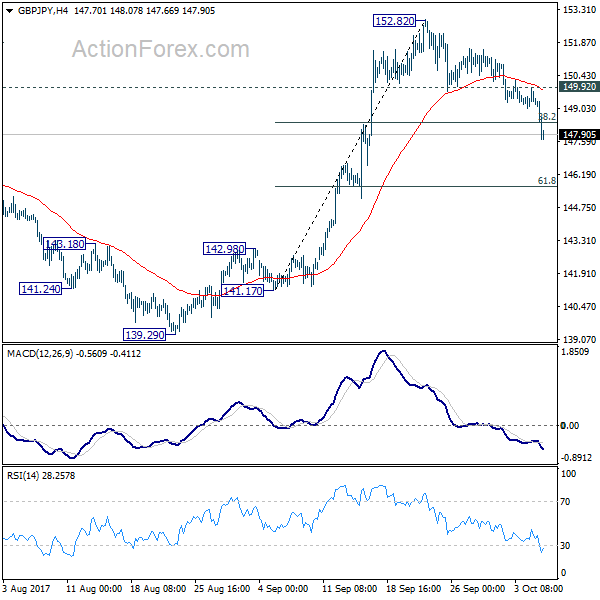

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.96; (P) 149.43; (R1) 149.83; More

GBP/JPY's decline from 152.82 accelerates lower and breaks 38.2% retracement of 141.17 to 152.82 at 148.36 firmly. The development argues that whole rise from 139.29 is completed. Intraday bias stays on the downside for 55 day EMA (now at 146.27). Sustained trading below there will bring retest of 139.29 key support level. On the upside, break of 149.92 minor resistance is needed to indicate completion of the fall. Otherwise, deeper decline will now remain in favor.

In the bigger picture, medium term rebound from 122.36 is in progress. Firm break of 38.2% retracement of 196.85 to 122.36 at 150.43 will carry long term bullish implications. In that case, GBP/JPY could target 61.8% retracement at 167.78. For now, the bullish scenario is preferred as long as 139.29 support holds.

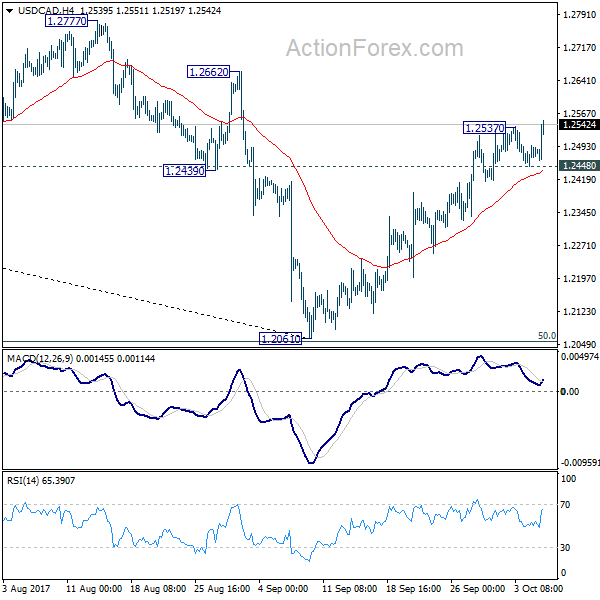

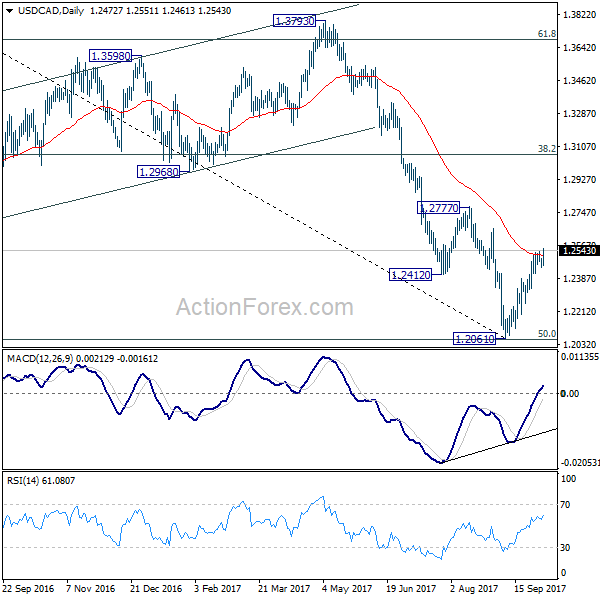

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2449; (P) 1.2474; (R1) 1.2499; More....

Break of 1.2537 suggests that rebound form 1.2061 has resumed. Intraday bias is back on the upside for 1.2777 resistance next. Decisive break there will target key medium term fibonacci level at target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. On the downside, below 1.2448 minor support will turn intraday bias neutral again.

In the bigger picture, current development argues that USD/CAD has defended 50% retracement of 0.9406 (2011 low) to 1.4869 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Break of 1.2777 will further affirm this bullish case. That is, larger up trend from 0.9406 is not completed. However, on the other hand, firm break of 1.2048 will indicate that fall from 1.4689 is at least a medium term down trend and should target 61.8% retracement at 1.1424 and below.

Pound Slides on Political Worries; Euro Weaker after ECB Minutes

The pound was the worst performing major currency in Thursday's European session as speculation mounted about whether the UK prime minister would resign. The euro also underperformed as the European Central Bank's September meeting minutes showed policymakers wanted to maintain a "highly accommodative" monetary policy once tightening gets underway. The US dollar meanwhile was broadly firmer after another batch of solid US data.

Fears about the possible resignation of British Prime Minister Theresa May were heightened today following a party conference speech on Wednesday that was marred by a series of mishaps. In what was meant to be a keynote speech aimed at uniting her party that has been gripped by infighting over Brexit and leadership, May's annual address to the Conservatives only contributed to talk of her departure. Also weighing on the pound were growing concerns that the UK is headed for a 'hard' Brexit amid lack of progress in the negotiations with the EU.

The pound fell to a near 4-week low of $1.3126, to stand 0.9% lower on the day in late European session. It was also sharply down against the euro and the yen. The single currency gained 0.6% versus sterling and was last up at 0.8926, while against the yen, the pound tumbled by more than 1% to a three-week low of 147.66.

The euro wasn't having a much better day either as dovish signals from the ECB and renewed threat of political instability dragged on the currency. The ECB's account of the September policy meeting indicated there was growing concern by Governing Council members about the appreciating exchange rate, which was creating "a source of uncertainty" and requires "close monitoring". The minutes confirmed policymakers had begun discussions on reducing the size of the asset purchases and that the bulk of the decisions will be made at the October meeting.

Governing Council member Ewald Nowotny further reinforced expectations of tighter policy in the coming months. In an interview for an Austrian magazine, Nowotny said "I assume that we will transition to a cautious deceleration at the start of the coming year".

Meanwhile in Spain, the situation in Catalonia showed no sign of deescalating. Spain's Constitutional Court today suspended the Catalan parliamentary session scheduled for Monday when the regional government was due to meet to decide on declaring independence.

The euro slid by about 0.4% to a session low of 1.1711 against the dollar and was down by 0.5% against the yen at 131.84.

The US dollar was stuck in a tight range against the yen today and saw only muted reaction to economic data out of the United States. Initial jobless claims fell from 272k to 260k in the week ending September 30, beating estimates of 265k. August trade data also surprised to the upside, with the deficit shrinking to $42.40 billion from $43.60 billion. It compares with forecasts of a deficit of $42.70 billion. Factory orders completed the hat trick as they rose by 1.2% month-on-month in August, surpassing expectations of a 1.0% increase and follows a 3.3% drop in the prior month.

The greenback was slightly down versus the yen at 112.62 at the start of US trading, but it's broader measure, the dollar index was firmer, climbing 0.4% to 93.83. The dollar index was lifted by hawkish comments from Fed officials.

Speaking to CNBC, Philadelphia Fed President Patrick Harker today repeated that he expects one more rate rise this year and three in 2018. This view on the rate hike path was shared by San Francisco Fed President John Williams, who said he still expects low unemployment to drive up wages, which should push up inflation.

In other currencies, the Australian and Canadian dollars were both lower against their US counterpart on Thursday. The aussie extended its Asian session losses to drop below the 0.78 handle following worse-than-expected retail sales figures out of Australia earlier in the day. It was last down 0.8% at $0.7798.

The Canadian dollar touched a five-week low as expectations of further rate hikes by the Bank of Canada this year continued to recede. Canada posted a much larger-than-forecast trade deficit in August of C$3.41 billion, further dampening sentiment on the loonie. The greenback was last up 0.5% at C$1.2538, with a jump in oil prices providing little boost for the loonie.

Oil prices surged by around 2% today after Russia and Saudi Arabia suggested that the current deal between OPEC/non-OPEC countries to cap output could be extended until the end of 2018. WTI crude rose was last trading at $50.91 a barrel, while Brent crude was at $56.89 a barrel.