Sample Category Title

EURUSD Lower on Stronger Greenback; ECB Minutes

The Euro slipped from the session high at 1.1778, after recovery attempts repeatedly stalled on approach to falling 10SMA which marks significant barrier.

Stronger dollar in mid-European session and release of ECB minutes helped bears to push the single currency lower.

Minutes showed that the ECB policymakers discussed various scenarios for extension of QE program into next year and also expressed concerns about Euro's rise.

Policymakers need to decide about asset purchase program which expires at the end of the year, as main argument was about the size and duration of QE extension.

Two solutions were on the table: smaller QE cut with shorter duration or bigger reduction with longer duration.

Regarding the monetary policy, it should be highly accommodative under all scenarios.

Final decisions are likely to be made on ECB's policy meeting on October 26.

The Euro stands at the back foot ahead of beginning of the US session and release of US Jobless Claims and Trade Balance data.

Fresh weakness surged below hourly cloud (1.1759/1.1738) but was so far unable to sustain losses below cloud base.

Bearish setup of daily techs favors further downside and renewed attack at 1.1720 pivot, break of which will be seen as bearish signal.

US data are also expected to impact performance of EURUSD pair.

Res: 1.1778; 1.1790; 1.1816; 1.1832

Sup: 1.1734; 1.1720; 1.1696; 1.1662

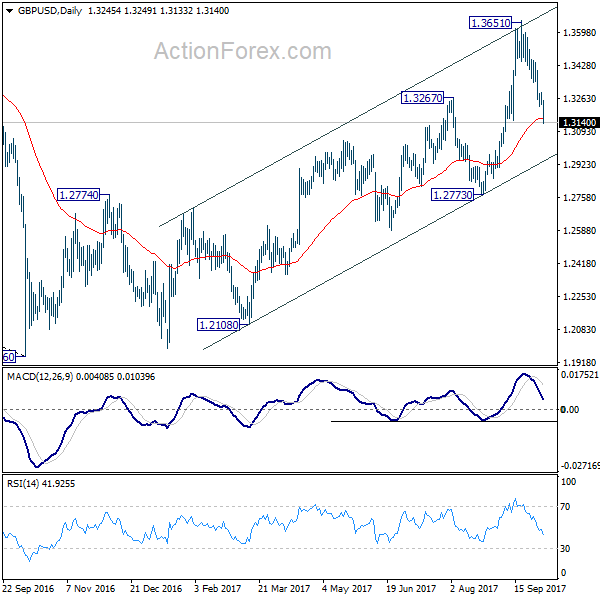

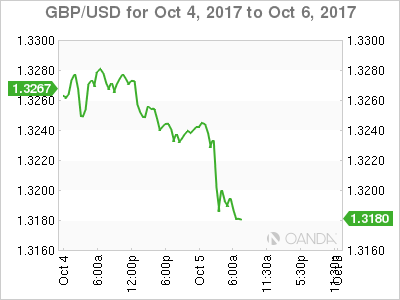

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3218; (P) 1.3254; (R1) 1.3285; More....

GBP/USD's fall extends to as low as 1.3133 so far. Intraday bias remains on the downside for 61.8% retracement of 1.2773 to 1.3651 at 1.3108. Firm break there will target a test on 1.2773 key support it's still early to call for trend reversal as it's staying well inside medium term channel. But a break of the channel support (1.2942) will build up the chance of the bearish case. On the upside, above 1.3221 minor support will turn intraday bias neutral first.

In the bigger picture, current development argues that the long term trend in GBP/USD has reversed. That is, a key bottom was formed back in 1.1946 on bullish convergence condition in monthly MACD. Current rise from 1.1946 will target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 next. In any case, medium term outlook will now stay bullish as long as 1.2773 support holds.

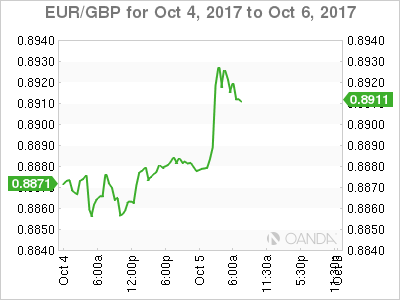

Sterling Selloff Accelerates on Talks that May May be Ousted

Fresh, broad based selling is seen in Sterling today and the currency staying as the weakest one for the week. Political uncertainty seems to be a main driver. Talks of UK Prime Minister Theresa May being ousted by her own party members surface. That comes after May's keynote speech at the Conservative Party Conference yesterday. And the occasion was overshadowed by her coughing as a prankster storming the stage.

It's reported that some Tory MPs want May to quit. However, the underlying split down the middle of the party is seen as the more serious problem. A clear representation of the division is the conflicting messages from ministers regarding UK's Brexit position. And that leads to a lack of position which has been heavily criticized by EU officials.

Meanwhile, markets could be reassessing BoE outlook after a string of weaker than expected data released this week. This is no change in the expectation for BoE to hike in November. And, the central bank will continue to do so barring any disasters. However, a 25bps hike would just bring interest rate back to pre-Brexit referendum level. BoE will very likely stop there afterwards, until the Brexit picture becomes clearer.

ECB account showed discussion on policy adjustment started

The account of ECB's September 6-7 monetary policy meeting showed that policymakers kicked start the discussion on adjustment of policies after the current asset purchase program ends in December. And, "a view was put forward that conditions were increasingly falling into place that would allow the intensity of monetary policy accommodation to be adapted and would provide an opportunity to scale back the Eurosystem's net asset purchases."

The account also noted that there were discussions on "general trade-offs inherent in various scenarios for the future recalibration of the APP and, in particular, the choice between the pace and the intended duration." It added that, "the benefits from a longer intended purchase horizon, combined with a greater reduction in the pace, were compared with those from a shorter period of purchases and larger monthly volume."

Still, the account emphasized that "any reassessment of the monetary policy stance should proceed in a very gradual and cautious manner, while maintaining sufficient flexibility." And there was "broad agreement" among ECB officials that substantial accommodation is still needed. Also, "discomfort was widely expressed about the very prolonged period over which inflation had been -- and was still expected to remain -- distant from the Governing Council's aim."

Released from Eurozone, retail PMI rose to 52.3 in September. Also from Europe, Swiss CPI climbed to 0.7% yoy in September.

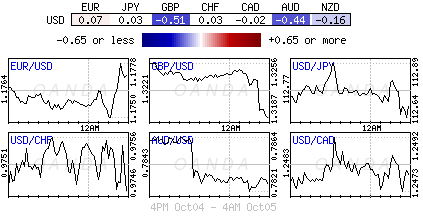

Dollar firm but lacks decisive momentum

Dollar is trading generally firm, except versus Yen. But there is still no follow through buying in the greenback yet. Traders seem to be holding their bets ahead of non-farm payroll report tomorrow. In addition, the lack of decision from US President Donald Trump on the next Fed chair could be rather unsettling. adding to that, there is no more news regarding Trump's tax plan, which he targets to get through Congress by the end of the year. Release from US, initial jobless claims dropped 12K to 260K in the week ended September 30. Trade deficit narrowed to USD -42.4B in August. Canada trade deficit widened to USD -3.4B.

Yen rebounding, looking forward to Oct 22 election

Yen is picking up momentum for a more sustainable rebound as traders are starting to turn cautious. And, volatility in Japanese financial markets is set to intensify as the snap election for the parliament (Lower House), scheduled on October 22, approaches. Our base case is that PM Shinzo Abe's LDP would remain the biggest party. He would continue to be the leader of the LDP/Komeito coalition in the new term. However, the rapid rise of the new party Kibo no To (Party of Hope), led by Tokyo Governor Yuriko Koike, might result in a decrease in number of seats for LDP. This, together with the decline in Abe's approval rating, has created much uncertainty in the upcoming election. More in Japan's Snap Election And The Impacts On Policies.

Aussie lower after worse retail sales contraction in four years

Australian Dollar trades mildly lower today after disappointing retail sales, that contracted -0.6% mom in August, much worse than expectation of 0.3% mom rise. That's also the steepest decline in more than four years. Also, the contraction is broad-based, as sales dropped in every state and territory across the country. The sluggish sales is seen partly a result of poor wage growth in the job market, and partly due to high household debt level. Also from Australia, trade surplus widened to AUD 0.99B in August, above expectation of AUD 0.87B. Exports grew 1% to AUD 32.2B while imports were flat at AUD 31.2B. The trade data was somewhat also consistent with retail sales, suggesting weak domestic demand growth. That's seen as one of the major reasons for RBA to stand pat while global central banks are exiting stimulus.

Staying in Australia, former RBA board member John Edwards warned that "very low interest rates at a time of firm economic expansion invite trouble." And, there is "too great a risk that the price of assets like houses and shares may get too far out of whack with what prove to be sustainable levels." Then he pointed to Australia 10 year bond year at around 2.6%, 1.1% above the cash rate. The long-term average premium sits at 0.8%. So, "there is perhaps some allowance for a rise in the cash rate over the ten years of the bond, but not much."

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3218; (P) 1.3254; (R1) 1.3285; More....

GBP/USD's fall extends to as low as 1.3133 so far. Intraday bias remains on the downside for 61.8% retracement of 1.2773 to 1.3651 at 1.3108. Firm break there will target a test on 1.2773 key support it's still early to call for trend reversal as it's staying well inside medium term channel. But a break of the channel support (1.2942) will build up the chance of the bearish case. On the upside, above 1.3221 minor support will turn intraday bias neutral first.

In the bigger picture, current development argues that the long term trend in GBP/USD has reversed. That is, a key bottom was formed back in 1.1946 on bullish convergence condition in monthly MACD. Current rise from 1.1946 will target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 next. In any case, medium term outlook will now stay bullish as long as 1.2773 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Trade Balance (AUD) Aug | 0.99B | 0.87B | 0.46B | 0.81B |

| 00:30 | AUD | Retail Sales M/M Aug | -0.60% | 0.30% | 0.00% | -0.20% |

| 07:15 | CHF | CPI M/M Sep | 0.20% | 0.20% | 0.00% | |

| 07:15 | CHF | CPI Y/Y Sep | 0.70% | 0.60% | 0.50% | |

| 08:10 | EUR | Eurozone Retail PMI Sep | 52.3 | 50.8 | ||

| 11:30 | USD | Challenger Job Cuts Y/Y Sep | -27.00% | 5.10% | ||

| 12:30 | CAD | International Merchandise Trade (CAD) Aug | -3.4B | -2.7B | -3.0B | |

| 12:30 | USD | Initial Jobless Claims (SEP 30) | 260K | 263K | 272K | |

| 12:30 | USD | Trade Balance Aug | -42.4B | -43.0B | -43.7B | -43.6B |

| 14:00 | USD | Factory Orders Aug | 0.90% | -3.30% | ||

| 14:30 | USD | Natural Gas Storage | 58B |

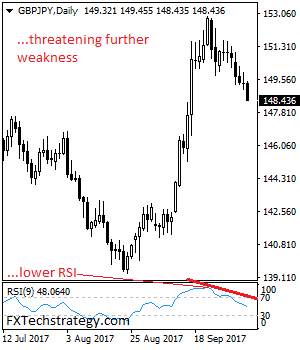

GBPJPY – Bears Accelerate on Political Concerns

The cross slumped in Europe on Thursday and hit three week low near 148.00 handle, as rising political concerns over PM May's position hit pound across the board.

Bears are looking for target at 147.67 (Fibo 38.2% of 139.30/152.85 rally) and could move further down on extension of current third wave of five-wave sequence from 152.85, towards its FE 138.2% at 147.03.

Meanwhile, bears may take a breather ahead of 147.67 target as near-term studies are oversold.

Broken 20SMA now acts as good resistance at 149.17 and should ideally cap corrective rallies.

Res: 148.70; 149.17; 149.45; 150.00

Sup: 148.00; 147.67; 146.51; 147.03

GBP Lower on Speculation over Theresa May’s Position

- Are we on course for a perfect week for US indices?

- GBP lower on speculation over Theresa May's position;

- Four Fed policy makers scheduled to speak;

- ECB minutes get muted response.

US futures are indicating a slightly higher open on Wall Street on Thursday, as indices target a fourth consecutive record close this week.

Sterling is coming under pressure again this morning following speculation that Theresa May's position is increfasingly under threat following yesterday's shambolic speech at the Conservative party conference. A change of leadership so soon after the election and just as Brexit talks appear to be making some progress may seem like a ludicrous idea but a leadership challenge has been brewing since the disastrous election campaign and yesterday was just the icing on the cake.

It seems more a matter of when rather than if a challenge will come. You get the feeling that those below her gunning for her job are simply biding their time, waiting for the opportune moment rather than fully throwing their support behind her. Naturally, all of this uncertainty is not good for the pound, especially as a change of leadership will likely alter the direction of the Brexit negotiations which have already progressed at a much slower pace than hoped.

The pound will likely remain in focus today, with speeches from Bank of England policy makers Ian McCafferty and Andy Haldane still to come. While McCafferty is a known hawk and already in favour of raising interest rates, Haldane has previously sided with the majority but has shown a willingness to jump ship. Should he indicate today that he's tempted to do so at the November or December meetings, we could see the pound rally once again.

We'll also hear from four Federal Reserve policy makers throughout the course of the day, including one of the leading candidates for the Fed Chair post, Jerome Powell. With the Fed having indicated at the last meeting that it still intends to raise interest rates again this year, it will be interesting to hear whether the data since then has changed this view or whether the same still applies. Jobless claims, trade data and factory orders make up today's economic releases, although traders will be more focused on tomorrow's jobs report.

The ECB minutes from the last meeting received a somewhat muted response in the markets. The minutes effectively reiterated points already made in the statement and during Mario Draghi's press conference, including how they will manage the QE programme beyond the end of the year – albeit without any indication of what the preferred method is – and a reference to the difficulty that the FX rate poses. The lack of a reaction is unsurprising as the minutes were quite clearly carefully worded to generate such a response and leave little to be interpreted, or more importantly, misinterpreted.

GBPJPY – Bearish, Retains Its Downside Pressure

GBPJPY - The cross remains vulnerable to the downside on further weakness as it retains its bearish bias. On the downside, support comes in at the 148.00 level where a violation will aim at the 147.50 level. A break below here will target the 147.00 level followed by the 146.50 level. Conversely, resistance is seen at the 149.00 level followed by the 149.50 level. A cut through that level will set the stage for a move further higher towards the 150.00 level. Further out, resistance resides at the 150.50 level. All in all, GBPJPY remains weak and vulnerable to the downside.

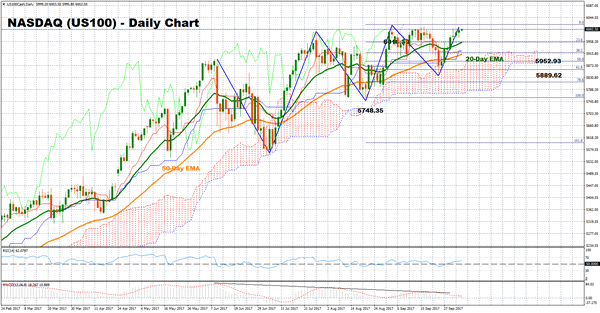

US100 Stock Index Bullish In Short- And Medium-Term, Positive Momentum Though Weakens

The tech-heavy US100 index is currently trying to post another green candle around record high levels, stretching its upleg started on September 26. The outlook in the short- and medium-term remains bullish based on oscillator signals. However, momentum has slowed down, hinting to softer upside movement in the short-term.

The RSI has entered bullish territory above 50 at the end of September and is currently positively sloped, suggesting a bullish picture in the short-term. The MACD is also above zero and its signal line but the fact that it has been making lower highs since June highlights that the index might be losing steam. This could also be seen from the last recorded top not being far above the previous peak. Additionally, the Kijun-sen recently moved below Tenkan-sen; this being a negative alignment.

A break above the previous September 1 high of 6016.30 would confirm the continuation of the long-term uptrend and the posting of new record highs. Further extensions would target the 6100 psychological level before the 6200 key mark comes into view.

If the index retreats, support could be first found around the 23.6% Fibonacci point of the upleg from 5748.38 to 6016.30 (August 21- September 1) at 5952.93 which is also where the 20-day exponential moving average (EMA) lays. Next, the focus would shift to the 50% Fibonacci at 5889.62 with the outlook turning to neutral in case the index violates that point. Further declines would turn the attention to the August 21 low of 5748.35 which is also near the bottom of the Ichimoku cloud.

In the medium-term, the outlook remains positive as long as the bullish cross between the 20-day EMA and the 50-day EMA remains in place.

Japan’s Snap Election And The Impacts On Policies

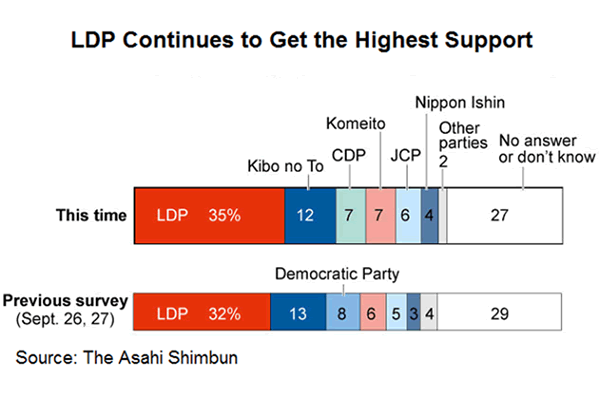

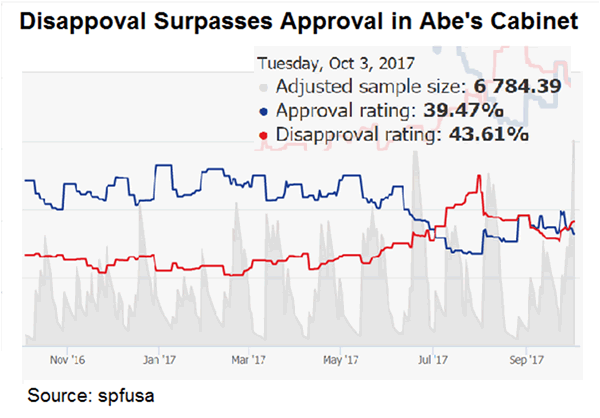

Volatility in Japanese financial markets is set to intensify as the snap election for the parliament (Lower House), scheduled on October 22, approaches. Our base case is that PM Shinzo Abe's LDP would remain the biggest party. He would continue to be the leader of the LDP/Komeito coalition in the new term. However, the rapid rise of the new party Kibo no To (Party of Hope), led by Tokyo Governor Yuriko Koike, might result in a decrease in number of seats for LDP. This, together with the decline in Abe's approval rating, has created much uncertainty in the upcoming election.

Electoral Platform: LDP vs Party of Hope

Party of Hope's draft platform, announced on October 5, focuses on following areas: 1) Constitutional amendment, 2) Phase out of nuclear power, 3) Freeze of the consumption tax increase, 4) Enhancement of national security 5) Reduction of the number of Diet members and their annual allowances, 6) Economic growth through loosened regulations, 7) Education and welfare, 8) Diversity in society, and 9) Decentralization of power.

Constitutional Amendment and Revision of Article 9

As former allies (Koike served as defence minister during Abe's first term as prime minister), Abe and Koike are both categorized as conservative and populist. They are in support of constitutionals amendment, including the most sensitive issue of the war-renouncing Article 9

LDP in its election pledge unveiled the intention to revise the Constitution in four areas. Among which the most sensitive is clarification of the legal status of the self-defence force (SDF) in Article 9. Acknowledging the controversy of this proposal, Abe announced that his party also proposes to keep the first and second paragraphs* unchanged.

Party of Hope also proposes discussions on revising Article 9, possibly allowing the country to exercise its right to collective self defense when it is required in the actual situation.

*Article 9: 1. Aspiring sincerely to an international peace based on justice and order, the Japanese people forever renounce war as a sovereign right of the nation and the threat or use of force as a means of settling international disputes. 2. In order to accomplish the aim of the preceding paragraph, land, sea and air forces, as well as other war potential, will never be maintained. The right of belligerency of the state will not be recognized.

Consumption Tax and Nuclear Power

Indeed, the biggest divisions are on consumption tax and nuclear power. Abe calls for raising the consumption tax rate to 10% from 8% in October 2019. Rather than using the revenue to repay debts, he proposes to allocate the spending on free education and social welfare. Koike, however, proposes to freeze the increase in the consumption tax. She believes a tax hike would suffocate domestic demand growth which has been sluggish. Nuclear power would continue to be key energy source under the leadership of LDP. As indicated in the election pledge, LDP noted that it would restart nuclear power reactors that have confirmed to be safe, after getting consensus from local government. By contrast, Koike's Party of Hope plans to completely end on nuclear power by 2030 while increasing the share of renewable energy to 30%.

Impact of Monetary and Fiscal Policies

Abe noted that it would be considered as victory if the LDP/Komeito could get the majority of seats. Indeed, opinion polls continue to suggest so despite the dropping approval rate of the prime minister. Note at the current parliament, LDP has secured 287 out of 475 seats. Together with Komeito's 35 seats, the coalition government has dominated over two-third of the parliament. This is sufficient to propose constitutional change and reapprove bills rejected by the House of Councilors (Upper House). The number of seats in the next parliament is reduced to 465. As such, 233 seats are sufficient for a majority and 310 seats for two-third. We doubt if Abe could retain his grip on power if he ends up losing 89 (287+35-233) seats to barely secure the majority.

Below we consider three possible outcomes and see how they would affect Japan's monetary and fiscal policy outlooks.

1. LDP/Komeito Majority with Abe as PM (Status Quo)

BOJ would maintain the existing accommodative monetary policy. Abe would continue to push his three arrows in the Abenomics. One of which is aggressive monetary easing. Haruhiko Kuroda would also stay as the central bank head as he was handpicked by Abe, thanks to his dovish stance. Consumption tax would increase in 2019 under Abe's leadership. As he promised, educational and socal welfare spending would rise. Moreover, the second arrow in Abenomics is robust fiscal policy, i.e. the government increases spending to stimulate the economy.

2. LDP/Komeito Majority with new PM

If Abe has to step down, his successor would determine the monetary and fiscal policy stances. The media has identified that Taro Aso, Yoshihide Suga, Fumio Kishida and Shigeru Ishiba as potential candidates. We expect the monetary policy would largely remain accommodative no matter who becomes the new PM. However, the fiscal policy might differ. Aso, Kishida and Ishiba propose fiscal adjustment while Suga advocates bold fiscal policy. Aso, at his capacity as the deputy PM and finance minster, warned last month that the government needs to maintain its efforts to achieve fiscal consolidation on soaring debts. Meanwhile, Ishida indicated that a primary fiscal surplus is a must. Chief Cabinet Secretary Suga believes the current fiscal policy is aimed at boosting economic growth and raising tax revenue.

3. Coalition of Party of Hope and other Smaller Parties

This scenario brings very high uncertainty to Japan's outlook. Koike has yet to reveal her platform on the monetary policy. Yet, judging from her aim to 'rest' Japan, it is possible that she might prefer a less accommodative monetary policy. Indeed, she suggested on September 25 that it is a 'mistake' to rely on monetary policy alone. On the fiscal front, she objects a consumption tax hike. The party has yet to announce more details on the fiscal policies.

Abe called the snap election when his popularity was at peak, hoping to have a landslide victory with increase in the number of seats. This wishful thinking is reminiscent of what UK PM Theresa May did in June. However, Conservatives eventually lost the majority in the election, amidst the surging support of the Labor Party. In Japan, support for the LDP remains the highest despite the decline after Abe's announcement of the snap election. It is also surprising as the Party of Hope has managed to secure over 10% of support, given this party was launched last week. We expect Japanese market volatility would be high as we approach the election day. Investors fear uncertainty. As we witnessed in the elections (France, UK Germany, New Zealand) so far this year, the country's currency fall if uncertainty increase and investors become more risk-averse. We might see some difference in this time. As a safe-haven currency, Japanese yen rises during time of risk aversion.

Expect U.S Jobs To Be Affected By Summer Hurricanes

Thursday October 5, 2017: Five things the markets are talking about

The U.S. dollar continues to fluctuate against the major currencies as investors pause ahead of tomorrow's North American jobs data. Minimal non-farm payroll (NFP) risk is being priced in to USD majors, as seasonal factors and recent hurricanes may give the data less credence.

One in 13 U.S workers are employed in counties ravaged by this summer's hurricanes in Florida and Texas.

Yet, any signs of solid U.S jobs growth will help justify an additional interest-rate increase by the Fed again this year. The U.S economy added +156k jobs in August while the unemployment rate held at +4.4%.

Note: The median forecast for tomorrow's release is a +80k gain in NFP, less than half the average +182k rise since the start of last year.

Fed fund futures is pricing in a +78% probability that the Fed will hike interest rates by the end of the year, up from around +44% last month.

Elsewhere, elections in the eurozone have rattled currency markets recently. The EUR (€1.1774) outright trades atop of this week's intraday low after an illegal independence vote in the Spanish province of Catalonia took place on the weekend. The prospect of secession has increased pressure on PM Rajoy while rattling Spanish markets.

Note: That came a week after the ‘single unit' was jarred by German Chancellor Merkel's conservative alliance losing ground in the federal election. Austria's legislative election this month (Oct 15) and Italian elections expected to be held by May 2018 could also raise risks for the EUR.

Investors are also watching for developments as President Trump considers replacing Fed Chairwoman Janet Yellen. The U.S administration has interviewed former Fed governor Warsh and Fed governor Powell about taking the helm at the Fed.

1. Stocks stay close to home

Japan's Nikkei share average ended little changed (-0.1%) overnight after hitting a two-year high Wednesday – investors remain cautious ahead of tomorrows U.S data. The broader Topix fell -0.1%.

Note: The Shanghai Composite and Korea Kospi remained closed for Golden Week, while the Hang Seng was closed for a holiday.

Down-under, Australia's S&P/ASX 200 slipped -0.1%, pressured by financial and energy shares.

In Europe, regional bourses are little changed with banking shares underperforming while utilities are supporting. Investors seem to be getting used to uncertainty in Catalonia as peripherals return to positive.

Note: Market attention is turning to ECB minutes to be released at 07:30 am EDT and tomorrow's release of non-farm payroll (NFP).

U.S stocks are set to open unchanged.

Indices: Stoxx600 -0.3% at 389.3, FTSE +0.1% at 7477, DAX -0.2% at 12940, CAC-40 -0.1% at 5359, IBEX-35 +0.4% at 10005, FTSE MIB -0.1% at 22429, SMI -0.3% at 9254, S&P 500 Futures flat

2. Oil steady as talk of new OPEC deal balances U.S exports, gold unchanged

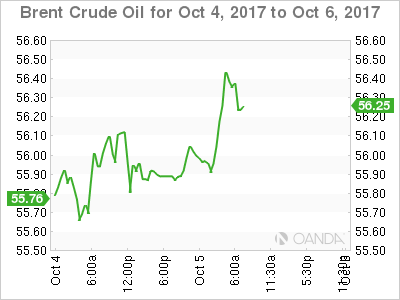

Oil prices are steady on expectations that Saudi Arabia and Russia would extend production cuts, although record U.S exports and the return of supply from a Libyan oilfield are dragging on the market.

Brent crude is up +20c at +$56.00 a barrel, while U.S light crude (WTI) is unchanged at +$49.98.

Note: Both crude benchmarks have fallen more than -5% over the last week as investors booked profits after almost three months of gains.

The Energy Information Administration (EIA) said yesterday that U.S crude oil exports jumped to +1.98m bpd last week, surpassing the +1.5m bpd record set last week.

Ahead of the open, gold is holding steady within a tight trading range as the ‘mighty' dollar holds firm on stronger U.S services sector growth data Wednesday, as investors wait for tomorrow's key U.S employment data. Spot gold is at +$1,274.11 an ounce.

3. Sovereign yields remain atop lofty heights

Firming expectations that the Fed will hike rates in December coupled with domestic data pointing to steady growth in the U.S and talk of a potentially more ‘hawkish' successor to Fed Chair Janet Yellen is helping to support higher U.S yields.

Ten-year yields are trading atop of +2.33%; it's highest yield since mid-July, which has also pushed the dollar higher against G10 currencies. Elsewhere, Germany's 10-year yield gained +1 bps to +0.46%, the highest in a week, while

Spain's 10-year yield climbed less than +1 bps to +1.789%, the highest in more than six months.

Note: The volatility of Spanish government bonds is to become stronger; with yields potentially rising further versus its regional peers (Italian BTP yields) if the standoff between Catalonia's regional government and the central government escalates.

4. Dollar trades in a tight range

Sterling (£1.3190) is trading close to its three-week low on reports that over two dozen U.K members of parliament are prepared to call for PM May to resign before the end of 2017. With the Tory party conference concluded; the market focus has swung back to Brexit and the negotiations. Germany's BDI Industry Association noted that it had concern at current Brexit talks and added that German companies with presence in U.K must make provision for the possibility of a hard Brexit

The EUR (€1.1766) trades steady despite the Spanish region of Catalonia threatening to declare independence next week. Should Catalonia turn independent, the E.U would have to apply the ‘Prodi doctrine' from 2004, suggesting Catalonia would leave the E.U and the Eurozone.

Down-under, AUD is trading atop of its two-month low outright (A$0.7820) after last nights Aussie retail sales headline missed market expectations -0.6% vs. +0.3% m/m.

5. U.K new car registrations slides in September

U.K. new car registrations fell sharply in the key month of September for the first time in six-years. New registrations fell -9.3% to +426,170 units. September is a key month of the year, which normally accounts for up to +20% of annual demand, making it highly likely sales this year will be down for the first time since 2011.

Business and political uncertainty is reducing buyer confidence, with consumers and businesses more likely to delay big ticket purchases.

The figures show a fall in registrations of petrol vehicles of -1.2%, with diesel declining by -21.7%, while demand for alternatively fuelled vehicles was up +41%. Year-to-date, new car registrations have fallen -3.9%.

Catalan Independence Threat Shaking Investors | US NFP And Trump Pick Under Focus

Traders are mindful of Catalonian Independence news could hit the newswire anytime

The US ADP data is always parsed for hints about the upcoming US NFP number

European markets and US futures are trading lower as investors are caught on Catalan independence situation. Even though Catalan President Carlos Puigdemont didn’t announce independence last night, which was widely expected of him, traders are mindful of the fact that the announcement could hit the newswire anytime. This datum is triggering the sell-off in the market. As long as the guessing game carries on, we expect the Spanish equity market to remain under pressure.

Over in the US, the US ADP data is always parsed for hints about the upcoming US NFP number (due tomorrow). There is a correlation between the ADP and NFP but not a strong one. Traders usually take their clues from the ADP number. The impact of the hurricanes was prominent. Companies employed the least number of workers (135K) in a year. Back in 2005, Hurricane Katrina had an even worse influence on the ADP number as it was pushed into the negative territory. Similarly, Hurricane Sandy wasn’t pleasing either as the ADP printed 130K in November 2012, which was below from the three month average of 189K.

We expect the US non-farm to yield a number which could be below the consensus forecast of 60K. Small businesses have felt the most influence of destruction caused by Irma which hit Florida in September. However, past experience explains that this negative impact does fade away fairly quickly and the evidence of this can be seen in the auto sales number which has experienced a sharp rise. We expect developers to hire more workers to construct and rebuild the impacted areas.

The dollar rally is dependent on two things; the economic data and Trump’s pick for the next Fed chair. Despite the blowout ISM non-manufacturing number yesterday, the dollar index hasn’t exploded and this tells us that the economic data isn’t providing the kind of tail which helped the dollar rally. So, it must be Trump’s pick for the next Fed chair. It is almost given that how the market could perceive each candidate depends on who becomes the next Fed chairperson. Kevin Warsh is perceived as the most hawkish person amid other candidates which would trigger flattening treasury yield and aggressive rate hikes. Yellen coming back would keep the volatility suppressed.