Sample Category Title

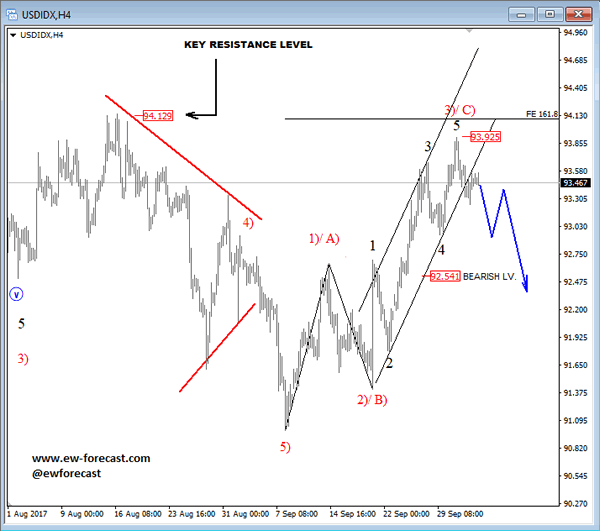

Elliott Wave Analysis: USD Index Can Face A Reversal

USD Index touched levels near the 93.92 level and later made a new intra-day drop lower. This intra-day fall can now be an early indication of a completed three-wave recovery and more weakness to follow. If that is the case and price breaches below the 92.54 level then we would be certain that more weakness will follow and that price completed a three-wave recovery. A decisive breach below the lower channel line would also be a confirmation for a change in trend.

USD Index, 4H

Market Update – European Session: Hard Brexit Concerns Resurface, Spain Bond Auction Results Seen As ‘Solid’

Notes/Observations

UK Tory Party conference failed to unify the party

Catalonia threatens to declare independence next week; Central govt assures it won’t happe

Spain's launch of a new five-year government bond prompted solid demand

Overnight

Asia:

Australia Aug Retail Sales miss expectations (M/M: -0.6% v +0.3%e)

Shanghai Composite and Korea Kospi remained closed for Golden Week; Hang Seng closed for holiday as well

Europe:

Spain region Catalan govt President Puigdemont stated that was obliged to apply the results of the independence referendum; to seek a mediation process. Catalonian Govt to discuss the outcome of region’s referendum in an extraordinary session on Monday, Oct 9th

Spanish PM Rajoy said to be threatening to trigger Article 155 of the constitution which allowed the central government to force a region to obey laws when disobedience “gravely threatened the general interest of Spain.” 155 had never been used.

S&P rating agency placed Catalonia B+/B ratings on CreditWatch negative; saw risk that escalation with Spain’s govt might damage the coordination and communication between the two govts which was essential for Catalan to service its debt on time and in full

Over two dozen UK members of parliament said to be prepared to call for PM May to resign; could be out of office before end of year

Americas:

Sec of State Tillerson refutes press specuklation that he might resign. Stated that he was committed to the President and the country

US Senate advanced nomination of Randall Quarles to be member of Fed Board of Governors with vote next Thursday, Oct 12th (**Reminder: Fed Vice Chair Fischer to step down on or around Oct 13th)

Economic data

(NL) Netherlands Sept CPI M/M: -0.2% v +0.2%prior; Y/Y: 1.6% v 1.5%e

(NL) Netherlands Sept CPI EU Harmonized M/M: -0.4% v +0.2%prior; Y/Y: 1.4% v 1.7%e

(IN) India Sept PMI Services: 50.7 v 47.5 prior (1st expansion in 3 months); PMI Composite: 51.1 v 49.0 prior

(CH) Swiss Sept CPI M/M: 0.2% v 0.2%e; Y/Y: 0.7% v 0.6%e

(CH) Swiss Sept CPI EU Harmonized M/M: +0.2% v -0.1% prior; Y/Y: 0.8% v 0.5% prior

(SE) Sweden Aug Industrial Production M/M: -1.7% v -0.3%e; Y/Y: 7.3% v 10.0%e

Fixed Income Issuance:

(ES) Spain Debt Agency (Tesoro) sold total €4.3B vs. €3.75-4.5B indicated range in 2022 and 2029 bonds

Sold €3.21B in new 0.45% Oct 2022 SPGB; Avg yield: 0.530% v 0.213% prior, Bid-to-cover: 2.12x v 1.88x prior

Sold €1.09B in 6.0% Jan 2029 SPGB; Avg Yield: 1.867% v 1.880% prior, bid-to-cover: 2.5x v 1.67x prior

(ES) Spain Debt Agency (Tesoro) sold €304M vs. €250-750M indicated range in 1.80% Nov 2024 I/L bonds (Bonoei/SPGbi); Real Yield: -0.520% v 0.113% prior; Bid-to-cover: 3.2x v 1.99 prior

(FR) France Debt Agency (AFT) sold total €8.498B vs. €7.5-8.5B indicated range in 2025, 2028 and 2048 Oats

Sold €2.735B in 1.00% Nov 2025 Oat; Avg Yield: 0.46% v 0.64% prior; Bid-to-cover: 1.99x v 2.34x prior

Sold €4.00B in 0.75% May 2028 Oat; Avg Yield: 0.88% v 0.67% prior; Bid-to-cover: 1.85x v 1.99x prior

Sold €1.765B in 2.00% May 2048 Oat; Avg Yield: 1.82% v 1.79% prior, Bid-to-cover 1.78x v 1.57x prior

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 -0.3% at 389.3, FTSE +0.1% at 7477, DAX -0.2% at 12940, CAC-40 -0.1% at 5359, IBEX-35 +0.4% at 10005, FTSE MIB -0.1% at 22429, SMI -0.3% at 9254, S&P 500 Futures flat]

Market Focal Points/Key Themes: European indices open down but reverse course as the session progressed; banking shares underperform while utilities supported; markets getting used to uncertainty in Catalonia and peripherals return to positive; Israel closed for holiday; attention turning to ECB minutes to be released later today and tomorrow's release of NFP in the US; earnings releases in the upcoming US session include Constellation Brands and Costco.

Equities

Consumer discretionary: DFS Furniture DFS.UK -4.3% (results), Norwegian Air NAS.NO -3.1% (traffic data), Scout24 G24.DE -0.4%(stake sale)

Industrials: Assa Abloy ASSAB.SE -4.8% (CEO considering resignation), Evonic EVK.DE +1.2% (analyst action), Technotrans TTR1.DE -2.1% (analyst action)

Financials: Credito Valtellinese CVAL.IT -9.2%(analyst action)

Technology: Osram Licht OSR.DE -0.7% (Stake sale)

Telecom: Telecom Italia TIT.IT +2.5% (potential asset sale)

Healthcare: Cosmo Pharmaceuticals +3.1% (FDA NDA approval), TiGenix TIG.BE 1.5% (study results)

Energy: Electricite de France EDF.FR +4.3% (analyst action)

Speakers

SNB President Jordan: Inflation remained very, very weak; need to continue with current monetary policy of negative rates and FX intervention pledge. Forex market remained fragile; CHF currency (Franc) remained strong

ECB’s Praet (Belgium): Sustainable convergence needed for Euro adoption

UK govt stated that resignation of PM May was not an issue (refutes recent press concerns)

Italy Stats Agency (Istat) Monthly Economic Note: Domestic growth picking up aided by manufacturing and investment

Spain Fin Min De Guindo: Catalonia independence will NOT happen, independence was irrational would be very harmful for Catalonia. Spain govt will enforce the law perfectly. Reiterated view that Catalan banking sector was solvent but banks could leave region if process goes further

Germany BDI Industry Association: Looking with concern at current Brexit negotiations. British govt lacking clear concept despite a lot of talk. German companies with presence in UK must make provision for the possibility of a hard Brexit

Turkey President Erdogan: Those who open the way for Kurdish referendum will pay

Turkey Dep PM Simsek: Monetary policy has been tight since Q4 2016 and would continue to be so. Saw CPI under 10% by end of 2017 (**Note: Sept YoY reading was 11.2%)

Japan PM Abe adviser Hamada: Supports planned timeline of planned hike in sales tax

Currencies

GBP exhibited weakness. Some dealers attributed its tone to reports that over two dozen UK members of parliament were prepared to call for PM May to resign before the end of 2017. Also the focus returned to the state of Brexit negotiations after Tory Party conference was now out of the way. Germany BDI Industry Association noted that it had concern at current Brexit negotiations and added that German companies with presence in UK must make provision for the possibility of a hard Brexit

EUR/USD was steady despite Spain region of Catalonia threatening to declare independence next week. Analysts noted that should Catalonia turn independent, the EU would have to apply the ‘Prodi doctrine’ from 2004, suggesting Catalonia would leave the EU and the Eurozone

Fixed Income

Bund futures trades at 161.29 down 3 ticks, recovering from early losses filling the morning gap to 161.13 after a well received Spanish auction. A move back lower paves the way to 160.65 base, while continued momentum higher sees 161.40.

Thursday's liquidity report showed Wednesday's excess liquidity rose to €1.787T from €1.778T prior. Use of the marginal lending facility rose to €615M from €344M.

Corporate issuance saw $4.5B come to market via 5 issuers bringing week to date issuance to above $11B. Issuance was headlined by BNS $1.25B issuance and Braskem $1.75B 2 part offering.

Looking Ahead

05:30 (ZA) South Africa Sept SACCI Business Confidence: No est v 89.6 prior

05:30 (UK) DMO to sell £2.75B in 0.75% July 2023 Gilt

05:30 (HU) Hungary Debt Agency (AKK) to sell 12-month Bills

05:30 (HU) Hungary Debt Agency (AKK) to sell Floating Bonds

06:00 (IE) Ireland Sept Live Register Monthly Change: No est v -7.3K prior

06:00 (IE) Ireland Aug Industrial Production M/M: No est v 1.8%; Y/Y: No est v -9.5% prior

06:45 (US) Daily Libor Fixing

07:00 (ZA) South Africa Aug Electricity Production: No est v-1.8% prior; Electricity Consumption Y/Y: No est v -1.5% prior

07:30 (US) Sept Challenger Job Cuts: No est v 33.8K prior; Y/Y: No est v 5.1% prior

07:30 (EU) ECB account of the monetary policy meeting (Sept Minutes)

07:30 (CL) Chile Aug Economic Activity Index (Monthly GDP) M/M: 0.7%e v 0.9% prior; Y/Y: 2.1%e v 2.8% prior

08:00 (CL) Chile Aug Nominal Wage M/M: No est v 0.6% prior; Y/Y: No est v 5.8% prior

08:05 (UK) Baltic Dry Bulk Index

08:15 (FR) ECB’s Coeure (France) on panel in Frankfurt

08:30 (US) Initial Jobless Claims: 265Ke v 272K prior; Continuing Claims: 1.95Me v 1.934M prior

08:30 (US) Aug Trade Balance: -$42.7Be v -$43.7B prior

08:30 (CA) Canada Aug Int'l Merchandise Trade (CAD): -2.7Be v -3.0B prior

08:30 (US) Weekly USDA Net Export Sales

09:00 (MX) Mexico Sept Consumer Confidence: 86.0e v 88.5 prior

09:00 (RU) Russia Gold and Forex Reserve w/e Sept 29th: No est v $427.1B prior

09:00 (RU) Russia Sept CPI data

09:10 (US) Fed’s Powell (voter, neutral)

09:15 (US) Fed’s Williams (non-voter)

10:00 (US) Fed’s Harker (voter, hawk) at conference

10:00 (US) Aug Final Durable Goods Orders: 1.7%e v 1.7% prelim; Durables Ex Transportation: 0.2%e v 0.2% prelim

10:00 (US) Aug Factory Orders: +1.0%e v -3.3% prior; Factory Orders (Ex Transportation): No est v 0.5% prior

10:30 (US) Weekly EIA Natural Gas Inventories

11:00 (US) Treasury announcement for upcoming issuance during week of Oct 9th (3-year, 10-year and 30-year bonds)

12:00 (UK) BOE’s McCafferty

13:30 (UK) BOE’s Haldane (chief economist)

15:00 (MX) Mexico Citibanamex Survey of Economists

16:30 (US) Fed’s George (non-voter, hawk) at conference

CRUDE OIL Declining Towards $50

Crude oil is pushing lower towards $50 level. Key support is given at 45.40 (17/08/2017 high). Strong resistance found at 52.43 (26/09/2017) has been broken. Expected to show continued weakness.

In the long-term, crude oil has recovered after its sharp decline last year. However, we consider that further weakness are very likely. Strong support lies at 35.24 (05/04/2016) while resistance can now be found at 55.24 (03/01/2017 high).

SILVER Selling Pressures

Silver is weighing down. Hourly resistance is given at 16.89 (04/10/2017 high) while hourly support can be found at 16.54 (04/10/2017 high). Expected to show further bearish move.

In the long-term, the trend is rater negative. Further downsides are very likely. Resistance is located at 25.11 (28/08/2013 high). Strong support can be found at 11.75 (20/04/2009).

GOLD Bouncing Higher On Strong Support

Gold is monitoring hourly support given at 1267 (15/08/2017 low). Hourly resistance is located at 1357 (08/09/2016). Stronger support lies at 1204 (10/07/2017 high). Expected to show further monitoring of support at 1267.

In the long-term, the technical structure suggests that there is a growing upside momentum. A break of 1392 (17/03/2014) is necessary ton confirm it, A major support can be found at 1045 (05/02/2010 low).

BITCOIN Declining Within Uptrend Channel

Bitcoin is still on a strong momentum despite ongoing consolidation. Strong support is given at 2975 (22/08/2017 low). Sell walls around $4000 have been broken. Key resistance can be located at 4921 (01/09/2017 high). The road is wide open for further increase.

In the long-term, the digital currency has had an exponential growth. There are decent likelihood that the asset will reach $10'000.

EUR/CHF Breaking Short-Term Uptrend

EUR/CHF has exited bearish downtrend. Yet momentum is not strong at the moment. Strong resistance is now at 1.1623 (22/09/2017 high). Downside risk is very likely.

In the longer term, the technical structure has reversed. Strong resistance is given at 1.20 (level before the unpeg). Yet, the ECB's QE programme is likely to cause persistent selling pressures on the euro, which should weigh on EUR/CHF. Supports can be found at 1.0184 (28/01/2015 low) and 1.0082 (27/01/2015 low).

EUR/GBP Bullish Breakout

EUR/GBP has isurged. The pair has broken the resistance at 0.8899 (19/09/2017 low), the shortterm technical structure is biased to the downside. Hourly support is given at 0.8746 (27/09/2017).

In the long-term, the pair has largely recovered from recent lows in 2015. The technical structure suggests a growing upside momentum. The pair is trading above from its 200 DMA. Strong resistance can be found at 0.9500 (psychological level).

AUD/USD Ready To Test Strong Support

AUD/USD is consolidating over the past weeks. Hourly resistance is given at 0.7883 (27/05/2017 high). The pair is approaching support at 0.7786 (18/07/2017 low). Expected to show continued consolidation.

In the long-term, the trend is turning positive. Key supports stands at 0.6009 (31/10/2008 low) . A break of the key resistance at 0.8164 (14/05/2015 high) is needed to invalidate our long-term bearish view.

USD/CAD Bullish

USD/CAD continues to move higher despite ongoing consolidation. Strong support is located at a distance 1.2062 (08/09/2017 low). Hourly support lies at 1.2331 (26/09/2017 high). Resistance is given at 1.2532 (29/09/2017 high). Expected to show continued short-term bullish pressures.

In the longer term, the pair has broken longterm support that can be found at 1.2461 (16/03/2015 low). Strong resistance is given at 1.4690 (22/01/2016 high